Altcoins are not merely speculative investments outside of Bitcoin. In most cases, they are built to represent – or aim to represent – specific operating sectors in Web3, a decentralized alternative to traditional internet and its associated services.

Evaluating the outlook and potential of the altcoin market cannot solely rely on price fluctuations. Important on-chain metrics like gas usage, transaction volumes, and the number of unique active wallets (UAW) provide a realistic picture of activity and adoption levels. Meanwhile, coin price volatility shows whether the market is in sync with these on-chain trends.

AI and social DApps are emerging as new pieces of Web3.

The UAW index – measuring the number of unique wallets interacting with DApps – is often used as a measure of adoption. However, this figure can still be influenced by one user owning multiple wallets or automated activity from bots.

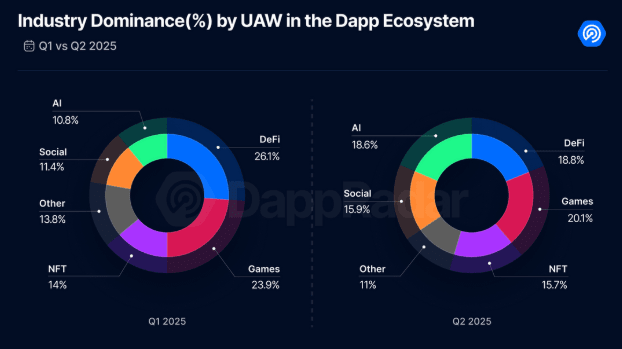

According to DappRadar's Q2 2025 report, the number of daily active wallets remains stable at around 24 million. However, the market share landscape is gradually changing: blockchain games still hold the lead with over 20% but have decreased compared to the previous quarter; DeFi is also declining, from over 26% to below 19%.

In contrast, social and AI DApps are becoming the new highlights. In the social space, Farcaster dominates with about 40,000 UAW daily. In the AI space, agent-based protocols like Virtuals Protocol (VIRTUAL) are notable, recording an average of 1,900 UAW weekly.

DeFi: Few users, many transactions, and institutional capital flowing in.

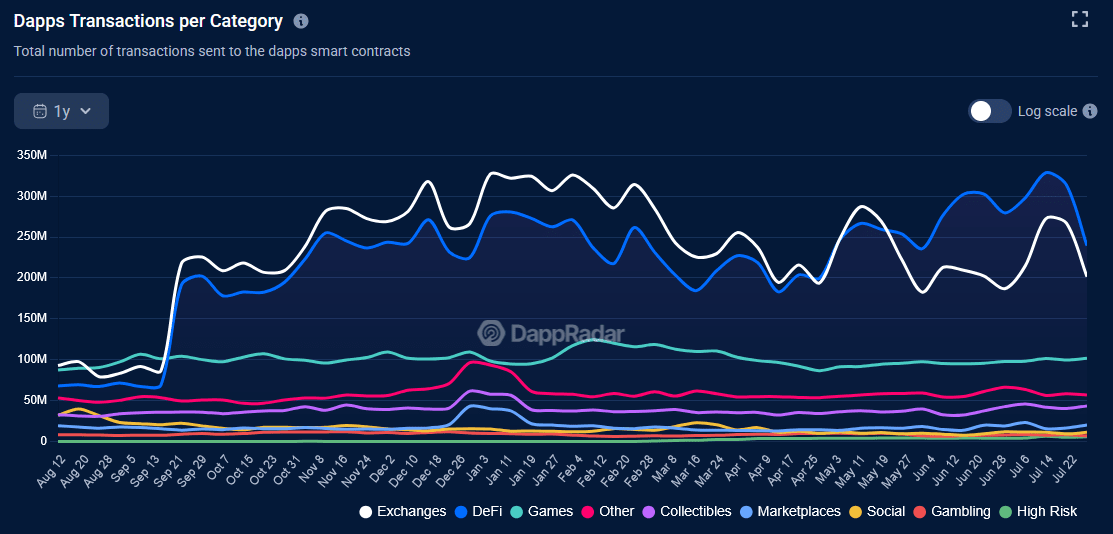

The number of transactions often reflects the frequency of smart contracts being activated, although this metric may be inflated by bots or automated processes.

