Original title: What I Learned from Analyzing 12 Tokenized U.S. Treasuries

Original author: Four Pillars

Original source: https://x.com/

Translation by: Daisy, Mars Finance

Key Points

One of the most actively traded tokenized assets in the RWA market is U.S. government bonds. This is due to their strong liquidity, stability, relatively high yields, increasing institutional participation, and convenient tokenization processes.

The tokenization of U.S. government bonds does not involve special legal mechanisms; its implementation method is for transfer agents managing the official shareholder register to use blockchain to replace traditional internal databases for operations.

This article proposes three major analytical frameworks to study mainstream U.S. government bond tokens: first is the token overview, including protocol summaries, issuance scale, number of holders, and management fees; second is the regulatory framework and issuance structure; and finally, the on-chain application scenarios.

As digital securities, U.S. government bond tokens must comply with securities laws and related regulatory requirements, which significantly impact issuance scale, number of holders, on-chain application scenarios, and more. This article explores how these seemingly unrelated factors interact in a dynamic mechanism.

Finally, it should be noted that, contrary to popular belief, U.S. government bond tokens face numerous restrictions. The final chapter will provide unique insights into these constraints.

1. Everything can be tokenized.

"Every stock, every bond, every fund, every asset can be tokenized." — Larry Fink, CEO of BlackRock

Since the passage of the U.S. (GENIUS Act), global attention on stablecoins has surged, and South Korea is no exception. But is stablecoin really the ultimate destination?

As the name suggests, stablecoins are public chain tokens anchored to fiat currencies. They are essentially still money and must find application scenarios. As stated in the stablecoin research report released jointly by Hashed Open Research and 4Pillars, stablecoins can be applied in various fields such as remittances, payments, and settlements. However, the most discussed and potentially liberating area for stablecoins is RWA (Real World Assets).

RWA refers to Real World Assets, indicating all tangible assets represented in digital token form on the blockchain. However, in the blockchain realm, RWA typically refers specifically to traditional financial assets such as commodities, stocks, bonds, and real estate.

Why can RWA become the next focus after stablecoins? Because blockchain not only has the potential to change the form of currency but may also completely revolutionize the backend system of traditional financial markets.

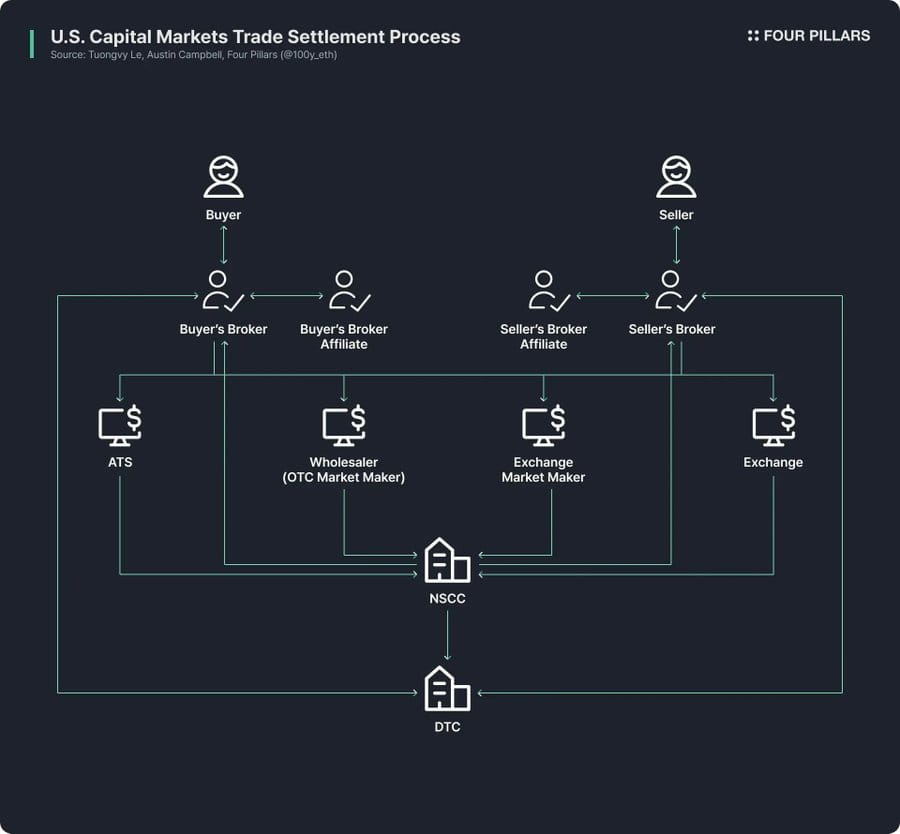

Today's traditional financial markets still rely on highly outdated infrastructure. While fintech companies have improved retail experiences by enhancing the accessibility of financial products and securities, the backend trading systems remain extremely backward.

