💠 Product: Details determine destiny

We often say that details determine destiny. Isn't it true that—product details also determine the fate of the project?!

Debridge cross-chain exchange, in addition to a smooth cross-chain experience, is one of the few products that supports inputting output amounts, with precision down to the decimal point.

Using Debridge to exchange assets across chains, you can exchange as much as you need, no longer having to worry about leaving a pile of small change on-chain.

On one hand, it really cures obsessive-compulsive disorder, and on the other hand, it reduces unnecessary waste of various small change.

💠 Ecosystem: A step further on a hundred-foot pole

Although deBridge is called a "bridge", it is actually more than just a bridge.

It is a cross-chain protocol that can be integrated into other applications. Currently, the OKX wallet and Phantom wallet have integrated deBridge, allowing asset cross-chain in the wallet.

Thus, the user base of deBridge is larger than it appears. On August 1, deBridge announced that the user count reached 1 million.

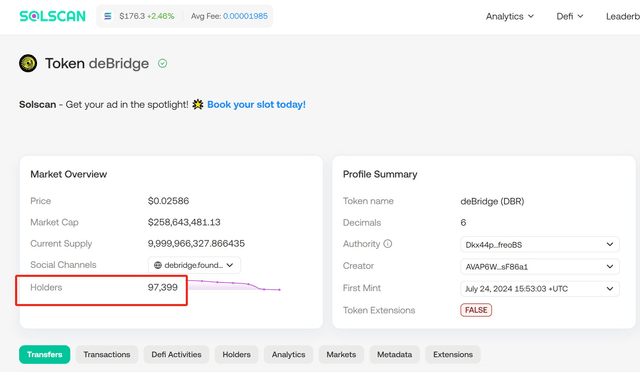

The reality is far more than that. There are nearly 100,000 on-chain holders of $DBR, not including those holding coins on CEX.

💠 Value: Motivation and Potential

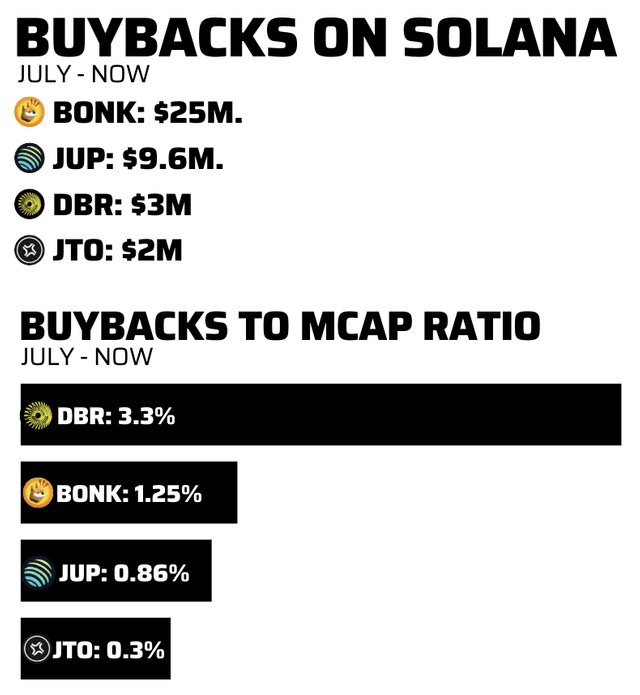

I noticed that a teacher overseas has compiled statistics on the ratio of repurchase amounts to market values of mainstream projects in the Solana ecosystem.

Among them, the repurchase ratio of $DBR is much higher than that of the other three projects. The highest repurchase ratio, $BONK, is less than half of that of $DBR.

Repurchase ratio = repurchase amount/market value

$DBR's repurchase ratio is noticeably higher for two reasons. First, the numerator (repurchase amount) is relatively large, and second, the denominator (market value) is relatively small.

On one hand, the repurchase motivation for $DBR is strong, as the deBridge foundation's funds participate in the DeFi of ecosystems like Solana, Ethereum, and Arbitrum, generating financial income and thus not relying on protocol income. Therefore, all protocol income is used for the repurchase of $DBR.

On the other hand, $DBR has significant value potential, and its market value is relatively low compared to the other three projects. Therefore, the repurchase ratio is greater.

Under the influence of such repurchase motivation and market value potential, $DBR may not be the largest in market value, but it could have the strongest growth potential.

