At 10 PM tonight, Federal Reserve Chairman Powell will speak at the Jackson Hole Global Central Bank Annual Meeting. It is well-known that a single statement from the Federal Reserve chairman can cause significant tremors in the crypto market. Based on subjective speculation and past experiences, it’s not hard to conclude that there will likely be notable volatility tonight.

As for what Powell will actually say, whether the information released is hawkish or dovish, currently no one can guess. It may very well happen that when Powell makes a dovish remark, the market rises, and when he makes a hawkish remark, the market falls, leaving investors confused. If you don't have sufficient English listening skills and real-time machine translation may not be accurate, by the time domestic data sites translate and publish Powell's remarks, the market may have already moved.

Is there any way to make money regardless of price fluctuations? Yes, there is, my friends. Today, I will introduce one of the trading strategies for options — the straddle strategy. I believe most traders are not formally trained, and options, being non-linear derivatives, are indeed relatively complex. Therefore, I will explain options and this trading strategy in relatively easy-to-understand language 🥳🥳🥳🥳.

Everyone is quite familiar with spot trading and contracts (futures), and I believe most traders typically use these two trading models. However, options might be less familiar to many. Let me briefly introduce options. Let’s keep it simple for now; we will only cover the buyer of the option, who is the one gaining the rights. In one sentence, an option is like buying insurance. Options generally have several key elements: underlying asset, contract type, strike price, expiration date, and premium.

Additionally, options are divided into European and American options. European options can only be exercised at expiration, while American options can be exercised prior to expiration. However, since all options on Binance are European options, all the content we discuss later will pertain to European options.

Underlying asset: It refers to the currency that your selected option is about, just like how there are BTC perpetual contracts and ETH perpetual contracts.

Contract Types: Divided into Call Options and Put Options. A call option is somewhat similar to going long in a contract, while a put option is similar to going short.