Taking the U.S. securities market as an example—this venue for trading stocks and bonds has its current framework established in the 1970s to address the "paperwork crisis" of the late 1960s. At that time, the (Securities Investor Protection Act) was enacted, amendments to the securities law were implemented, and institutions such as the Depository Trust Company (DTC) and National Securities Clearing Corporation (NSCC) were created.

In other words, this complex system has been operating for over fifty years, consistently plagued by issues such as excessive intermediation, settlement delays, lack of transparency, and high regulatory costs.

Blockchain technology can fundamentally revolutionize this outdated market structure, creating a more efficient and transparent system. Upgrading the backend of the financial market with blockchain will enable instant settlement, programmable finance through smart contracts, direct ownership without intermediaries, enhanced transparency, reduced costs, and support for fragmented investments.

Because of this transformative potential, many public institutions, financial institutions, and enterprises are actively promoting the tokenization of financial assets on the blockchain.

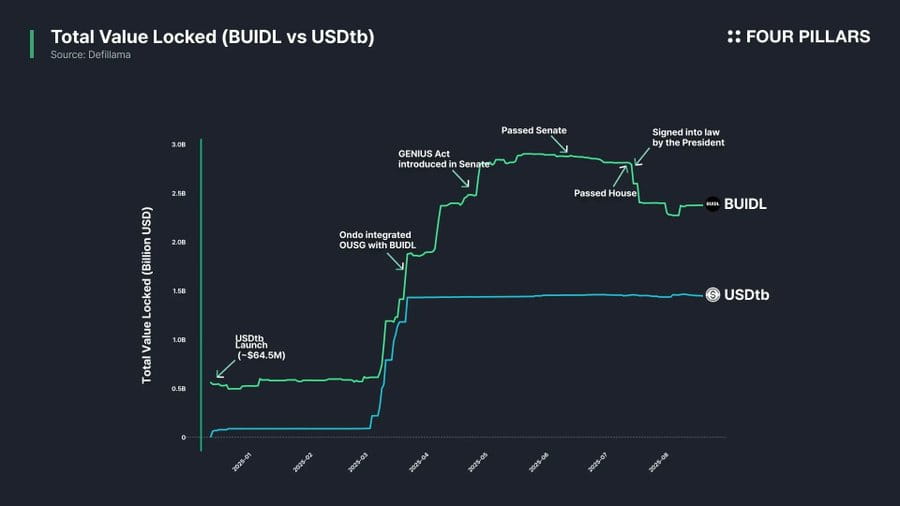

For example, Robinhood announced plans to support stock trading through a self-built blockchain network and submitted a proposal to the SEC to establish a federal regulatory framework for RWA tokenization; BlackRock collaborated with Securitize to issue a tokenized money market fund BUIDL worth $2.4 billion. Former SEC chairman Paul Atkins publicly expressed support for stock tokens, and the agency's internal crypto working group is institutionalizing periodic meetings and roundtable discussions related to RWA.

Source: rwa.xyz

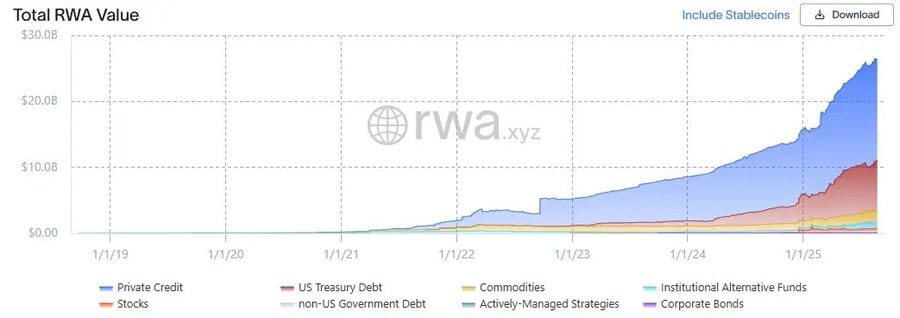

Beyond market speculation, the RWA market is expanding at an astonishing pace. As of August 23, 2025, the total issuance of RWA has reached $26.5 billion, reflecting growth rates of 112%, 253%, and 783% compared to one year ago, two years ago, and three years ago, respectively. Although the types of tokenized financial assets are diverse, the fastest-growing areas are U.S. government bonds and private credit, followed by commodities, institutional funds, and equity assets.