In the case of DeFi, data shows an interesting paradox: the user base is declining, yet the system still records over 240 million transactions weekly — more than any other Web3 segment. This dominance is primarily due to trading-related activities (partially overlapping with DeFi). Meanwhile, blockchain gaming only achieves about 100 million transactions/week, while the 'Other' category (including AI and RWA but excluding social) reaches 57 million transactions/week.

Alongside transaction data, total value locked (TVL) provides an even more impressive perspective. According to DefiLlama, the TVL of DeFi has reached $137 billion, up 150% since January 2024, although still below the peak of $177 billion at the end of 2021.

The noteworthy point is the discrepancy between increasing TVL and decreasing UAW, reflecting a major trend in the current cryptocurrency cycle: institutionalization. Capital is increasingly concentrated in large wallets — including investment funds — rather than being dispersed among the retail community. Although this trend is still in its infancy and DeFi faces many legal uncertainties in various regions, organizations have begun to 'explore' the market:

Providing liquidity for licensed pools.

Bond-based lending via platforms like Ondo Finance (ONDO) and Maple. Notably, Maple attracts attention with its partnership with investment bank Cantor Fitzgerald.

Additionally, protocol-level automation from services like Lido (LDO) and EigenLayer (EIGEN) is also reducing activity from individual wallets. This indicates that DeFi is increasingly evolving into a capital-efficient infrastructure layer, focusing on large-scale yield rather than relying on direct participation from retail investors.

Other use cases dominate gas consumption.

Raw transaction data cannot reflect the entire picture of Web3. Another important metric is gas usage on Ethereum, which indicates the practical importance of economic activities and computations on the blockchain.

According to Glassnode, although DeFi is a key sector of Ethereum, it currently accounts for only about 11% of gas consumption. NFTs, which consumed significant gas in 2022, now account for only about 4%.

Meanwhile, the 'Other' category has surged, accounting for over 58% of current gas consumption, compared to around 25% in 2022. This category includes emerging sectors such as:

Tokenization of real-world assets (RWA)

Decentralized physical infrastructure (DePIN)

AI-based DApps

Other novel services, potentially becoming the next growth drivers of Web3.

Notably, RWA is particularly regarded as one of the most promising areas of cryptocurrency today. Excluding stablecoins, the total RWA value has increased from $15.8 billion at the beginning of 2024 to $25.4 billion, with around 346,250 token holders.

Are prices reflecting the developments in Web3?

History shows that asset prices rarely fluctuate in sync with on-chain activity. While frenzies and hype can create short-term price spikes, sustainable growth is often associated with sectors that deliver real utility and clear applicability. Over the past year, this has meant that projects focused on infrastructure and yield have outperformed those relying solely on hype stories.

Specifically:

Smart contract platform tokens recorded the strongest gains. The top 10 increased by an average of +142% (unweighted), led by HBAR (+360%) and XLM (+334%), reflecting long-term investor confidence in Web3 development.

DeFi tokens also recorded impressive results, averaging +77%, with Curve DAO (CRV) +308% and Pendle (PENDLE) +110%.

The top 10 RWA tokens increased by an average of +65%, led by XDC (+237%) and OUSG (+137%). Meanwhile, standout DePIN tokens like JasmyCoin (JASMY) +72% and Aethir (ATH) +39% have yet to pull the industry average higher, hovering around +10%.

On the contrary:

AI tokens lag behind, averaging -25% decline, with only Bittensor (TAO) +34% as the exception.

Game tokens mostly incur losses, except for SuperVerse (SUPER) +750% over the past 12 months.

Social tokens are nearly absent, as leading protocols have not yet released native assets.

Overall, investment flows in Web3 are still concentrated in mature sectors, driving the token values of smart contract platforms higher. DeFi and RWA tokens focusing on yield also deliver solid returns, while the most hyped areas – AI, DePIN, Social – have yet to convert attention into significant token profits.

As adoption deepens and nascent sectors mature, the gap between actual usage and token price performance may narrow. However, currently, investor confidence is still primarily placed in the foundational platforms of Web3.

The current altcoin market reflects a clear reality: investors trust infrastructure platforms and DeFi/RWA more than hype stories. As adoption expands and nascent sectors mature, the gap between real utility and token price performance may gradually narrow.

But at this moment, smart contract platforms, DeFi, and RWA are the pillars supporting investor confidence in the decentralized economy.