Written by: arndxt

Compiled by: Luffy, Foresight News

Every cycle has its unique narrative, and currently, the market is struggling with contradictory chapters: Bitcoin's seasonal patterns versus post-halving dynamics, the Federal Reserve's dovish statements versus inflation, and the steepening of the bond market that may signal relief or recession.

We are in a market of extreme volatility:

In the short term: Bitcoin may experience volatility that has not occurred this year in September. For those willing to downplay seasonal patterns in halving years, a pullback may be a buying opportunity.

In the medium term: the Federal Reserve's policy faces the risk of credibility damage. Rate cuts caused by rising inflation will change the investment landscape.

In the long term: the key to the cryptocurrency cycle may lie not only in retail or institutional capital flows but also in the structural health of corporate cryptocurrency treasuries. This is a fragile pillar, and if it breaks, demand will turn into supply.

The core logic for investors is simple: we are entering an environment of extreme narrative volatility, where seasonal, policy, and structural mechanisms point in different directions.

In the eyes of investors, signals do not lie in a single data point but in the collisions of these narratives.

Bitcoin's 'September ghost' versus the reality after halving

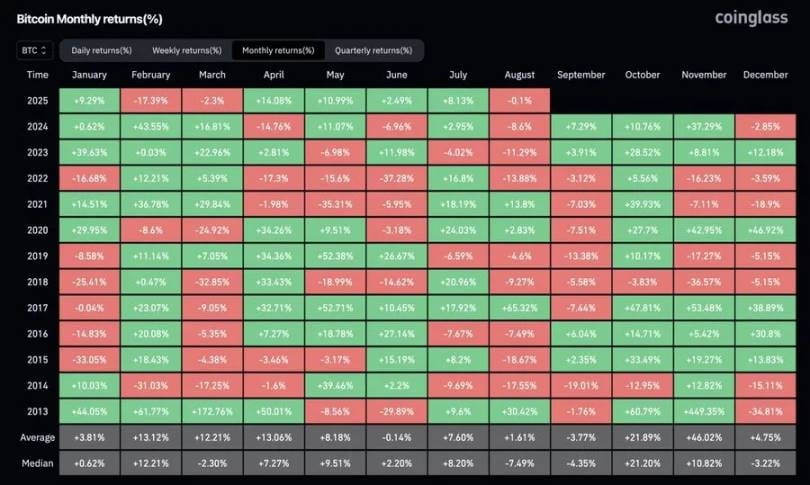

Historically, September is the worst-performing month for Bitcoin. Charts show that declines caused by liquidations of long positions occur repeatedly. But this cycle is different from the past: we are in a halving year, and historically, the third quarter of such years tends to be bullish.

Since 2025, there has not been a single month with gains exceeding 30% (or even 15%), which means volatility has been compressed. In every bull market, explosive rallies tend to concentrate. With four months left this year, the question is not whether volatility will return, but when it will return. The conclusion for investors is that if September sees a pullback, it could become the last significant entry window before the inevitable rise in the fourth quarter.

The narrative split of the Federal Reserve

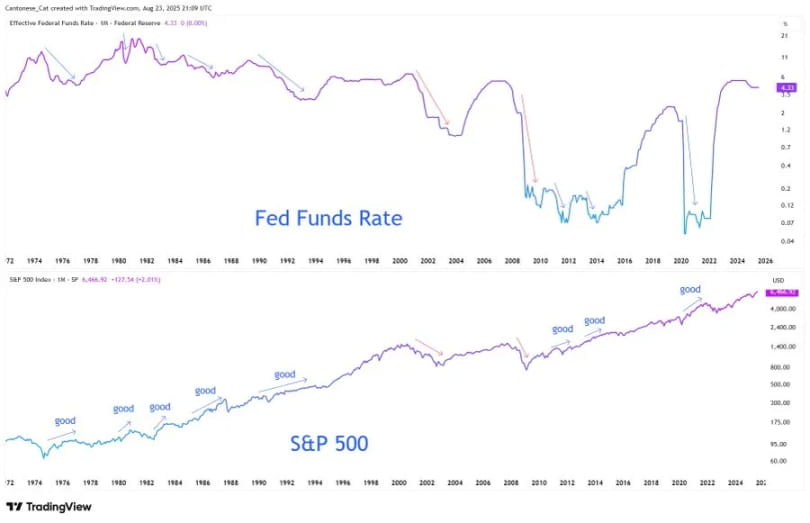

Powell's speech at Jackson Hole was widely misinterpreted as a green light for aggressive easing. In fact, his remarks were more nuanced: he left a door open for a rate cut in September but emphasized that this does not signal the start of an easing cycle.

