The White House is preparing to issue an executive order to punish banks that discriminate against cryptocurrency companies. Recently, this news has been widely circulated in social media circles. Those who have been in the cryptocurrency industry for over two years may find themselves rubbing their eyes in disbelief, exclaiming 'it's like a different era.'

However, just over a year later, in March 2023, the 'Choke Point Action 2.0' was fully implemented, with the Biden administration issuing a joint statement through the Federal Reserve, FDIC, OCC, and other agencies, categorizing cryptocurrency business as 'high-risk' and requiring banks to strictly assess the risk exposure of crypto customers. Regulatory agencies exerted informal pressure to force crypto-friendly banks like Signature Bank and Silvergate Bank to shut down core businesses and restrict new customer access. Builders of payment and trading platforms should particularly feel this impact, as publicly listed companies like Coinbase were caught in the middle, forced to invest hundreds of millions to establish independent banking relationships, while many small and medium-sized crypto startups registered offshore due to the inability to meet KYC/AML requirements.

The policy direction in the past month has swiftly redefined almost all types of crypto assets, including stablecoins, DeFi, ETFs, LSTs, etc. The accelerated entry of traditional financial institutions and the prevalence of crypto-stock companies have created a strong sense of disconnection. But aside from signaling the 'institutional' starting point, what opportunities can we find within these bills?

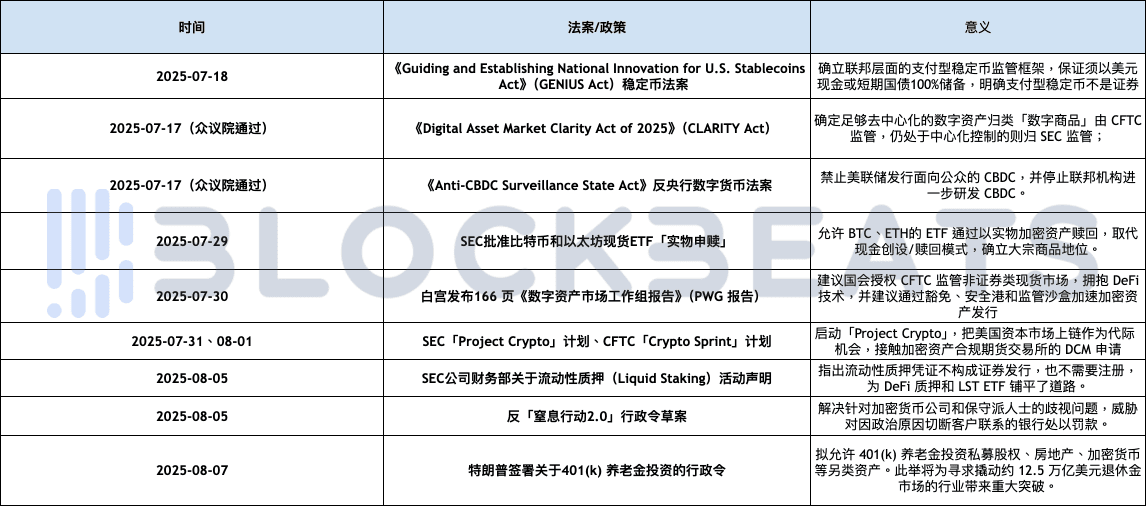

Four statements, three bills, and two executive orders.

Before interpreting, let's fully review some of the statements and initiatives launched by the US government and regulatory bodies from July to August; they appeared densely and fragmentarily, but together they piece together the current US crypto regulatory blueprint.

On July 18, Trump signed the GENIUS Act.

The bill establishes the first federal-level stablecoin regulatory framework in the US, including:

Stablecoins are required to be 100% backed by liquid assets such as US dollars or short-term Treasury bonds and to provide monthly disclosures.

Stablecoin issuers must obtain 'federal qualified issuer' or 'state qualified issuer' licenses.

The bill prohibits issuers from paying interest to holders and requires priority protection for stablecoin holders in the event of bankruptcy.

The bill explicitly defines payment stablecoins as neither securities nor commodities.

On July 17, the House of Representatives passed the CLARITY Act.

The bill aims to establish a market structure for crypto assets, including:

Clearly allocate jurisdiction to the CFTC (regulating digital commodities) and SEC (regulating restricted digital assets).

Allow projects to transition from securities to digital commodities through temporary registrations once the network matures, providing a safe harbor for developers, validators, and other decentralized participants. The CLARITY Act creates a (Securities Act) Section 4(a)(8) exemption for digital commodity issuance, with a financing cap of $50 million every 12 months, using 'mature blockchain systems' tests to determine whether a network has moved beyond the control of any person or team.

On July 17, the House of Representatives passed the Anti-CBDC Surveillance State Act.

The House of Representatives passed a bill prohibiting the Federal Reserve from issuing central bank digital currency (CBDC) to the public and forbidding federal agencies from researching and developing CBDCs. Congressman Tom Emmer explained that CBDCs could become 'tools for government surveillance.' This bill enshrines the president's prohibition against developing CBDCs into law to protect citizens' privacy and freedom.

On July 29, the SEC approved physical redemption for Bitcoin and Ethereum spot ETFs.

The committee approved that trading products for crypto assets such as Bitcoin and Ethereum can be created and redeemed with crypto assets in kind instead of cash, which means that Bitcoin and Ethereum are treated similarly to commodities like gold.

On July 30, the White House released a 166-page report (Digital Asset Market Working Group Report) (PWG report).

The White House's digital asset working group released a 166-page report proposing a comprehensive crypto policy blueprint, including:

Emphasize the establishment of a digital asset classification system to differentiate between security tokens, commodity tokens, and commercial/consumer tokens.

Request Congress to grant the CFTC the authority to regulate the spot market for non-security digital assets based on the CLARITY Act, and embrace DeFi technology.

It is recommended that the SEC/CFTC quickly allow the issuance and trading of crypto assets through exemptions, safe harbors, and regulatory sandboxes.

It is suggested to restart crypto innovation in the banking sector, allow banks to custody stablecoins, and clarify the process for obtaining Federal Reserve accounts.

On July 31 and August 1, SEC 'Project Crypto' plan and CFTC 'Crypto Sprint' plan.

In a speech at the SEC, Atkins launched the 'Project Crypto' initiative aimed at modernizing securities rules to bring US capital markets on-chain. The SEC will establish clear rules for the issuance, custody, and trading of crypto assets and ensure that traditional rules do not hinder innovation by using interpretations and exemptions until the rules are perfected, including:

Guide the issuance of crypto assets back to the US and establish clear standards distinguishing between digital commodities, stablecoins, collectibles, and other categories.

Revise custody regulations to emphasize citizens' right to self-custody digital wallets and allow registered intermediaries to provide crypto custody services.

Promote 'super apps' that enable broker-dealers to simultaneously trade securities and non-securities crypto assets on a single platform and provide staking, lending, and other services.

Update the rules to create space for decentralized finance (DeFi) and on-chain software systems, clarify the distinction between pure software publishers and intermediary services, and explore innovative exemptions to allow new business models to enter the market quickly under 'light compliance.'

Subsequently, on August 1, the CFTC officially launched the 'Crypto Sprint' regulatory program to work in tandem with Project Crypto. Four days later, on August 5, it further proposed to include spot crypto assets within CFTC-registered futures exchanges (DCM) for compliant trading, which means that exchanges like Coinbase or on-chain derivatives protocols can obtain compliance operation licenses through registration with DCM.

On August 5, the SEC's Division of Corporation Finance issued a statement regarding liquid staking activities.

The SEC's Division of Corporation Finance released a statement analyzing the liquid staking scenario, stating that liquid staking activities themselves do not involve securities trading, and that liquid staking receipt tokens (Staking Receipt Tokens) are not securities. Their value only represents ownership of the staked crypto assets rather than being based on the entrepreneurial or managerial efforts of third parties. This statement clarifies that liquid staking will not constitute an investment contract, providing clearer compliance space for DeFi staking services.

On August 5, the draft of the anti-'Choke Point 2.0' executive order.

