If Bitcoin's story is 'digital gold', then Ethereum's narrative is quietly shifting towards a 'global ledger', with a key 'resonance moment' expected in 2025.

Ethereum stands at an unprecedented 'multi-narrative resonance' node.

On-chain, ETH staking continues to rise, gradually establishing a 'risk-free interest rate anchor'; in traditional finance, the spot ETF has been running for over a year, with trading volume and net inflows rapidly increasing, marking a continuous ramp-up of compliant capital; at the corporate level, an increasing number of U.S. publicly traded companies are strategically choosing to incorporate ETH into their treasury reserves.

Staking, ETFs, and corporate treasuries—these three seemingly independent threads are resonating with each other, pushing ETH from a singular cryptocurrency towards a comprehensive financial asset with yield characteristics, compliant channels, and corporate reserve value.

If Bitcoin's story is 'digital gold', then Ethereum's narrative is quietly shifting towards a 'global ledger', with a key 'resonance moment' expected in 2025.

Staking steadily rises, and ETH's 'benchmark interest rate' emerges.

Since the Shanghai upgrade opened the staking withdrawal feature in April 2023, Ethereum has completely resolved the risks of a bottleneck exit, unlocking the growth potential of the staking ecosystem. Since then, the derivatives market based on LSD has rapidly expanded, driving the ETH staking rate to continually rise.

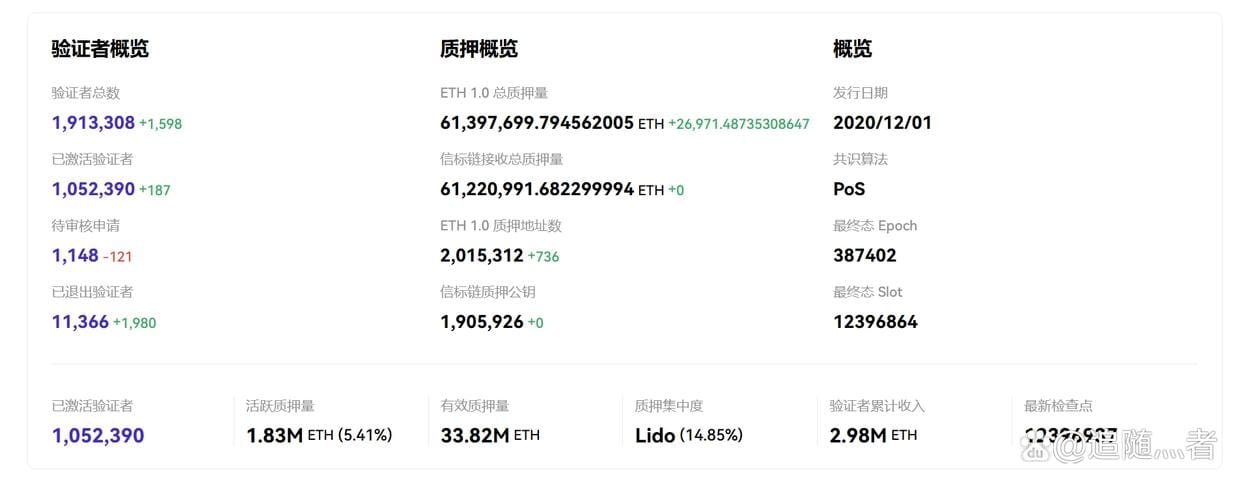

As of the time of publication, the amount of ETH staked has surpassed 33.8 million, calculated at the current price of about $140 billion, accounting for over 25% of the total supply. This is a significant increase from about 10% staking rate a few years ago, which not only strengthens network security but also enhances ETH's scarcity from a supply-demand perspective.

More importantly, ETH staking is gradually becoming the 'interest rate anchor' of on-chain finance.

Over the past year, an annualized staking return rate of 3%-5% has been widely accepted by the market, and some institutional research reports even regard it as the 'on-chain version of treasury yield', forming an implicit contrast with the U.S. Treasury yield curve. This characteristic makes ETH not just a trading asset but endows it with the underlying logic of quasi-fixed income products.

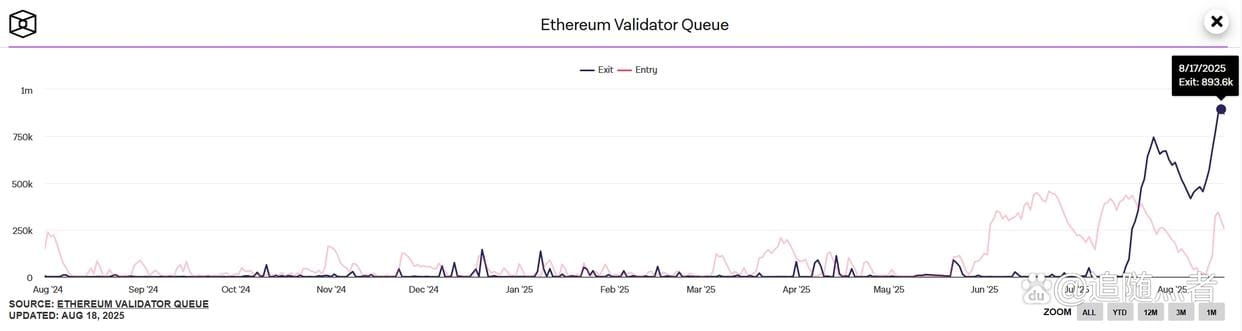

Of course, a noteworthy counter-trend has recently emerged—since July 16, the number of ETH unstaking requests has surged, with validator exit requests skyrocketing from less than 2,000 to 475,000 by July 22, and the waiting time extending from less than an hour to over 8 days.