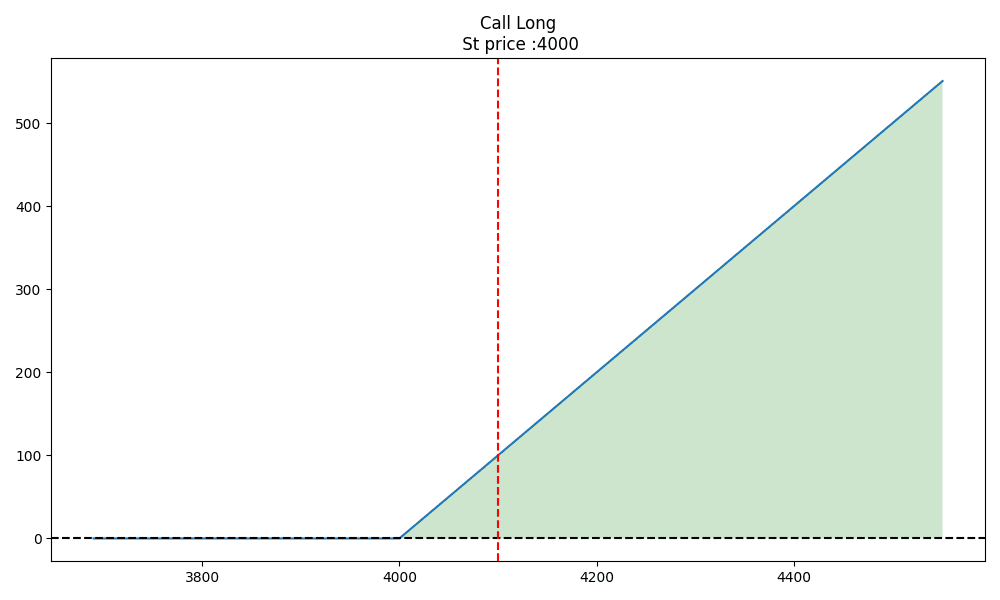

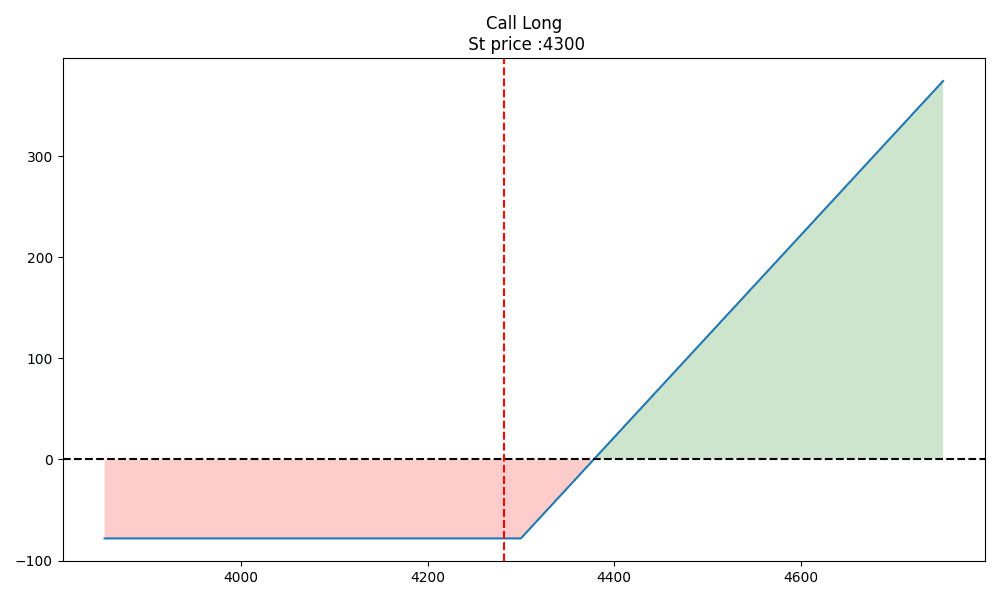

Strike Price: As mentioned before, an option is like buying insurance, and the strike price is the price at which you can exercise your rights at expiration. For example, if we now buy a call option with a strike price of 4000 and an expiration date of one day later, then one day later, you have the right to purchase ETH at the price of 4000, regardless of the current market price of ETH. Clearly, you will only choose to exercise it when the market price is above 4000. For instance, if the market price is 4500, you have the right to buy ETH at 4000. After exercising that right, if you sell it in the market at 4100, you net 100. Conversely, if the market price of ETH is 2000, then why not just buy directly in the market without exercising this right? That means you would not exercise the option. So, ignoring the premium, the profit curve for this option trading would be as follows:

Just like how people generally find shorting harder to understand than going long, I think people might also find put options a bit harder to grasp compared to call options. So, I will explain what put options are.