The order aims to address discrimination against cryptocurrency companies and conservatives, threatening fines against banks that sever customer relationships for political reasons and taking consent orders or other disciplinary actions. Reports indicate that the executive order also directs regulators to investigate whether any financial institutions have violated the Equal Credit Opportunity Act, antitrust laws, or consumer financial protection laws.

On August 7, Trump signed an executive order regarding 401(k) pension investments.

It is proposed to allow 401(k) pension funds to invest in private equity, real estate, cryptocurrencies, and other alternative assets. This will bring a significant breakthrough for the industry seeking to tap into the approximately $12.5 trillion pension market.

In the era of the Super App where everything is on-chain, which crypto sectors can benefit from policy dividends.

Thus, the compliance framework for the US in the crypto field has been established. The Trump administration established the fundamental position of 'stablecoins' with the stablecoin bill and anti-central bank digital currency bill, tying them to US Treasury bonds and linking them to global liquidity, thus allowing stablecoins to be extended into various crypto domains without worry. The genius CLARITY Act defined the jurisdiction of the SEC and CFTC. Furthermore, from July 29 to August 5, four statements were issued in just one week, more related to on-chain matters, from opening the BTC and ETH ETFs 'physical redemption' to information about liquid staking receipts, all aimed at first connecting the channels of 'old money' to the on-chain before using 'DeFi yields' to expand more financial systems on-chain. The two executive orders issued in the past two days have genuinely injected 'bank' and 'pension' money into the crypto space. This series of moves has ushered in the first genuine 'policy bull market' in crypto history.

Regarding Atkins’ mention of a key concept when launching Project Crypto, the term 'Super App' refers to the 'horizontal integration' of product services. In his vision, a single application in the future can provide customers with comprehensive financial services. Atkins stated, 'Broker-dealers with alternative trading systems should be able to simultaneously provide trading in non-security crypto assets, crypto asset securities, and traditional securities, as well as staking and lending services for crypto assets, without needing to obtain licenses from over 50 states or multiple federal licenses.'

When discussing this year's hottest candidates for the Super App, traditional brokers Robinhood and the earliest 'compliant' trading platform Coinbase are undoubtedly at the forefront. While Robinhood this year acquired Bitstamp, launched tokenized stocks, and collaborated with Aave to bring them on-chain (where trading on the platform and on-chain can occur simultaneously), Coinbase further integrated its Base chain ecosystem and the Coinbase exchange's channels and upgraded the Base wallet into a unified app that integrates social and off-chain application services. However, the various areas under the Super App backdrop are truly where RWA will explode.

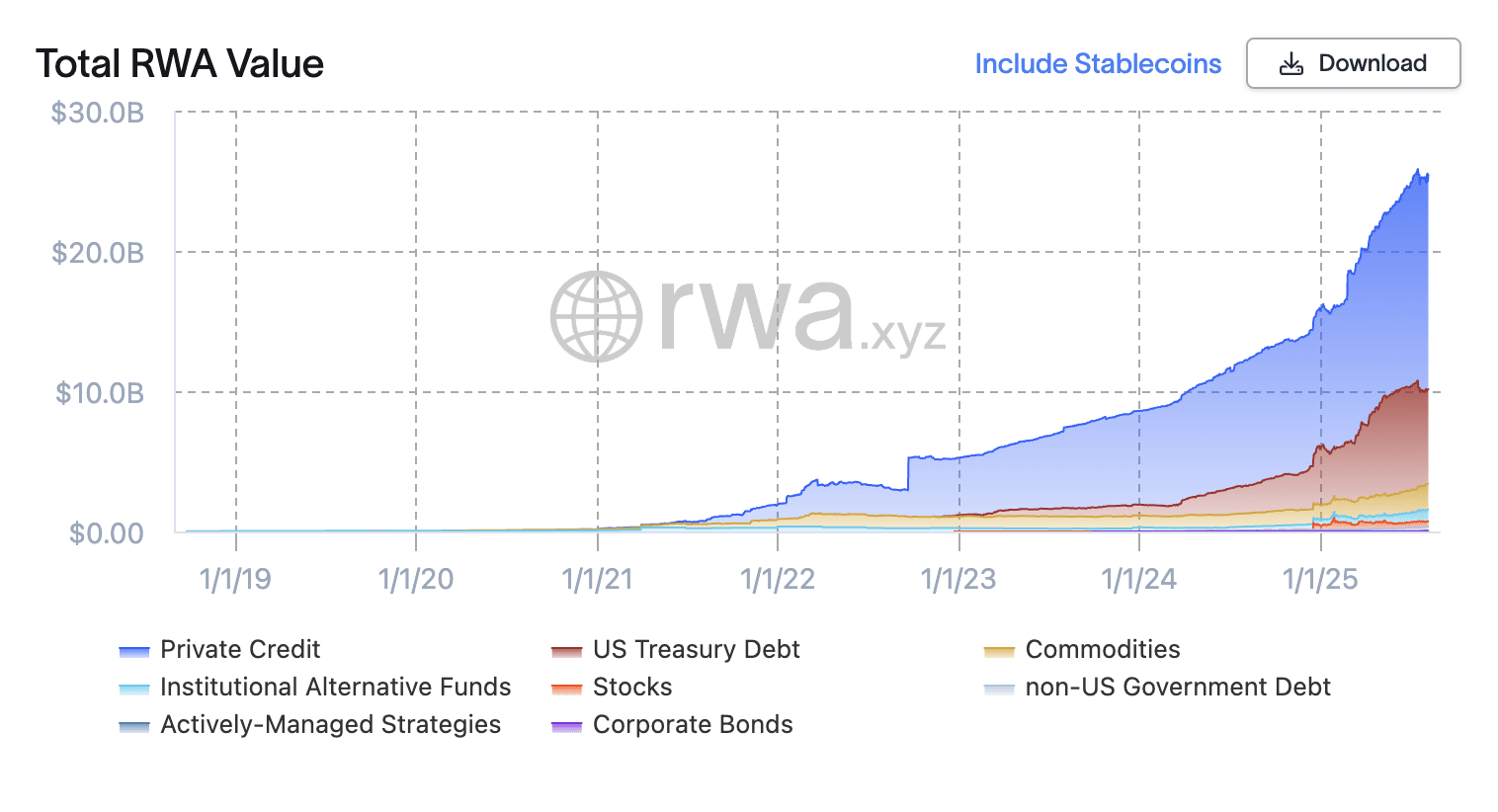

With policy encouragement for traditional assets to go on-chain, Ether bonds, tokenized stocks, and tokenization of short-term Treasury bonds will gradually enter compliant pathways. According to data from RWA.xyz, the global RWA market is expected to grow from about $5 billion in 2022 to about $24 billion by June 2025. However, rather than calling this RWA, it is better to consider them as Fintech, as their purpose is to make financial services more efficient in terms of systems and technology. From the real estate investment trusts (REITs) born in the 1960s, E-gold, to the emergence of ETFs, after countless experiments and failures, they have finally become RWA.

Currently, after being recognized by the policy system, they have become the most reliable endorsement, and their market will be huge. The Boston Consulting Group believes that by 2030, 10% of global GDP (about $16 trillion) can be tokenized, while Standard Chartered estimates that tokenized assets will reach $30 trillion by 2034. Tokenization opens exciting new doors for institutional firms by reducing costs, streamlining underwriting, and increasing capital liquidity. It also helps improve returns for investors willing to take on more risk.

The essence of stablecoins is on-chain Treasury bonds.

