Author: Joseph Ayoub, former head of cryptocurrency research at Citigroup

Translated by: Shenchao TechFlow

Summary: From premium to discount, Saylor's financial alchemy will come to an end.

Introduction

The last time cryptocurrency experienced a 'traditional' bubble was in the fourth quarter of 2017, when the market exhibited staggering double-digit or even triple-digit percentage daily increases, exchanges were overwhelmed by surging demand, new participants flocked in, speculative ICOs (Initial Coin Offerings) emerged in droves, trading volumes hit historic highs, and the market welcomed a new paradigm, new heights, and even first-class luxurious experiences. This was the last mainstream, traditional retail bubble in the cryptocurrency space, nearly nine years after the birth of the first 'trustless' peer-to-peer currency.

Fast forward four years, and cryptocurrency has experienced a second major bubble, this time larger, more complex, and incorporating new paradigms of algorithmic stablecoins (such as Luna and Terra), alongside some 'rehypothecation' crimes (like FTX and Alameda). This so-called 'innovation' is so complex that few truly understand how the biggest Ponzi schemes operate. However, like every new paradigm, participants firmly believe this is a new form of financial engineering, a new mode of innovation, and if you don't understand it, no one has time to explain it to you.

The largest retail Ponzi scheme collapses.

The era of DATs has arrived (2020-2025)

At that time, we did not realize that Michael Saylor's MicroStrategy, born in 2020, would become the seed driving institutional-level funds to reposition in Bitcoin, all beginning with the dramatic crash of Bitcoin in 2022 [1]. By 2025, Saylor's 'financial alchemy' has become the core driving force behind today's marginal buyer demand for cryptocurrency. Similar to 2021, very few truly understand this new paradigm of financial engineering mechanisms. Nevertheless, those who have experienced the 'dangerous atmosphere' of the past are gradually becoming more alert; however, the occurrence and secondary effects of this phenomenon are precisely what distinguishes 'knowing there might be a problem' from 'profiting from it.'

A new paradigm of financial wisdom..?

What is the basic definition of DAT?

Digital Asset Treasuries (DATs) are quite simple tools. They are traditional equity companies whose sole purpose is to purchase digital assets. New DATs typically operate by raising funds from investors, selling company shares, and using the proceeds to purchase digital assets. In some cases, they will continue to sell equity, diluting existing shareholders' rights, to continue raising funds to purchase digital assets.

