Written by: Luke, Mars Finance

The cryptocurrency market in August 2025 resembles the sea surface before a typhoon, appearing calm on the surface but with undercurrents raging. The price chart is stretched into an agonizing horizontal line, but this is not a brief pause in a bull market; it is a state of extreme fragility. The stagnation of Bitcoin and Ethereum’s upward momentum is not due to a single external shock, but rather the result of four powerful and conflicting forces locking prices tightly within a narrow range.

These four forces are like four invisible walls, jointly constructing the current market predicament: the tens of billions of buying from Wall Street through ETFs collides with the 'epic' profit-taking wall from early holders; within the Ethereum DeFi ecosystem, an algorithm-driven de-leveraging engine continuously creates selling pressure; the derivatives market exhibits a 'split personality' state, where retail speculative fervor and deep hedging by professional institutions coexist; and fundamentally, the high yield of dollar stablecoins acts like a massive magnet, siphoning off new liquidity that should have flowed into risk assets.

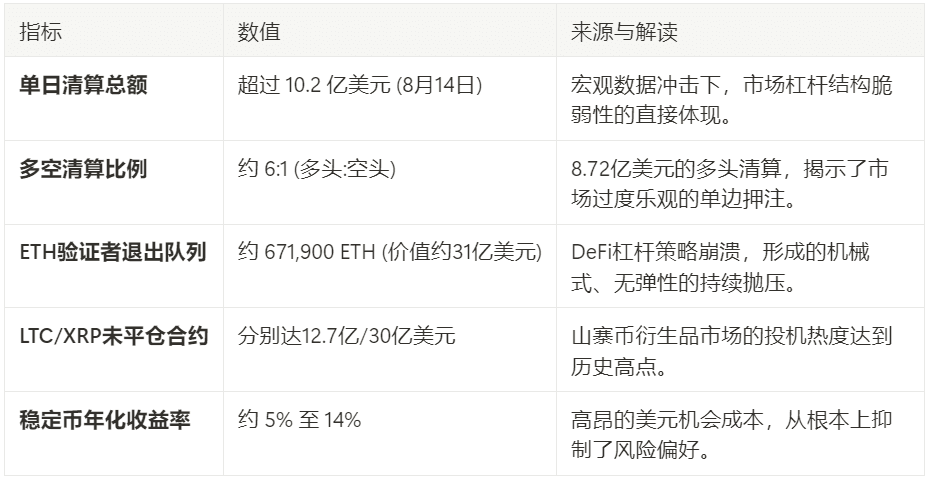

This delicate balance makes the entire market extraordinarily sensitive to any macro fluctuations; any unexpected spark could ignite the entire 'powder keg.' The following table summarizes the key quantitative indicators supporting this analysis, serving as cold footnotes to this multifaceted game.

Table 1: Key Indicators of Structural Pressure in the Market (August 2025)

The Illusion of Calm: A Warning from a Billion-Dollar Leverage Cleanse

Before mid-August, the market was shrouded in a strange calm. However, beneath the calm lies an already imbalanced leverage structure. On August 14, this fragility was instantly pierced by an unexpectedly high inflation report. The U.S. Bureau of Labor Statistics released the July Producer Price Index (PPI), which far exceeded expectations, becoming the last straw that broke the camel's back.

The transmission of news to the highly leveraged crypto market has disastrous consequences. In just 24 hours, the entire market liquidated over $1.02 billion in derivatives positions, affecting more than 220,000 traders. Bitcoin's price quickly fell from a historic high of over $124,000.

However, the key to this liquidation is not in its scale but in its extreme asymmetry. Among the liquidated positions, long positions reached $872 million, while shorts were only $145 million, a stark contrast. This indisputably proves that before the event occurred, the market had already been hijacked by excessive, one-sided bullish sentiment. Traders built up massive leveraged long positions but lacked sufficient risk hedging, resulting in a market structure that was 'top-heavy.' The PPI report merely pulled the trigger, while the bullet was already chambered. This flash crash was an inevitable and brutal correction of this internal structural imbalance.