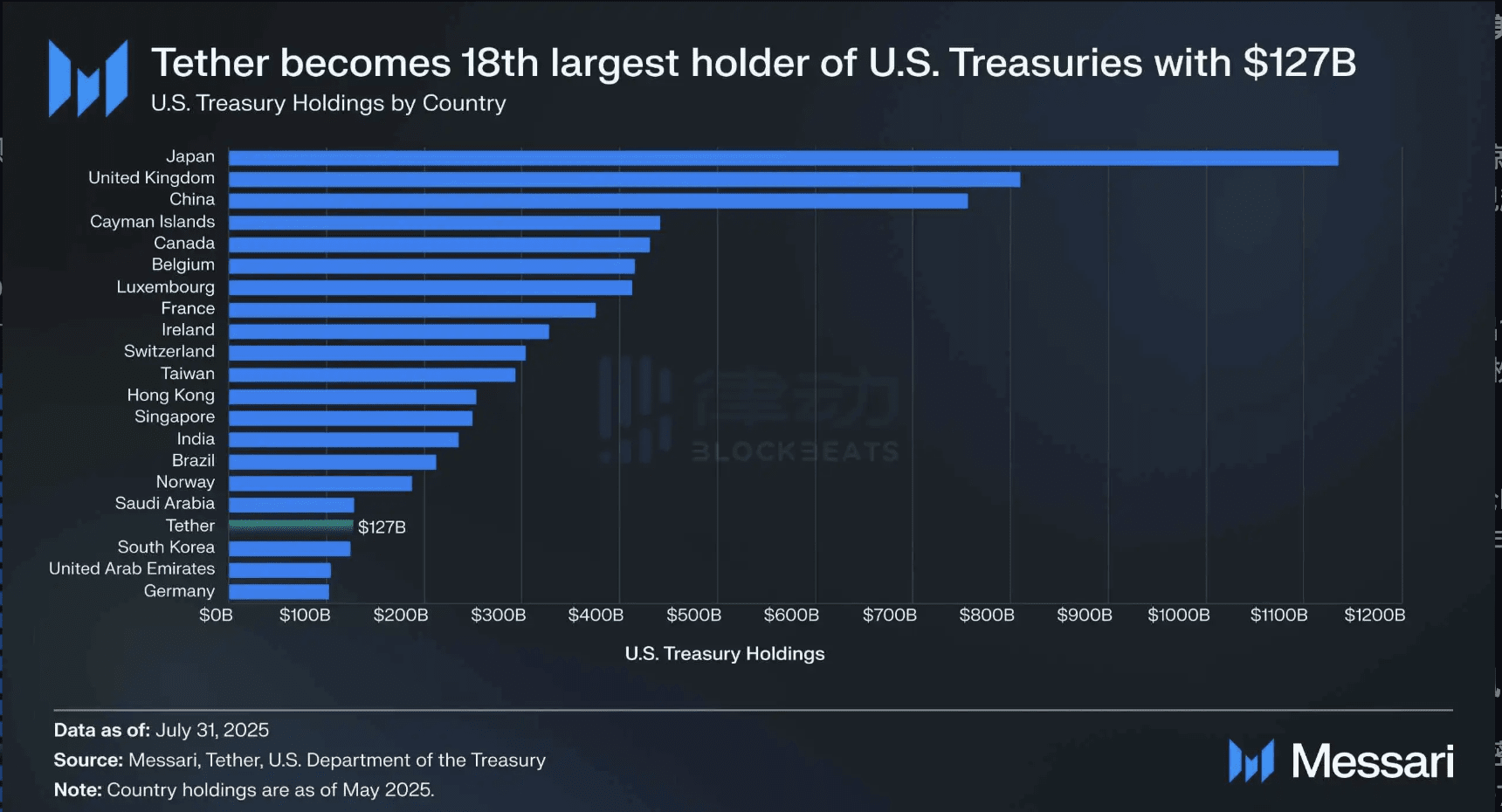

When discussing RWAs in cryptocurrencies, dollar assets, especially dollar currency and US Treasury bonds, always occupy the center stage. This is the result of nearly 80 years of economic history, with the Bretton Woods system of 1944 evolving to make the dollar the pillar of global finance. Central banks around the world hold the majority of their reserves in dollar-denominated assets, with about 58% of official foreign exchange reserves held in dollars, most of which are invested in US Treasury bonds. The US Treasury bond market is the largest bond market in the world, with approximately $28.8 trillion in outstanding bonds and unparalleled liquidity. Foreign governments and investors hold about $9 trillion of this debt.

Historically, there have been almost no assets that match the depth, stability, and credit quality of US Treasury bonds. High-quality government bonds are the cornerstone of institutional portfolios, used for safely storing capital and as collateral for other investments. The crypto world has leveraged the same fundamentals, and since stablecoins became the largest 'entrance and exit' of crypto, the relationship between the two has deepened more than ever.

Although on one hand, cryptocurrencies have not fulfilled Satoshi Nakamoto's expectation of 'establishing an alternative to the dollar system,' they have instead become a more efficient infrastructure based on the dollar's financial establishment. This has become a necessary condition for the US government to 'fully accept its existence'; in fact, the US government may need it more than ever.

With the recent addition of countries like Saudi Arabia, the UAE, Egypt, Iran, and Ethiopia, the GDP sum of the BRICS group is expected to reach $29.8 trillion in 2024, surpassing the US's GDP of $29.2 trillion, meaning the US is no longer the largest economic group in the world by GDP. Over the past two decades, the growth rate of BRICS countries has significantly outpaced that of the G7.

As of May 15, 2025, US Treasury data shows that Tether's holdings of US Treasury bonds exceed those of South Korea, source: Messari.

Stablecoins, closely related to this, hold a unique position in the global financial landscape, serving as the most liquid, efficient, and user-friendly wrappers for short-term US Treasury bonds, effectively addressing two barriers related to de-dollarization: maintaining the dollar's dominance in global transactions while ensuring continued demand for US Treasury bonds.

As of December 31, 2024, stablecoin holders reached 15% to 30% of the total traditional dollar development over five years, source: Ark Investment.

