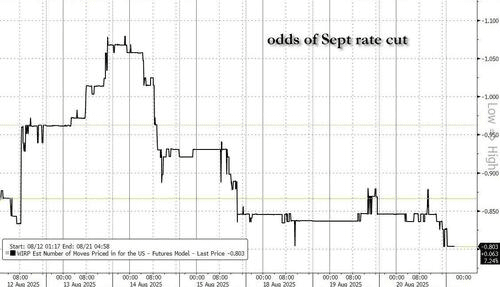

#杰克逊霍尔会议 Market focus is on Powell's views regarding the July non-farm payroll data and whether it opens the door for a rate cut in September. Currently, money market traders expect an 80% probability of a 25 basis point rate cut in September. Several large investment banks expect Powell may partially reverse the flexible average inflation targeting (FAIT) policy introduced at the 2020 meeting, rebalancing the Federal Reserve's dual mandate regarding employment and inflation.

This Friday, global financial markets will focus on Jackson Hole at the foot of the Teton Mountains in Wyoming.

At that time, Federal Reserve Chair Powell will speak at the Jackson Hole Global Central Bank Conference, and the market is closely watching whether he will open the door for a rate cut in September. Currently, money market traders anticipate an 80% probability of a 25 basis point rate cut in September. The Jackson Hole meeting has historically been an important platform for the Federal Reserve to convey policy signals, and Powell's speech in 2023 guided market expectations toward the first rate cut in September.

This year's meeting theme is 'The Transforming Labor Market: Demographics, Productivity, and Macroeconomic Policy.' On the surface, it is an academic topic, but the actual signal conveyed is that after inflation declines, the Federal Reserve is refocusing on employment. Given the current cracks in the labor market, slight adjustments in policy tone could directly determine the market direction in the coming months.

Meanwhile, this meeting may also address some results of the Federal Reserve's framework review. Several major investment banks expect Powell may partially reverse the flexible average inflation targeting (FAIT) policy introduced at the 2020 meeting, rebalancing the dual mandate of the Federal Reserve regarding employment and inflation.

Focusing on Powell's views on the labor market

Powell will give a speech titled 'Economic Outlook and Framework Review' at 10 AM Eastern Time on Friday (10 PM Beijing Time on Friday). Market attention is focused on how he will assess the signs of weakness in the U.S. labor market shown in the July employment report, and whether this data is sufficient to prompt the Federal Reserve to initiate a rate cut cycle at the September meeting.

Powell warned at the July FOMC press conference that the potential for new job creation in the U.S. labor market is declining due to factors such as a slowdown in immigration and an aging population, leading to a decreased 'employment increment threshold.' The significant downward revision of the July non-farm data confirms this: job growth may be nearing a standstill, with the unemployment rate rising to 4.2% (still below the long-term average), and while wage growth has slowed, it has not fully receded.

The July non-farm payroll report not only showed data significantly below expectations but also made significant downward revisions to the previous two months' data. The Bureau of Labor Statistics described these revisions as 'greater than normal levels' (the net revision for the two months was -258,000), raising market concerns about the state of the labor market. The subsequently released CPI data was mixed, generally viewed by the market as 'not as hot as feared,' further boosting expectations for a rate cut in September.

According to Goldman Sachs economist David Mericle's forecast, Powell may modify his statements from the July FOMC press conference, no longer emphasizing that the committee is 'well positioned' to wait for more information. Instead, he may point out the risks the Federal Reserve faces in fulfilling its dual mandate while highlighting the downside risks in the labor market indicated by the July employment report, thereby signaling to the market an intention to support rate cuts if necessary.

Is the Federal Reserve's policy framework undergoing adjustments?

Jackson Hole has traditionally been seen as a policy barometer for the Federal Reserve. Over the past five years, it has almost annually brought about a 'policy turning point': signaling easing in 2019, introducing the average inflation targeting (FAIT) in 2020, continuing easing leading to misjudgment in 2021, shifting to aggressive tightening in 2022, hinting at the end of rate hikes in 2023, and releasing signals for rate cuts in 2024.