2. U.S. Government Bonds

Source: rwa.xyz

The most active sector for tokenization in the RWA market is undoubtedly U.S. government bonds. As of August 23, 2025, the U.S. bond RWA market size is approximately $7.4 billion, achieving a 370% explosive growth over the past year.

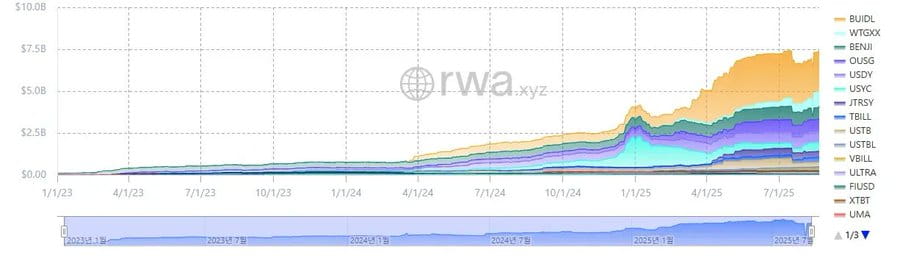

It is worth noting that global traditional financial institutions and DeFi platforms are actively positioning themselves in this field. BlackRock's BUIDL fund leads the market with approximately $2.4 billion in assets, while DeFi protocols like Ondo have launched OUSG funds based on bond-collateralized RWA tokens like BUIDL and WTGXX, maintaining approximately $700 million in management scale.

Why have U.S. government bonds become the most active and largest sector for tokenization in the RWA market? The reasons can be summarized as follows:

Absolute liquidity and stability: U.S. Treasuries possess the deepest liquidity globally and are regarded as safe assets with almost zero default risk, enjoying a very high level of market trust;

Global accessibility: Tokenization technology has enhanced the availability of U.S. Treasuries, allowing overseas investors with demand to invest more conveniently;

Increased institutional participation: Major institutions like BlackRock, Franklin Templeton, and WisdomTree are leading the market by launching tokenized money market funds and Treasury products, providing credit endorsement for investors;

Profitability advantage: U.S. Treasuries provide stable and relatively high yields, currently averaging around 4%;

Feasibility of tokenization: Although there is currently a lack of a dedicated regulatory framework for the tokenization of U.S. Treasuries, basic tokenization operations can already be achieved under existing regulations.

3. U.S. Treasury Tokenization Process

How exactly does U.S. Treasury achieve on-chain tokenization? On the surface, it seems to require complex legal and regulatory mechanisms, but in reality, its tokenization process is remarkably simple under the premise of complying with existing securities laws (Note: As issuance structures vary by token, only representative models are discussed here).

Before explaining the specific process, it is important to clarify a key concept: the so-called "RWA tokens based on U.S. Treasury bonds" in the current market do not directly tokenize the bonds themselves but rather tokenize funds or money market funds based on U.S. Treasuries.

According to traditional regulatory requirements, public asset management funds like U.S. Treasury funds must designate a transfer agent registered with the SEC. Such institutions act on behalf of securities issuers to manage investors' fund holding records in financial institutions or service companies, legally bearing the core function of maintaining securities records and ownership, and are responsible for the official custody of fund investor shares.

The tokenization method of U.S. Treasury funds is very straightforward: tokens representing fund shares are issued on-chain, while transfer agents run internal operations based on a blockchain system to manage the official shareholder register. In other words, the database storing shareholder records has only migrated from a proprietary database to the blockchain.

Of course, since the U.S. has not established a clear regulatory framework for RWA, holding tokens does not guarantee 100% legal assurance of fund share ownership. However, in practice, transfer agents manage fund share ownership based on on-chain token ownership. Therefore, in the absence of hacking or unforeseen incidents, token ownership can indirectly guarantee fund share ownership in most cases.