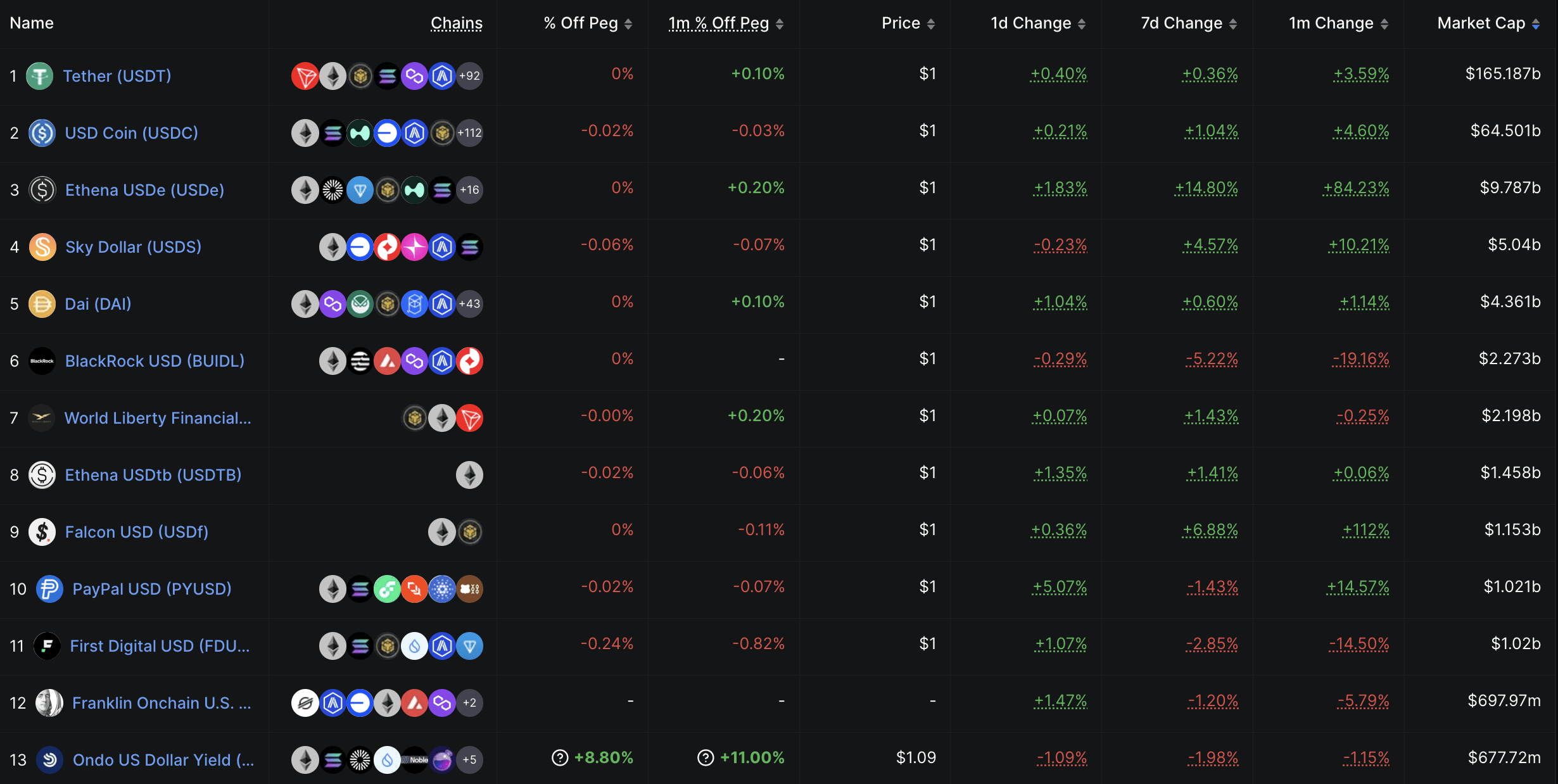

Dollar stablecoins such as USDC and USDT provide traders with a stable trading currency and are supported by the same bank deposits and short-term Treasury bonds relied upon by traditional institutions. In these Treasury bond stablecoin scenarios, the Treasury income is not owned by the holding users, but more on-chain financial products will incorporate the concept of US Treasury bonds, with two main methods to build tokenized treasury bonds on-chain: yield generation mechanisms and base token mechanisms.

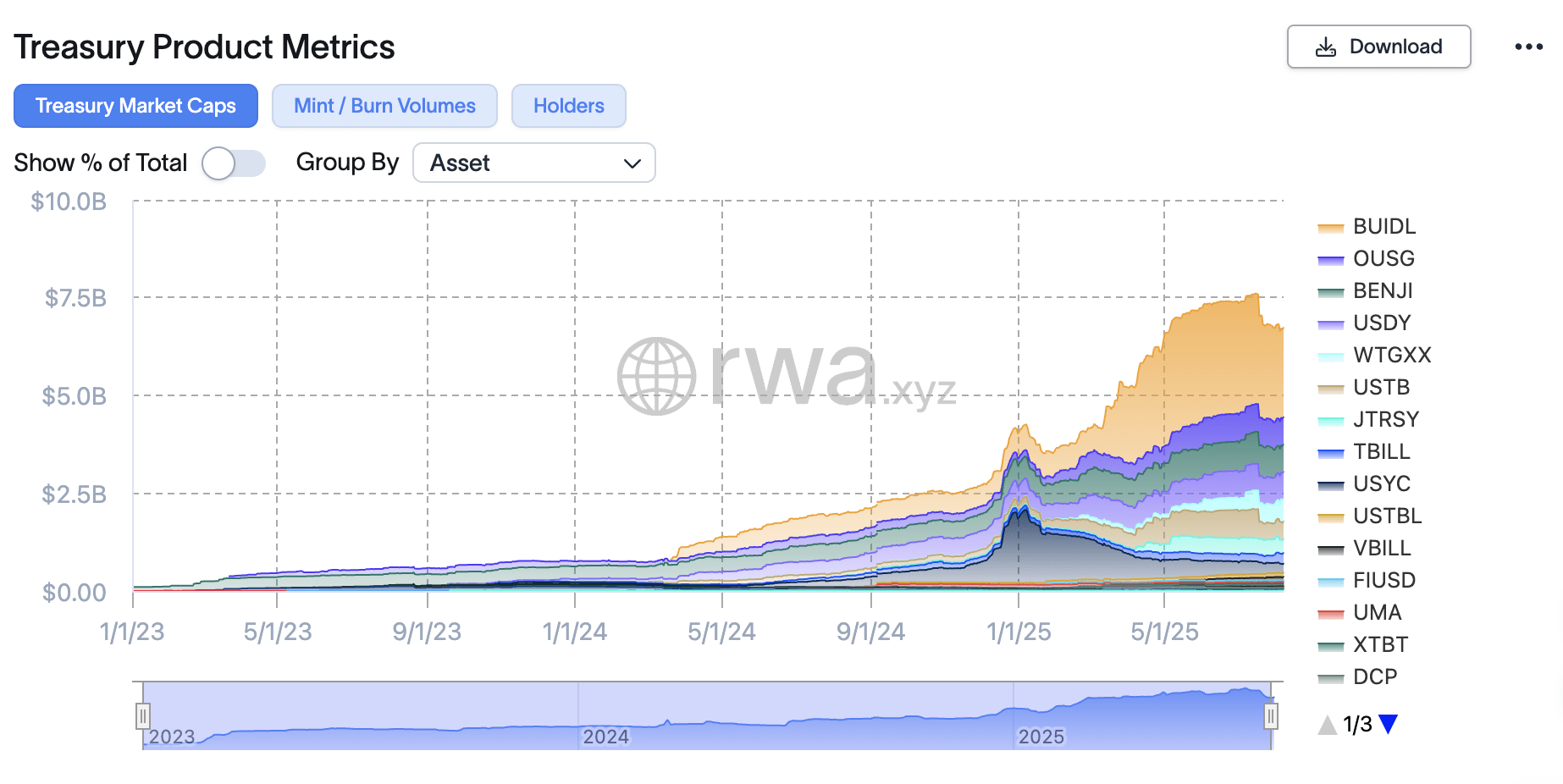

For example, yield tokens like Ondo's USDY and Circle's USYC use various mechanisms to increase asset pricing to accumulate base returns. In this model, due to cumulative yields, the price of USDY after six months will be higher than today. In contrast, base tokens like BlackRock's BUIDL and Franklin Templeton's BENJI or Ondo's OUSG maintain dollar parity through pre-defined intervals of new token distributions.

Whether 'yield stablecoins' or 'tokenization of US Treasury bonds', just like the adoption of fund portfolios in TradFi, on-chain financial products use on-chain US Treasury bonds as a stable income component, which has become a substitute for high-risk DeFi, allowing crypto investors to obtain stable annual yields of 4-5% with minimal risk.

Extended reading: (The stablecoin bill in hand and the restlessness of Wall Street bankers)

The easiest area to make money is on-chain credit.

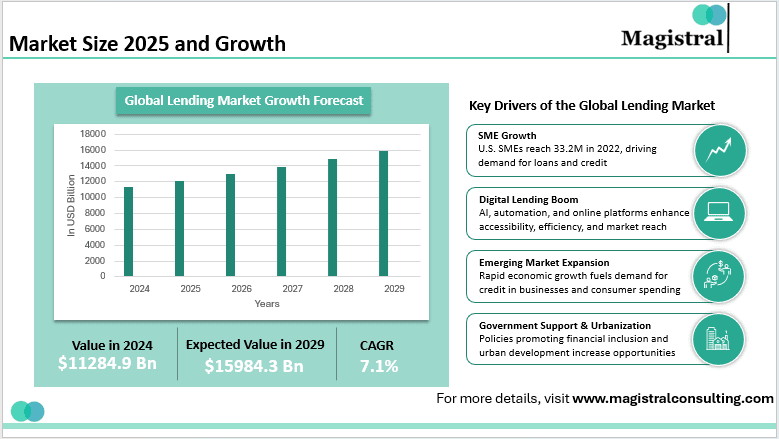

The traditional lending industry is one of the core profit sectors of the financial system. According to research from Magistral Consulting, the global credit market is expected to reach $11.3 trillion in 2024 and $12.2 trillion in 2025. In contrast, the entire crypto lending market is still below $30 billion, but the yields are generally around 9-10%, significantly higher than traditional finance. If regulations are no longer restrictive, it will unleash tremendous growth potential.

