Original authors: Tanay Ved, Victor Ramirez, Coin Metrics

Reprinted: Daisy, Mars Finance

Key Points:

In a favorable regulatory environment and with clear investor interest in exposure to crypto assets in the public market, Kraken, Gemini, and Bullish are planning to go public (IPO).

Coinbase's IPO in 2021 set an industry benchmark. At the time of its IPO, Coinbase was valued at $65 billion, with 96% of its revenue coming from trading fees, whereas subscription and service revenue accounted for 44% in Q2 2025.

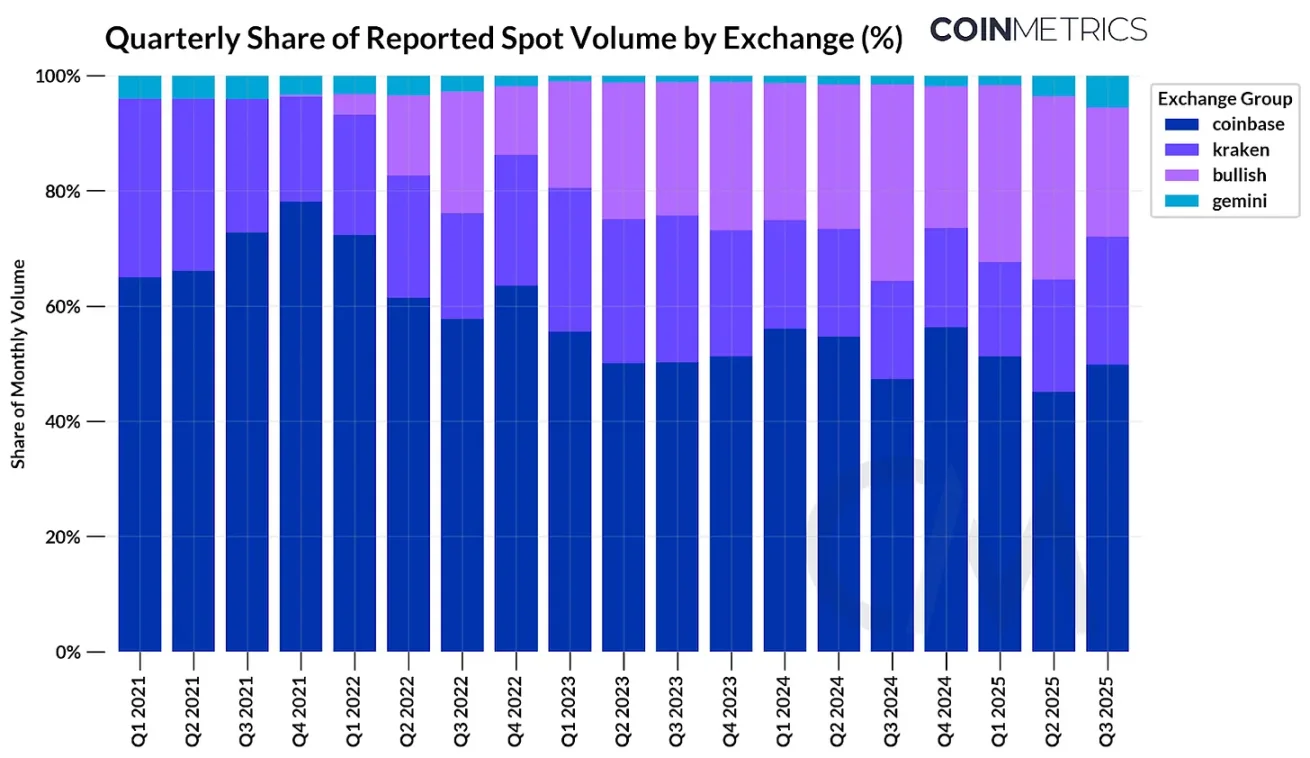

Among the IPO candidate exchanges, Coinbase still leads with 49% of spot trading volume. Bullish and Kraken each represent 22%, rapidly expanding new services.

Not all reported trading volumes carry equal value. Analyzing round-trip trades reveals inflated activities on some platforms and underscores the need to evaluate the quality and transparency of exchanges.

Introduction

Throughout the history of the cryptocurrency industry, the U.S. government's stance has often been lukewarm, even hostile. But last week, the situation changed positively.

The President's Working Group on Digital Assets released a 166-page report outlining the current state of digital assets and proposing policy recommendations for establishing a comprehensive market structure. Meanwhile, SEC Chairman Paul Atkins announced the "Crypto Project" in a public speech, aimed at making the U.S. the "global crypto capital" by chainifying financial markets, simplifying the cumbersome licensing regime for cryptocurrency businesses, and supporting the creation of financial "super applications" offering various services.

The main beneficiaries of this new regulatory framework are centralized exchanges. Several private centralized exchanges, such as Kraken, Bullish, and Gemini, are seeking IPOs in this relatively favorable environment. As these companies open up investment to the public, it is essential for investors to understand their fundamental drivers. In this article, we will thoroughly assess the key metrics of these exchanges and highlight some considerations when using exchange reported data.