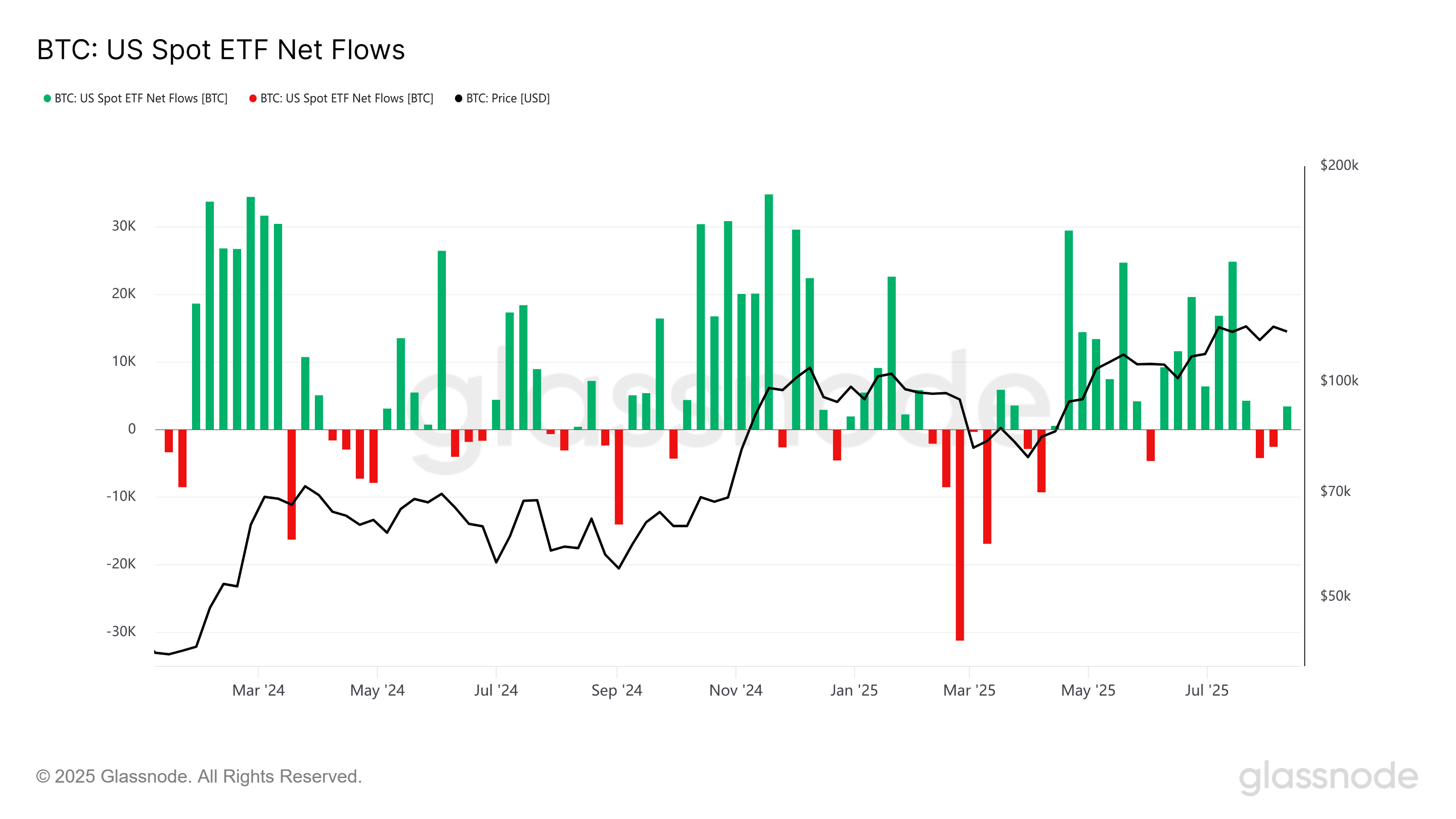

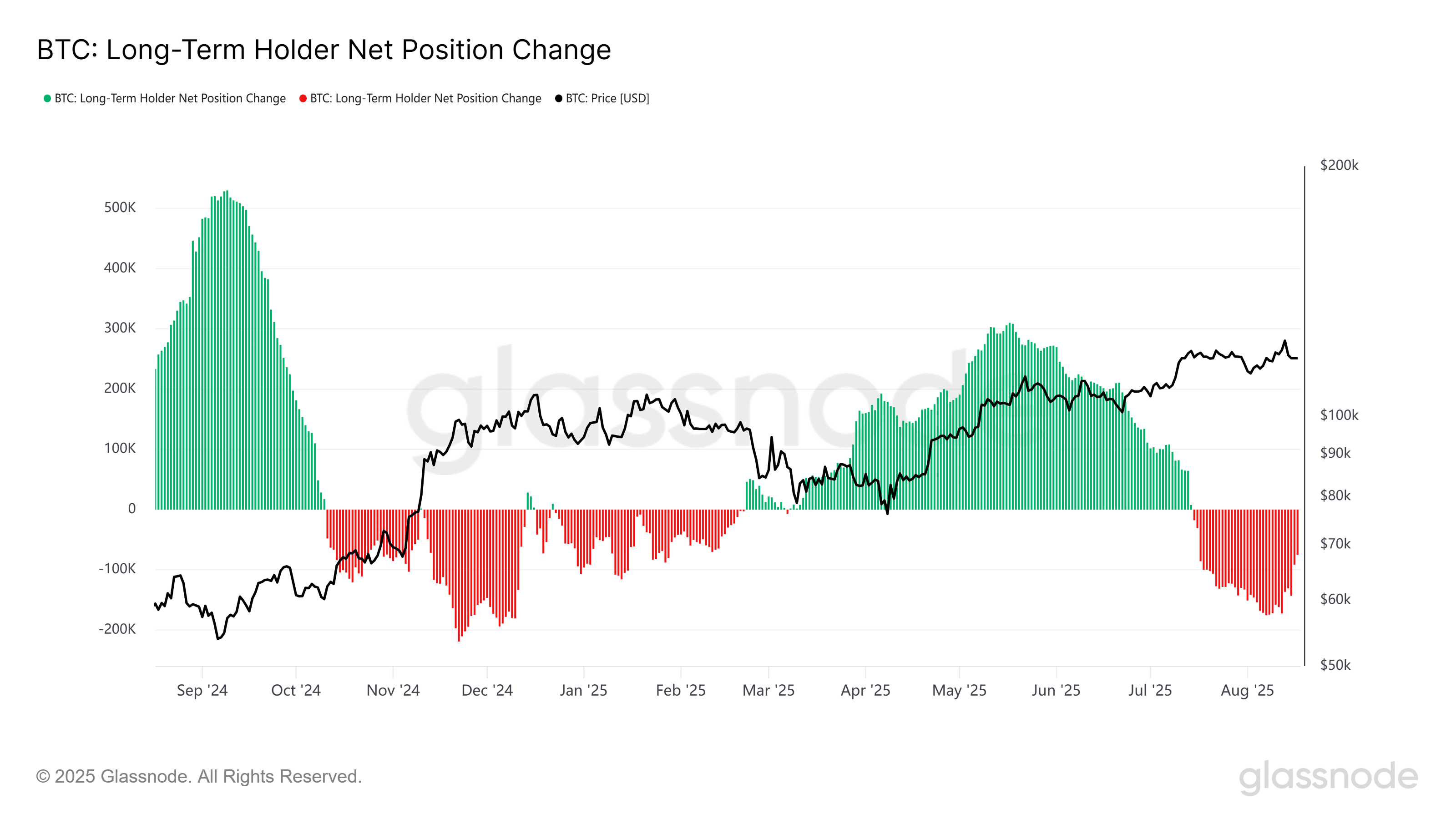

Historic Handover: ETF Demand Meets the 'Elder' Sell Wall

The first core contradiction of market stagnation lies in a historic asset handover between new and old capital.

First, we need to have an accurate understanding of the inflow of ETF funds. Despite high market sentiment, according to Glassnode data sources, the weekly net inflow of U.S. spot Bitcoin ETFs remained at a robust level of hundreds of millions in August. This institutional buying from Wall Street is real and ongoing, but it faces equally massive sell pressure.

So, who exactly is this 'mysterious opponent'? The answer is hidden in on-chain data. Glassnode's report reveals that July 2025 was one of the months with the most severe sell-offs in Bitcoin's history, with long-term holders realizing profits at a pace of up to $1 billion per day. These early market participants and builders are selling their held Bitcoin to new institutions entering through ETFs.

Putting these two sets of data together, the market stagnation is perfectly explained. This is not the engine of a bull market stalling, but rather an unprecedented capital rotation. For the first time in Bitcoin's history, there is one side composed of strictly regulated institutional buyers aiming for asset allocation, and on the other side, early holders who have experienced multiple cycles and seek to achieve life-changing wealth.