In March 2023, a research team led by Giulio Cornelli at the University of Zurich published a paper in the Journal of Banking & Finance on the importance of loans from large tech companies. The study showed that a clear regulatory framework for fintech can double the growth of new lending activities (some research indicated that FinTech lending volumes grew by 103% when clear regulations were in place). The principle remains the same for crypto lending: clear policies attract capital.

Lending market size, source: Magistral consulting.

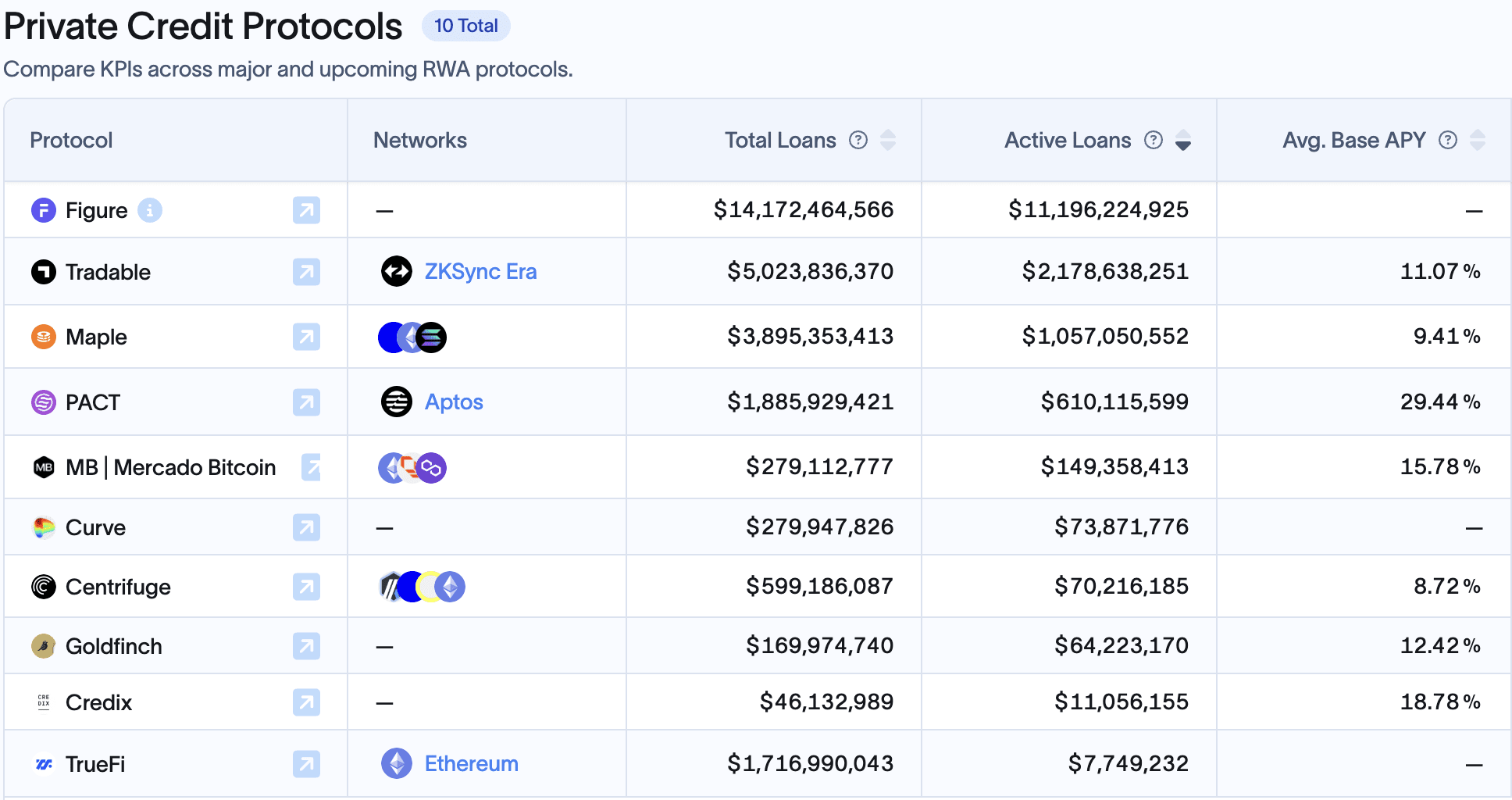

Therefore, in this period of increasing asset tokenization in the RWA field, one of the biggest beneficiaries of compliance may be the on-chain lending industry. Currently, the Crypto field lacks the 'government credit score' system of big data support found in traditional finance, thus it can only focus on 'collateralized assets.' Hence, private credit assets account for about 60% of on-chain RWA, approximately $14 billion.

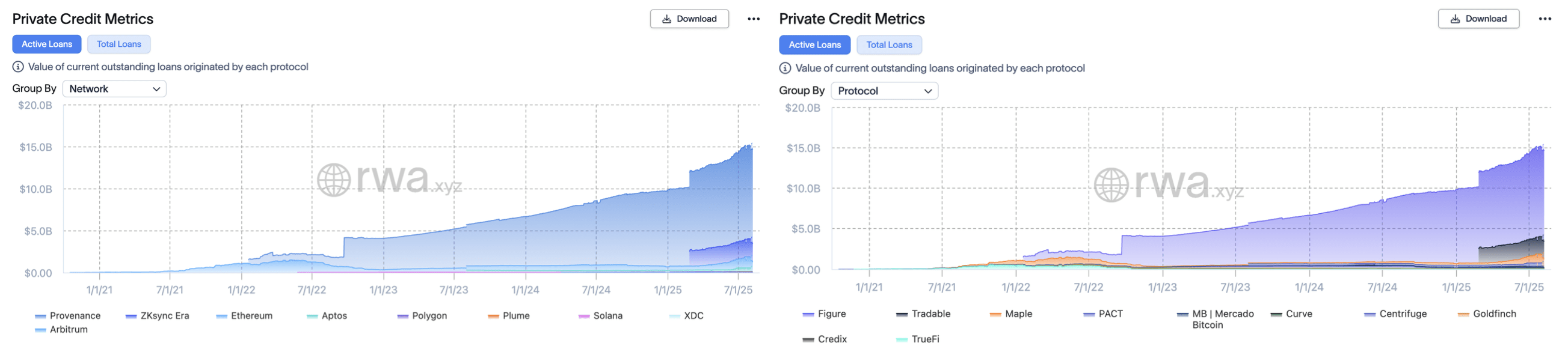

Behind this wave is the deep involvement of traditional institutions, the largest among which is Figure, which is recently discussing its IPO. They launched the Provenance Cosmos ecosystem chain designed specifically for asset securitization and loan finance scenarios, having managed about $11 billion in private credit assets as of August 10, 2025, accounting for 75% of that track. Its founder, Mike Cagney, the former founder of SoFi, as a 'serial entrepreneur' in the lending field, is adept at blockchain lending, with the platform connecting the entire chain from loan initiation, tokenization, to secondary trading.

The second place is Tradable, leveraging a partnership with Janus Henderson, which has $330 billion in assets under management. They tokenized $1.7 billion in private credit on Zksync at the beginning of the year (making Zksync the second-largest 'lending chain'), while the third place is Ethereum, the 'world computer', but its market share in this field is only 1/10 of Provenance.

Left: 'Credit Public Chain' market cap, Right: Credit project market cap, source: RWAxyz.

Extended reading: (From scandals to the first RWA stock, Figure's 'American Scam')

(Bitcoin mortgages, a new blue ocean worth $6.6 trillion)

DeFi native platforms are also entering the RWA lending market. For example, Maple Finance has facilitated over $3.3 billion in loans, with approximately $777 million currently active, some targeting real-world receivables. MakerDAO has also begun allocating real assets like treasury bonds and commercial loans, with platforms like Goldfinch and TrueFi laying early groundwork.

All of this was suppressed under a hostile regulatory environment, but now the 'warming of policies' may completely activate this sector.

