Written by: Tiger Research

Translated by: AididiaoJP, Foresight News

Major global exchanges are launching their own public chains to explore new sources of revenue, and Upbit and Bithumb are also not without the possibility of joining this competition.

There are four possible scenarios: Layer 2 based on OP Stack, Korean Won stablecoin infrastructure, leveraging the liquidity characteristics of the Korean market, and non-listed stock tokenization. Each of these could serve as a differentiated approach reflecting the unique market environment of Korea.

Of course, regulatory restrictions and technical complexity remain significant obstacles. Achieving this in the short term is not easy. However, with trading volumes decreasing and global competition intensifying, it is clear that both exchanges must seek new growth drivers.

The Prelude to Competition Among Exchange Public Chains

Cryptocurrency exchanges are officially beginning to join the competition for blockchain infrastructure. With the inclusion of Coinbase's Base, Kraken's Ink, and recently Robinhood, the competitive landscape is becoming increasingly intense.

Behind this intense competition lies the limitations of the existing fee-based business model. Although the fee model of exchanges is the most stable and proven source of revenue in the cryptocurrency industry, it is highly dependent on market conditions due to its structural characteristics, thus requiring revenue diversification. Additionally, it is worth noting that past exchanges competed within limited domains of their respective jurisdictions, while the competitive stage has now expanded to a global level. Meanwhile, decentralized exchanges (DEX) have held over 25% of the market share, challenging the position of centralized exchanges.

At the same time, as the cryptocurrency industry integrates into the traditional financial system at an accelerating pace, from the exchange's perspective, opportunities for derivative businesses utilizing blockchain infrastructure beyond simple trading intermediaries are rapidly opening up. Ultimately, these changes intertwine, making competition among exchange public chains likely to accelerate further in the future.

If Upbit and Bithumb launch their own public chains?

In the context of global exchanges rushing to launch their own public chains, it is natural to raise the question: 'Is it possible for Korean exchanges Upbit and Bithumb as well?' To determine this, it is necessary to examine the current status of these exchanges and their past attempts.

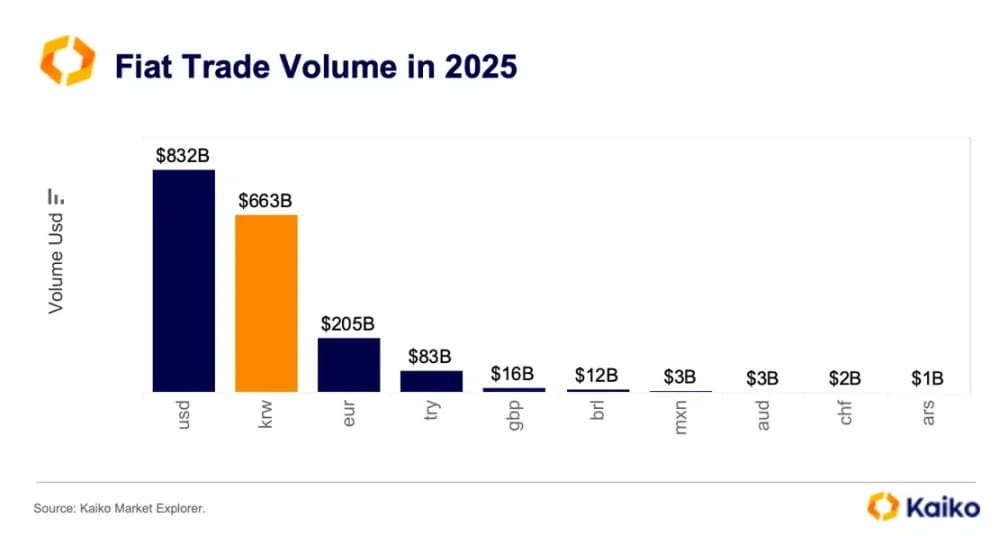

South Korea occupies a unique position in the global cryptocurrency market. In terms of fiat currency, the trading volume of the Korean Won (KRW) ranks second globally, only behind the US Dollar (USD), and sometimes even surpasses it. It is extremely rare for such a large trading volume to be generated by users from a single country. Thanks to this market environment, Upbit and Bithumb have grown into large enterprises with total assets exceeding 5 trillion KRW.

