Tonight, Powell delivered his final speech as Chairman of the Federal Reserve in Jackson Hole.

First, the opening line was 'The basic outlook and the changing risk balance may require us to adjust our policy stance'—sending a signal of a rate cut in September—similar to last year's meeting, where his first sentence was 'the time to adjust policy has come.'

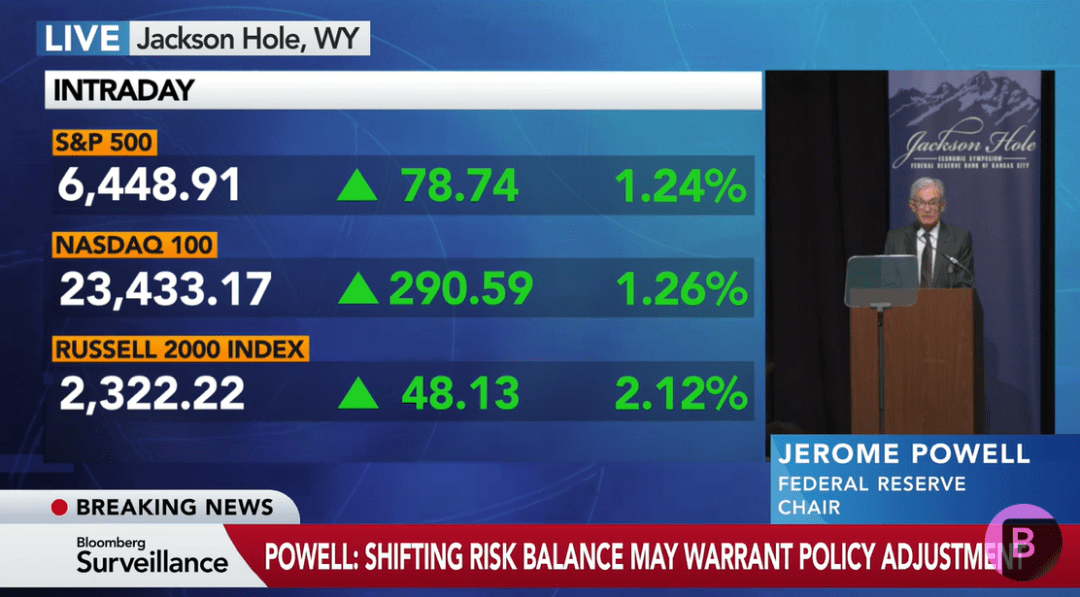

This is no different from a 'loud bang' for the financial markets—no one had expected him to 'decisively signal a rate cut,' and in the stark contrast, the market reacted violently. Gold surged more than $30 instantly, the dollar index dropped 0.5% upon hearing the news, and the three major U.S. stock indices all rose more than 1%. Traders once again fully priced in two rate cuts by the Fed before the end of the year.

Second, other key points from the speech (the speech lasted 23 minutes):

'The reasonable basic situation' is that tariffs lead to a 'one-time' increase in price levels, but these effects need time to fully manifest in the economy (this was his first statement suggesting that the impact of tariffs on inflation would be relatively short-lived).

In the short term, inflation risks lean upward, and employment risks lean downward—this is a challenging situation. When our goals face such significant conflicts, our framework requires us to balance the dual mission (this statement is actually 'reserved opinion,' implying a rate cut, but not wanting the market to feel that the Fed will definitely adopt a path of substantial easing).

Let us proceed with caution (there are no signs of a 50 basis point rate cut).

Monetary policy is not on a preset path; decisions will be made entirely based on the assessment of data and its impact on the economic outlook and risk balance. We will never deviate from this principle (Powell is actually 'leaving room'—on the surface, releasing dovish signals to give the market a direction, but carefully emphasizing 'caution,' 'data dependence,' and 'not a preset path.' He hopes the market sees this as a 'conditional adjustment' rather than a 'declaration of a complete shift').

Although a dovish tone was struck, it was more about 'preparing for fine-tuning' and not meant to be understood as 'immediately starting a rate-cutting cycle.' It is clear that the market was overly optimistic.

Third, although investors got the answers they wanted, this is not a happy ending for Powell—because the stock market has become fervent again, effectively offsetting his efforts over the past year. Last year, he repeatedly mentioned 'higher for longer' out of fear that the market would ease too early, leading to another asset bubble. But today, the market directly took his words as a clarion call for 'a rate cut in September.'

Powell intended to end cautiously, but his curtain call left the market with a 'party signal.'