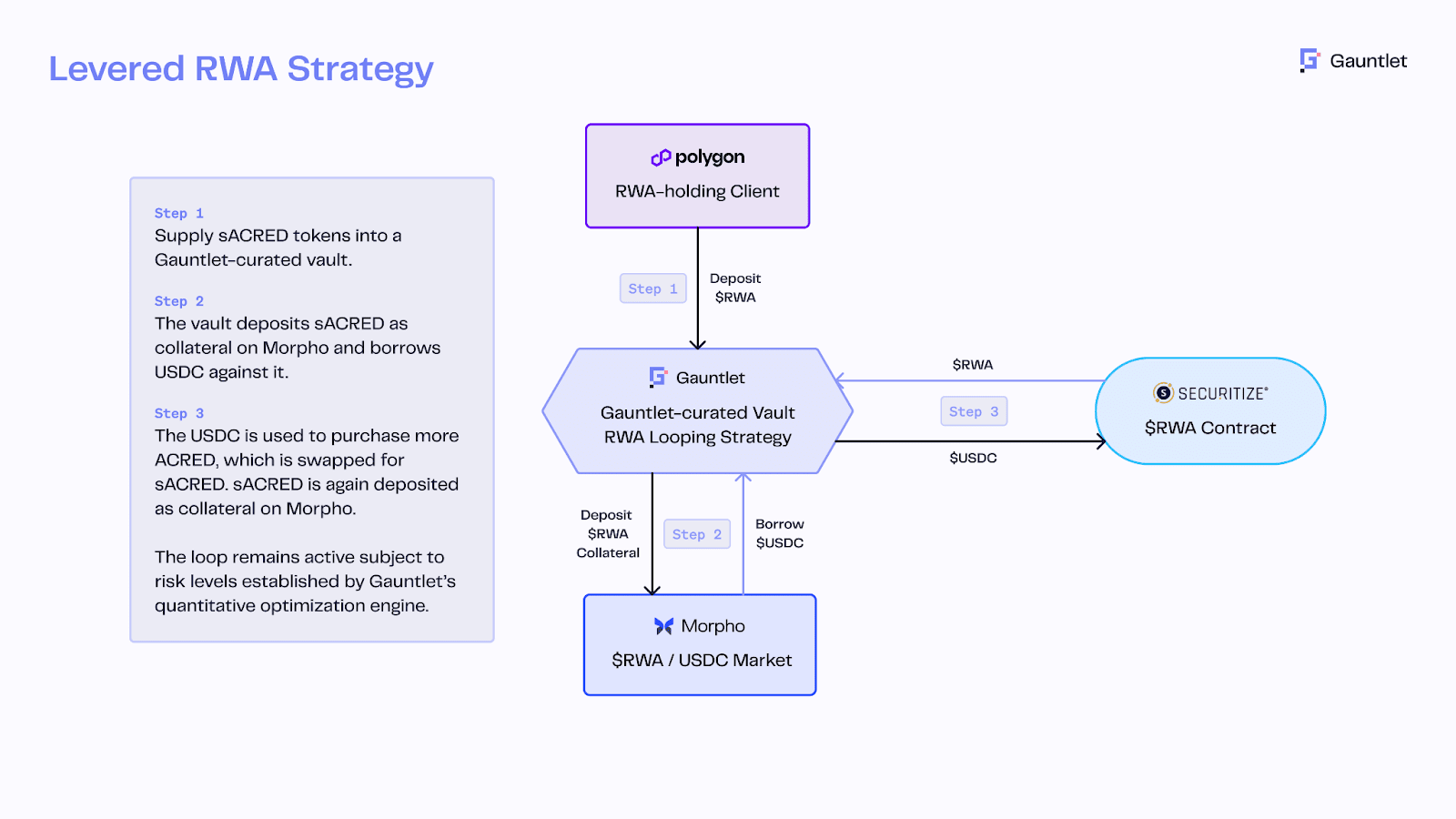

For example, Apollo launched its flagship credit fund, the tokenized fund of ACRED, allowing investors to mint sACRED tokens representing their shares through Securitize, and then use those tokens for lending arbitrage operations on DeFi platforms (like Morpho on Polygon). Using the RedStone price oracle and Gauntlet risk control engine, sACRED is collateralized to borrow stablecoins, then leveraged to repurchase ACRED, thus leveraging a 5-11% base yield to 16% annualized. This innovation combines institutional credit funds with DeFi leverage.

sACRED circular lending structure, source: Redstone.

In the long run, 401(k) reforms will indirectly benefit on-chain credit. Wintermute's OTC trader Jake Ostrovskis stated that the impact of this move cannot be underestimated. 'Just a 2% allocation to Bitcoin and Ethereum is equivalent to 1.5 times the total inflow of ETF funds to date, and a 3% allocation would more than double the overall market inflow. The key is that these buyers are mostly price insensitive; they focus on meeting allocation benchmarks rather than making tactical trades.' The return demands of traditional pensions are likely to spur interest in investing in stable, high-yield DeFi products. For example, tokenized assets based on real estate debt, small business loans, and private credit pools, if packaged properly for compliance, may become new choices for pensions.

Current market share of the top 10 on-chain lending projects, source: RWAxyz.

Under clear regulations, these institutional-level 'DeFi credit funds' may rapidly replicate. After all, most large institutions (Apollo, BlackRock, JPMorgan) have regarded tokenization as a key tool to enhance market liquidity and yields. After 2025, as more assets (such as real estate, trade financing, and even mortgages) are tokenized on-chain, on-chain credit is expected to become a multi-trillion-dollar market.

Transform the 'American value' of 5*6.5 hours into a 'chain-based US stock market' that the whole world can play 7*24 hours.

The US stock market is one of the largest capital markets globally. As of mid-2025, the total market capitalization of the US stock market is approximately $50-55 trillion (USD), accounting for 40%-45% of the total global market capitalization. However, such a massive 'American value' has long been limited to trading within a window of about 6.5 hours on weekdays, with evident regional and time constraints. Now, this situation is being rewritten, as on-chain US stocks allow global investors to participate in the US stock market 7×24 hours without interruption.

On-chain US stocks refer to the digitization of the stocks of US-listed companies into tokens on the blockchain, with prices pegged to real stocks and backed by actual stocks or derivatives. The biggest advantage of tokenized stocks is that trading times are no longer limited: traditional US stock exchanges are only open for about 6.5 hours on working days, while blockchain-based stock tokens can trade continuously around the clock. Currently, the tokenization of US stocks is primarily achieved through three directions: third-party compliant issuance + multi-platform access model, licensed brokers' self-issuance + closed-loop on-chain trading, and contract for differences (CFD) model.

Extended reading: (How is US stock tokenization achieved from Robinhood to xStocks?)

Currently, various projects related to the tokenization of US stocks have emerged in the market, from Republic's 'Pre IPO' mirror coins to Hyperliquid's ability to long and short 'Pre IPO' with Ventuals, to Robinhood and multiple institutional partnerships causing dual tremors in both the TradFi and crypto circles, allowing users to receive stock dividends through MyStonk, and the upcoming integration of brokerage + on-chain token dual-track gameplay with DeFi by StableStock.

