In mid-August, Ethereum (ETH) strongly broke through $4700, reaching a four-year high; during the same period, Solana (SOL) oscillated mostly between the $180-$200 range, performing far worse than BTC and ETH. Looking back at 2024, Solana was viewed as a strong competitor to ETH due to the Meme frenzy sparked by platforms like Pump.fun, with SOL reaching a historical high of around $293 on January 19, 2025. However, SOL then fell into a retracement and consolidation, with market sentiment fluctuating, contrasting sharply with ETH's 'continued strengthening' trend.

Behind this differentiation are systematic differences in funding entry points, value anchor points, and network narratives. This article will analyze on-chain data and ecological performance on the Solana chain to dissect the core reasons for SOL's phase lagging behind ETH, analyze its advantages and disadvantages for another rise, and forecast potential trends for Q3-Q4 2025.

1. 2025 Solana Ecological Performance Overview

The development path of Solana is starkly different from Ethereum: it does not rely on 'high Gas fees + deflation' to capture value, but instead leverages single-chain high throughput and ultra-low fees to accommodate massive long-tail and high-frequency trading.

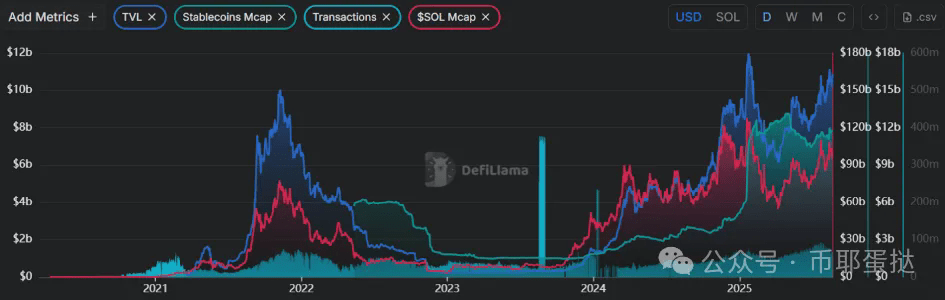

1. Core On-Chain Indicators

Since the beginning of this year, the Solana ecosystem has shown a 'high-level pullback followed by oscillating upward' trend. TVL is about $10.42 billion, with stablecoin market capitalization around $11.62 billion, indicating that the on-chain 'underlying dollar liquidity pool' has returned and stabilized at the $10 billion level; the number of on-chain transactions remains high, with stable activity in high-frequency and long-tail trading; SOL's total market capitalization significantly fell in Q1 but began to show a wave-like oscillating rise from Q2; the resurgence of Meme enthusiasm provides marginal boosts to DEX trading and chain fees, though it has not yet returned to peak levels for the year.

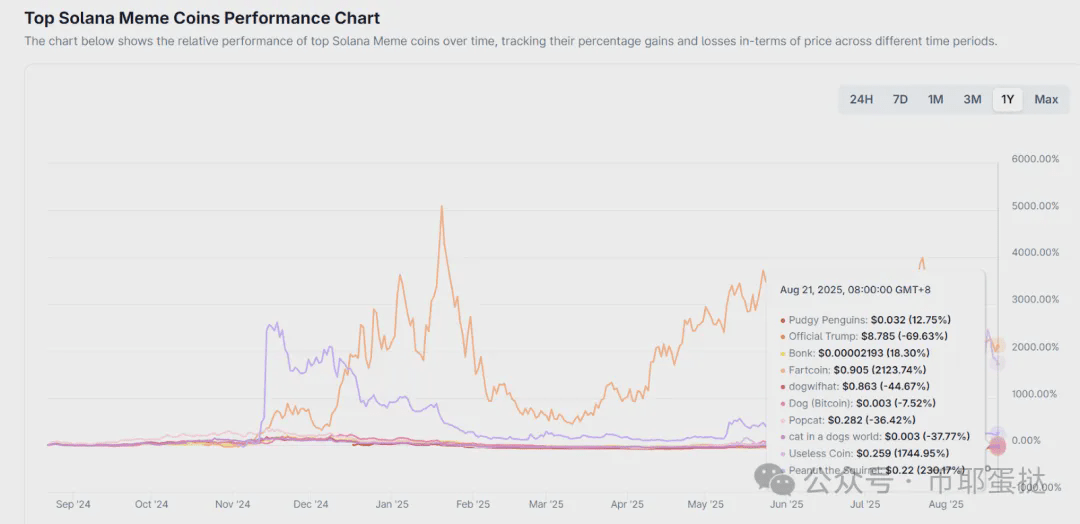

2. Meme Coin Sector

As the core network for Meme coins, Solana has nurtured star tokens like BONK, WIF, and PENGU, with a total sector market capitalization of about $11.7 billion, showing characteristics of 'high volatility + strong rotation + strong event-driven' dynamics. The five most popular Meme coins this year are as follows:

PENGU: A 'brand coin' linked to popular NFT IP, with physical toy sales exceeding $10 million, covering over 3,100 stores; Canary Capital has submitted a PENGU ETF application to the SEC, ranking among the top in Solana Meme coins by market capitalization.

BONK: The 'elder' of Solana's dog-themed Meme coins, relying on community traffic, has gained traction through LetsBonk.fun, but currently shows significant retracement.

TRUMP: An emotion-driven coin on political topics, which has seen oscillating declines since its launch in January, with a brief revival following Trump's crypto dinner in May, currently still in decline, sensitive to event catalysts.

FARTCOIN: Captivating with humorous themes and viral spread, users submit fart jokes or Memes to earn coins, with transactions accompanied by digital fart sounds, combining AI narratives (created by AI Truth Terminal), easily triggering FOMO emotions.

USELESS: Marketed with 'uselessness' as a selling point, satirizing the hollow promises of other tokens, with higher prices accentuating 'uselessness,' attracting speculative capital.

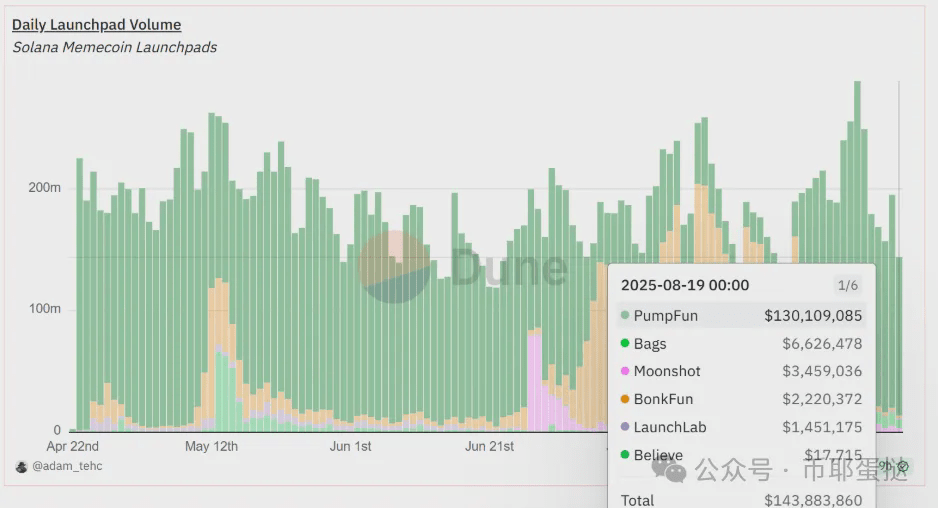

3. Launchpad Sector

Solana Launchpad competition has evolved from 'low price, fast listing' to a struggle for 'creator economy, token buyback, community governance':

Pump.fun: With a 1% trading fee and 'fool-proof issuance' has ignited the entire chain's Meme scene, generating about $13.48 million in revenue in a single week in mid-August, with cumulative revenue exceeding $800 million, having raised market share from 5% to 90% in just two weeks.

LetsBonk.fun: Rapidly rose after its April launch, at one point capturing over 78% of issuance share in July, becoming a core competitor to Pump.fun with 'community mobilization + low-threshold issuance.'

Bags: Focused on 'creator profit sharing/royalties,' binding opinion leaders and creators, with trading volume exceeding $1 billion in the last 30 days.

Moonshot: A fiat-entry-level app supporting Apple Pay direct top-ups and fiat deposits, once topped the US App Store's 'Finance Free Apps' chart, lowering the entry barrier for newcomers.

Believe: A social media entry where 'replying generates coins,' which sparked controversy in June due to suspending some on-chain distributions and shifting to offline payout, later adjusting the automatic listing to 'manual review.'

