Original title: 'The rush to buy' becomes consensus, long-term ETH market value will surpass BTC

Author: Trend Research

Reprinted from: White55, Mars Finance

Since ETH entered this round of rising cycle, every short-term fluctuation adjustment has led the market to start spreading data about ETH unstaking. However, from the supply-demand perspective, the demand generated by institutional consensus far exceeds the supply from unstaking, and we believe that a long-term loaded unstaking situation is not sustainable. Since treasury companies represented by SharpLink began purchasing, U.S. companies holding ETH have accumulated nearly $20 billion worth of ETH, accounting for 3.39% of the total supply, with Bitmine still 75% away from achieving the goal of holding 5% of ETH. With the further implementation of crypto-friendly policies and Wall Street forming a consensus on ETH's long-term value, the 'rush to buy' ETH has only just begun. As the interest rate cut cycle approaches, we adjust our long-term ETH target price upward, believing that ETH's market value will surpass BTC in 1-2 bull-bear cycles.

1. Unstaking data

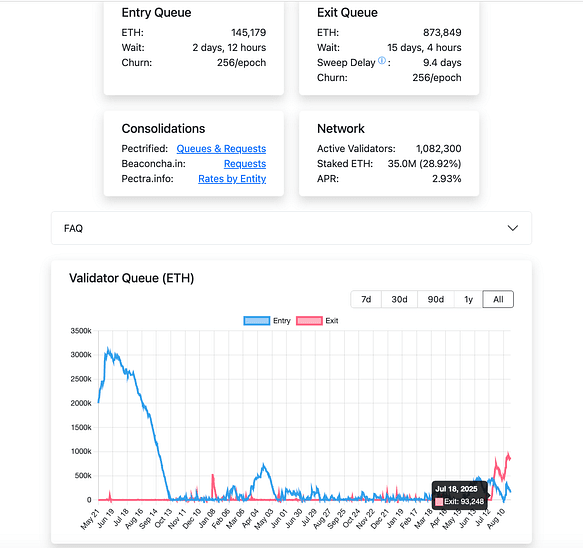

Since the Ethereum Pectra (Prague + Electra) mainnet upgrade took effect in May 2025, the theoretical exit rate for staking is capped at 256 ETH/epoch (1 epoch ≈ 6.4 minutes). In daily terms, the theoretical limit is 256 × (1440 ÷ 6.4) = 256 × 225 = 57,600 ETH/day.

Since July 18, the unstaking situation in the ETH mainnet has been in a fully loaded queue state, with 873,849 ETH currently waiting to be unstaked, requiring 15 days and 4 hours to digest.

The weekly amount of ETH unstaked has a limit, with a maximum of 403,200 ETH (57,600*7), while last week treasury companies purchased 531,400 ETH. Even if 100% of the unstaked portion enters circulation, it can be fully absorbed under the continued buying state of treasury companies. We believe that the current network value of ETH has not been fully recognized by the market, and the unstaked ETH does not completely enter circulation. With further consensus formation, the loaded state of unstaking will improve.

The weekly amount of ETH unstaked has a limit, with a maximum of 403,200 ETH (57,600*7), while last week treasury companies purchased 531,400 ETH. Even if 100% of the unstaked portion enters circulation, it can be fully absorbed under the continued buying state of treasury companies. We believe that the current network value of ETH has not been fully recognized by the market, and the unstaked ETH does not completely enter circulation. With further consensus formation, the loaded state of unstaking will improve.

In simple terms, unstaking does not represent the complete supply situation in the market. Although the total amount of unstaking shows a certain negative correlation with the rise in ETH prices, we believe that this portion of supply will not dominate ETH's transition from rising to falling.

2. Demand analysis for treasury companies and ETFs

Since June 2025, when ETH treasury companies represented by SharpLink entered the market, it confirmed our previous speculation that the U.S. would prioritize ETH as the primary infrastructure for financial on-chaining (see our articles published on June 11 and July 3, titled 'Ahead of the Surge: Why We Are Optimistic about ETH' and 'Storm Clouds Gathering: The Market Forces Will Propel ETH to Value Discovery'). The entry of institutional-level purchasing power represented by treasury companies fundamentally changed the dominant forces behind ETH price fluctuations.