On the labor market, Powell admitted to a 'strange balance': both labor supply and demand are slowing, leaving the market in a fragile state. The risks are asymmetric; if this balance is broken, it could rapidly explode in the form of layoffs.

On inflation, he spoke frankly: tariffs have obviously pushed up prices, and the impact will continue to accumulate. Although Powell called this a 'one-time change in price level', he emphasized that the Federal Reserve cannot allow inflation expectations to get out of control.

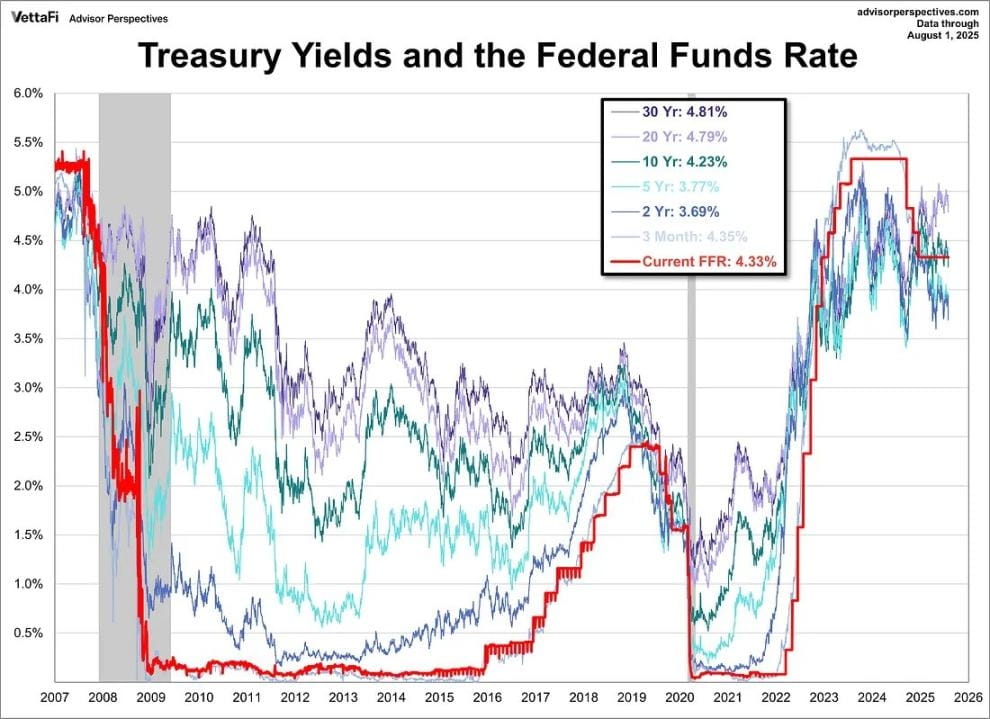

The shift in framework is more enlightening. The Federal Reserve officially abandoned the 'average inflation targeting' of 2020, returning to the 'balanced path' model of 2012: no longer tolerating inflation above 2%, and no longer focusing solely on the unemployment rate. In other words, even if the market has digested the almost certain interest rate cut, the Federal Reserve is still sending signals of a stricter interpretation of the 2% inflation target.

The contradiction is that the Federal Reserve is preparing to cut rates in a stagflation environment while easing amidst accelerating core inflation and a weak labor market. Why? Because structurally, America's debt burden makes it politically and fiscally unsustainable to 'maintain high rates for a long time'. Powell can talk about credibility, but the system is trapped in a vicious cycle: spending, borrowing, printing money, and repeating.

For investors, the key conclusion is: credibility risk has now become an asset pricing risk. If the 2% target devolves from an 'anchor' to a 'vision', it will reset the valuations of bonds, stocks, and hard assets. In this environment, scarce assets (Bitcoin, Ethereum, gold) become reasonable choices to hedge against dilution risks.