4. DeFi Sector

Solana DeFi positions itself as 'high-frequency/long-tail trading infrastructure,' with clear division of labor among various platforms:

Raydium: Established DEX/AMM that takes on most long-tail spot liquidity and launch pool functions, with fees and revenue consistently ranking among the top in its category, forming a positive feedback loop of 'platform cash flow — token value.'

Jupiter: Default-tier liquidity aggregator, integrating liquidity from multiple DEXs, with the JPL pool gathering substantial funds, soon to launch a lending sector.

Kamino: Known for 'active market-making treasury + lending,' consistently ranks at the top in Solana TVL, serving as a core 'distribution center' for LPs and funds.

Jito: LST and MEV infrastructure that makes MEV explicit through clients and block engines, allocating part of MEV revenue to stakers via jitoSOL, with Jito tips representing a high proportion of on-chain 'real economic value (REV).'

2. Core Reasons for SOL Lagging Behind ETH

ETH closes the loop of 'compliant funds → secondary liquidity → market-making/derivatives' through spot ETFs, combined with a larger scale of enterprise treasuries and the narrative of 'on-chain financial hub,' forming a stronger capital attraction and valuation anchor; while Solana focuses on a trading-type ecology of 'high-frequency/long-tail applications,' price elasticity relies on the prosperity of themes like Meme and Launchpad, making it easier to 'lose anchor' when risk appetite declines or hotspots rotate.

1. ETF Funding Increment Gap

SOL: Although there is a Solana ETF (SSK) in the US stock market that offers staking rewards, it is complex and not a SEC-registered spot ETF, accumulating only about $150 million in net inflows since its listing. The market is currently focused on the SOL spot ETF applications from VanEck and Grayscale; if approved around October, it could open compliant models and passive capital channels.

ETH: The spot ETF scale has surpassed $22 billion, becoming the main entry point for institutional funds. Leading institutions like BlackRock are pushing for 'stakable ETH ETF' applications, which, once implemented, will combine 'staking rewards' with 'compliant channels,' further solidifying long-term allocations.

2. Differences in Enterprise Holding Sizes

SOL: Known as 'SOL Microstrategy,' Upexi currently has an NAV of about $365 million and holds 1.8 million SOL; although Arthur Hayes has been invited to join the advisory board, the overall company holding size is far less than that of ETH's camp.

ETH: BitMine Immersion (BMNR) positions itself as 'ETH Microstrategy,' planning to increase its fundraising scale to $20 billion, with a current NAV of about $5.3 billion, second only to Bitcoin’s MicroStrategy; it also has endorsements from globally influential opinion leaders like Tom Lee, strengthening market narratives and capital appeal.

3. Differences in Network Narrative Positioning

Solana: Leans towards 'consumer-grade applications + speculative hotspots' (Meme, Launchpad), with multiple attempts this year to enter the RWA field but mostly ending in failure; in August, China Merchants International × DigiFT issued dollar money market fund tokens (CMBMINT) on Solana, a rare compliant RWA case, with SOL surpassing $200 on the same day, seen as a potential narrative switch starting point.

ETH: Building compliant and sustainable on-chain financial infrastructure and settlement layers, receiving 'structural subscriptions' from institutions. Over half of stablecoin issuance, around 30% of Gas fees occur on ETH; Robinhood launched stock tokens on ETH L2, and Coinbase is fully developing Base, further solidifying its position as a financial hub.

4. Different Value Capture Mechanisms

Solana: High interaction density is achieved through low fees and high throughput, with value capture relying on total transaction volume, application layer fees, and MEV; when Meme and long-tail activities decline, chain fees and application fees cool down, leading to a weakening valuation anchor.

ETH: Directly burns base fees through EIP-1559, showing net deflation or low inflation during busy periods, along with staking rewards, forming a solid valuation anchor of 'supply-side contraction + cash flow.'

5. Historical Risks and 'Credibility Discount'

Solana experienced an approximately 5-hour shutdown on February 6, 2024; subsequent phases saw a decline in consensus nodes. Although this has been repaired, it is still regarded as a risk factor by institutions; in contrast, ETH's 'no downtime' feature and broader developer and compliance ecology bring a lower credibility discount, which may be amplified during macro volatility.

3. Can SOL Take Off Again: Analysis of Advantages and Disadvantages

SOL has a foundational profile of 'high activity + low fees + MEV sharing + application layer cash flow,' combined with catalysts like spot ETFs and compliant RWA landing, offering the chance to initiate a new trend; however, in the absence of ETF increments, with treasury scale and narratives weaker than ETH, and lingering shadows of historical stability, prices remain highly 'event-driven.'

