Original title: (IOSG Weekly Brief | Defection and Independence: Reassessing Appchain Arguments #288)

Original author: Jiawei, IOSG Ventures

Three years ago, we wrote an article on Appchain, triggered by dYdX announcing its decentralized derivatives protocol migration from StarkEx L2 to the Cosmos chain, launching its v4 version as an independent blockchain based on Cosmos SDK and Tendermint consensus.

In 2022, Appchain may have been a relatively marginal technical option. By 2025, with the launch of more Appchains, particularly Unichain and HyperEVM, the competitive landscape of the market is quietly changing, forming a trend around Appchains. This article will start from this point to discuss our Appchain Thesis.

The choices of Uniswap and Hyperliquid

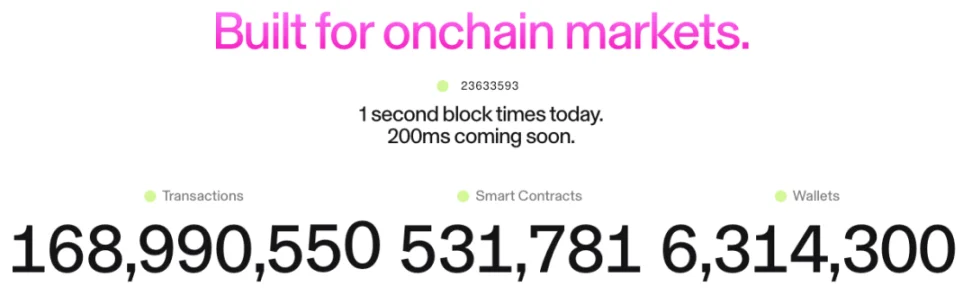

Source: Unichain

The concept of Unichain appeared early, with Nascent founder Dan Elitzer publishing 'The Inevitability of UNIchain' in 2022, highlighting Uniswap's scale, brand, liquidity structure, and demand for performance and value capture, pointing to the inevitability of its launch of Unichain. Since then, discussions about Unichain have been ongoing.

Unichain was officially launched in February today, with over 100 applications and infrastructure providers building on Unichain. The current TVL is approximately $1 billion, ranking among the top five of many L2s. In the future, Flashblocks with 200ms block times and the Unichain verification network will also be launched.

Source: DeFiLlama

As a perp, Hyperliquid clearly had a demand for Appchain and deep customization from day one. In addition to its core products, Hyperliquid also launched HyperEVM, which, like HyperCore, is protected by the HyperBFT consensus mechanism.

In other words, beyond its own powerful perp products, Hyperliquid is also exploring the possibility of building an ecosystem. Currently, the HyperEVM ecosystem already has over $2 billion in TVL, and ecosystem projects are beginning to emerge.

From the development of Unichain and HyperEVM, we can intuitively see two points:

The competitive landscape of L1/L2 is beginning to differentiate. The combined TVL of Unichain and HyperEVM ecosystems exceeds $3 billion. These assets should have been deposited in general-purpose L1/L2s like Ethereum and Arbitrum in the past. The top applications establishing themselves directly led to a loss of TVL, trading volume, trading fees, and MEV from these platforms.

In the past, L1/L2 coexisted with applications like Uniswap and Hyperliquid, where applications brought activity and users to the platform, and the platform provided security and infrastructure for applications. Now, Unichain and HyperEVM have become platform layers themselves, forming direct competition with other L1/L2s. They are not only competing for users and liquidity but also for developers, inviting other projects to build on their chains, significantly changing the competitive landscape.

The expansion paths of Unichain and HyperEVM are distinctly different from the current L1/L2. The latter often builds infrastructure first and then attracts developers with incentives. In contrast, Unichain and HyperEVM's model is 'product-first'—they first have a market-validated core product with a large user base and brand recognition, then build ecosystems and network effects around this product.

This path is more efficient and sustainable. They do not need to 'buy' ecosystems through high developer incentives but rather 'attract' ecosystems through the network effects and technological advantages of core products. Developers choose to build on HyperEVM because there are high-frequency trading users and real demand scenarios, not because of nebulous incentive promises. Clearly, this is a more organic and sustainable growth model.

What has changed in the past three years?

