In July, the global market welcomed a critical turning point as Trump rarely 'pressed' the Federal Reserve, attempting to exert pressure for a rate cut to alleviate government debt burdens, but Powell upheld independence and maintained interest rates unchanged, causing expectations for a September rate cut to drop from 60% to 47%. Meanwhile, the tariff war has entered a 'post-era'; although the game has not completely concluded, market reactions have become subdued, with three new main lines emerging in the post-tariff era: rate cuts, AI, and the institutionalization of crypto assets.

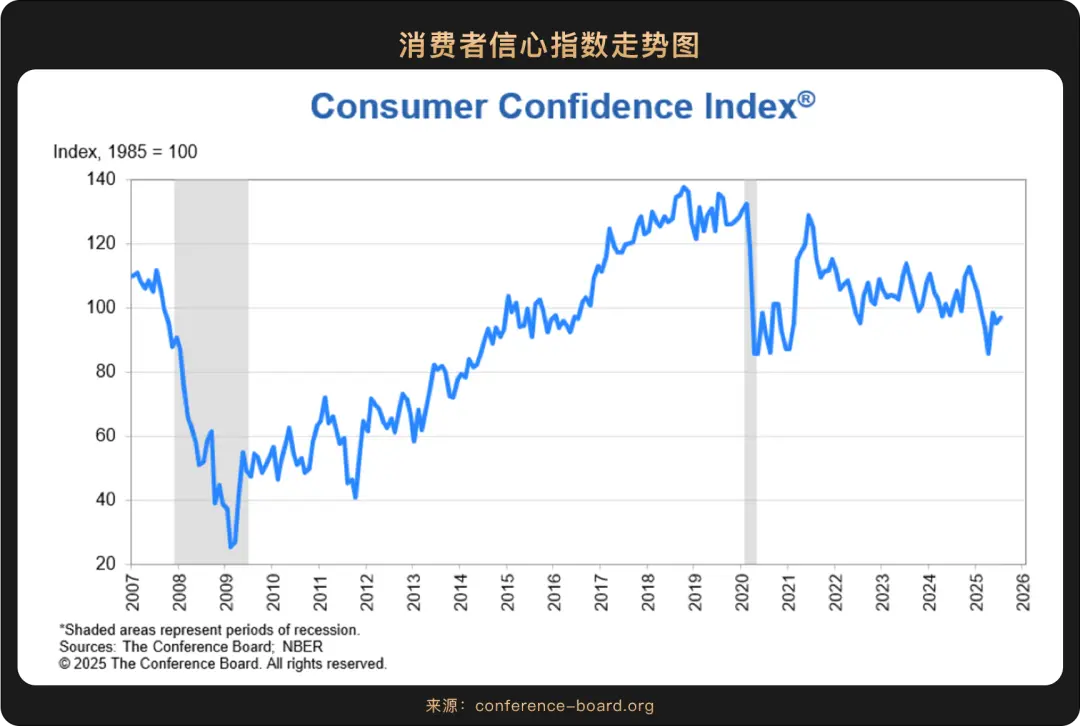

Currently, the U.S. economy resembles a tightrope walker: on one side is the 'soft foot brick' of consumer confidence—though the consumer confidence index rose slightly to 97.2 in July, up from 95.2 in June, it is indeed below market expectations, reflecting overall consumer caution, especially regarding confidence in the employment market; on the other side is inflation pressure, with June CPI up 2.7% year-on-year and 0.3% month-on-month, intensifying consumers' concerns that tariff policies may drive up prices, adding significant uncertainty to future inflation trends.