The current price stagnation reflects the dynamic balance achieved by these two forces. The inflow of ETF funds successfully absorbed the massive selling pressure from mature investors, averting a price collapse. From this perspective, the market's stagnation is precisely a sign of its maturity. This shift from 'belief-driven' to 'allocation-driven' asset transfer is bound to be long and fraught with friction, leading to price weakness in the short term.

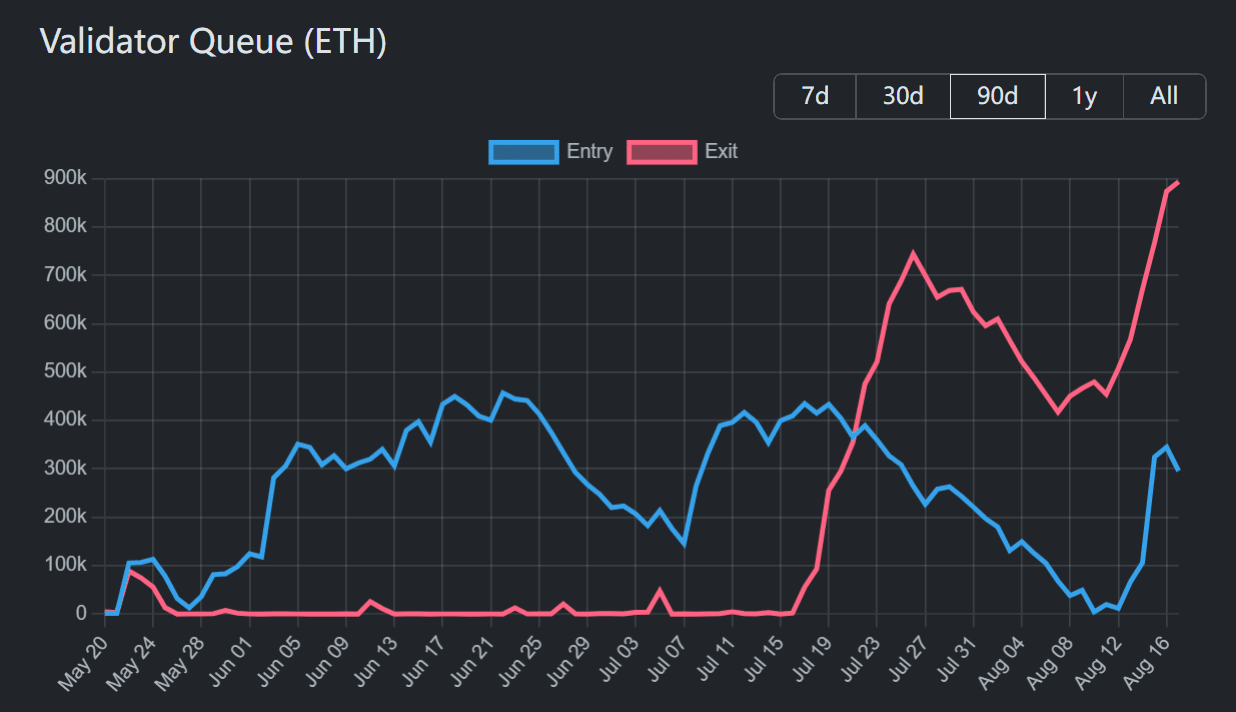

DeFi De-leveraging Engine: Continuous Headwinds from Ethereum Core

The second structural pressure in the market comes from within the Ethereum DeFi ecosystem, where a large-scale de-leveraging driven by protocol mechanisms is underway.

As of mid-August, the scale of validator exits on the Ethereum Beacon Chain reached a historical peak. Approximately $3.1 billion worth of ETH is queued to be unstaked, while only about $480 million is waiting to be staked. This severe imbalance in capital flow creates a powerful potential selling pressure.

The root cause is the collapse of a once-popular DeFi leveraged yield strategy. In the past, investors amplified returns by depositing staked ETH (such as stETH) into lending protocols like Aave, borrowing more ETH for re-staking. The core of this strategy relied on borrowing rates for ETH being lower than its staking yields. However, recent market volatility has caused borrowing rates to soar, even exceeding staking yields, turning the entire strategy from profitable to loss-making.