1. The operational logic of treasury companies - accumulating coins leads to a premium

1. The operational logic of treasury companies - accumulating coins leads to a premium

The market premium (MNAV) of cryptocurrency treasury companies comes from investors' recognition of the growth potential of their purchased assets. DAT companies increase their crypto assets through financing (stock issuance or debt), forming a flywheel effect: more crypto assets → balance sheet expansion → stock price increase → more financing capability → further accumulation. This cycle amplifies the market's optimistic expectations for coin-holding stocks, driving MNAV premiums. This flywheel effect is evidenced by the success of MicroStrategy, while ETH has some characteristics that make it more suitable as treasury assets compared to BTC.

2. How treasury companies differ - assets come with earnings

Unlike the limited asset scarcity of BTC, ETH, as the largest DeFi network in the crypto world, will naturally generate returns through large-scale holding.

(1) Staking returns: Ethereum transitioned to a PoS mechanism after the 'Merge' in 2022, endowing ETH with income-generating asset properties, while its ecosystem supports high-yield activities like DeFi and RWA. These characteristics provide DAT with a stable cash flow source, forming the basis for 'cash flow premium'. As of August 2025, the total amount staked in Ethereum reached 36 million ETH, accounting for 30% of the total supply, with an average annualized yield of about 2.95% (actual yield around 1.5%-2.15%). A 1.5% risk-free return is similar to the cash flow of traditional bonds.

(2) Liquidity returns: Additional returns can be obtained by providing liquidity through DeFi protocols within the Ethereum ecosystem. In 2025, the TVL of Ethereum DeFi protocols is expected to be around $120 billion, with annualized liquidity mining yields typically between 2-10%. Assuming that coin-holding stocks provide liquidity through DeFi protocols, a conservative estimate would yield an annualized return of 3.5%. Combining staking returns (1.5%) and liquidity returns (3.5%), coin-holding stocks can achieve approximately 5% annualized cash flow returns. Using a discounted cash flow (DCF) model, assuming a discount rate of 5%, the cash flow premium is 1 times MNAV, meaning the total MNAV multiple is 2 times.

(3) Other premiums: Ethereum's EIP-1559 mechanism gives ETH potential deflationary characteristics by burning base transaction fees. In 2025, Ethereum is expected to net issue 730,000 ETH (annual inflation rate of about 0.6%), but with network burn. If ETH achieves net deflation in the future, its price may only rise and amplify the cash flow returns of coin-holding stocks, indirectly boosting MNAV premiums.

3. The buying power of treasury companies has just begun.

With the higher buying costs of BMNR and SBET's ETH treasury companies and ample backhand, the overall buying power of traditional finance is still in its initial stages. According to data summarized by Yujin, BitMine (BMNR) started reserving 1,523,373 ETH on July 9, costing $5.68 billion at an average price of $3,730, while SharpLink (SBET) started reserving 740,760 ETH on June 13, costing $2.57 billion at an average price of $3,478, also including 1,388 ETH rewards obtained through staking. As Ethereum prices continue to rise, these companies' holding costs will also increase.

From the perspective of future financing capabilities:

From the perspective of future financing capabilities:

BMNR: According to the Prospectus Supplement released on August 12, 2025, BMNR has increased its total ATM amount to $24.5 billion, and it is estimated to have raised about $4.45 billion through the ATM mechanism, holding approximately 1.52 million ETH, with about $18-$20 billion still available theoretically. If ETH is priced at $4,700 each, BMNR could potentially increase its holdings by about 4.26 million ETH, bringing its total potential holdings close to 5.78 million ETH, nearing the target of holding 5% of the total.

SBET: SharpLink has rapidly accumulated about 740,760 ETH since launching its ETH treasury strategy in June 2025 through ATM financing (approximately $1.2 billion) and registered direct sales. Its ATM limit has been adjusted from the initial amount to a maximum of $6 billion, and in addition, it is expected to raise about $600 million through targeted issuance. Assuming all financing is used to purchase ETH, based on ETH costs, the remaining ATM balance is expected to purchase 851,000 ETH.

