When you see that mountain of legal terms and disclaimers on an investment prospectus, would you choose to read it carefully from beginning to end? Most people's answer is no, which explains why even portfolio managers at large asset management firms don't have the time to read the prospectus of every bond they purchase.

As investment master Ray Dalio said: "It all comes down to interest rates. As an investor, what you do is pay a total amount for future cash flows." This statement accurately encapsulates the essence of fixed income investing and reveals why market conventions are so important in this field.

Despite the lengthy nature of these prospectuses, each page plays a crucial role in ensuring the efficient operation of the modern fixed income market. These documents have been meticulously constructed over years of legal precedents, fundamentally supported by the implicit and explicit contracts we discussed in the first part.

Take the example of a transaction involving dollar-denominated fixed income Tesla bonds: all parties involved—market makers, buyers, sellers, and issuers—must collectively agree to price the bond relative to the spread convention against the nearest active US Treasury bond, also known as the dollar "risk-free" rate. Regardless of whether the US Treasury yield curve is truly "risk-free" (there have indeed been cases of near-default in recent years), it is the closest level to "risk-free" that any interest rate can achieve.

Why is this the case? Because the US government has the exclusive power to print dollars, any resulting government default would trigger larger, more systemic social issues. Given that the US government should be essentially safer, why take on the risk of Tesla with a lower yield than US government bonds? Or simply put, why worry about the risk of Tesla default in a doomsday scenario where the monetary system supporting the US government fails?

This convention has gained global respect—fixed income instruments denominated in US dollars reference US Treasury yields, while fixed income instruments in other currencies reference their respective government bond yield curves. This standardized practice provides a unified risk assessment benchmark for global investors, greatly reducing the complexity of cross-border investments.

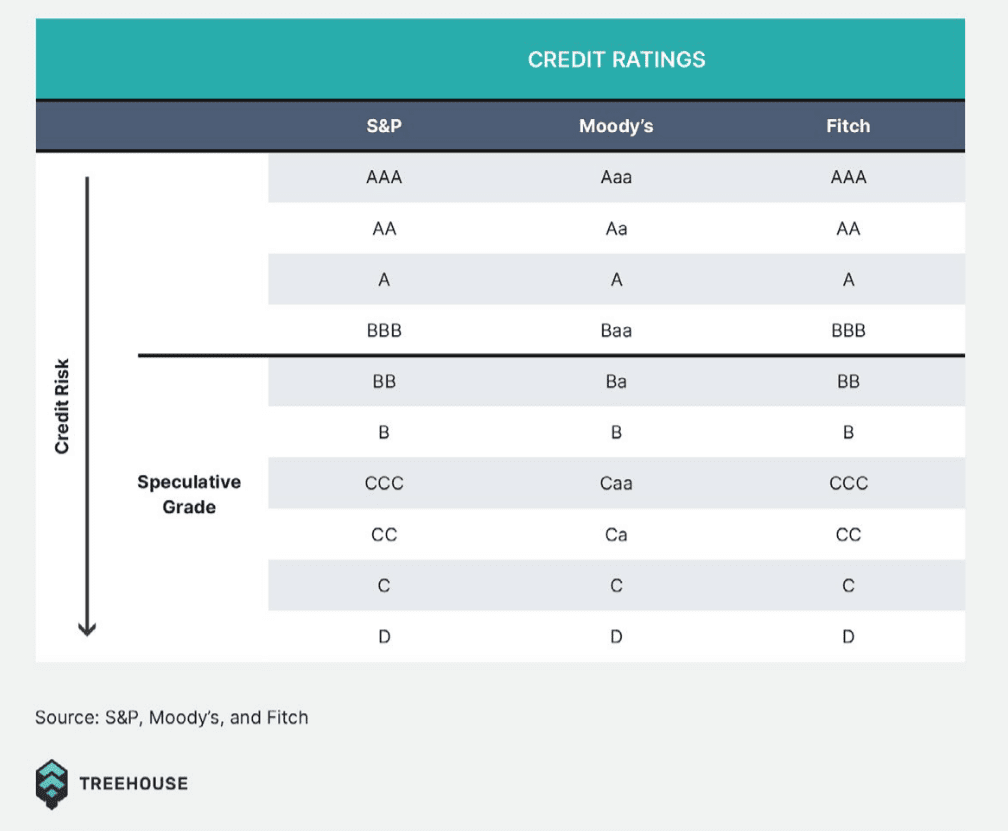

Aside from the "risk-free" rate, using third-party private rating agencies is another widely accepted centralized convention in the fixed income market. Moody's, Standard & Poor's, and Fitch have established themselves as the arbiters of creditworthiness today. As of June 2024, these agencies rated the US government at Moody's Aaa, Fitch's AA+, and S&P Global Ratings' AA+, while Tesla's ratings are lower at Moody's Baa3, Fitch's BBB, and S&P Global Ratings' BBB.

The not-so-secret fact about the market is that rating agencies often react retrospectively to changes in creditworthiness. The subprime mortgage crisis was, to some extent, driven by these agencies exaggerating the ratings of worthless bonds, which was one of the key factors leading to the global financial crisis. Despite these flaws, investors, banks, and funds around the world still heavily rely on these ratings.

Market conventions go far beyond this. The history of fixed income is filled with social and more explicit conventions, from market trading times and quoting practices to minimum tick sizes and mandatory settlement processes. The same principles extend beyond the financial realm—social systems around the world rely on collective trust in conventions to function.

Although these systems are not perfect, as history repeatedly shows, these standards are accepted as carriers of trust because society has recognized the role of standardization in enhancing productivity, efficiency, and convenience—key factors that have allowed the debt capital market to thrive.

In traditional financial markets, the establishment of these conventions often takes decades or even centuries. However, in the digital age, we have the opportunity to rethink and redesign these conventions. The emergence of blockchain technology and smart contracts offers the possibility of establishing more transparent, efficient, and inclusive fixed income market conventions.

Smart contracts can automatically execute complex bond terms without human intervention, significantly reducing operational risks and costs. Decentralized credit assessment mechanisms may challenge the monopoly of traditional rating agencies, providing more objective and real-time risk assessments. These innovations can not only enhance market efficiency but also open the door to fixed income investing for more participants.

As the digital asset ecosystem matures, new market conventions are forming. These conventions will blend the wisdom of traditional finance with the innovation of blockchain technology, creating a fairer, more transparent, and efficient investment environment for investors. In this transformative era, understanding and participating in the establishment of new conventions will be key to seizing future investment opportunities.

#Treehouse and $TREE arose in this context, dedicated to establishing new standards and conventions for the digital asset fixed income market, providing investors with reliable and transparent investment channels.