4. Mainstream Protocols and RWA Analysis Standards

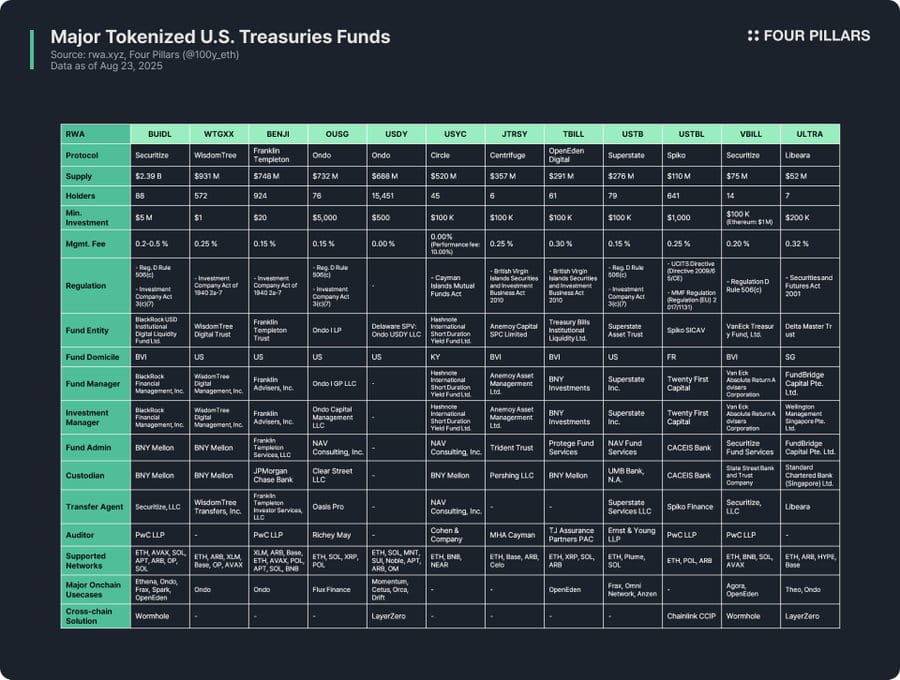

Given that U.S. Treasury funds are the most active tokenized sector in the RWA space, many tokenization protocols have issued related RWA tokens. The table above summarizes the main protocols and tokens, and I will analyze them from three major dimensions:

First is the token overview. This includes background information on the issuance protocol, issuance scale and number of holders, minimum investment amount, and management fees. Due to differences in fund structure, tokenization methods, and on-chain application levels among various issuance protocols, examining the issuer can quickly grasp the core characteristics of the tokens.

The issuance scale is an important indicator for measuring fund size and market heat. The number of holders suggests the fund's legal structure design and on-chain application scenarios—if the number of holders is small, it likely means that according to securities law, investors must be accredited qualified investors or high-net-worth qualified purchasers. It also indicates that, apart from whitelisted addresses, the holding, transfer, or trading of the tokens may be restricted, and due to the small base of holders, the token may be difficult to apply widely in DeFi protocols.

Secondly, the regulatory framework and issuance structure. This section clarifies the regulatory jurisdiction that the underlying fund adheres to and outlines the various entities involved in fund management.

By analyzing 12 types of U.S. Treasury fund RWA tokens, their regulatory frameworks can be roughly categorized as follows (varying based on the fund's registration location and the scope of fundraising):

(Regulation D Rule 506(c) and Investment Company Act Section 3(c)(7)): This is the most widely adopted regulatory combination. Rule 506(c) allows public fundraising from unspecified investors, but all investors must be accredited qualified investors, and the issuer must strictly verify investor qualifications through tax records, asset proof, etc. Section 3(c)(7) allows private funds to be exempt from SEC registration, but requires all investors to be qualified purchasers and the fund to maintain a non-public structure. The dual regulation can expand the investor base while efficiently avoiding registration disclosure and other regulatory burdens. Notably, as long as the requirements are met, this framework applies not only to U.S. funds but also to foreign funds. Representative funds include BUIDL, OUSG, USTB, and VBILL.

(Investment Company Act Rule 2a-7): This regulatory framework is for money market funds registered with the SEC, requiring them to maintain stable net asset values, invest only in ultra-short-term high-credit instruments, and ensure high liquidity. Unlike the previous framework, it allows public investors to participate, thus the minimum investment threshold for such fund tokens is lower, enabling ordinary people to participate. Representative funds include WTGXX and BENJI.

(Cayman Islands Mutual Funds Law): Applicable to open-ended mutual funds established in the Cayman Islands with flexible subscription and redemption. U.S. Treasury funds based in the Cayman Islands must comply with this regulation, with the minimum initial investment usually set at over $100,000. The representative fund is USYC.

(British Virgin Islands Securities and Investment Business Act 2010 (Professional Funds)): This is the core law governing all investment funds established or operating in the BVI. Professional funds are classified as open-ended funds targeting professional investors rather than the public, with a minimum investment requirement of $100,000. It is particularly important to note that if a BVI fund wishes to raise funds from U.S. investors, it must also comply with the U.S. (Regulation D Rule 506(c)), and merely conforming to the BVI framework does not allow fundraising from U.S. investors. Representative funds include JTRSY and TBILL.

Other frameworks: Different regulations apply based on the fund's registration location. For example, the Spiko USTBL issued in France adheres to (UCITS Directive (2009/65/EC)) and (Money Market Funds Regulation (EU 2017/1131)); the Libeara ULTRA issued in Singapore follows (Securities and Futures Act 2001).