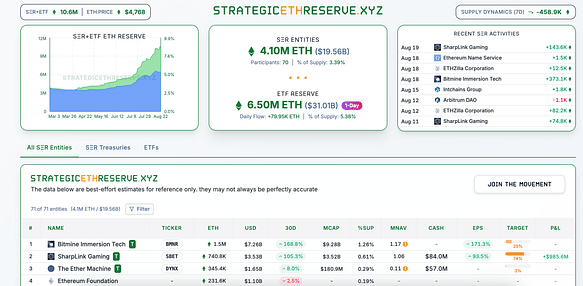

Currently, U.S. companies holding ETH have accumulated nearly $20 billion worth of ETH, accounting for 3.39% of the total supply, with Bitmine still 75% away from achieving the goal of holding 5% of ETH.

Daily ATM available funds:

MicroStrategy is a representative of Bitcoin treasury strategy, with trading volumes showing significant differences in bull and bear markets.

MicroStrategy implemented a Bitcoin treasury strategy in 2020, and during the bull market of 2020-2021, its stock price rose from $13 to a peak of $540, with daily trading volume significantly increasing, but it was heavily influenced by market activity and BTC prices. Based on recent stock prices and average trading volumes, the daily trading volume is estimated to be around $3.5 billion to $7 billion.

During the 2022 bear market, the price of Bitcoin plummeted from $69,000 to $16,000, MicroStrategy's stock price halved, and trading volume significantly shrank, with average daily trading volume dropping to $200 million to $500 million.

Compared to ETH DAT companies, a similar situation may arise:

BitMine's current trading volume has reached $2 billion daily, peaking at $6 billion, nearing or exceeding MicroStrategy's previous bull market peak, attracting significant market attention. Meanwhile, SBET's daily trading volume fluctuates greatly, averaging 50 million shares, with a daily trading volume of about $1 billion. If the market enters a bear market, DAT company's trading volume might shrink to $100 million to $500 million daily, similar to MicroStrategy's performance in 2022. Assuming that 10%-20% of the daily trading volume can be converted to ATM, under the current trading volume, it could raise $2 billion to $4 billion weekly to purchase ETH, expected to last for 3 months.

4. The long-term performance of ETFs remains strong

4. The long-term performance of ETFs remains strong

ETFs, as passive funds that achieve success on a large scale with low costs, have become the preferred choice for traditional large-scale capital allocation. From May 16 to August 15, ETH ETFs recorded 14 consecutive weeks of net inflows, with the highest weekly net inflow of $2.85 billion, and the net asset value accounted for 5.38% of the total supply, with $19.2 billion (68%) of ETH accumulated during the 14 weeks, with an estimated combined buying cost around $3,600.

BlackRock's ETHA is the largest ETF, holding about 2.93% of the tokens, with a current market value of $17.2 billion. Since April 2025, ETHA has been in a net inflow state every week, with net inflows of approximately $8 billion, and the largest single-week net inflow of $2.32 billion.

Currently, the global gold ETF (sum of various ETF/ETP) scale is $386 billion, Bitcoin is $179.5 billion, while Ethereum is only $32.6 billion. If the Ethereum narrative continues, it would require a $140 billion increase in buying power to catch up to the current Bitcoin ETF scale.

Currently, the global gold ETF (sum of various ETF/ETP) scale is $386 billion, Bitcoin is $179.5 billion, while Ethereum is only $32.6 billion. If the Ethereum narrative continues, it would require a $140 billion increase in buying power to catch up to the current Bitcoin ETF scale.