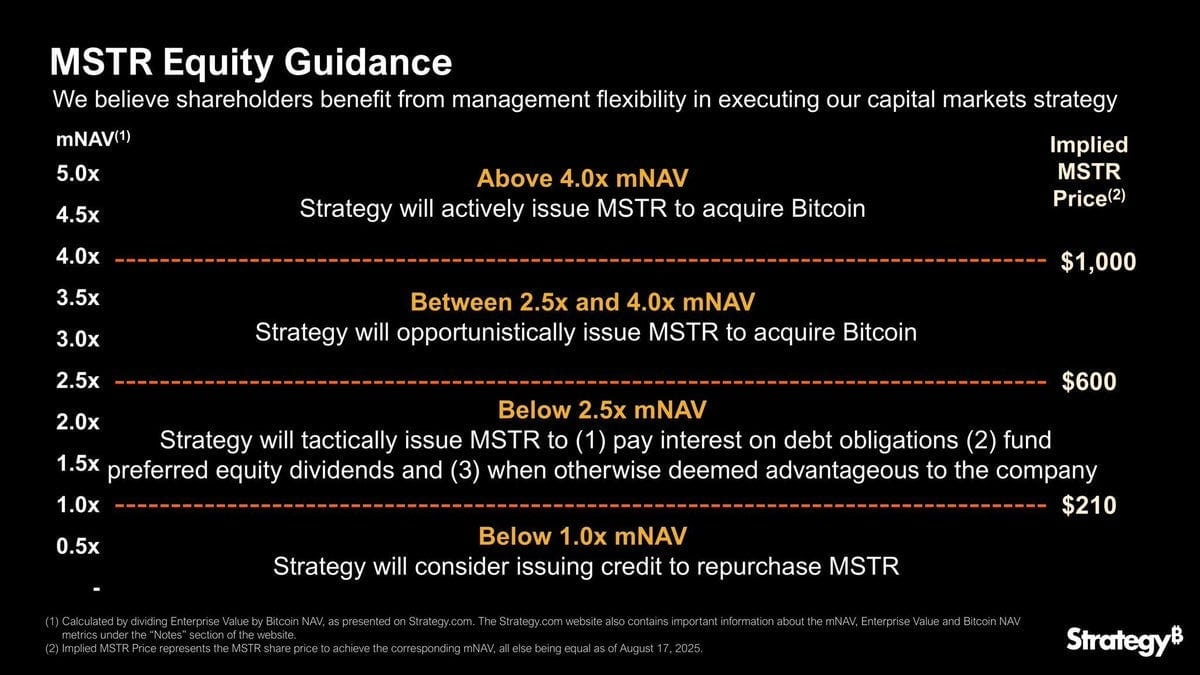

The net asset value (NAV) of a DAT is calculated very simply: assets minus liabilities, divided by the number of shares. However, what is traded in the market is not the NAV, but mNAV, which is the market's valuation of these shares relative to their underlying assets. If investors pay $2 for every $1 exposure to Bitcoin, that is a 100% premium. This is what is known as 'alchemy': in a premium situation, companies can issue shares and purchase BTC in a value-enhancing manner; whereas in a discount situation, the logic reverses—buybacks or pressure from activist investors dominate.

The core of this 'alchemy' lies in the fact that these are new products with the following characteristics:

A) Exciting (SBET skyrocketing 2,000% in a trading day)