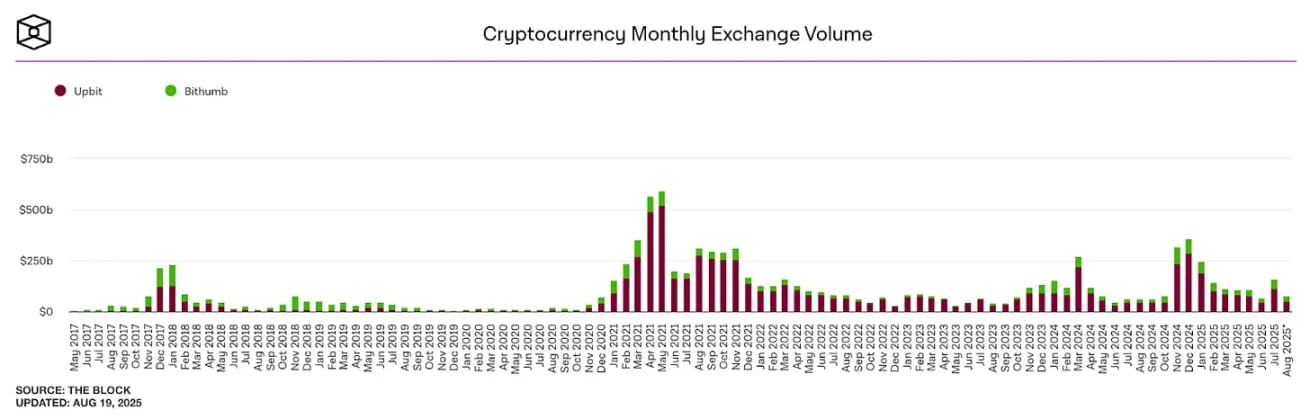

Source: The Block

However, this seemingly solid structure is also undergoing changes. Since trading volumes peaked in 2021, both exchanges have experienced a downward trend in trading volumes. This is because domestic users are shifting to global exchanges like Binance and Bybit or decentralized exchanges (DEX). This means that the domestic exchanges can no longer solely rely on the Korean liquidity characteristics environment.

Exchanges have also noticed this change. Upbit and Bithumb have both attempted to enter the global market by establishing overseas branches and diversifying their businesses. However, relying solely on the 'Korean exchange' brand makes it difficult to ensure differentiated competitiveness in overseas markets. Moreover, although various businesses based on platform operations have been launched, most are far from the inherent competitive advantages of exchanges and have not achieved significant results. Of course, regulatory sanctions may also limit business diversification.

But now the winds of change are blowing. The pro-cryptocurrency policy of Trump's second term has improved the global regulatory environment, allowing exchanges to seek new growth strategies more actively. In this context, it is entirely a viable option for Upbit and Bithumb to launch public chains.

If they launch a public chain, different results than in the past can be expected. They can directly leverage the inherent advantages of a large user base and abundant liquidity of the exchanges. Especially, if combined with the unique characteristics of the Korean market, it is entirely possible to create differentiated value.

Expected Scenario 1: Building Layer 2 Based on OP Stack

If these exchanges build their own chains, the likelihood of choosing Layer 2 is higher than Layer 1.

The biggest reason is the complexity of development and the scale of resources required. Developing and operating Layer 1 requires massive resources. Even in Layer 2, where the entry barriers have been lowered due to Rollup services, a considerable number of professionals are still needed; the fact that Kraken's Ink project invested around 40 developers is evidence of this. From the exchange's perspective, independently building and operating such infrastructure is bound to be a heavy burden. Furthermore, their goal is to expand business based on infrastructure, rather than focusing on building high-performance infrastructure itself.

In addition to regulatory risks, Layer 1 must issue a native token, but under Korea's regulatory environment, token issuance is practically impossible and there is a high risk of sanctions from authorities. Therefore, the Layer 2 model that operates without the need to issue a native token, as adopted by Coinbase, will become the most realistic alternative.