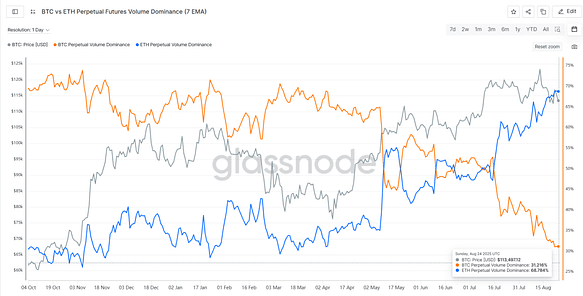

5. Market risk preference shifts from BTC to ETH trading

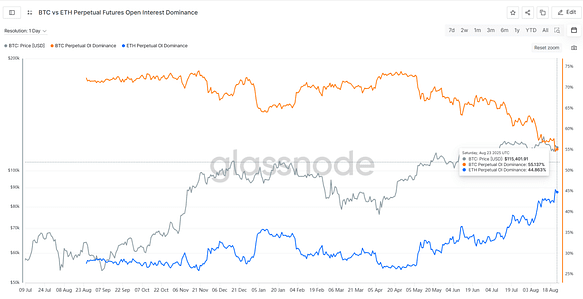

From the perspective of contract positions and trading volumes, BTC has clearly cooled down, with funds concentrating in ETH. At the beginning of May, the BTC contract position accounted for 73%, and now it is only 55%; the ETH position has increased from 27% to 45%.

From the contract trading volume, BTC's trading volume proportion dropped from 61% in early May to 31% currently; ETH's trading volume proportion increased from 35% in early May to 68%, with a continuous increase.

From the contract trading volume, BTC's trading volume proportion dropped from 61% in early May to 31% currently; ETH's trading volume proportion increased from 35% in early May to 68%, with a continuous increase.

From the recent behavior of on-chain whales, there is a notable shift in risk preference as they sell BTC to purchase ETH. According to data from @ai_9684xtpa, since August 20, an ancient BTC whale that had been dormant for 7 years sold part of its BTC and exchanged it for 71,108 ETH (worth about $304 million) at an average cost of about $4284/ETH. The total holding later increased to 105,599 ETH (worth about $495 million). Meanwhile, they built long positions in ETH on Hyperliquid and staked 269,485 ETH (worth $1.25 billion) to the ETH beacon chain on August 25, surpassing the Ethereum Foundation's holdings (231,000 ETH).

From the recent behavior of on-chain whales, there is a notable shift in risk preference as they sell BTC to purchase ETH. According to data from @ai_9684xtpa, since August 20, an ancient BTC whale that had been dormant for 7 years sold part of its BTC and exchanged it for 71,108 ETH (worth about $304 million) at an average cost of about $4284/ETH. The total holding later increased to 105,599 ETH (worth about $495 million). Meanwhile, they built long positions in ETH on Hyperliquid and staked 269,485 ETH (worth $1.25 billion) to the ETH beacon chain on August 25, surpassing the Ethereum Foundation's holdings (231,000 ETH).

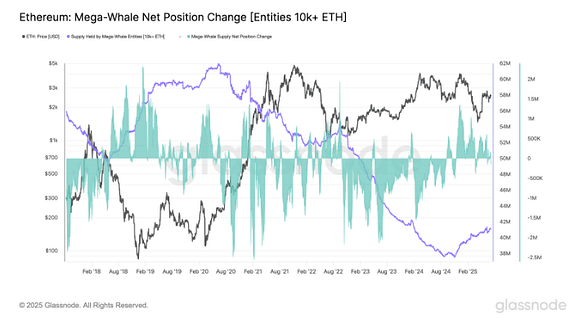

During Q2 2025, on-chain Ethereum whales (wallets holding 10,000 to 100,000 ETH) increased their holdings by 200,000 ETH ($515 million), while super whales (holding over 100,000 ETH) saw their total ETH holdings rebound from a historical low of 37.56 million ETH in October 2024 to over 41.06 million ETH, having increased by 9.31% since October 2024.

3. BTC chip structure remains relatively stable

Due to the risk preference shift from BTC to ETH, BTC has recently performed relatively weakly. From the ETF perspective, there has been a significant net outflow; from the on-chain whales' perspective, there has been a large number of whales exchanging BTC for ETH. Based on the four-year cycle experience in the crypto space, this bull market is expected to reach a comparable duration to previous bull markets in another 2-3 months. Thus, market concerns exist: Is BTC about to enter a bear market, and if BTC enters a bear market, how can ETH stand out and maintain an independent upward trend?

We believe that the current fiscal cycle in the U.S. is longer than the cycles during the previous two crypto bull markets, while BTC's chip structure remains relatively stable and is currently in a fluctuation state.