The IPO frenzy of cryptocurrency exchanges

Since Coinbase went public in April 2021, there have been very few IPOs related to the cryptocurrency industry over the past four years, mainly due to the adversarial relationship between cryptocurrency companies and the former SEC. As a result, private companies have been unable to obtain liquidity from the public market, and non-qualified investors cannot profit from investing in these companies. With the Trump administration's commitment to a more favorable regulatory regime, a new wave of private cryptocurrency companies has announced plans to go public.

This environment, combined with renewed investor interest in public market crypto exposure, has birthed some of the most explosive IPOs, such as Circle's recent public IPO. Gemini, Bullish, and Kraken plan to list in the U.S. to seize this opportunity and position themselves as full-stack service providers for digital assets.

Coinbase's IPO in 2021

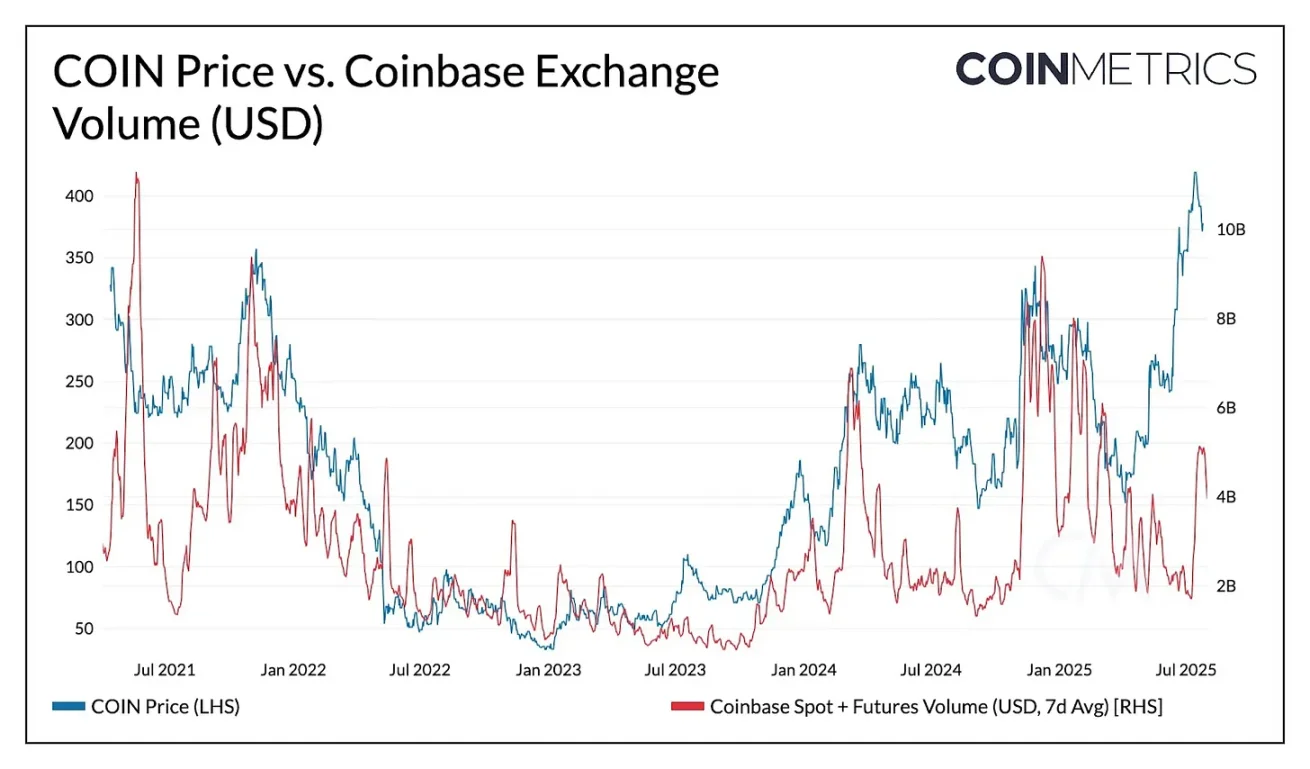

Coinbase's IPO in 2021 provides a useful benchmark for evaluating the investment prospects of potential exchange IPOs. The company went public on April 14, 2021, through a direct listing on Nasdaq, with a reference price of $250 per share and a fully diluted valuation of $65 billion, opening at $381 per share. Coinbase's listing occurred at the peak of the 2021 bull market, when Bitcoin prices approached $64,000 and exchange trading volumes exceeded $10 billion.

According to its S-1 filing, Coinbase's business model at that time was very simple, with most revenue coming from trading fees:

"From our inception until December 31, 2020, we generated over $3.4 billion in total revenue, primarily from transaction-based fees from retail users and institutions on our platform. As of December 31, 2020, trading revenue accounted for over 96% of our net income. We leveraged the advantages of trading to expand and broaden our platform, launching new products and services through investment flywheels and growing our ecosystem."