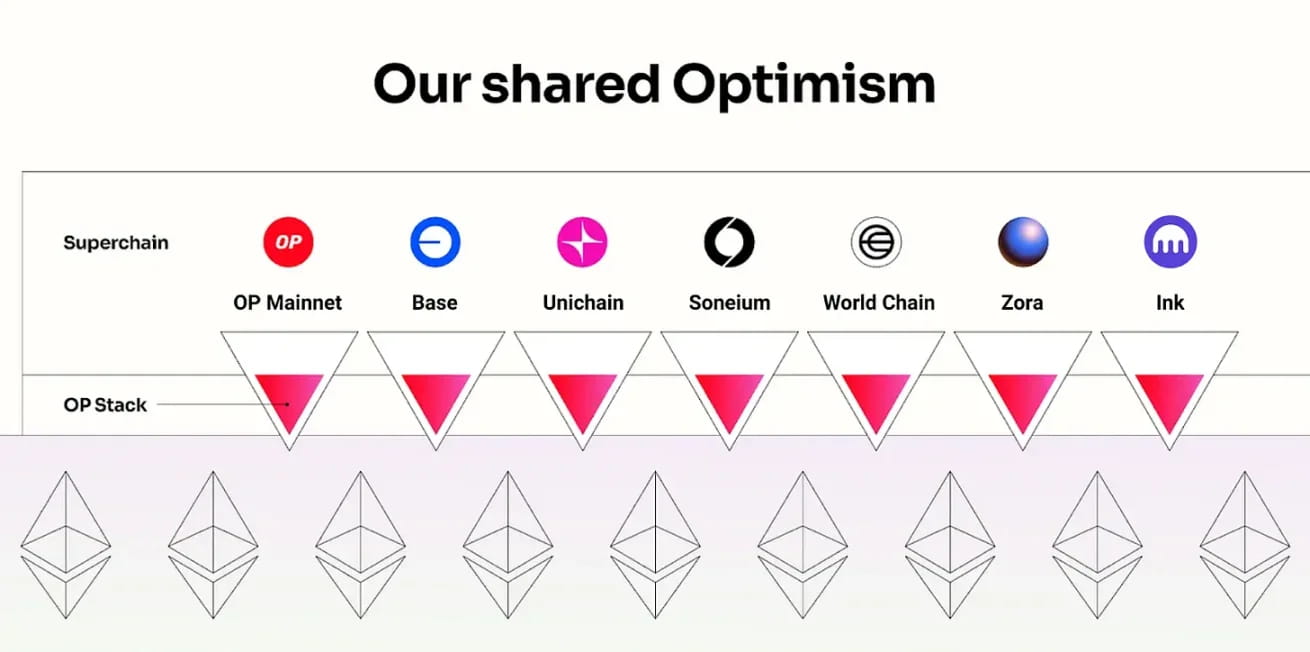

Source: Optimism, Tiger Research

While there are various stacks for Layer 2 development, the Optimism (OP) Stack is currently almost standardized among global exchanges. Coinbase's Base and Kraken's Ink are built on this and have become reference models for exchange types. Robinhood has exceptionally chosen Arbitrum due to its differing strategic objectives. Coinbase and Kraken pursue broad ecosystem expansion with interoperability as a priority, while Robinhood focuses on putting its financial services on-chain, thus judging that Arbitrum with greater customization flexibility is more suitable.

Upbit and Bithumb share similar goals with Coinbase. Both exchanges need to overcome the limitations of the current fee-centered model and leverage their large user bases to expand into on-chain services to create new sources of revenue, making openness and interoperability key. Therefore, if Upbit and Bithumb launch their own chains, the most likely option will be a Public Layer 2 based on OP Stack.

Expected Scenario 2: Korean Won Stablecoin Infrastructure

Another scenario for Upbit and Bithumb launching their own chains is to build dedicated infrastructure around Korean Won stablecoins.

Upbit's KRW Stablecoin Trademark, Source: KIPRIS

In fact, both exchanges have shown positive trends towards the stablecoin market. Upbit and Bithumb have applied for trademarks related to stablecoins, particularly Upbit's collaboration with Korea's leading simple payment service Naver Pay, officially announcing plans to enter the Korean Won stablecoin market. Focusing on Upbit, which has the highest potential, the realistic scenario is that Naver Pay issues a stablecoin based on the Korean Won, while Upbit provides the blockchain infrastructure for it. This is due to the (Virtual Asset User Protection Act) prohibiting exchanges from trading virtual assets issued by themselves or related parties.