Faced with the complex economic situation, the pressure on the Federal Reserve is naturally increasing, but at the latest monetary policy meeting on July 31, the Fed still chose to maintain interest rates unchanged, marking the fifth consecutive time this year that the benchmark interest rate has remained in the range of 4.25%-4.5%. This decision sparked strong dissatisfaction from President Trump, who made a rare personal visit to the Fed headquarters to exert pressure, demanding a significant rate cut to 1%, and trying to use issues such as cost overruns on the Fed building renovation as political leverage. At this meeting, for the first time since 1993, two governors appointed by Trump—Vice Chairman Michelle Bowman and Governor Christopher Waller—cast dissenting votes in support of an immediate 25 basis point rate cut, highlighting the publicization of decision-making differences within the Fed.

In the face of pressure, Federal Reserve Chairman Powell remains steadfast, asserting that monetary policy is guided only by data, not by 'verbal pressure.' He stated that current inflation levels are still above the Fed's target, necessitating a moderately restrictive policy stance.

This tough stance directly impacts market expectations.

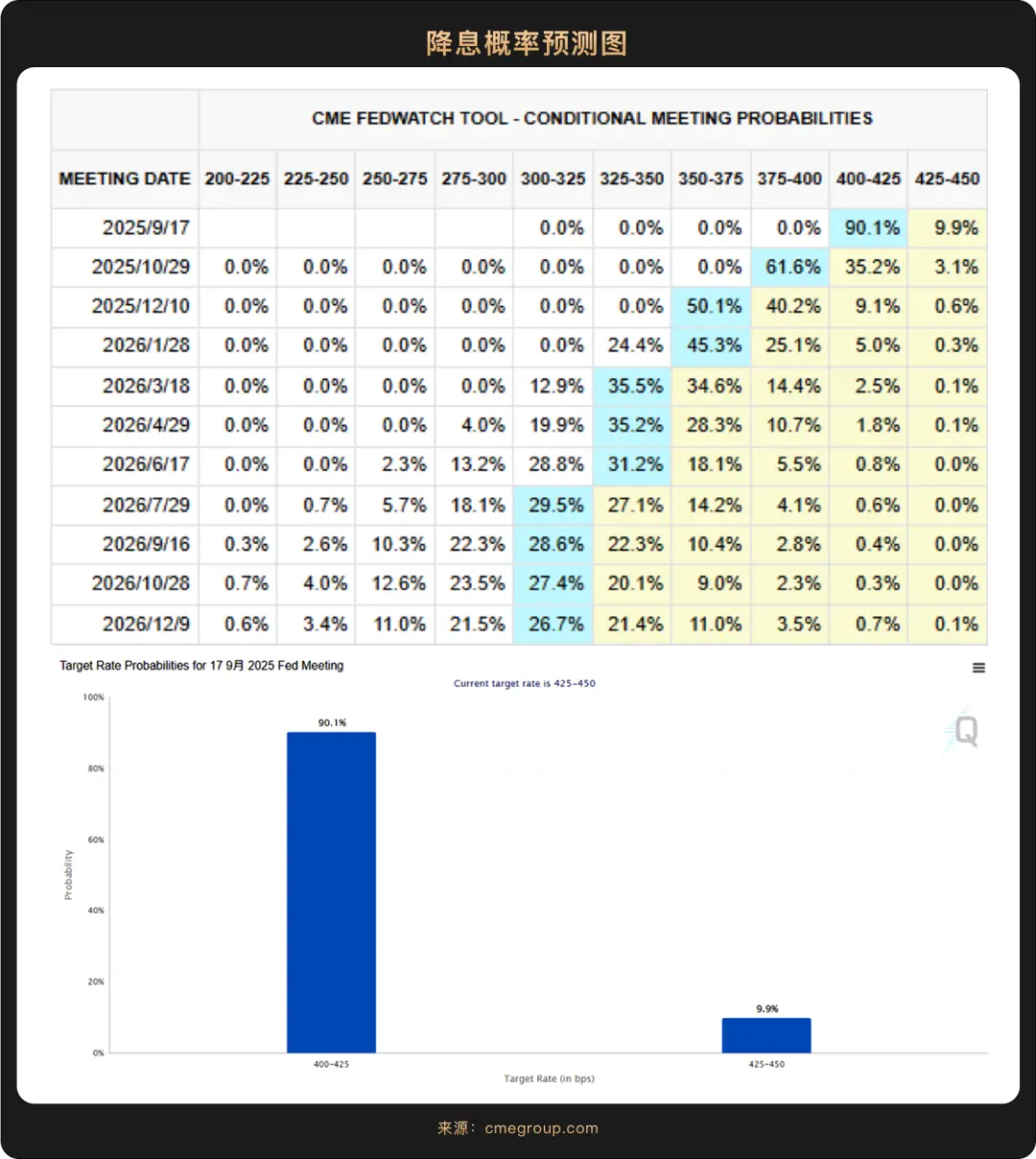

Currently, the market is focusing on the September monetary policy meeting, with the probability of a 25 basis point rate cut once rising to between 65% and 90%. Some institutions (like Goldman Sachs and Citigroup) predict that the Fed will cut rates consecutively in September, October, and December, totaling 2-3 rate cuts.