B) High volatility

C) Seen as a new paradigm of financial engineering

Reflexive flywheel mechanism

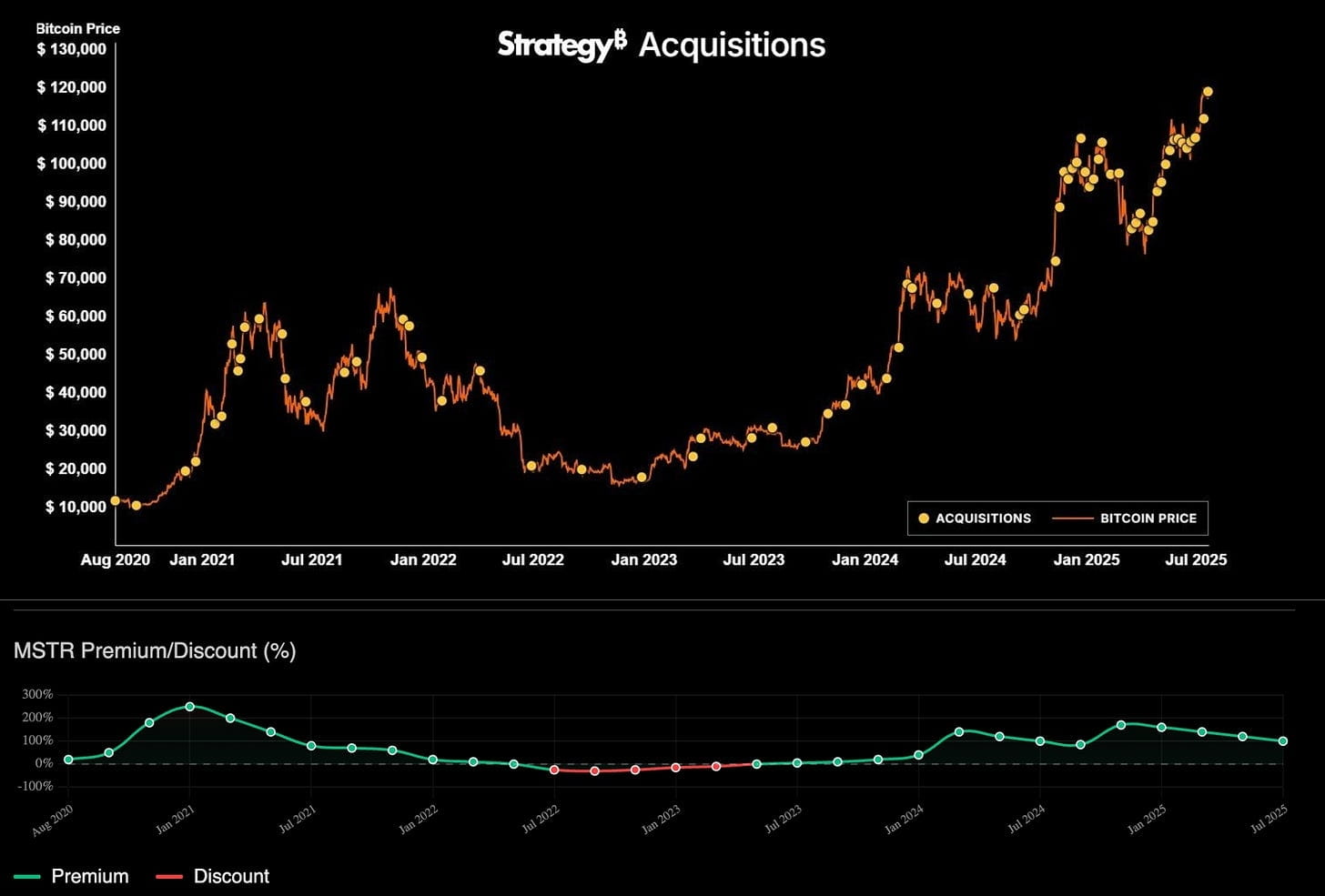

Thus, with this 'alchemy,' Saylor's MicroStrategy has been trading at a premium above its net asset value for the past two years, allowing Saylor to issue shares and purchase more Bitcoin without significantly diluting shareholder equity or affecting the stock price premium. In this case, this mechanism is also highly reflexive:

MicroStrategy's acquisition behavior can be more aggressive during periods of premium. Meanwhile, during discount periods, debt and convertible bonds become the main driving force.

mNAV premium allows Saylor → issue shares → buy BTC → BTC price rises → increases its NAV and stock price → attract more investment with a stable premium → further financing and more purchases. [2]

However, a phenomenon has emerged: the strong correlation between discounts and Bitcoin prices seems to have diverged; this may be a result of other DATs coming to market. However, this could signal a critical turning point, as MicroStrategy's ability to sustain this flywheel mechanism through financing has weakened, and its premium has significantly decreased. This trend deserves close attention; in my view, this premium is unlikely to return significantly.

MSTR premium/discount compared to Bitcoin price.

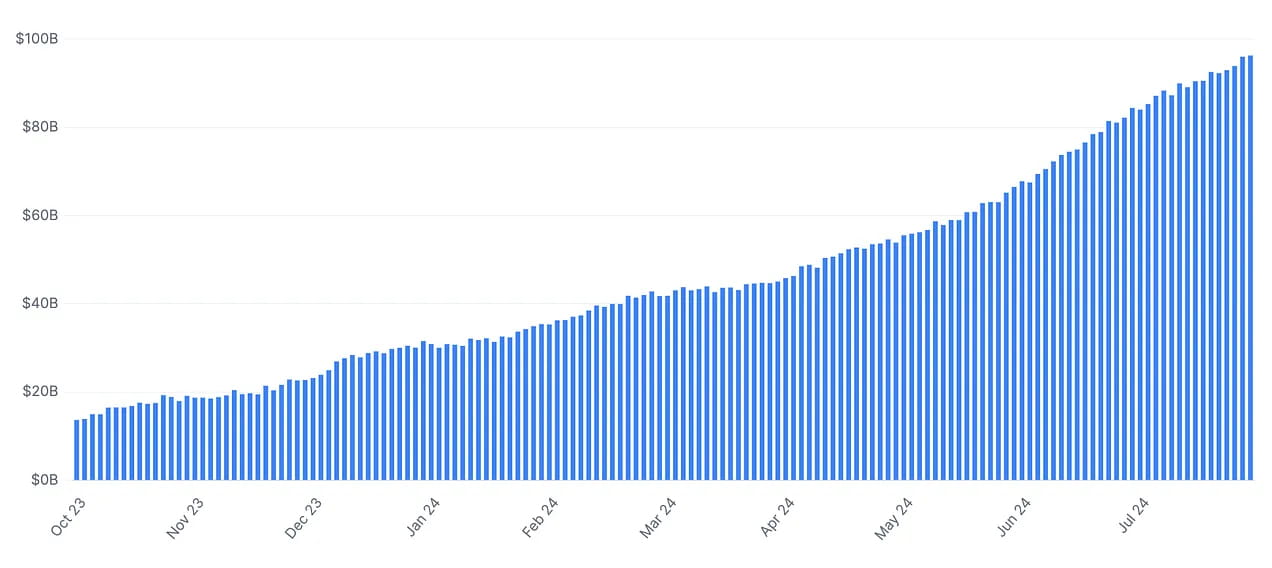

Undoubtedly, as the net asset value of DATs has grown from $10 billion in 2020 to over $100 billion today, this tool has provided significant liquidity to the market, comparable to the total of all Bitcoin ETFs at $150 billion. Under positive risk conditions, including Bitcoin, all risky assets, this mechanism has also injected a highly reflexive price mechanism into the underlying assets [3].