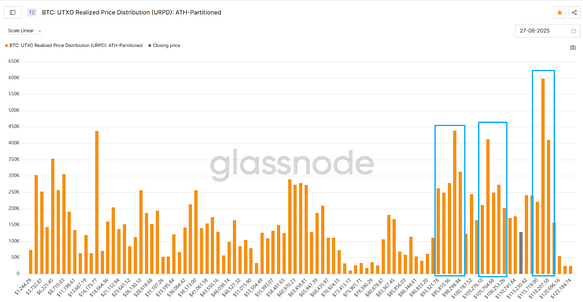

The following chart illustrates the distribution of BTC chip costs, with gray bars representing the current price, and blue boxes indicating the main concentrated chip areas, which are 93K-98K, 103K-108K, and 116K-118K. These three areas have accumulated a massive amount of chips, with a large number of low-cost chips exchanging hands in these ranges, thus forming relatively strong support.

The following chart illustrates the distribution of BTC chip costs, with gray bars representing the current price, and blue boxes indicating the main concentrated chip areas, which are 93K-98K, 103K-108K, and 116K-118K. These three areas have accumulated a massive amount of chips, with a large number of low-cost chips exchanging hands in these ranges, thus forming relatively strong support.

Currently, the chips in the 116K-118K range are in a slight loss state, while the chips in the 93K-98K and 103K-108K ranges are in a profitable state. Although BTC price performance is relatively weak, it has received support around the 11K mark, with two large support areas below, overall remaining in a fluctuation state.

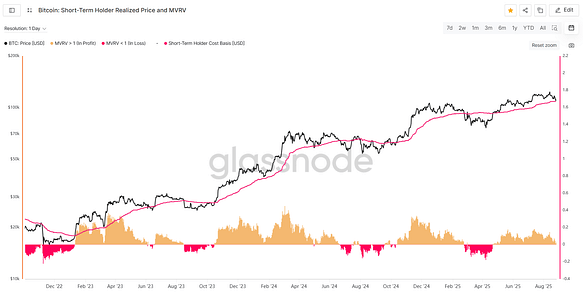

Additionally, the current cost of short-term holders is approximately 108,800. When BTC is above this position, short-term holders remain in profit and will not panic sell. Historically, there have been two rebound instances near the cost line for short-term holders in early 2024, as well as a situation in February 2025 where the first touch of that cost line resulted in a drop. If this cost line is breached, BTC will enter a mid-term adjustment, affecting the overall trend of the crypto industry.

Currently, BTC is at a critical position, having rebounded after touching that cost line yesterday; this week we should closely monitor whether BTC can stabilize at this position.

4. Continuously improving macro environment

4. Continuously improving macro environment

1. Fundamental valuation logic reconstruction under U.S. regulations

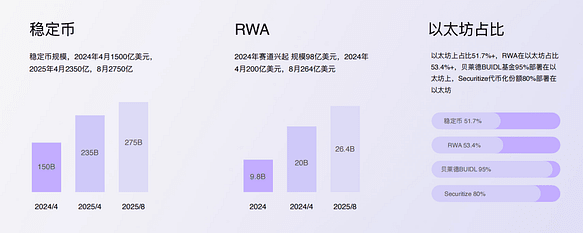

In July 2025, the U.S. GENIUS stablecoin bill was officially legislated. Compared to BTC, stablecoins are pegged 1:1 to the dollar, and their higher capital efficiency makes them more suitable as debt reduction tools. At the same time, stablecoins can drive efficient global capital inflow into the dollar system, support U.S. Treasury purchases, and inject liquidity into on-chain financial assets, promoting the digital expansion of dollar hegemony. Currently, the total market value of stablecoins is $275 billion, while BTC's market value is $2.2 trillion; the estimated global mining value of BTC is $15-$20 billion, and ETH's market value is $550 billion, with staking value of about $165 billion. In the future, whether replacing BTC's role in debt reduction or promoting the on-chain value of assets, or accommodating new payment systems, the scale of stablecoins will accelerate expansion in the long term, quickly growing to a multi-trillion dollar market scale.