However, Federal Reserve Chairman Powell and most officials are cautious about a rate cut in September, emphasizing the need to observe more economic data, especially employment and inflation dynamics, and have not made a clear decision on the rate cut. Powell's remarks once led to expectations of a September rate cut dropping to about 40%.

In fact, the Federal Reserve has been striving to maintain policy independence in this dilemma, but the shadow of political interference lingers. Recently, Trump, dissatisfied with the latest employment data released by the U.S. Department of Labor, ordered the dismissal of the head of the Labor Statistics Bureau, McKentaff, intensifying market concerns over the uncertainty of U.S. economic policy.

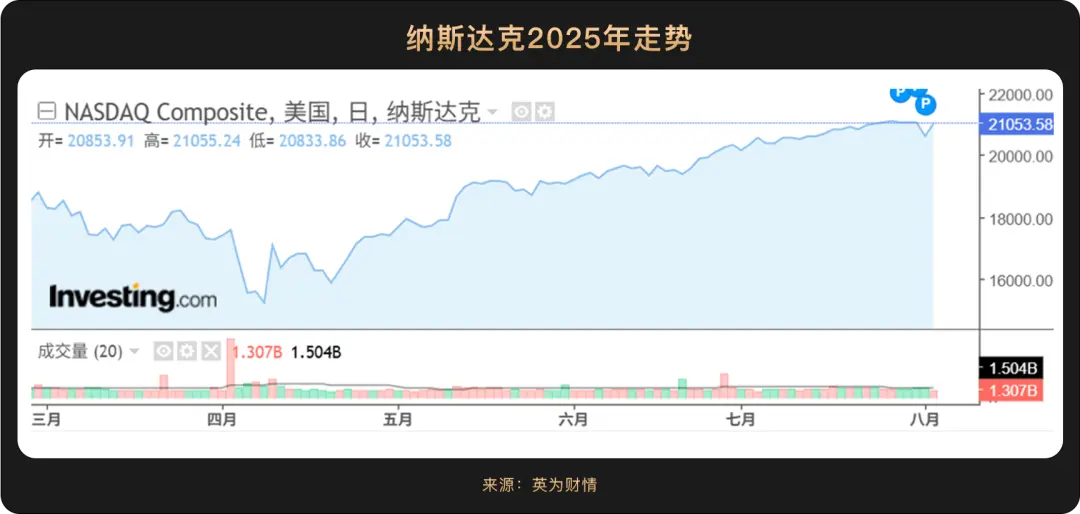

The tariff policy, once a 'market time bomb' led by the United States, is now taking a backseat. In July, the U.S. signaled tariff easing with major economies such as China, Europe, and Japan, particularly with the announcement of a new trade agreement between the U.S. and Europe at the end of the month. Although the U.S. still imposes a 15% tariff on most EU goods, this is lower than the originally threatened rate, reducing short-term uncertainties and propelling the S&P 500 and Nasdaq to historic highs. Looking ahead, although occasional regional tariff frictions may still 'update,' the market generally believes that overall tariff levels will be controlled within a 'safe zone that does not push the economy into recession,' akin to installing safety rails on a roller coaster.