💠 Written at the end

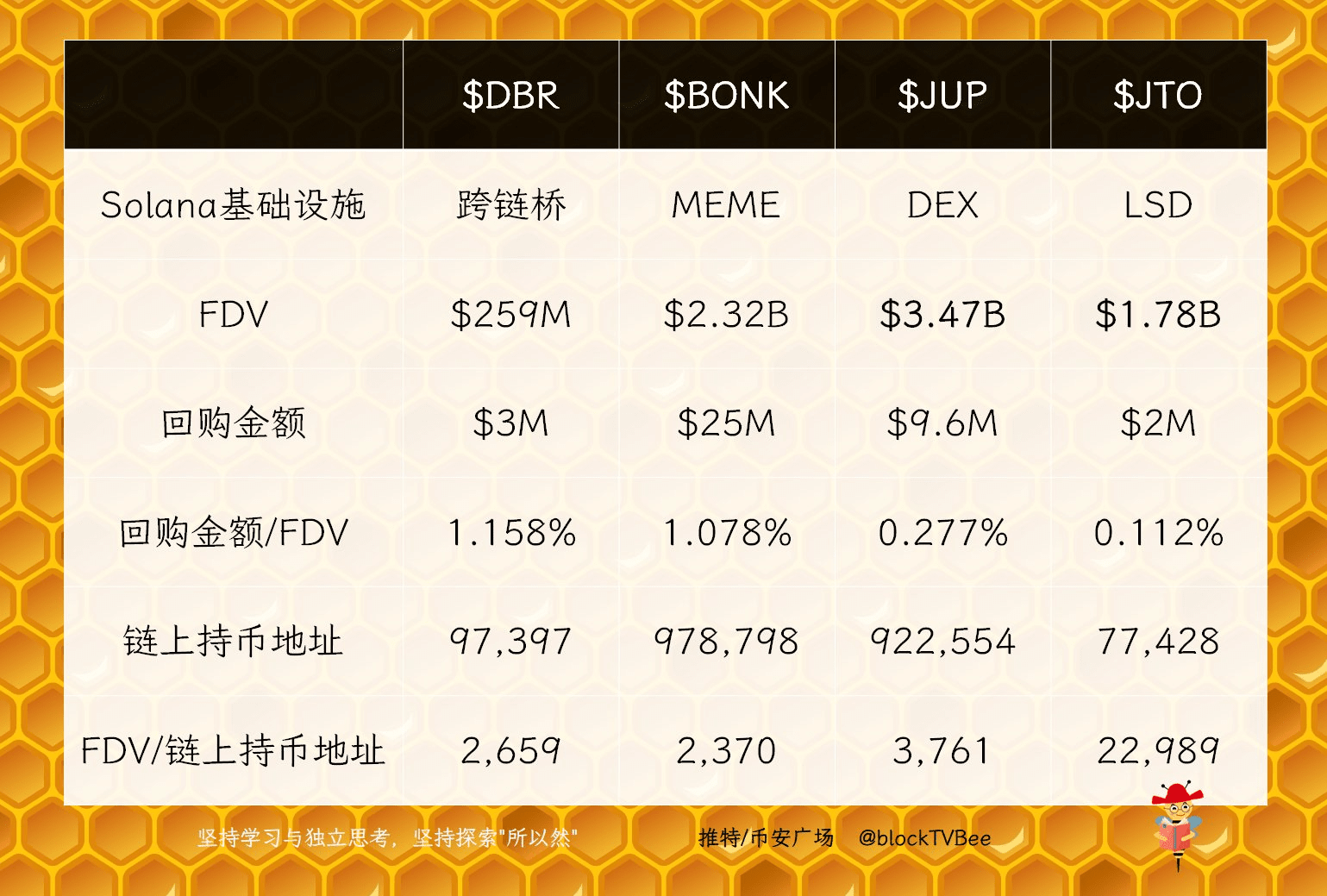

Considering the continuous release of tokens, Bee Brother has converted market value into FDV, calculating the repurchase amount/FDV, and FDV/on-chain holding addresses respectively.

Data comparison results:

In the Solana ecosystem infrastructure:

FDV/on-chain holding addresses reflect static value, $BONK and $DBR are relatively undervalued, while $JTO may be overvalued.

Repurchase amount/FDV reflects dynamic growth, $DBR and #BONK have stronger growth capabilities, while $JTO may have weaker growth capability.

Considering the product details of deBridge, the scarcity of $DBR, and the fact that deBridge, as a cross-chain bridge, connects more ecosystems, the potential of $DBR may be greater.