Traditionally, merchants often wait for days for accounts to settle before receiving payments, locking up funds and incurring high costs. Huma uses blockchain and stablecoins to convert bills or invoices (receivables) directly into cash, providing 'advances' to businesses through LOs (liquidity providers). Everything is completed in seconds, with funds immediately available for businesses to operate. In simple terms, it enables global payment institutions to settle seamlessly 24/7—that's the magic of PayFi.

How does its core operate?

1. Dual-track Product: Institutional vs. Retail (Huma 2.0)

Huma Institutional: This is the version for institutions and professionals, requiring KYC/KYB verification, suitable for enterprise-level approval processes, interfacing with real-world receivables (RWA).

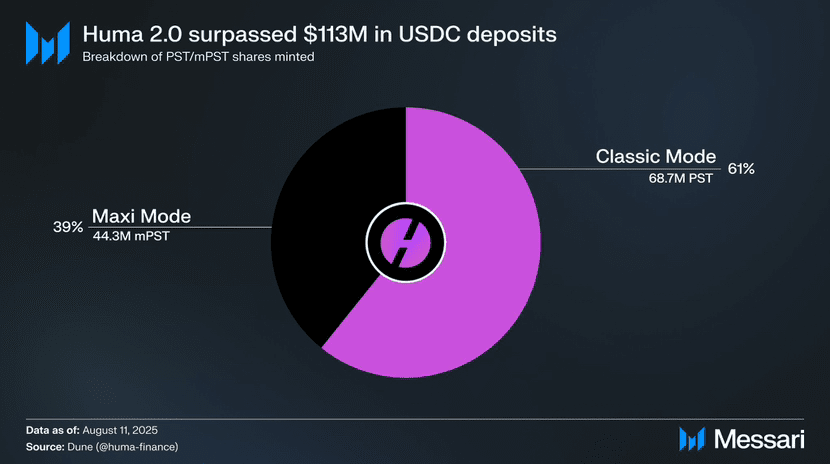

Huma 2.0 (Retail): Launching in April 2025, no KYC required to participate; everyone can deposit stablecoins, choose the Classic mode for dual income or the Maxi mode for more token rewards and points [Feathers].

2. PayFi architecture with a six-layer system.

From support of underlying chains like Solana, stablecoin settlement, to compliance modules and data processing that generates certificates, Huma has pieced together a complete on-chain funding penetration tool with 'transaction flow - currency flow - custody - compliance - financing - application'.

Where is the HUMA token useful?

Governance + tools: Holders can stake and participate in governance voting, such as adjusting protocol parameters and incentive mechanisms.

Reward Distribution: LPs providing funds or participating in ecosystem building can earn HUMA rewards; combined with the Feathers system, there are tiered rewards to enhance returns.

Burn Mechanism: 50% of the fees collected by the protocol will be used to buy back and burn HUMA, encouraging usage while creating deflation, supporting long-term token prices.

The total token supply is 1 billion, with an initial circulation of about 173 million, accounting for 17.33%, with clear allocations to LPs, investors, teams, airdrops, etc.

How reliable are its real achievements and collaborations?

Rich trading and credit data: To date, over $2.3 billion in credit lines have been issued, with transaction volume reaching $4.5 billion, and Huma 2.0 platform has over 53,000 active LPs, with locked funds reaching $50 million USDC.

Solid investment background: raised over $46 million, including $8.3M in angel round + $38M in Series A; backed by institutions like Circle, Stellar, and Galaxy Digital.

Institutional cooperation adds points: Huma has many paths deeply integrated with Circle’s USDC, Solana provides chain infrastructure support, and connects with DeFi tools like Kamino, RateX, and Jupiter.

What are the advantages? Why do users love it?

1. Efficiency is top-notch: Say goodbye to delays—receiving payments, financing, settlements are completed in seconds, especially suitable for small and micro enterprises, and new DeFi players.

2. Model Innovation: Truly linking offline cash flow (invoice receivables) to on-chain financing, coupling financial lines with DeFi.

3. Broad user coverage: Institutional lays the foundation, Huma 2.0 attracts the masses, running on both ends and expanding opportunities.

4. Smart Token Economics Design: Using burn incentives + lock-up + dual income mechanism to bind value to the ecosystem long-term.

But there are a few areas to keep a close eye on.

Regulatory risks are complex: on one side, real-world credit involves legal and financial regulations, while the other side is on-chain DeFi, with unclear regulatory paths.

Challenges in credit risk management: Although it has established a layered structure and risk control modules, who will assess borrowers and how to handle defaults, these mechanisms are a real test.

The market competition is fierce: other DeFi credit protocols and PoR projects are also vying for the PayFi track, and Huma needs to maintain differentiation to continue winning.

In one sentence, summarize whether it is worth watching:

Huma Finance is a PayFi network that combines 'invoice monetization' and 'on-chain financing', truly addressing the pain points of financial efficiency for intermediaries, enterprises, and payment institutions. It has technology, scenarios, and token mechanisms, making it a future-oriented infrastructure project worth keeping an eye on.