1. Advantages and Bullish Logic

High throughput + low fees = Long-tail asset soil: Single chains accommodate millions of daily interactions, with active trading and market-making at low fees, conducive to the continuous testing and diffusion of Meme, long-tail assets, and high-frequency DeFi.

Initial compliance RWA landing: China Merchants International × DigiFT issued dollar money market fund tokens on Solana, bringing 'institutionally interpretable cash-like assets' and fiat/stablecoin entry, expected to form a 'long-term capital narrative.'

Inflation curve is predictable: Initial inflation is 8%, decreasing by 15% every approximately 180 epochs (1 year), stabilizing long-term at 1.5%; actual annualized inflation for 2025 is about 4.3%-4.6%, with the community still discussing proposals to accelerate deflation, beneficial for medium- to long-term valuation.

ETF Approval = Funding Gateway Opens: Institutions like VanEck have submitted or updated SOL spot ETF S-1 filings; if approved, it may replicate ETH's 'compliant funds → passive allocation → market making/derivatives' pathway, attracting institutional treasury entry.

2. Disadvantages and Bearish Logic

ETF increments have yet to materialize: The scale of ETH's spot ETF exceeds $22 billion, forming a closed loop for institutional funds; SOL is still in the application phase, with current US stock products being non-standard spot ETFs, which weakens their capital-raising ability, and the difference between 'already realized' and 'awaiting expectations' is directly reflected in relative returns.

Disparities in treasury and 'spokesperson': The treasury companies in the ETH camp (like BMNR) are far larger than those in the SOL camp (like Upexi), with endorsements from opinion leaders like Tom Lee providing greater support for ETH during market turbulence.

Narrative positioning leans toward 'speculation': ETH occupies the high ground in the financial narrative, while Solana relies on Meme and Launchpad to drive activity and fees, where theme rotation directly affects on-chain yield and price anchors, resulting in weaker stability.

'Low fee' advantage under pressure: ETH mainnet fee rates are declining, and competition from public chains like BSC, Base, and Sui has intensified, making 'low fees' no longer an exclusive selling point for Solana, diverting new developers and funds.

4. Outlook for SOL Trends in Q3-Q4 2025

Solana is essentially a consumer-grade high-frequency chain characterized by 'high activity, low fees, and application monetization.' Whether it can 'take off again' in Q3-Q4 depends largely on whether ETFs can bring compliant increments, whether RWAs can establish scalable closed loops, and whether network stability continues to improve.

Baseline Scenario: Q3 enters a 'trading recovery + narrative waiting' oscillation upward phase. On-chain activity, DEX, and perpetual contract trading remain at high levels, with Meme displaying a cycle of 'pulse activation - pullback - reactivation'; prices oscillate around the 'valuation center raised by fundamentals' and 'event expectation risk premium contraction,' overall biased upward.

Bullish Scenario: If a spot ETF is approved around Q4, coupled with large-scale issuance of RWA (like more government bonds, bills, and fund products), then the three elements of SOL's 'funding gateway, sustainable cash flow, and network resilience' will be strengthened simultaneously, and prices are expected to break previous highs, showing a trend upward.

Bearish Scenario: ETF delays or rejections, Meme/Launchpad decline, and other public chains introducing innovative functions or hotspots may trigger valuation anchor loosening and trading β contraction; if compounded by macro tightening or ETH mainnet/L2 further reducing fees, SOL will enter a 'high volatility downturn - weak rebound' structure.

Conclusion

In 2025, Solana experienced fluctuations in popularity: at the beginning of the year, it shone during the Meme frenzy; by mid-year, it was relatively dim under ETH pressure, with the market wavering on its positioning. However, it is undeniable that Solana's unique value as a high-performance public chain remains prominent, and the ecosystem has not stagnated due to short-term cooling.

In the long run, whether Solana can regain leadership depends on its ability to convert high-speed network advantages into sustained user value: it needs to retain users after speculative enthusiasm fades, expand application boundaries, and gain mainstream capital trust, seizing opportunities in compliance processes. Currently, there are signs of institutional layouts, technological upgrades, and ecological narrative transformations; the current pullback may be a buildup, waiting for the right moment to take off again.