This trend of 'worst expectations easing' has become an important psychological foundation for the new highs in U.S. stocks and cryptocurrencies, also indicating that global capital will conduct a new round of evaluations of risks and opportunities.

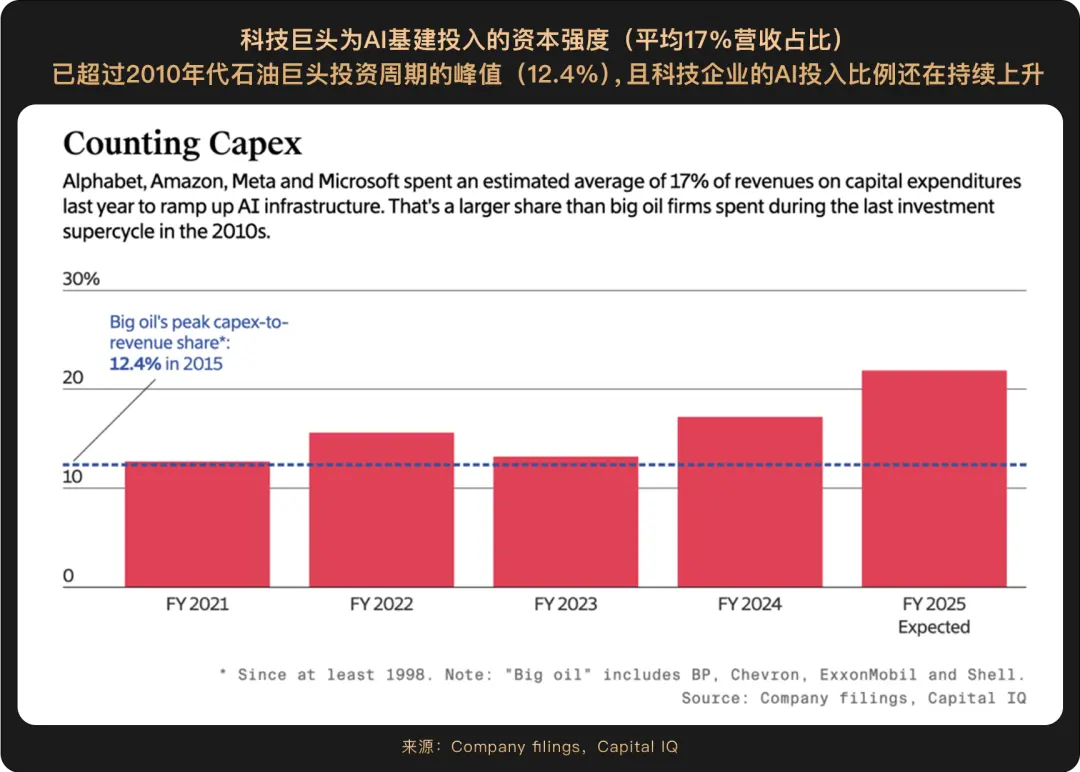

In the new opportunities, the commercialization breakthrough of AI has taken up the banner of a new market narrative. In the latest earnings season, the performance of tech giants generally exceeded expectations, particularly Meta (Nasdaq: META) and Microsoft (Nasdaq: MSFT). Meta benefited from the deep empowerment of AI technology in its advertising business, with its stock price rising sharply after the earnings report, briefly nearing a market value of $2 trillion, soon to join the 'trillion-dollar club' alongside Google (Nasdaq: GOOGL) and Amazon (Nasdaq: AMZN); Microsoft (Nasdaq: MSFT) became the second company to officially join the 'four trillion-dollar club' after Apple (Nasdaq: AAPL), thanks to strong growth in Azure cloud services. The previously dominant tariff issue is now taking a backseat, indicating that investors' sensitivity to such policy risks is decreasing, while the profit expectations brought by AI innovation are becoming the core driving force for the market, especially for the tech sector.