A major highlight of this year's meeting is the framework review. Goldman Sachs and Deutsche Bank expect the Federal Reserve may partially revise the FAIT framework introduced at the 2020 Jackson Hole meeting.

Goldman Sachs believes that the Federal Reserve may return to a more traditional 'dual mandate' target (focusing on both underemployment and overheating) while abandoning the 'average inflation target' and re-adopting a 'flexible inflation target' as the main strategy. However, when interest rates reach the zero lower bound, some compensatory tools may still be retained.

Deutsche Bank is more aggressive. They pointed out that the framework reform in 2020 was a significant driver of the inflation overshoot, and therefore expect Powell's speech to potentially call for the repeal of the 2020 modifications and restore the dominant role of preventive policy adjustments.

If these expectations materialize, the 'turning point effect' of Jackson Hole may reoccur: the framework established in 2020 could be partially revised in 2025.

One rate cut this year? Three? There is a huge divergence on Wall Street.

Regarding the Federal Reserve's rate decision in September, Wall Street shows a clear divergence in expectations for the number of rate cuts, with different institutions focusing on various interpretations of employment and inflation data.

Goldman Sachs leans toward a dovish stance, expecting that although Powell will not signal a rate cut in September explicitly, he will clearly indicate that he may support such action.

The bank believes that the Federal Reserve may implement three 25 basis point rate cuts this year. The reasoning is based on the July non-farm payroll data and revisions from the previous two months, which show a significant slowdown in job growth. Although the unemployment rate remains low, the potential for new job creation is declining, and market and wage pressures are manageable. Goldman Sachs expects the Fed to act decisively to prevent further deterioration of the labor market.

Barclays believes that the market is overly confident about a rate cut in September. The bank's baseline forecast indicates that the next rate cut will not occur until December. Barclays pointed out that Powell hinted at the FOMC press conference in July that the committee is not in a hurry to adjust interest rates, and the bank believes that the latest employment report data does not entirely invalidate Powell's remarks.

J.P. Morgan holds a more cautious stance. The bank's market intelligence team noted in a report that considering the Fed's rate cut decision in September will depend on the non-farm payroll data on September 5 and the CPI data on September 11, the Jackson Hole meeting 'may not have a substantial impact.'

How the market trades around the Jackson Hole meeting

Historically, the bond market has usually reacted significantly to the Jackson Hole meeting. According to Bloomberg data, U.S. Treasury yields have often seen notable fluctuations during the meeting period over the past few years.

Goldman Sachs U.S. Treasury trader Kyle Peterson believes that this year's Jackson Hole meeting will not bring significant new information, stating, 'The threshold for a 50 basis point rate cut is extremely high, and I don't think we have seen enough data to support that.' He suggests taking profits on any long positions at this stage and maintaining a neutral stance.

In the foreign exchange market, Goldman Sachs foreign exchange trader Sarah Stone noted that while most market participants believe that the important events in September deserve more attention, they have 'more or less completely ignored this weekend's Jackson Hole meeting,' underestimating the possibility that Powell may turn dovish.

Goldman Sachs derivatives strategist John Marshall pointed out that ahead of the Jackson Hole meeting, the option prices for most ETFs are relatively low compared to historical levels, especially for ETFs related to high-yield bonds, emerging markets, and the S&P 500 index. Investors expect volatility for ETFs related to regional banks, real estate, and technology sectors to increase.

As the meeting date approaches, market participants are reducing their short positions in the dollar and protecting themselves by purchasing 'cheap' dollar call options to manage the risks that the meeting may bring.

Risk warning and disclaimer

The market carries risks, and investments should be made cautiously. Follow our guidance to avoid unnecessary risks! This article does not constitute personal investment advice and does not take into account individual users' specific investment goals, financial situations, or needs. Users should consider whether any opinions, views, or conclusions in this article are appropriate for their specific circumstances. Invest accordingly at your own risk!!!