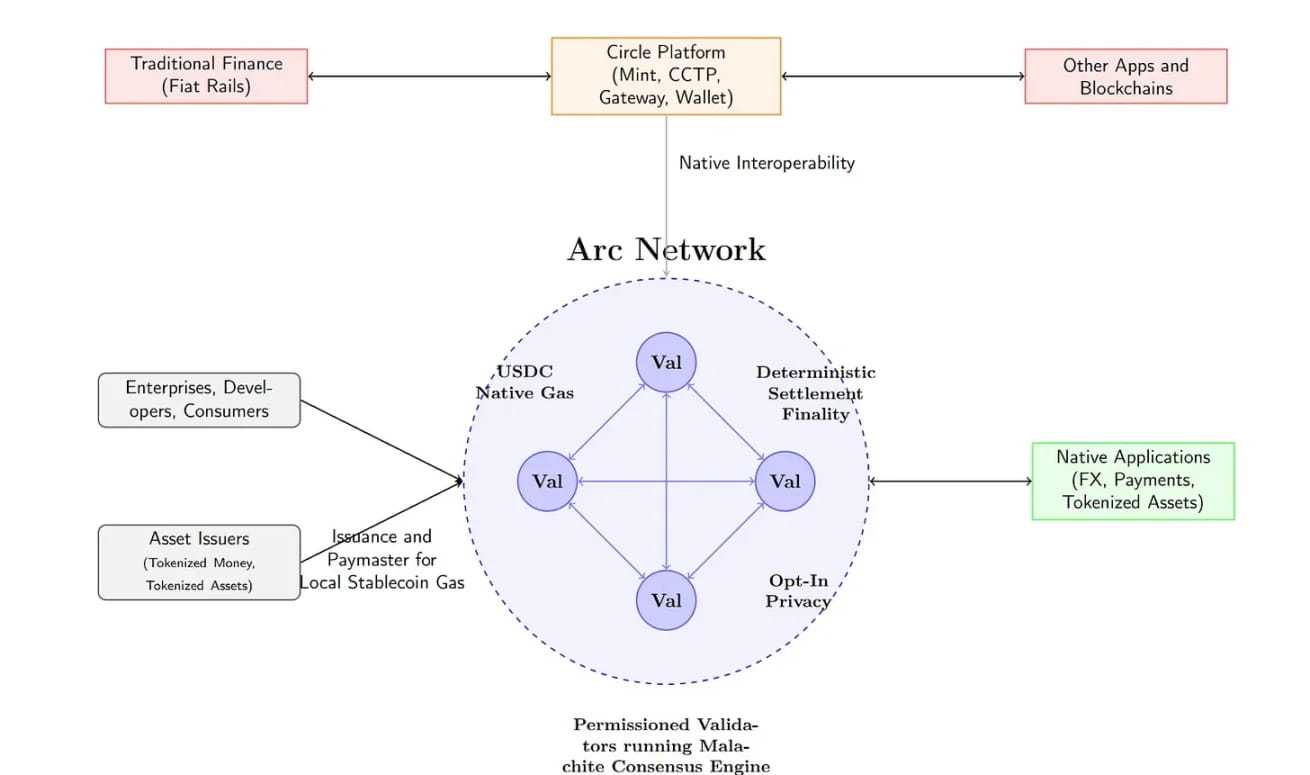

Source: Circle

In this case, the core lies in building dedicated infrastructure optimized for stablecoins. Functions like daily payment or privacy protection can be added to achieve differentiated services, and a structure for using Korean Won stablecoin to pay network gas fees can be designed. This is a model similar to USDC's Arc Network, aimed at building an ecosystem where all transactions revolve around stablecoins. This structure provides users with a stable cost structure while creating actual demand for Korean Won stablecoins, laying the foundation for sustained usage.

However, there are technical limitations. Optimism defaults to using Ethereum for gas fees and does not support custom gas token functionality. Therefore, in this case, building a Layer 2 based on customizable Arbitrum or a Layer 1 that uses the Korean Won stablecoin as a native token may be a more suitable choice.

Expected Scenario 3: Strategy Utilizing the Liquidity Characteristics of Korea

One strategy that Upbit and Bithumb can try is to leverage the liquidity characteristics of Korea. Currently, Korea has immense liquidity, ranking second globally in terms of fiat currency, but this liquidity remains confined within the internal systems of the exchanges.