Total net asset value of cryptocurrency treasury companies

Why it will collapse

I believe the development path of this matter is not complex; to me, there are only three paths and one logical conclusion:

DATs continue to trade at a premium above mNAV, the flywheel mechanism continues to operate, and insatiable demand drives further increases in cryptocurrency prices. This is a new paradigm driven by financial alchemy.

DATs begin to trade at a discount, leading the market to gradually unwind until forced liquidation and bankruptcy protection occur, ultimately resulting in a complete collapse.

DATs begin to trade at a discount, being forced to sell underlying assets to repurchase shares, repay debts, and cover operating costs. This unwinding process becomes recursive until the size of these DATs shrinks, ultimately turning into 'zombie companies.'

I believe the likelihood of DATs continuing to trade at a premium is extremely low; in my view, this premium is a result of risk assets benefiting under loose liquidity conditions, which also allowed Nasdaq stocks and overall stock prices to perform well. However, when liquidity conditions tightened in 2022/2023, it was clear that MSTR was not trading at a premium, and even traded at a discount in the short term. This is the first area where I believe there is mispricing—DAT companies should not exist at premium trading; in fact, these companies should trade at a deep discount well below NAV.

The root cause is that the implied equity value of these companies depends on their ability to create value for shareholders; traditional companies achieve this through dividends, stock buybacks, acquisitions, business expansions, etc. However, DATs lack such capability, and their only ability is to issue shares, raise debt, or perform some minor financial operations like pledging, but these have no significant impact. So what value is there in holding shares of these companies? Theoretically, the value of these DATs lies in their ability to return net asset value to shareholders; otherwise, their equity value is not very meaningful. But given that these tools have failed to realize this potential, and some companies even promise never to sell their underlying assets, in such cases, the value of these shares only depends on the price the market is willing to pay.

Ultimately, the equity value now depends on:

The potential for future buyers to create premiums (based on the ability of DATs to continuously raise funds at a premium).

The price of the underlying assets and the liquidity of the market to absorb sales.

The implied probability that shares can be redeemed at net asset value.

If DATs can return capital to shareholders, it would be similar to an ETF. However, since they cannot achieve this, I believe they are closer to closed-end funds. Why? Because they are a tool for holding underlying assets but lack any mechanism to distribute the value of these assets to investors. For those with good memory, this clearly reminds me of GBTC and ETHE, which underwent a similar situation during the significant unwinding process in 2022, when the premiums of closed-end funds quickly turned into discounts [4].

This unwinding is essentially priced based on the implied probabilities of liquidity and future conversion possibilities. Given that neither GBTC nor DAT can achieve redemptions, when liquidity is abundant and demand is high, the market will price at a premium, but when the price of the underlying assets declines and begins to contract, this discount becomes very apparent, with discounts on trusts even reaching 50% of NAV. Ultimately, this 'discount' on NAV reflects the price investors are willing to pay for an asset that cannot logically or foreseeably distribute NAV value to trust holders; thus, pricing is based on its future potential to achieve this goal and the demand for liquidity.

Market confidence and tightening liquidity, the grayscale Bitcoin trust market premium gradually collapses.

Debt and subordinate risks

Similarly, apart from returning capital, DATs can only create value for shareholders in two ways: through financial management (like pledging) or through leveraging debt. If we see DATs starting to incur significant debt, it will be a signal that a large-scale unwinding may be imminent, although I believe the likelihood of leveraging debt is low. Regardless of the situation, these two ways of creating value fall far short of the equity value of companies holding assets, which brings to mind GBTC. If this analysis holds, investors will eventually realize this, the confidence bubble will be burst, leading to a shift from premium to discount, and potentially triggering the sale of underlying assets.