According to The Block data, there are currently about 670,000 ETH (approximately $3.1 billion) in the exit queue, far exceeding new staking demand, with an estimated processing time of nearly 12 days. Factors such as the unwinding of leveraged staking cycles against the backdrop of rising prices, LST decoupling risks, and arbitrage opportunities are the main reasons driving a large number of ETH unstakings, with Lido, EthFi, and Coinbase being the primary sources of exits.

However, despite the short-term volatility brought by the unstaking wave, from a long-term perspective, ETH staking has gradually become the 'risk-free interest rate anchor' on-chain, becoming one of the underlying financial logics of ETH.

It's worth noting that U.S. Treasury yields are expected to remain in the 4%-5% range throughout 2024, making ETH staking yields seem less attractive at times. However, as the Federal Reserve opens up a rate cut channel in 2025, ETH's 3%-5% staking yields regain competitiveness and are even seen as 'excess returns' in some risk models.

This means that a deeper implicit connection is being established between ETH's on-chain interest rates and the global liquidity environment, especially as re-staking protocols like EigenLayer have absorbed over $10 billion worth of ETH, giving rise to a chain logic of 'staking rates → re-staking premiums → protocol security'.

In other words, ETH is not only an asset itself but is gradually becoming the underlying collateral for the Web 3 financial system.

ETFs have become the main channel for traditional capital.

In May 2024, the U.S. SEC approved the 19 b-4 application of 8 Ethereum spot ETFs, which officially began trading on July 23, marking the formal opening of a compliant channel between ETH and Wall Street. To date, Ethereum spot ETFs have been running for over a year.

Objectively speaking, ETFs, as a 'compliance gateway', provide traditional institutions with a direct channel to allocate ETH, reducing compliance friction at the financial and audit levels. According to SoSoValue data, as of now, the total net assets of U.S. Ethereum spot ETFs have exceeded $27 billion, accounting for about 5.34% of Ethereum's market cap, with a cumulative net inflow of $12.4 billion since their listing.

However, the market often overestimates the short-term effects of new things while underestimating their long-term impacts. The development of ETH spot ETFs is a reflection of this rule, as the true explosion of ETFs did not appear at the beginning—prior to May this year, the average daily trading volume of ETH ETFs was still relatively low, with limited market interest.

The turning point occurred on August 11, 2025, when the net inflow of Ethereum ETFs on that day first broke $1 billion, with BlackRock's ETHA attracting $640 million and Fidelity's FETH attracting $277 million, highlighting the siphoning effect of the two giants, and the institutional shift of Ethereum ETFs has clearly emerged.

The significance of ETFs lies in the fact that they are not only a 'channel' for funds but also a 'legitimate status' on compliance audits and financial statements, greatly reducing the resistance for institutions to hold ETH. Another profound significance is that it opens up arbitrage and allocation paths for cross-border financial institutions.

More importantly, the concentration of holdings in ETFs has begun to emerge, with the two major ETFs, BlackRock and Fidelity, accounting for two-thirds of the U.S. ETH ETF market. This trend towards a concentration of capital not only brings a siphoning effect but may also signify that the 'institutional pricing' characteristic of ETH will become increasingly evident in the future.

ETH accelerates influx into U.S. stock balance sheets.

If MicroStrategy's relationship with BTC is a milestone case of publicly traded companies incorporating crypto assets into their balance sheets, then starting in 2025, ETH is also approaching a similar turning point.

Recently, an increasing number of U.S. publicly traded companies are choosing to incorporate ETH into their treasuries, and this is not merely symbolic holding but rather large-scale, strategic allocation.

Taking BitMine as an example, according to official disclosures, its crypto asset holdings have exceeded $6.612 billion, an increase of about $1.7 billion from the previous week's $4.9 billion. BitMine holds 1.523 million ETH (calculated at the current price of $4,326 per ETH) and also holds 192 BTC.

At the same time, Nasdaq-listed company Cosmos Health also announced a securities purchase agreement with a U.S. institutional investor for up to $300 million to initiate the ETH treasury strategy and provide custody and staking infrastructure through BitGo Trust.

This proactive inclusion into corporate treasuries differs from the passive allocation of ETFs: ETFs primarily carry the exposure demand for financial products, while companies directly purchasing ETH and incorporating it into their treasury means that ETH is becoming an actual settlement medium and reserve asset. Whether for financial diversification, cross-border payments, or employee incentives and R&D incentives, ETH is beginning to demonstrate its potential as a 'liquid asset'.

Overall, after experiencing a wave of widespread pessimism, Ethereum's multiple narratives are beginning to converge.

Staking yields have brought ETH a quasi-'sovereign bond' interest rate anchor.

ETFs open up the allocation channel for compliant capital.

Corporate treasuries further endow ETH with real value for reserves and payments.

The three are intertwined, collectively driving ETH from a 'cryptocurrency' to a 'financial infrastructure asset.'

If Bitcoin represents 'digital gold' in corporate treasuries, then Ethereum's value narrative is gradually pointing to the 'liquidity core of the global ledger'.