Source: LlamaRisk

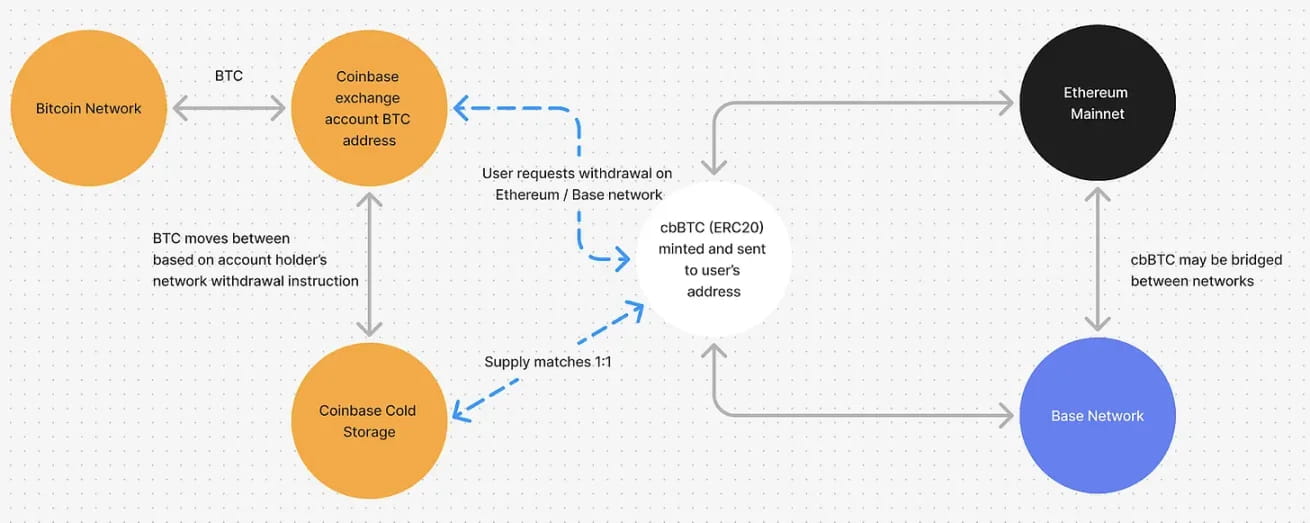

Exchanges can issue wrapped tokens such as upBTC and bbBTC based on custodial assets. Coinbase's cbBTC is a representative case. Although these wrapped tokens can also be used on other chains, if the exchange provides conveniences like one-click integration within the application, users are likely to remain within the chain built by the exchange rather than transferring externally. In this case, project teams attempting to leverage abundant liquidity have reason to choose this chain, activating the ecosystem and ensuring infrastructure-based revenue for the exchange. Furthermore, it is anticipated that wrapped tokens can also be used to explore additional business models like lending.

Expected Scenario 4: Entering the Non-Listed Stock (Pre-IPO) Tokenization Market

Another strategy that Upbit and Bithumb can choose is to enter the non-listed stock tokenization market. Upbit's operator Dunamu has long operated a non-listed stock trading platform through the Securities Plus non-listed platform and has accumulated experience, but this ultimately remains a P2P trading model connecting buyers and sellers. There are structural limitations such as low transaction completion rates and limited liquidity.

Source: Ustockplus

If non-listed stocks are tokenized based on their own chains, the situation will be different. Tokenized stocks can be traded in real-time through liquidity pools or market makers, with ownership transfers automated and transparently handled through smart contracts. In addition to purely improving trading efficiency, features like automatic dividends, conditional trading, and programmable shareholder rights can be realized on-chain, making it possible to design financial products that existing securities systems cannot achieve.

Recently, it is also worth noting that Naver is advancing the acquisition of Dunamu's securities Plus non-listed shares. If Upbit provides chain infrastructure, and Naver is responsible for platform operation and physical stock management, it could become a feasible division of labor under the regulatory environment. That is, entering the tokenization market by reducing institutional risk through separating trading infrastructure and securities management roles.

Summary

We explored various scenarios for Upbit and Bithumb to launch their own blockchain. However, the reality is that they face numerous challenges. The biggest obstacle is regulation. Korea adopts an active regulatory model, making it difficult to introduce services that are not explicitly defined by the law. Both exchanges are designated as group enterprises, further exacerbating the regulatory burden, while the lack of Web3-native leaders like Jesse Pollak from Base is also seen as a limiting factor. Additionally, the technical complexity and the likelihood of an independent blockchain becoming a reality in the short term are minimal.

Nevertheless, they still have considerable room for experimentation. Domestic trading volumes have been declining since peaking in 2021, and global competition is intensifying. The existing fee model has clear growth limitations, and previous attempts at revenue diversification have not achieved significant results. Continuous growth requires new driving forces, and bold attempts like building their own blockchain may be such a pathway. This may be the most realistic business diversification strategy, allowing full utilization of each exchange's competitive advantages, including user base and liquidity.