The fund issuance structure revolves around seven core participants:

Fund entity: A legal entity that pools investor funds, often using U.S. trusts or offshore fund structures like BVI and Cayman.

Fund manager: The entity responsible for establishing the fund and overseeing its operations.

Investment manager: The institution that actually makes investment decisions and manages the portfolio, sometimes overlapping with the fund manager.

Fund administrator: Responsible for accounting, net asset value calculation, investor reporting, and other back-office operations.

Custodian: Responsible for safely holding bonds, cash, and other fund assets.

Transfer agent: Manages the shareholder register, legally recording and safeguarding fund share ownership.

Auditing agency: Accounting firms that conduct independent audits of the fund's accounts and statements, a necessary step for investor protection.

Finally, the on-chain application scenarios. The greatest advantage of tokenizing bond funds lies in the application potential of the on-chain ecosystem. Although compliance requirements and whitelist mechanisms make it difficult for bond fund tokens to be directly used in DeFi, protocols like Ethena and Ondo have already used tokens like BUIDL as collateral to issue stablecoins or included BUIDL in their investment portfolios, indirectly providing exposure to retail users. In fact, BUIDL has rapidly increased its issuance scale by accessing mainstream DeFi protocols, becoming the top bond-type token.

Finally, the on-chain application scenarios. The greatest advantage of tokenizing bond funds lies in the application potential of the on-chain ecosystem. Although compliance requirements and whitelist mechanisms make it difficult for bond fund tokens to be directly used in DeFi, protocols like Ethena and Ondo have already used tokens like BUIDL as collateral to issue stablecoins or included BUIDL in their investment portfolios, indirectly providing exposure to retail users. In fact, BUIDL has rapidly increased its issuance scale by accessing mainstream DeFi protocols, becoming the top bond-type token.

Cross-chain solutions are crucial for realizing on-chain applications. Most bond fund tokens not only issue on a single network but also offer investors more choices through multi-chain issuance. Although bond fund tokens do not require the high liquidity of stablecoins (which they often do not possess), cross-chain solutions still play a key role in enhancing user experience by enabling seamless transfers of bond fund tokens across multiple networks.

5. Insights and Limitations

In the upcoming RWA research report, I will provide a detailed analysis of 12 major U.S. Treasury fund RWA tokens. Here, I will share the core insights and limitations discovered in this research:

On-chain application difficulty: RWA tokens cannot be freely used on-chain simply because they are tokenized. They are fundamentally still digital securities and must adhere to the regulatory framework that funds follow in the real world. Essentially, all bond fund tokens can only be held, transferred, or traded between whitelisted wallets that have completed KYC. This first access barrier makes it extremely difficult for bond fund tokens to be directly used in permissionless DeFi protocols.

Small number of holders: Regulatory barriers have led to a very low number of holders for bond fund tokens. Money market funds targeting retail investors (like WTGXX and BENJI) have relatively more holders, but most funds require investors to be accredited qualified investors, qualified purchasers, or professional investors, significantly limiting the size of the qualified investor group, leading to some funds having holders that struggle to even reach double digits.

On-chain B2B application scenarios: For the aforementioned reasons, there are currently no DeFi application cases for bond fund tokens aimed directly at retail users. Actual adopters are mostly large DeFi protocols—for instance, Omni Network uses Superstate's USTB for its own fund management, while Ethena issues USDe stablecoins collateralized by BUIDL, allowing retail users to benefit indirectly.

Fragmentation of regulations and lack of standards: Bond fund tokens are issued by different national funds under various regulatory frameworks. Although BUIDL, BENJI, TBILL, and USTBL are all bond fund tokens, they follow completely different regulatory systems, leading to significant differences in investor qualifications, minimum investments, and application scenarios. This regulatory fragmentation increases complexity for investors, and the lack of unified standards makes it difficult for DeFi protocols to generalize and integrate bond fund tokens, thus limiting the development of on-chain applications.

Lack of a dedicated regulatory framework for RWA: There is still a lack of a clear regulatory framework for RWA. Although transfer agents do indeed record shareholder registers via blockchain, on-chain token ownership has not yet been legally equated with securities ownership in the real world. Specific regulations are needed to connect on-chain ownership with legal ownership in the real world.

Insufficient application of cross-chain solutions: Although almost all bond fund tokens support multi-network issuance, very few have implemented cross-chain solutions. Further promotion of cross-chain technology is needed to prevent liquidity fragmentation and enhance user experience.

A report detailing the analysis of 12 major bond funds will be released in September, stay tuned.