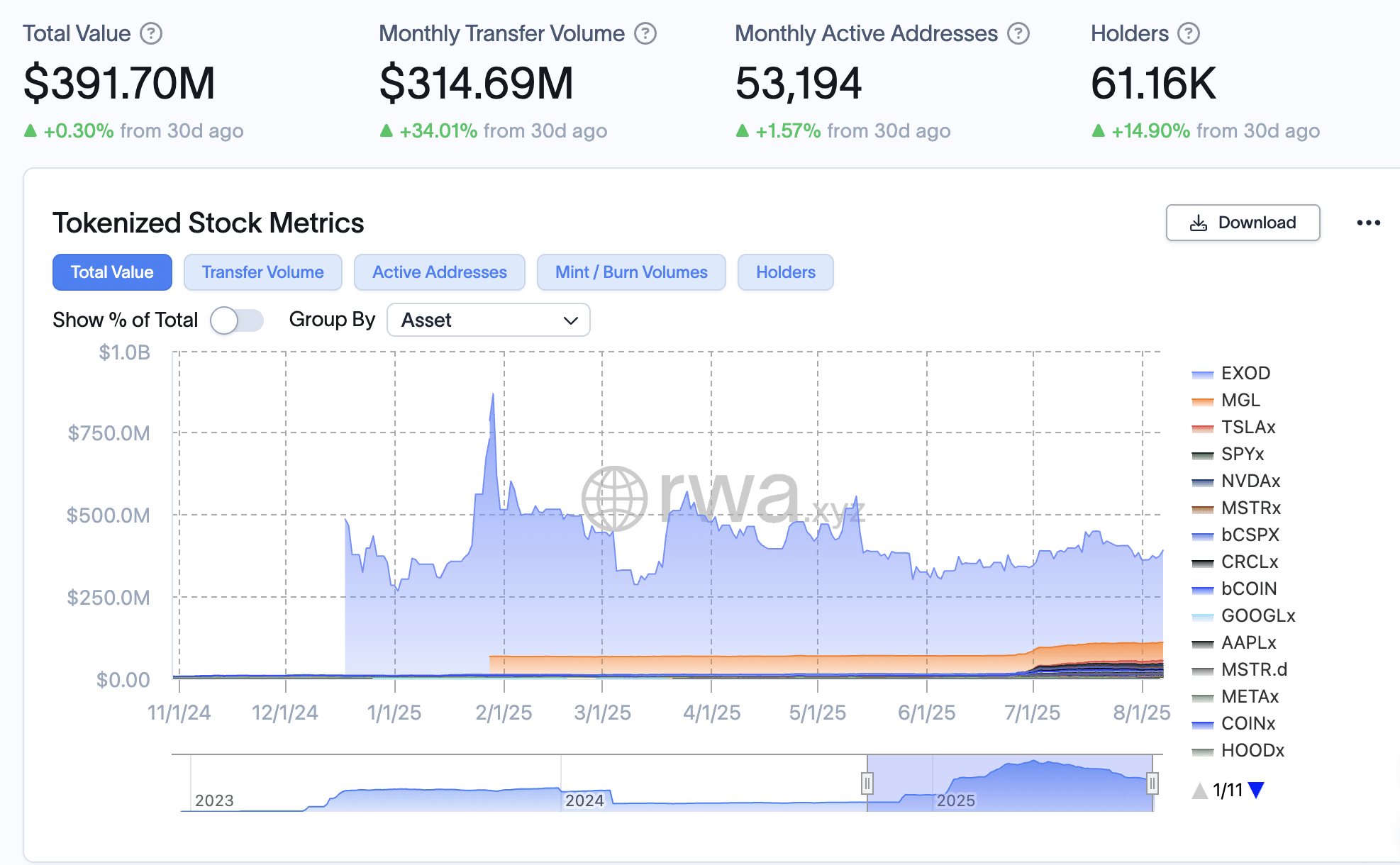

This trend is driven by a rapidly clarifying regulatory environment and the entry of traditional giants. The Nasdaq exchange has proposed creating a digital asset version of ATS (Alternative Trading System), allowing tokenized securities and commodity tokens to be listed and traded together to enhance market liquidity and efficiency. SEC Commissioner Paul Atkins even compared the on-chaining of traditional securities to the digital revolution of music media: just as digital music disrupted the music industry, the on-chaining of securities is expected to realize a new mode of issuance, custody, and trading, reshaping all aspects of capital markets. However, this field is still in its early stages, and compared to other RWA fields worth tens of billions of dollars, the upside potential for US stock tokenization seems larger, with the overall market value of on-chain stocks currently below $400 million and monthly trading volume only around $300 million.

The practical problems that this provision needs to address include the lack of a comprehensive compliance pathway, the complexity of regulations for institutional entry, and the high friction in the funding process. However, for most users, the primary issue to resolve is actually insufficient liquidity. Tech investor Zheng Di stated that the high OTC costs lead to a division between those playing in the US stock market and those in the blockchain space. 'You have to bear costs of several thousand when entering through OTC, and if using a licensed exchange like Coinbase in Singapore, you also have to add about 1% in fees and 9% in sales tax. Therefore, the money in the crypto world and that in traditional brokerage accounts are essentially two separate systems that rarely connect, as if you are fighting on two battlefields.'

For this reason, on-chain US stocks are now like a teacher educating this group of Degen players to accept basic knowledge of US stocks while simultaneously shouting to those accustomed to traditional brokers that here is 'open 7*24.' The founder of StableStock, ZiXI, categorized users of on-chain US stocks into three groups in an interview and analyzed why on-chain US stocks are 'needed' in their usage scenarios.

Beginner users: mostly located in countries with strict foreign exchange controls like China, Indonesia, Vietnam, the Philippines, and Nigeria. They have stablecoins but cannot open bank accounts abroad due to various restrictions, making it difficult to buy traditional US stocks. Professional users: have stablecoins and overseas bank accounts, but traditional brokers offer too low leverage; for example, Tiger's leverage ratio is only 2.5 times. However, on-chain, by setting a high LTV (loan-to-value ratio), high leverage can be achieved; for instance, with an LTV of 90%, 9 times leveraged trading can be accomplished. High-net-worth users: hold US stock assets for a long time and may earn interest, dividends, or benefits from stock price increases through margin trading in traditional brokerage accounts. Their tokenized stocks can be used for LP, lending, or even cross-chain operations on-chain.

From Robinhood's press conference to Coinbase submitting a pilot application to the SEC to become one of the first licensed institutions offering 'on-chain US stock' services. Coupled with the SEC's Division of Corporation Finance's favorable statement regarding liquid staking, it can be anticipated that as the policy bull market advances, on-chain US stocks can gradually integrate into the DeFi system, thus constructing relatively deep liquidity pools. The previously limited 'American value' of 5×7 hours of trading is accelerating its transformation into an on-chain equity market accessible to global investors at any time, regardless of time zones. This not only greatly expands the asset landscape for crypto investors but also introduces all-weather liquidity into traditional stock markets, marking Wall Street's move towards the 'Super-App era' of on-chain capital markets.

The renaming of staking assets, the rise of DeFi.