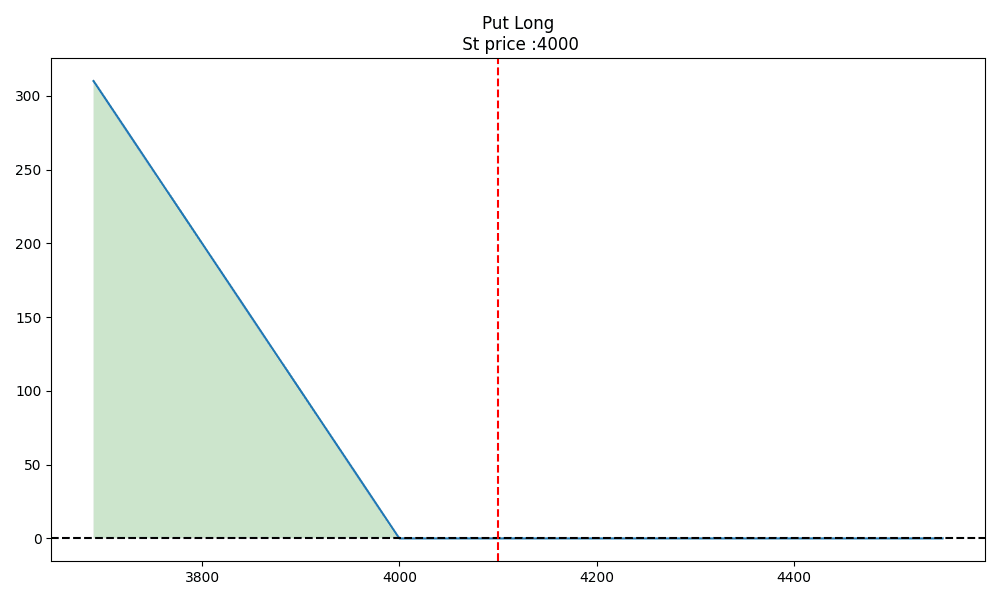

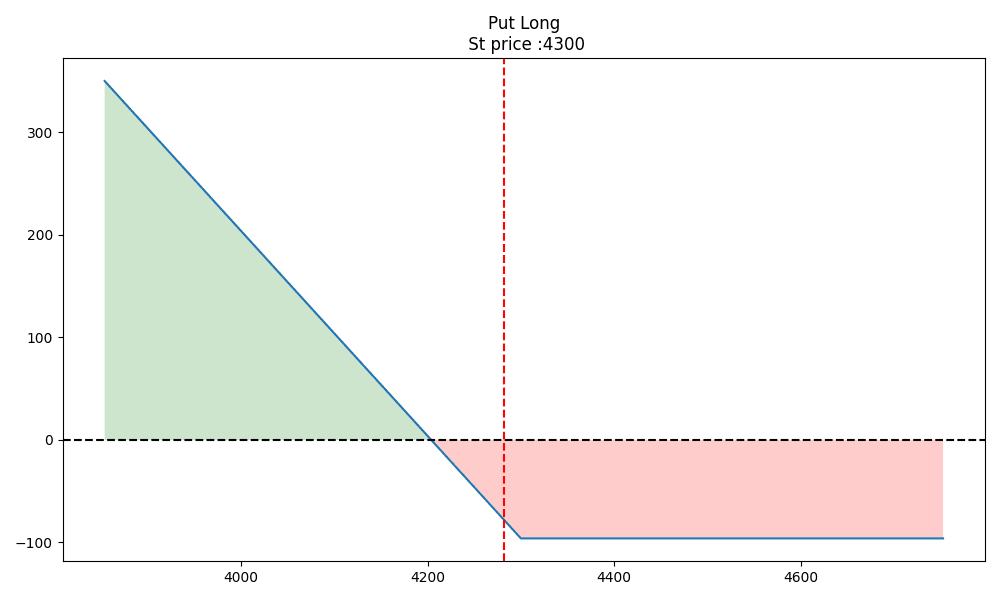

Put Option means that at expiration, you have the right to sell the underlying asset to the counterparty at the strike price. For example, if you currently have a put option with a strike price of 4000, and when it expires, if the market price is 3900, you can buy it at 3900 in the market and sell it at 4000, which nets you 100; conversely, if the market price is 4100, and you previously held the spot asset, you definitely wouldn't exercise your option to sell at 4000, nor would you spend 4100 in the market to buy and then sell at 4000. Therefore, the profit curve for this put option transaction is as follows:

Expiration Date: Literally.