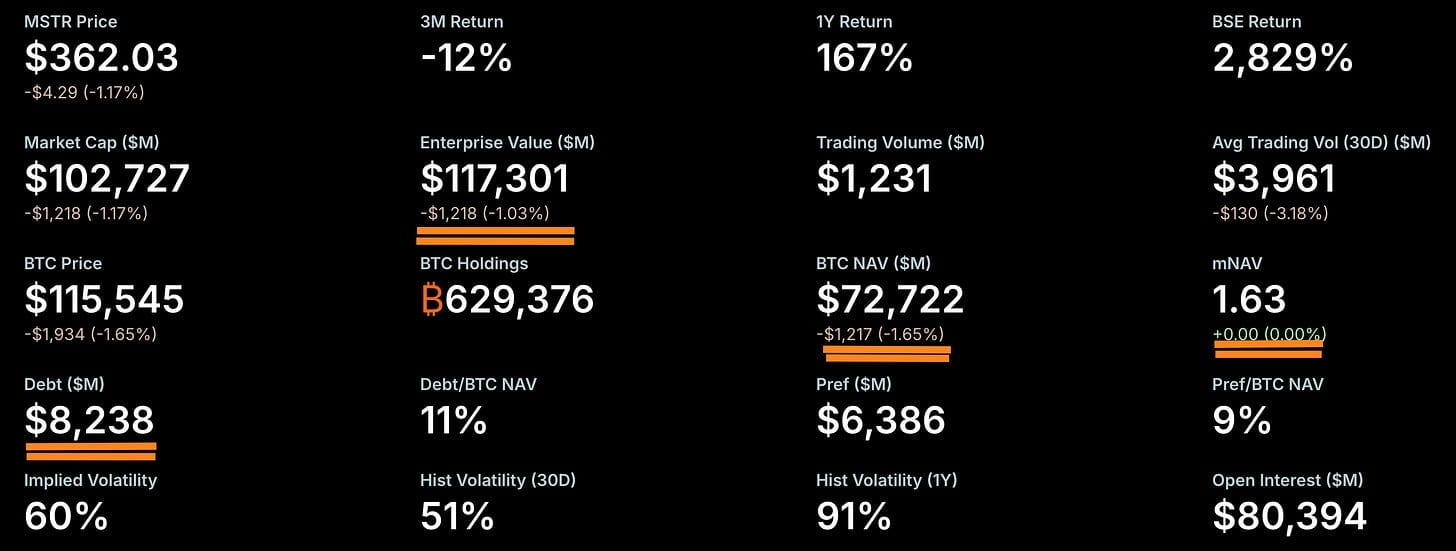

Currently, I believe the likelihood of forced liquidation or bankruptcy protection due to leverage or debt liquidation is also very low. This is because the current levels of debt are not enough to pose a problem for MicroStrategy or other DATs, considering these trusts are more inclined to finance through equity issuance. Taking MicroStrategy as an example, its debt is $8.2 billion, holding 630,000 Bitcoins; the price of Bitcoin would need to fall below $13,000 for debts to exceed assets, which I believe is extremely unlikely [5]. BMNR and other Ethereum-related DATs have almost no leverage, so forced liquidation is also unlikely to become a major risk. In contrast, other DATs, aside from MSTR, are more likely to gradually liquidate through aggressive acquisitions or shareholder votes, returning capital to shareholders. All acquired Bitcoins and Ethereum may directly return to the market and circulate again.

Saylor's choices

Although Saylor holds only about 20% of MicroStrategy's equity, he possesses over 50% of the voting rights. Therefore, it is almost impossible for activist funds or investor coalitions to force a sale of shares. The potential consequence of this situation is that if MSTR begins to trade at a significant discount, and investors cannot enforce a buyback, there may be investor lawsuits or regulatory oversight, which could further negatively impact the stock price.

Debt remains well below net asset value, and mNAV is still at a premium.

Overall, my concern is that the market may reach a saturation point, at which point additional DATs will no longer affect prices, thereby enhancing the reflexivity of these mechanisms. When market supply is sufficient to absorb both artificially created and immature DAT demand, the unwinding process will begin. In my view, such a future may not be far off. It seems to be just around the corner.

Nevertheless, Saylor's 'debt' theory has been greatly exaggerated. His current holding size is insufficient to pose a significant problem in the short term. In my view, his convertible bonds will ultimately have to be redeemed at face value in cash, as if the adjusted net asset value (mNAV) experiences a discount, his equity may significantly decline.