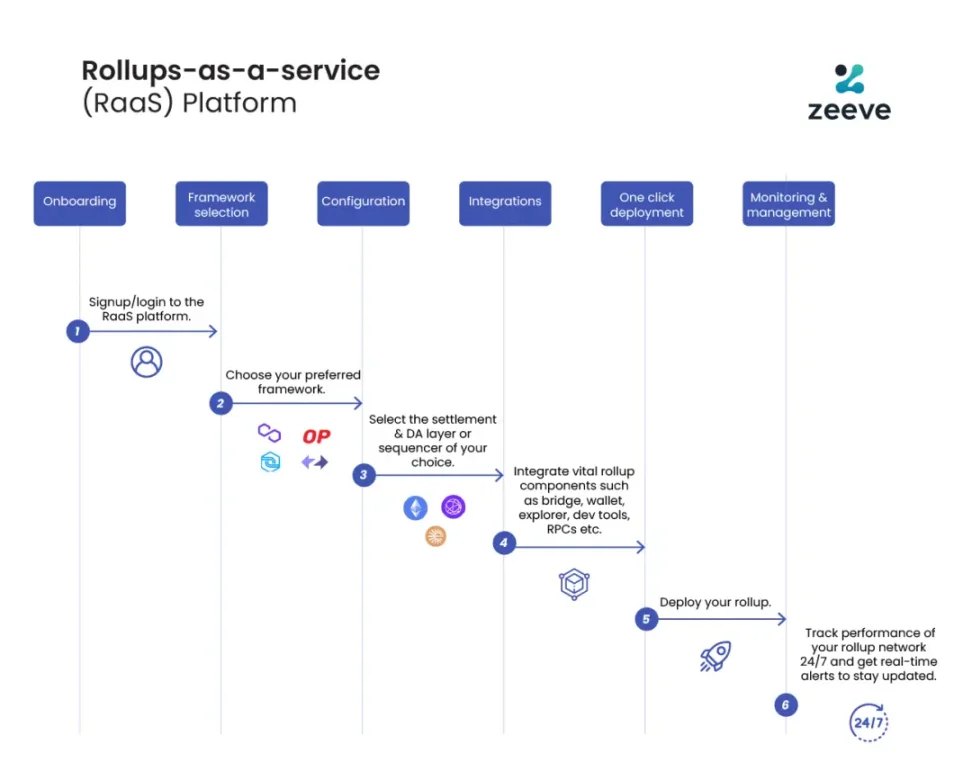

Source: zeeve

First, the maturity of the technology stack and the improvement of third-party service providers. Three years ago, building an Appchain required the team to master the full-stack blockchain technology, whereas with the development and maturity of RaaS services like OP Stack, Arbitrum Orbit, and AltLayer, developers can now assemble various modular components on-demand, significantly reducing the engineering complexity and upfront capital investment of building an Appchain. The operational model has shifted from building infrastructure in-house to purchasing services, providing flexibility and feasibility for application-layer innovation.

Secondly, brand and user perception. We all know that attention is a scarce resource. Users are often loyal to the application brand rather than the underlying technological infrastructure: users use Uniswap because of its product experience, not because it runs on Ethereum. As multi-chain wallets become widely adopted and UX improves further, users are almost unaware when using different chains—their touchpoints are often first the wallet and the application. When applications build their chains, users' assets, identities, and usage habits are settled within the application ecosystem, creating strong network effects.

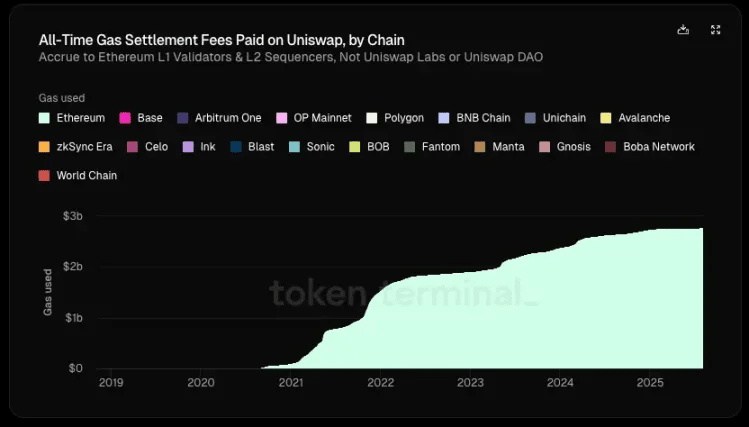

Source: Token Terminal

Most importantly, the pursuit of economic sovereignty by applications is slowly becoming prominent. In traditional L1/L2 architectures, we can see that the flow of value shows a clear 'top-down' trend:

· The application layer creates value (Uniswap's trading, Aave's lending)

· Users pay fees for using the application (application fees + gas fees), part of these fees goes to the protocol, and part goes to LP or other participants

· 100% of the gas fees flow to L1 validators or L2 sorters

· MEV is divided among searchers, builders, and validators in different proportions

· Ultimately, L1 tokens capture other values besides app fees through staking

In this chain, the application layer that creates the most value actually captures the least.