This forced all participants to close their positions, with the only way being: to unstake, retrieve original ETH, and repay loans. This series of forced actions directly led to a 'traffic jam' in the validator exit queue.

Unlike market sentiment-driven sell-offs, this selling pressure has two significant characteristics: mechanical and inelastic. It is a cold economic decision based on protocol rates, unrelated to market sentiment. Moreover, because the selling is to repay debt, this demand is rigid and will not dissipate due to price rebounds. Therefore, this $3.1 billion exit queue acts like a programmed sell order execution engine, continuously releasing ETH supply to the market at a predictable rate over the next few days, becoming a structural resistance that Ethereum's price struggles to overcome.

A Divided Market: Speculation and Hedging in Derivatives Trading

The third layer of pressure is reflected in the highly contradictory signals emanating from the derivatives market, revealing a 'split personality' market state.

On one hand, the market's speculative enthusiasm is vividly reflected in the altcoin space. The open interest of Litecoin (LTC) reached a historical peak of $1.27 billion, while Ripple (XRP) soared to over $3 billion. The surge in open interest reflects that a significant amount of leveraged funds is pouring into these high-volatility assets, pushing the entire market's risk appetite to the extreme.

However, on the other side of the market, professional players considered to be 'smart money' exhibit entirely opposite caution. In the Bitcoin options market, the open interest of put options with strike prices between $80,000 and $100,000 is nearly five times that of call options in the same range. This indicates that institutions and professional traders are spending real money to buy 'insurance' against potential large market corrections.

This contradictory state of speculation and hedging constitutes a typical 'barbell' market structure. The market's risk is allocated at two extremes: one end is speculative altcoin investors chasing high returns, while the other end is professional hedgers seeking extreme risk protection. The 'middle ground,' representing broad, robust, and medium-term bullish confidence, is remarkably empty. This inherent division makes the market structure extremely fragile, lacking a unified consensus to push prices beyond key resistance levels.

The Cost of Liquidity: When 'Risk-Free' Returns Are Too High

The fourth and most fundamental pressure comes from the high cost of dollar liquidity throughout the entire crypto ecosystem.

Currently, both centralized platforms and decentralized protocols generally maintain an annualized yield on dollar stablecoin deposits (APY) between 5% and 14%. Achieving such high returns on an asset pegged 1:1 to the dollar is unimaginable in the traditional financial world. It only indicates one thing: the market is extremely 'short of money,' and the demand for dollar liquidity is extremely high.

This high-yield environment creates a powerful 'liquidity black hole.' For funds and mature investors, when they can achieve nearly double-digit annualized returns on a low-risk asset, parking their funds in this safe harbor becomes an extremely rational choice.

This leads to a critical issue: new liquidity cannot effectively be transformed into fuel for price increases. A large amount of capital that could have flowed into Bitcoin or Ethereum is attracted by high interest rates, directly entering risk-free (or low-risk) arbitrage strategies. This capital is trapped in the 'money market' layer of the crypto ecosystem and fails to penetrate the 'capital market' layer, fundamentally weakening the market's upward momentum.

Conclusion: Beware of the boot named 'Interest Rate Cut'

In summary, the current market stagnation is a fragile balance resulting from four structural pressures acting together. Institutional buying is offset by the selling of early holders and hedging by professional investors; the DeFi de-leveraging engine continues to exert pressure; and high dollar funding costs suppress the willingness of new leveraged buying to enter the market.

Under such a fragile internal structure, the market seems to place its only hope on the macro expectation of the Federal Reserve about to enter a rate-cutting cycle. However, the ancient wisdom of financial markets repeatedly warns us: 'Buy the rumor, sell the news.'

When the boot of interest rate cuts truly lands, what the market may face is not a new round of celebration. Considering the ongoing inflationary pressure, the Fed's rate cuts are likely to be interpreted by the market as an official confirmation of potential economic recession. At that moment, the rate cut itself may transform from a bullish story about 'increased liquidity' to a bearish narrative about 'deteriorating economic fundamentals.'

This narrative shift is likely to become the trigger that ignites all current internal structural contradictions. At that time, a rate cut may not provide new upward momentum but could instead become the last straw that breaks the camel's back, triggering a deeper structural clearing.

On this temporarily stranded crypto vessel, the real test may have only just begun.