As ETH serves as a primary infrastructure for stablecoins and DeFi, its price benefits from ETH purchases driven by network security due to financial on-chain activities, and will also benefit from the endogenous DeFi model: stablecoins inject base liquidity - the DeFi ecosystem uses stablecoins to create leverage and derivatives to purchase more ETH - increased trading activity drives gas fees and facilitates ETH burning. Using the transaction fees (gas fees) and proof of stake (PoS) from the ETH network as cash flow income, a rough valuation calculation using a discounted cash flow (DCF) model shows that under optimistic conditions (7% growth rate, 9% discount rate, leverage factor of 3), ETH's market value has the potential to exceed $3 trillion, surpassing the current BTC market value.

2. The interest rate cut cycle is approaching

On August 22, Powell delivered a speech at the Jackson Hole meeting, stating that inflation remains high, but the downside risks to employment are increasing; against a backdrop of policies still in a 'restrictive' range, the committee will 'proceed cautiously' and will adjust policy positions if necessary. Analysts generally believe that a rate cut in September is almost 'a done deal' and represents a turning point towards a dovish shift. After the speech was released,

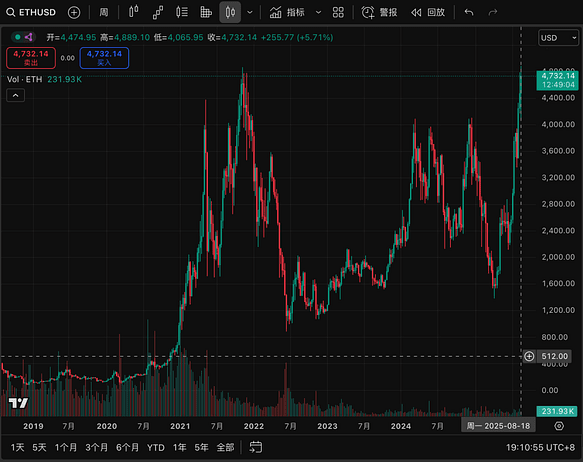

Cryptocurrency-related stocks and ETH-related assets surged dramatically, with ETH recovering all its losses from the beginning of the week and soaring to a historic high of 4887.

During past interest rate cut cycles, ETH has generally outperformed BTC. With Congress returning from recess in September, the push for crypto policy will accelerate quickly, and the expectations for ETH's financial on-chaining and DeFi prosperity have yet to materialize, providing a positive macro environment for ETH's market.

During past interest rate cut cycles, ETH has generally outperformed BTC. With Congress returning from recess in September, the push for crypto policy will accelerate quickly, and the expectations for ETH's financial on-chaining and DeFi prosperity have yet to materialize, providing a positive macro environment for ETH's market.

3. Preferred development of stablecoins and RWA

The U.S. government and financial institutions are consistently pushing the financial on-chain agenda. Currently, the scale of stablecoins is $275 billion, RWA scale is $26.4 billion, with over 50% of stablecoins operating on the Ethereum network, and RWA accounting for 53.4% on Ethereum. The total TVL of DeFi is $161.1 billion, with over 60% deployed on ETH. BlackRock's BUIDL fund has 95% deployed on Ethereum, and Securitize's tokenized shares have 80% deployed on Ethereum.

In this article, we tracked and analyzed some quantitatively clear and large-scale data. Overall, the recent supply-side unstaking data will not alter the upward trend of ETH, and the foreseeable upper limit of demand from treasury companies and new ETF buying is far from being reached, with high build-up costs. With the fundamental shift in financial logic under U.S. regulations, ETH simultaneously possesses characteristics of internally and externally driven growth, pushing prices higher. As the macro environment improves and policies further develop, the long-term market value of ETH is expected to surpass BTC.

In this article, we tracked and analyzed some quantitatively clear and large-scale data. Overall, the recent supply-side unstaking data will not alter the upward trend of ETH, and the foreseeable upper limit of demand from treasury companies and new ETF buying is far from being reached, with high build-up costs. With the fundamental shift in financial logic under U.S. regulations, ETH simultaneously possesses characteristics of internally and externally driven growth, pushing prices higher. As the macro environment improves and policies further develop, the long-term market value of ETH is expected to surpass BTC.