More importantly, these leading technology companies are significantly ramping up their AI investments with unprecedented intensity. Meta announced it would raise its capital expenditure plan for 2025 to $72 billion, while Microsoft plans to invest $120 billion in AI infrastructure by 2026. Such a massive investment scale not only demonstrates the companies' firm confidence in the prospects of AI but also suggests that the commercialization process of AI may be more rapid than the market expects.

The current market is shifting gears: the dominant pattern of trade friction in recent years is gradually receding, with new technology tracks represented by AI beginning to attract more attention, further altering the capital allocation pattern in the market.

In this round of technological investment boom, WealthBee observed that digital assets are becoming a new option for corporate balance sheets, with more and more listed companies starting to incorporate cryptocurrencies like Bitcoin into their corporate reserves. These pioneering companies that are 'first to take the plunge' often share two characteristics: first, they generally pay attention to the turning point in global monetary policy and potential inflationary pressures, viewing the scarcity and decentralized nature of cryptocurrencies, especially Bitcoin, as an effective tool for hedging against inflation and systemic risks; second, the technology sector they operate in has a natural affinity for new asset classes. Given the backdrop of a turning point in global monetary policy, the scarcity characteristic of cryptocurrencies makes them a natural potential tool for these companies to hedge against inflation.

The market situation in the first half of 2024 is starkly different from past years, where retail FOMO emotions 'propelled' market trends. The approval of Bitcoin spot ETFs, including those from BlackRock, Fidelity, and 11 other institutions receiving SEC entry permits, has fundamentally reshaped the capital structure and operating logic of the crypto market. By July 2025, this transformation is even more profound.

Throughout July, Bitcoin prices began a strong upward trend from the beginning of the month, continuously breaking through key resistance levels in the first half of the month. Compared to the beginning of the year, the overall trend shows a fluctuating upward trajectory, with a cumulative increase of over 20%. The influx of funds also demonstrated explosive growth, with institutional investors massively building positions through ETFs. As of July 2025, the total scale of Bitcoin ETFs in the U.S. is approximately $110 billion, and the market scale continues to grow rapidly. Among them, the iShares Bitcoin Trust ETF under asset management giant BlackRock accounts for nearly 48% of the market share, holding over 540,000 Bitcoin, with a market value of about $51.5 billion.