According to Token Terminal statistics, in Uniswap's total value creation of $6.4 billion (including LP earnings, gas fees, etc.), the distribution received by protocols/developers, equity investors, and token holders is less than 1%. Since its launch, Uniswap has generated $2.7 billion in gas revenue for Ethereum, which is about 20% of the settlement fees charged by Ethereum.

What if the application has its own chain?

They can capture gas fees for themselves, use their tokens as gas tokens; internalize MEV by controlling sorters to minimize malicious MEV, returning benign MEV to users; or customize fee models to implement more complex fee structures, etc.

In this view, seeking the internalization of value has become the ideal choice for applications. When applications have sufficient bargaining power, they will naturally demand more economic benefits. Therefore, high-quality applications have a weak dependence on the underlying chain, while the underlying chain has a strong dependence on high-quality applications.

Summary

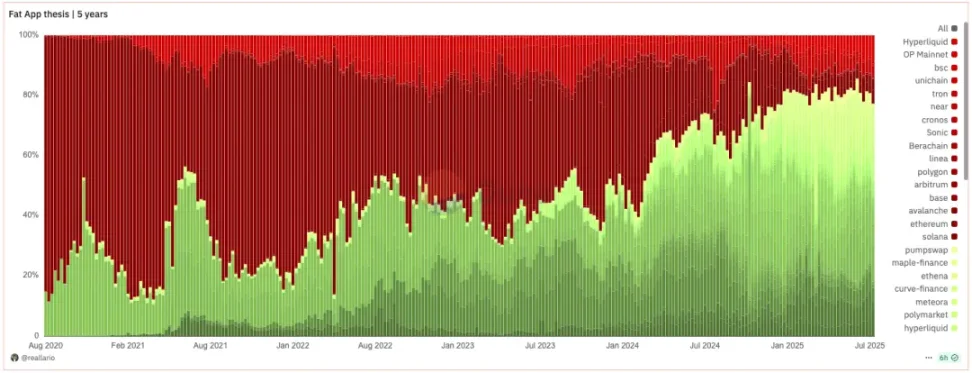

Source: Dune@reallario

The above chart roughly compares the revenues of protocols (in red) and applications (in green) from 2020 to the present. We can clearly see that the value captured by applications is gradually increasing, reaching about 80% this year. This may somewhat overturn Joel Monegro's famous theory of 'fat protocols and thin applications.'

We are witnessing a paradigm shift from the 'fat protocol' theory to the 'fat application' theory. Reflecting on the past pricing logic in the crypto space, which was primarily driven by 'technical breakthroughs' and underlying infrastructure, the future will gradually shift to a pricing method anchored by brand, traffic, and value capture ability. If applications can easily build their chains based on modular services, L1's traditional 'rent-seeking' model will be challenged. Just as the rise of SaaS reduced the bargaining power of traditional software giants, the maturity of modular infrastructure is also undermining L1's monopolistic position.

In the future, the market value of leading applications will undoubtedly exceed most L1s, and the valuation logic of L1 will shift from 'capturing total ecological value' to being a stable, secure decentralized 'infrastructure service provider.' Its valuation logic will be closer to that of public goods that generate stable cash flow, rather than 'monopolistic' giants that capture most ecological value. Its valuation bubble will be squeezed to some extent. L1 also needs to rethink its positioning.

Regarding Appchain, our view is that due to brand, user perception, and highly customizable on-chain capabilities, Appchain can better sediment long-term user value. In the 'fat application' era, these applications can not only capture the direct value they create but also build blockchains around themselves, further externalizing and capturing the value of infrastructure—they are both products and platforms; they serve end-users as well as other developers. In addition to economic sovereignty, top applications will also seek other forms of sovereignty: decision-making power for protocol upgrades, transaction ordering, censorship resistance, and ownership of user data, etc.

Of course, this article mainly discusses in the context of top applications like Uniswap and Hyperliquid that have already launched Appchain. The development of Appchain is still in its early stages (Uniswap's TVL on Ethereum still accounts for 71.4%). Also, protocols like Aave that involve wrapped assets and collateral and heavily rely on composability on one chain are not well-suited for Appchain. Relatively speaking, perpetuals that only require external demand from oracles are more suitable for Appchain. Furthermore, Appchain is not necessarily the best choice for mid-tier applications; specific situations need to be analyzed individually. This will not be elaborated further.

Original link