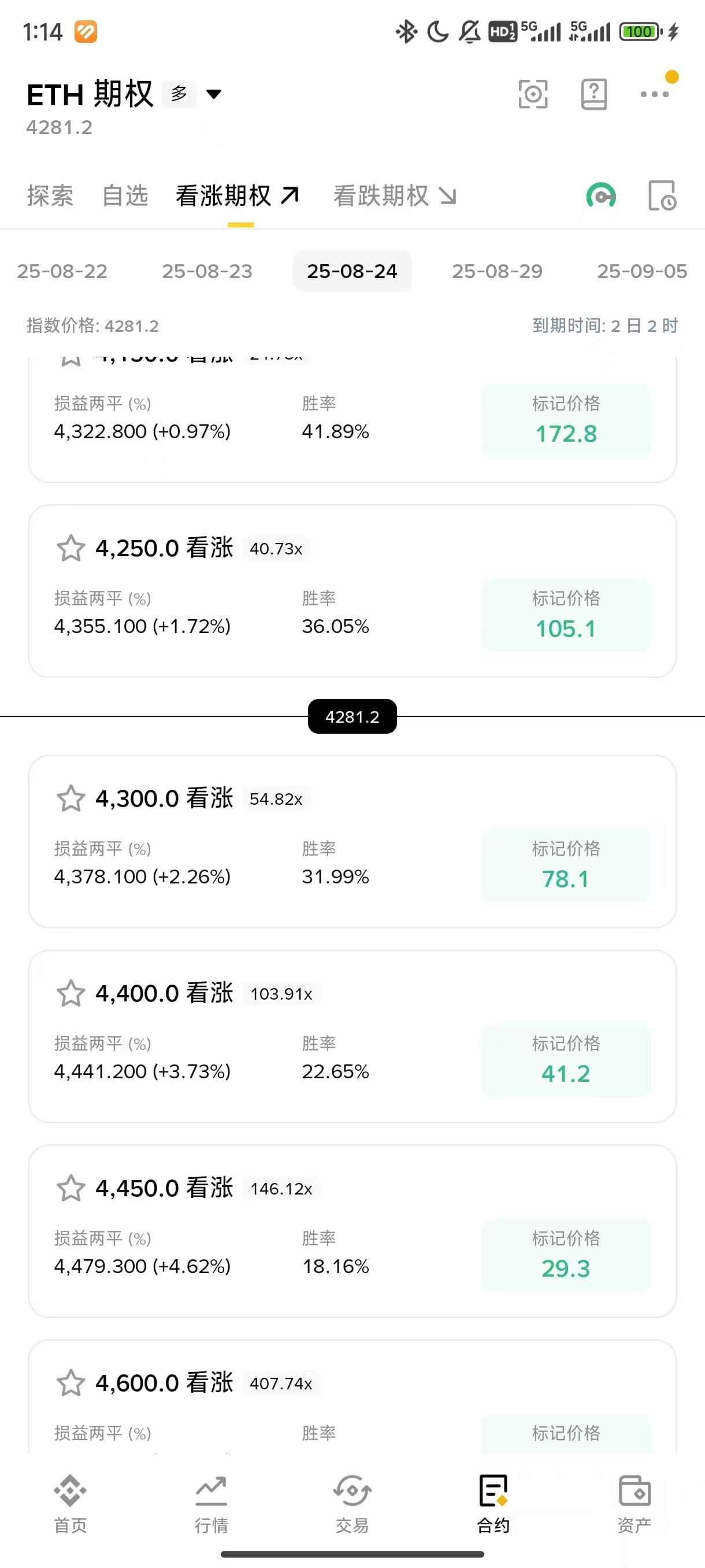

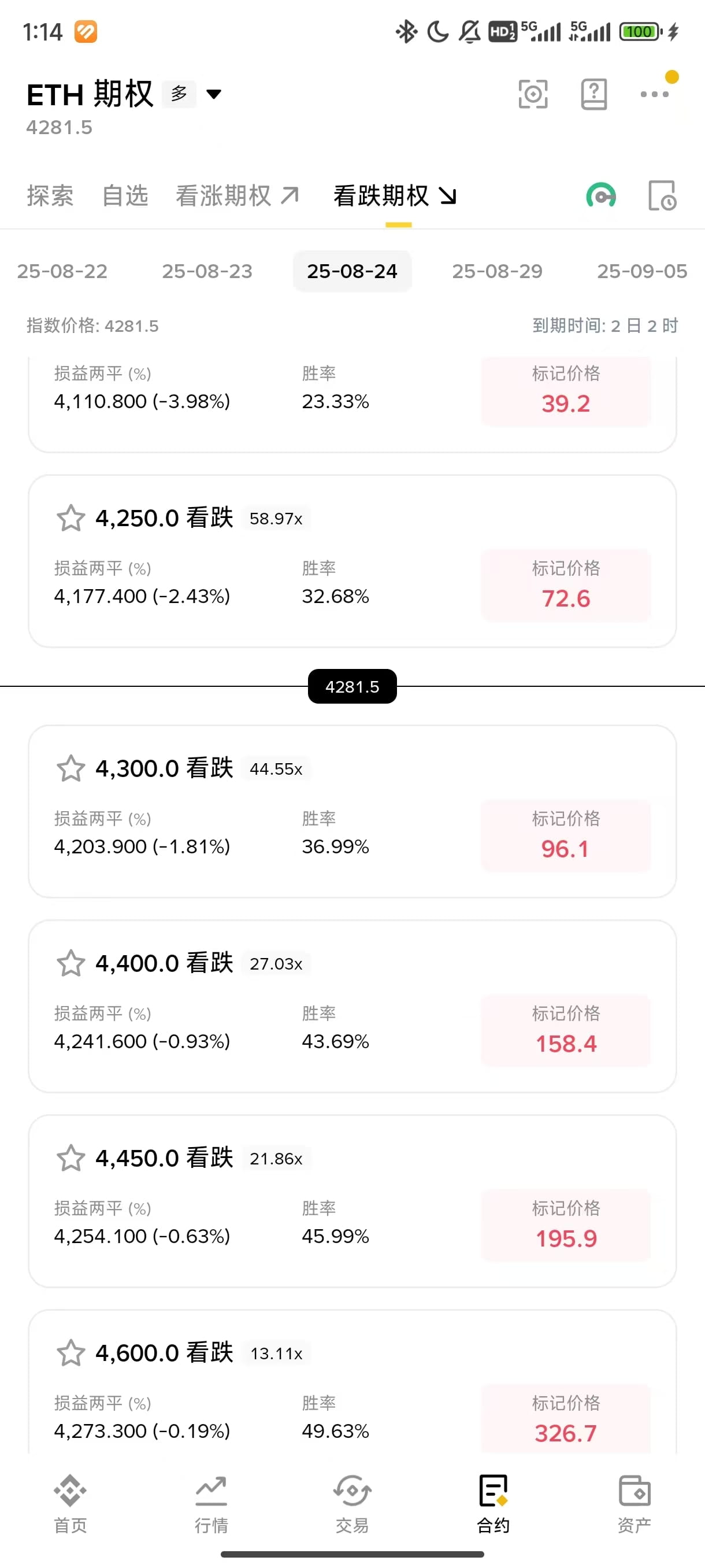

Premium: Also known as the option fee, it is similar to paying for insurance; why would someone provide you with a guarantee? Don’t you have to give something in return? So the money we spend to purchase options in trading is the premium. The example above uses some round numbers, and now let's look at the actual situation. When I wrote this article, the price of ETH was about 4282. Let's take a look at the prices for call and put options based on the recent price of 4300:

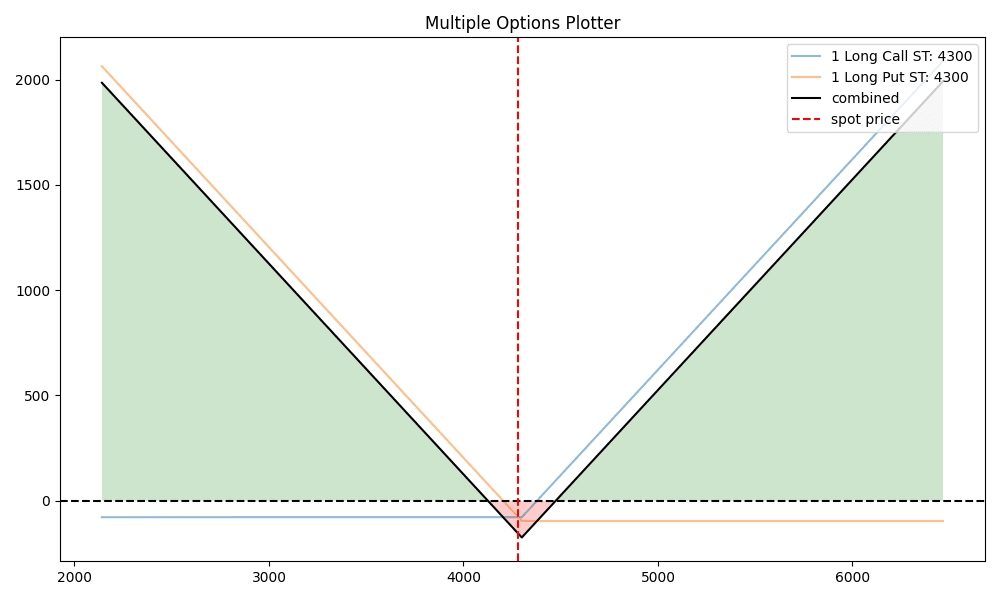

Now, let's take the premium into account, and its profit curve would look like this:

Returning to today's topic, we want to profit during large fluctuations. Since call options provide protection when prices rise and put options provide protection when prices fall, I can simply buy one of each, right? If the strike prices of the two options are the same, then this is a straddle strategy. There is also a variant where if the strike prices are not the same, then this is a strangle strategy.

It looks great, right? But don’t forget our premium: one is 78.1 and the other is 96.1. If we buy one of each option, we would first spend 78.1 + 96.1 = 174.2 USD, which is about 4.06% of the ETH price. This means that when you believe the volatility tonight will exceed 4.06%, you can construct such an option trading strategy. However, if unfortunately, it turns out to be calm tonight, you would have to bear some losses.

That’s the explanation of the straddle strategy. Follow Chainpion614 to learn more about financial content.