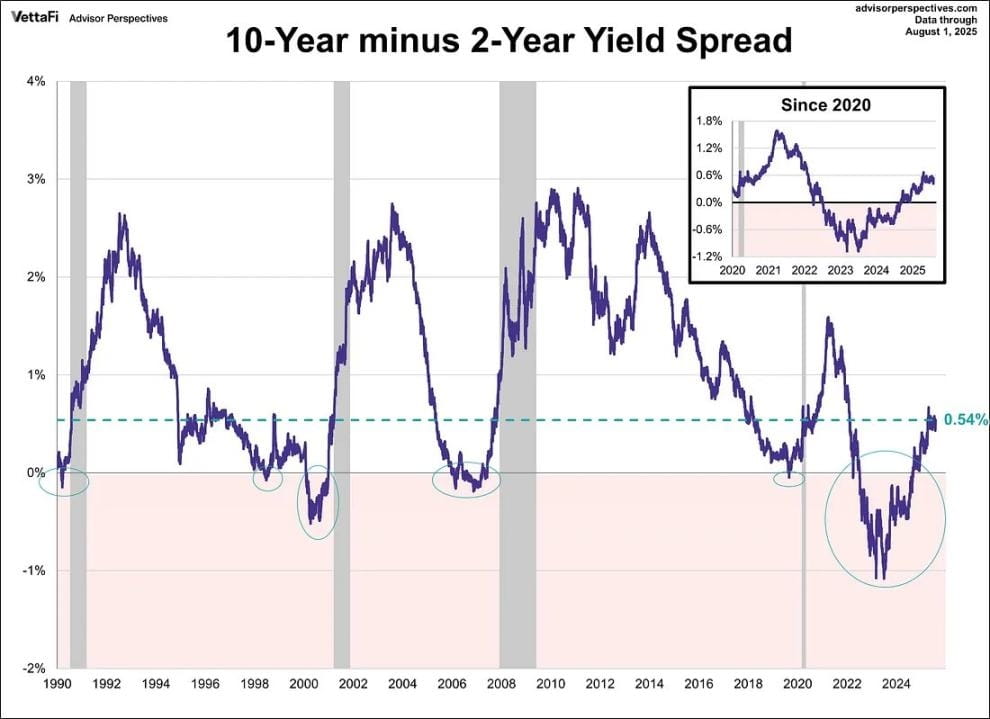

Signal of steepening in the bond market

The yield curve has quietly undone its inversion: the spread between 10-year and 2-year U.S. Treasury yields has rebounded from one of the deepest inversions in history to +54 basis points. On the surface, this looks like normalization; the curve is healthier.

However, history has given different warnings. In 2007, the steepening after the yield curve inversion was not a 'safe signal', but a precursor to collapse. The key lies in the reason for the steepening: if due to improved growth expectations, it is bullish; if due to short-term interest rates falling faster than long-term inflation expectations, it indicates recession risks approaching.

Currently, the yield curve is steepening for the wrong reasons: the market is translating rate cut expectations into sticky inflation. This is a fragile pattern.