One point to focus on is whether Saylor will buy back shares by issuing more debt when the adjusted net asset value falls below 1. I believe the likelihood of this approach addressing the mNAV issue is very low, as once investor confidence is damaged, it is hard to restore. Therefore, continuing to issue debt to compensate for the mNAV issue could be a risky path. Additionally, if mNAV continues to decline, MSTR's ability to issue more debt to cover its debts will become increasingly difficult, further affecting its credit rating and investor demand for its products. In this case, issuing more debt could trigger a reflexive downward spiral:

mNAV declines → Investor confidence declines → Saylor issues debt to buy back shares → Investor confidence remains low → mNAV continues to decline → Pressure increases → More debt issuance (short-term debt must reach a significant leverage level to pose danger).

Saylor is considering share buybacks through debt issuance—a potentially dangerous path.

Regulation and historical precedents

In the current situation, two more likely scenarios are:

MicroStrategy faces a collective lawsuit from investors seeking to return shareholder capital to net asset value;

Regulatory scrutiny. The first of these situations is relatively straightforward and may occur at significant discounts (below 0.7 times mNAV). The second situation is more complex and has historical precedents.

History shows that when companies masquerade as operating enterprises but actually act as investment tools, regulation may intervene. For example, in the 1940s, Tonopah Mining Company was ruled as an investment company due to its primary holdings in securities [6]. In 2021, GBTC and ETHE traded at extremely high premiums but subsequently collapsed to a 50% discount. Regulators turned a blind eye when investors profited, but when retail investors suffered losses, the narrative shifted, eventually forcing it to convert to an ETF.

MicroStrategy's situation is similar. Although it still calls itself a software company, 99% of its value comes from Bitcoin. In fact, its equity acts as an unregistered closed-end fund, without a redemption mechanism. This distinction can only be maintained when the market is strong.

If DATs continue to trade at a discount, regulators may reclassify them as investment companies, limiting leverage, imposing fiduciary duties, or forcing redemptions. They may even completely shut down the equity issuance 'flywheel' model. What was once seen as financial alchemy during premium periods may be defined as predatory behavior during discount periods. This may be Saylor's true vulnerability.

What is the headline news?

I have hinted at what may happen, and now I will make some direct predictions:

More DATs will continue to launch targeting riskier, more speculative assets, signaling that liquidity cycles are about to peak.

Pepe, Bonk, Fartcoin, and others

Competition among DATs will dilute and saturate the market, leading to a significant decrease in mNAV premium.

The valuation dynamics of DATs will gradually approach those of closed-end funds.

This trend can be captured through trades that 'short equity/long underlying assets' to capture mNAV premium.

Such trades will be accompanied by funding costs and execution risks. Additionally, using OTM (out-of-the-money) options is also a simpler way to express this.

In the next 12 months, most DATs will trade at a discount below mNAV, which will become a key point for the cryptocurrency market to shift toward a bear market.

Share issuance halts. Without new capital inflows, these companies will turn into 'zombie companies' with static balance sheets. No growth flywheel → no new buyers → discounts persist.

MicroStrategy may face collective lawsuits from investors or regulatory scrutiny, which could question its commitment to 'never selling Bitcoin.'

This marks the beginning of the end.

As the price declines, the reflexive impact on the underlying assets will quickly turn the positive evaluation of financial engineering and 'alchemy' into a negative one.

Views on Saylor, Tom Lee, and others will shift from 'genius' to 'fraud.'

Some DATs may use debt instruments during the market unwinding process, either for share buybacks or for purchasing more assets → this is a signal of imminent collapse.

The relevant trading strategy involves using debt leverage and increasing short premium positions.

An activist fund may acquire shares of a certain DAT at a discount and pressure or force its liquidation and asset distribution.

At least one activist fund (such as Elliott and Fir Tree) will buy DAT positions at a significant discount, inciting liquidation and forcing BTC/ETH to be returned to shareholders. This will set a precedent.

Regulatory intervention:

The SEC may enforce disclosure rules or investor protection measures. Historically, persistently discounted closed-end funds have prompted regulatory reform.

Sources

[1] MicroStrategy Press Release

[2] MicroStrategy SEC 10-K (2023)

[3] Bloomberg – 'Crypto Treasury Companies Now Control $100bn in Digital Assets'

[4] Financial Times – 'Grayscale Bitcoin Trust Slides to 50% Discount' (Dec 2022).

[5] MicroStrategy Q2 2025 10-Q filing.

[6] SEC v. Tonopah Mining Co. (1940s ruling on investment company status).