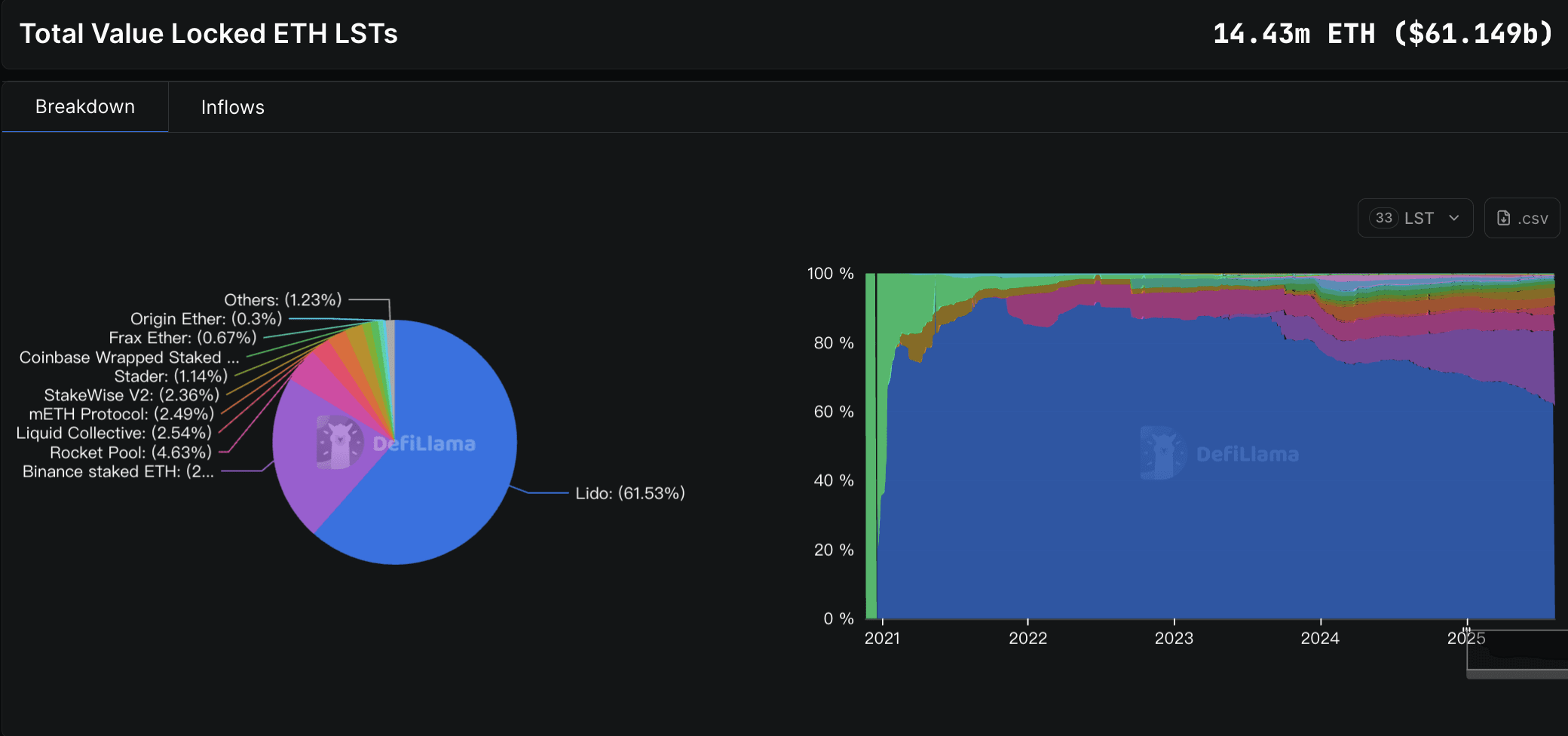

In this wave of regulatory goodwill, one of the biggest winners is undoubtedly DeFi derivative protocols, as the SEC's legitimization of liquid staking has paved the way for them, making it one of the most relevant benefits for 'crypto native' players. Previously, the SEC held a hostile attitude toward centralized staking services, forcing exchanges to delist staking services and raising concerns about whether Lido's stETH and Rocket Pool's rETH were unregistered securities. However, in August 2025, the SEC's Division of Corporation Finance declared that 'as long as the underlying assets are not securities, LSTs are also not securities.' This clear policy signal has been hailed by the industry as a watershed moment for staking's legitimacy.

This not only benefits staking itself but also activates an entire set of staking-based DeFi ecosystems: from LST collateralized lending, yield aggregation, to re-staking mechanisms, and yield derivatives based on staking. More importantly, clear US regulations mean that institutions can legally participate in staking and related product configurations. Currently, around 14.4 million ETH is locked in liquid staking, with accelerated growth. According to Defillama, from April to August 2025, the LST locked TVL surged from $20 billion to $61 billion, returning to historical highs.

The SosoValue DeFi index sector has outperformed the recently strong ETH over the past month, source: SosoValue.

From a certain point in time, these DeFi protocols seem to have formed a consensus and started deep cooperation with each other. They not only connect each other's institutional resources but also collaborate intensively on yield structures, gradually forming systematic 'yield flywheels.'

For instance, the integrated function newly launched by d Ethena and Aave allows users to gain leveraged exposure to sUSDe rates while maintaining better liquidity for their overall positions by holding USDe (with no cooling period restrictions). A week after its launch, the Liquid Leverage product has attracted over $1.5 billion in inflows. Pendle splits yield assets into principal (PT) and yield (YT), forming a 'yield trading market.' Users can buy YT with smaller amounts of funds to seek high returns, while PT locks in fixed yields, suitable for conservative investors. PT is used as collateral on platforms such as Aave and Morpho, forming the infrastructure for yield capital markets. Coupled with the recently established partnership with Ethena, Pendle's new plan 'Project Boros' expands the trading market to perpetual contract funding rates, allowing institutions to hedge Binance contract rate risks on-chain.

DeFi player JaceHoiX stated, 'Ethena, Pendle, and Aave are forming a triangular relationship of bubble TVL,' where users can cycle borrow 10x by using 1 USDT through minting USDe to mint PT to deposit PT to borrow USDT to mint USDe. At the same time, this $10 deposit exists in the TVL of these three protocols, turning $1 into $30 in deposits across these three protocols.

Many institutions have been entering this space early through various means in recent years, such as JP Morgan with its lending platform Kinexys, and companies like BlackRock, Cantor Fitzgerald, and Franklin Templeton. Clarifying policies will benefit the acceleration of DeFi protocols connecting with TradFi, ultimately extending the narrative of 'selling apples in the village' from 1 dollar to a much longer version.

The US public chain and the world computer.

Domestic public chain projects in the US are receiving favorable policies. The recently passed CLARITY Act proposes standards for 'mature blockchain systems,' allowing crypto projects to transition from securities to digital commodity assets once the network decentralizes and matures. This means that highly decentralized public chains and their tokens that comply with regulatory pathways are expected to gain commodity attributes and be subject to the jurisdiction of the Commodity Futures Trading Commission (CFTC) rather than the SEC.

KOL @Rocky_Bitcoin believes that the advantages of the US financial center are beginning to shift towards the crypto field, with 'CFTC and SEC having clear divisions of labor. The US wants to not only have a large trading volume in the next bull market but also become a project incubation hub.' This is a great advantage for US native public chains like Solana, Base, Sui, and Sei. If these chains can adapt to compliance logic natively, they may become the main networks carrying the next USDC and ETFs.

For instance, asset management giant VanEck has applied for a Solana spot ETF, stating that SOL functionally resembles Bitcoin and Ethereum and should be regarded as a commodity. Coinbase also launched Solana futures contracts regulated by the CFTC in February 2025, accelerating institutional participation in SOL and paving the way for future SOL spot ETFs. This series of moves indicates that under the new regulatory mindset, certain 'US public chains' are gaining commodity status and legitimacy, becoming important bridges for traditional capital to enter the chain, allowing established institutions to confidently transfer value to public chains.

At the same time, Ethereum, the 'world computer' of the crypto realm, has notably benefited from the policy shift, as the new rules restrict 'insider trading and rapid issuance cashing out,' favoring mainstream coins with actual construction and stable liquidity. As the most decentralized blockchain globally, with the most developers and an unbroken uptime record, Ethereum has long borne the throughput of the vast majority of stablecoins and DeFi applications.

Now, US regulators basically recognize Ethereum's non-security status. In August 2025, the SEC issued a statement that as long as the underlying asset, such as ETH, is not a security, then the liquid staking receipt pegged to it also does not constitute a security. Coupled with the SEC's earlier approval of Bitcoin and Ethereum spot ETFs, this effectively confirms Ethereum's status as a commodity.

With regulatory endorsement, institutional investors can participate more boldly in the Ethereum ecosystem, whether issuing on-chain Treasury bonds, stocks, and other RWA assets, or using Ethereum as a settlement layer to interface with TradFi businesses, all becoming realistic. It is foreseeable that as 'US public chains' compete to expand compliance, the 'world computer' Ethereum will still be the backbone of global on-chain finance. Not only due to its first-mover advantage and network effects, but also because this round of policy dividends has similarly opened new doors for deep integration with traditional finance.

Did policy really bring a bull market?

Whether it is the 'stablecoin bill' establishing the compliant status of dollar-pegged assets or the 'Project Crypto' outlining the blueprint for on-chain capital markets, this top-down policy shift has indeed brought unprecedented institutional space for the crypto industry. However, historical experience shows that regulatory friendliness does not equate to unlimited openness, and the standards, thresholds, and execution details during the policy testing phase will still directly determine the life and death trajectory of various tracks.

From RWA, on-chain credit to staking derivatives, almost every track can find its place within the new framework, but their true test may be whether they can maintain the efficiency and innovation inherent to crypto while complying. The global influence of US capital markets and the decentralized nature of blockchain will truly converge depending on the long-term interplay between regulators, traditional finance, and the crypto industry. The policy winds have shifted, and how to grasp the rhythm and control risks will be key to determining how far this round of 'policy bull market' can go.