Written by: John Wang

Compiled by: AididiaoJP, Foresight News

Abstract

HIP-3 can transform prediction markets from static betting to high-leverage perpetual contracts, enabling permissionless trading on events such as elections and macroeconomic data.

Binary markets face extreme gap risk at expiration, making structural safeguards crucial. For example: liquidation intervals, margin adjustments based on open contracts, and leverage decay.

Scalar markets (settling by range) are a safer near-term goal, as their price paths are smoother, losses are proportional, and liquidation synchronicity is lower, thereby supporting higher leverage.

With reasonable design, HIP-3 can serve as a complement and alternative to Kalshi and Polymarket, combining leverage, shared liquidity, permissionless market creation, and potential on-site hedging capabilities, creating the fastest and most flexible prediction market trading platform.

Introduction and Opportunities

Prediction markets have long been slow, fixed payout, and non-leveraged trading venues. HIP-3 achieves permissionless deployment, shared liquidity, and customizable parameters by running on Hyperliquid's perpetual contracts. This allows users to trade binary or continuous outcomes on events such as elections, macro data, and sports with the same speed and capital efficiency as cryptocurrency perpetual contracts.

Combining the global liquidity of perpetual contracts with the richness of information in prediction markets will open up a new category of high-frequency, multi-event trading. However, without structural safeguards, leveraged trading in event markets can be very dangerous, especially for binary outcomes.

Challenges of binary leverage

Binary markets can gap from 0 to 100 at expiration, instantly destroying one side of the bettors and triggering a chain liquidation across the entire market. Without natural hedges, market makers will bear event risk directly, and liquidation cannot occur in phases. In the absence of protective measures, a safe leverage rate is only 1-1.5x.

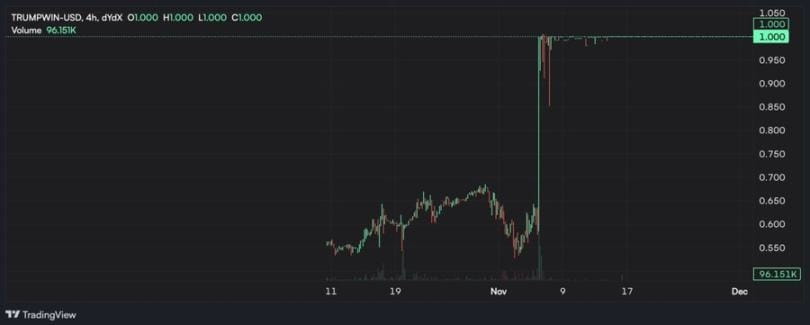

Example: dYdX's TRUMPWIN

On the eve of the 2024 U.S. presidential election, dYdX provided 20x leverage for the Trump victory market by allowing market makers to hedge on Polymarket's liquidity YES/NO contracts, supported by a mature liquidation mechanism, a large insurance fund, and socialized losses. Even so, the market price soared from about $0.60 to $1.00 on election night, leading to liquidity depletion during the liquidation process and triggering random deleveraging in an underfunded order book. Hedging delays, severe gaps, and liquidity disappearance caused traders who could have honored contracts to incur losses.

Currently, HIP-3 lacks on-site hedging of spot and gap risk control measures by default; thus, without built-in protection, similar chain reactions may still occur.

Construction based on external oracles.

Binary prediction perpetual contracts on HIP-3 will use BinaryHyperp contracts and rely on a probability oracle from 0 to 100. Strict limitations ensure trades occur only within market boundaries. If oracles reference Kalshi or Polymarket, liquidity providers can hedge in these spot markets, thereby reducing event risk and allowing for higher leverage. However, risks still exist, including hedging delays, liquidity gaps, and funding basis divergence.

Ensuring safe leverage

To raise the leverage of binary markets above 1x, structural controls are essential:

Liquidation intervals: splitting positions by price range. Lower ranges are prioritized for liquidation to control losses.

Margin coefficients based on open contracts: Margin requirements increase linearly based on open notional value: open_notional = OI × oracle_pricescaling_factor = (open_notional - lower_cap) / (upper_cap - lower_cap)effective_margin = min(base_margin + max(scaling_factor × (1 - base_margin), 0), 1.0)

Leverage decay: Gradually compressing the maximum leverage as the expiration date approaches and market volatility increases (e.g., 5x at 30 days, reduced to 1x on the last day).

Pre-settlement auction: Batch matching positions before the outcome is determined to avoid last-minute chaos.

Price and oracle limits: Restricting single price movement amplitudes and rate-limiting oracle updates to slow down chain reactions.

By combining these measures, the margin cap based on open contracts can control systemic risk, the liquidation intervals can stagger liquidation times, and leverage decay reduces tail risk on expiration dates.

Beyond binary: A breakthrough for scalar markets

Scalar markets settle based on ranges (such as CPI percentage or BTC dominance), rather than 0 or 100. This significantly reduces gap risk and supports higher leverage. Its main advantages include:

Smoother price paths: Most scalar markets settle based on gradually changing inputs (such as temperature, voting shares, or asset dominance).

Proportional loss: even if a gap occurs, the loss is only the deviation part, not the entire nominal value.

Predictable funding rates and liquidation: continuous pricing spreads the liquidation thresholds along the curve, reducing synchronous chain reactions.

Incremental pricing also naturally aligns with HIP-3's funding fees and margin logic, making scalar markets a safer breakthrough in the near term.

User experience of prediction perpetual contracts

Retaining the core elements of perpetual contracts (such as order books, depth charts, and leverage sliders), while adding components unique to prediction markets in the UI:

Clear question title

Yes / No options or scalar sliders

Payout visualization tools

Countdown to expiration

Mark price and oracle probability display

If the market hedges through external platforms like Kalshi or Polymarket, it must be prominently marked.

Comparison with the positioning of Kalshi and Polymarket

Kalshi and Polymarket are curated, fixed payout, and non-leveraged platforms. The differentiation of HIP-3 lies in:

Leverage: Scalar markets are safer, binary markets are engineered for optimization.

Permissionless market creation: Anyone can list new outcomes.

Shared liquidity: Access to the perpetual contract liquidity pool of Hyperliquid.

On-site hedging potential: Reduce event risk without leaving Hyperliquid.

This combination can attract professional liquidity providers and active traders, allowing HIP-3 to serve both niche event markets and cover high-traffic global outcomes.

Conclusion

Currently, no major team has publicly committed to the development of HIP-3 prediction perpetual contracts, but this situation is about to change. With reasonable design, liquidity, and permissionless market creation, HIP-3 can complement Kalshi and Polymarket, while also becoming an alternative.

The prediction market is about to sweep the globe, and as a blockchain that accommodates all financial activities, Hyperliquid will not miss this wave.