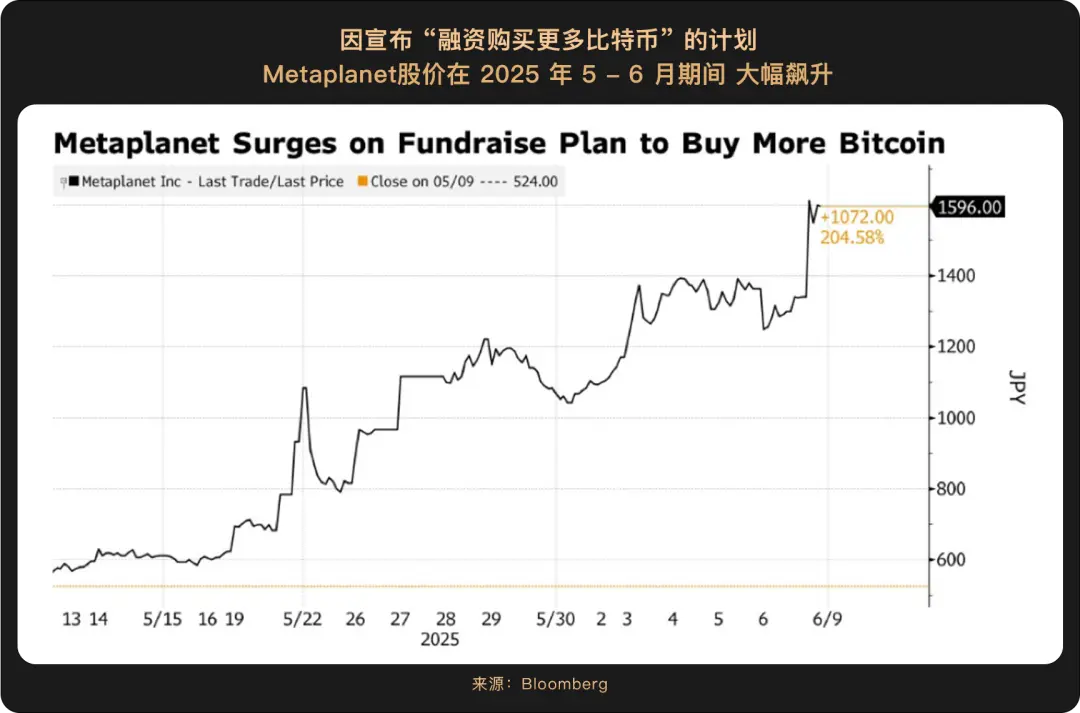

Institutional investors no longer view Bitcoin merely as a high-risk speculative asset; instead, they are incorporating it into their long-term asset allocation frameworks, initiating a competitive landscape for corporate holdings, which drives the market to form a more complex 'coin-stock linkage' mechanism: the absolute king of corporate Bitcoin holdings, Strategy (Nasdaq: MSTR), continued to add spot Bitcoin positions in July, unafraid of high prices, and stated in the latest disclosed 8-K filing that the company purchased $2.46 billion worth of Bitcoin during the last week of July; Japanese listed company Metaplanet has also followed Strategy, making a series of acquisitions to position Bitcoin as a core strategic asset, with Bitcoin reserves increasing to 4,206 coins, placing it among the top ten listed companies globally in terms of Bitcoin holdings. The company also plans to accumulate 21,000 Bitcoin by the end of 2026.

It is noteworthy that companies are no longer simply 'buy and hold' Bitcoin but are developing reserve structures that combine equity/debt/derivatives, such as Metaplanet, which achieves zero-cost financing to hoard Bitcoin by issuing zero-coupon bonds → granting stock appreciation rights (SARs) → redeeming bonds with exercise funds upon maturity, and the market is starting to give a premium to the financial engineering capabilities of such companies.

On regulatory matters, the U.S. SEC has released general listing standards for cryptocurrency ETPs, allowing assets with more than six months of futures trading history to apply for ETFs, with the first batch of Altcoin ETFs expected to be approved in September to October 2025; the stablecoin genius bill is just one step away from presidential signature, (the U.S. digital asset market clarification bill) is also beginning to go through the Senate process, clearing legal ambiguities for institutional participation. Hong Kong's stablecoin regulation took effect on August 1, requiring 1:1 reserves, a capital threshold of 25 million HKD, and transparent audits, prompting Chinese enterprises (like JD.com) to accelerate their layouts. It is evident that the focus of this round of regulatory collaboration is to clear regulatory barriers for traditional funds to enter and enhance the efficiency of traditional funds entering the market.

The crypto market in Q3 2025 is no longer solely driven by one-way ETF funds; it stands firmly on a new starting point characterized by 'institutional dominance + financial engineering + regulatory compliance.' The era of price speculation driven by emotions is quietly fading away, giving rise to a more mature and resilient market ecosystem that unfolds in the resonance of rules and innovation.

Overall, despite changes in the expected pace of rate cuts and the commercialization process of AI, future fluctuations in the market will still arise, but systemic risks have significantly decreased, and a new digital economic cycle is accelerating formation, with the deep integration of crypto assets and traditional financial systems becoming irreversible.