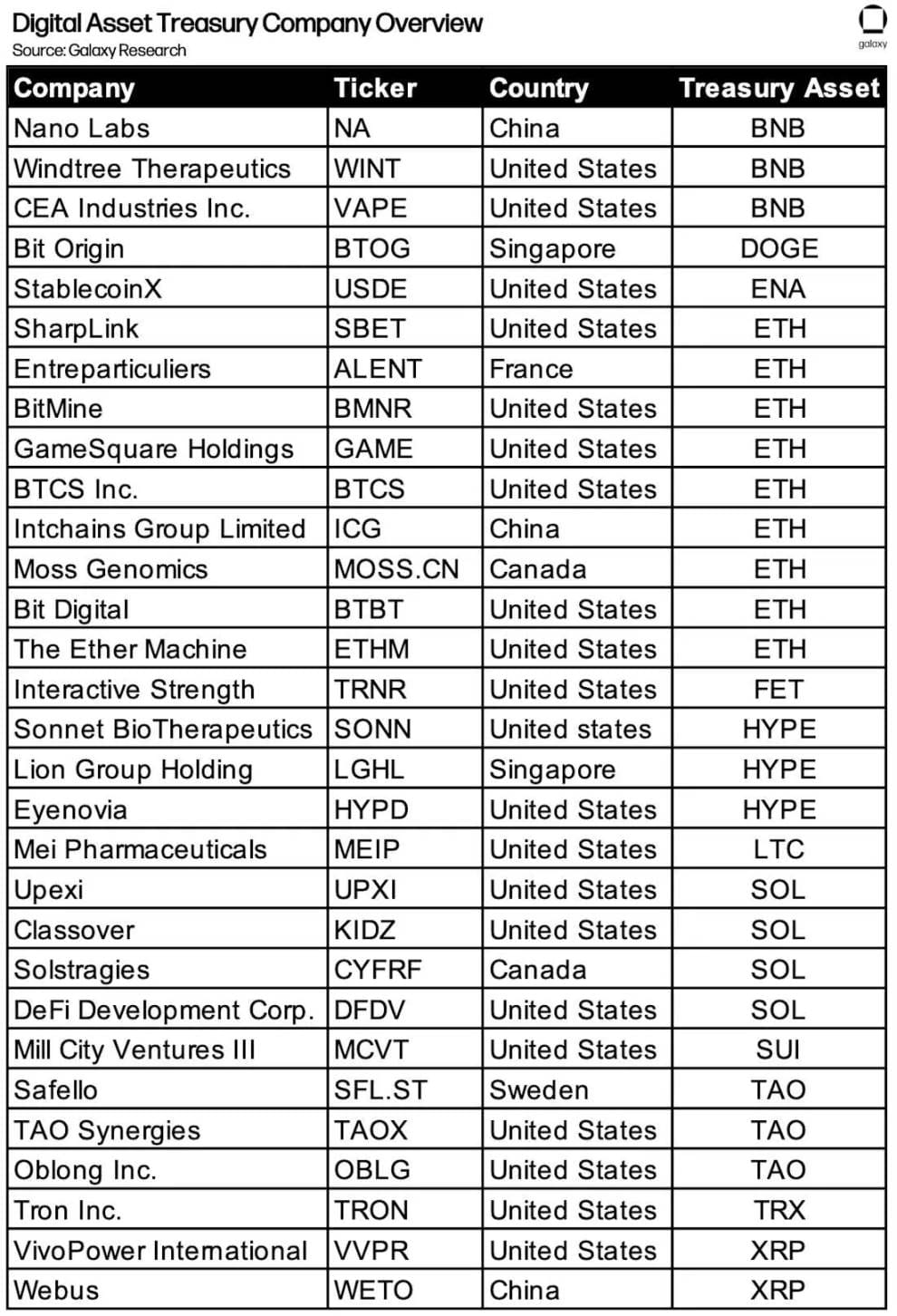

The structural issues of cryptocurrency

In such a macro context, cryptocurrencies face their own survival tests. 'Corporate treasury accumulation' (MSTR, Metaplanet, companies holding ETH, etc.) has always been a core demand pillar. However, as net asset premiums compress, the danger is that these entities may turn to discount, becoming forced sellers.

Cycles do not end because narratives disappear but rather conclude when the mechanisms driving demand reverse. 2017 was ICOs, 2021 was DeFi/NFT leverage, and 2025 could be the limit of cryptocurrency treasury reaching balance sheet arbitrage.

Overall, the core narrative of this cycle is 'disharmony': the market is pulled in opposite directions by seasonal, policy, and structural mechanisms.

Bitcoin's September pullback collides with the inevitable rise after halving;

The Federal Reserve issues cautious statements but is forced to cut rates in a stagflation backdrop;

The steepening in the bond market seems to ease but reveals fragility;

The fuel of cryptocurrency itself—treasury accumulation, faces the risk of turning into liquidation.

For investors, the logic is simple: we are in an era of narrative collisions, and the premium belongs to those who can foresee breakthroughs, hedge against dilution, and view volatility as the only true constant.

The opportunity lies not in choosing a particular narrative but in recognizing that volatility itself is an asset.