Source: Coin Metrics Market Data Pro and Google Finance

Today, Coinbase functions more like a "full-stack exchange." While trading remains its core business, its business model has significantly expanded into the full stack of cryptocurrency services. This shift is beginning to be reflected in the relationship between COIN price and trading volume, which were closely related in the early days but have weakened as the importance of subscription and service revenue (including stablecoin income (USDC interest income), blockchain rewards (staking), custody income, etc.) has increased.

Coinbase Q1 2021:

Revenue $1.6 billion

Trading revenue $1.55 billion (96%)

Subscription and service revenue $56 million (4%)

Coinbase Q2 2025:

Revenue $1.5 billion

Trading revenue $764 million (51%)

Subscription and service revenue $656 million (44%)

Interest income from corporate holdings $77 million (5%)

Comparative analysis of upcoming IPO exchanges

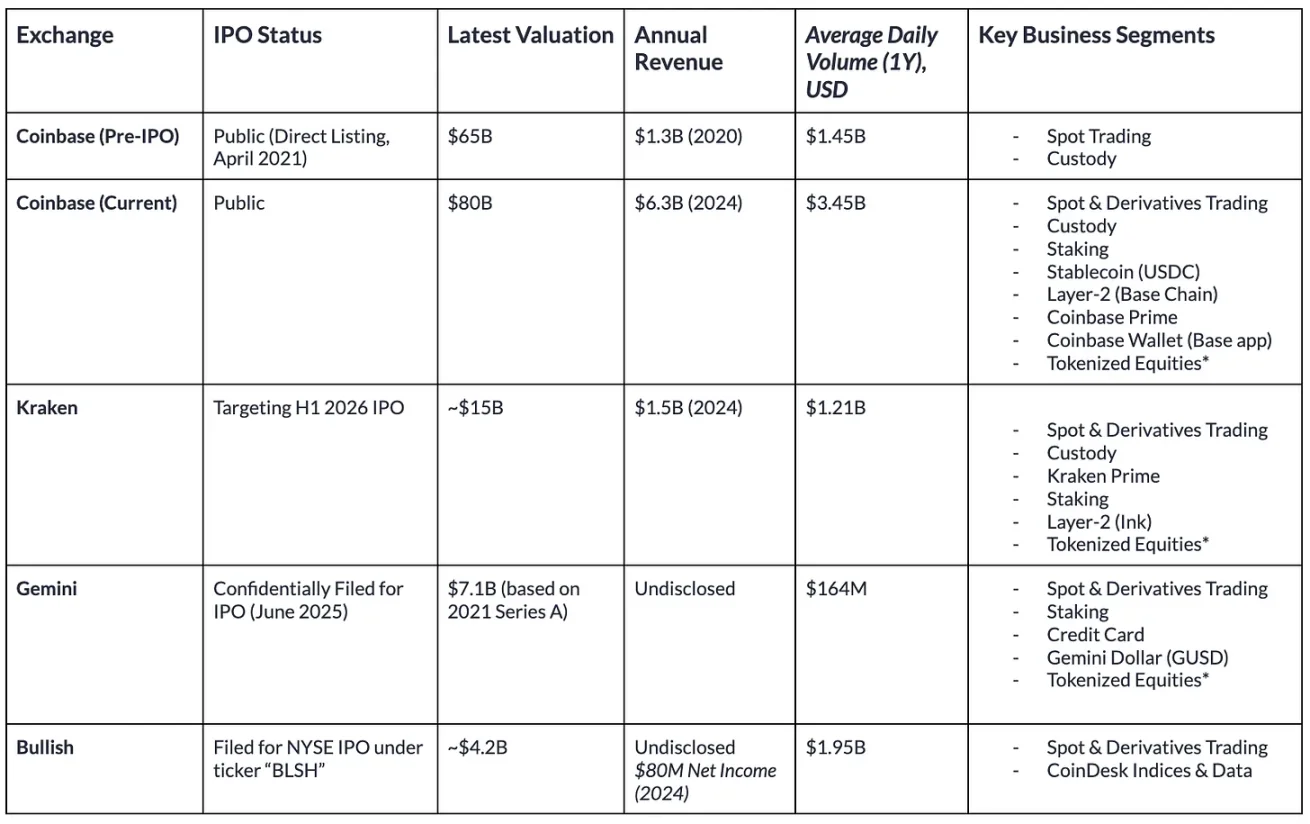

Based on this framework, we listed estimated data on the valuations, trading volumes, and business areas of upcoming IPO exchanges.

Source: Coin Metrics Market Data Pro and public company filings (data as of August 1, 2025)

Although the services offered by these exchanges tend to converge, there are significant differences in their market impact and scale of trading activity.

Kraken, founded in 2013, has reached a more mature stage. The company has strong financial growth, with 2024 revenue projected at $1.5 billion (up 128% from 2023) and Q2 2025 revenue at $412 million. Kraken has also strategically expanded into areas such as acquiring NinjaTrader, obtaining European MiCA licensing, and tokenized stocks, payments, and on-chain infrastructure (Ink). The target valuation is approximately $15 billion, with 2024 revenue of $1.5 billion and a revenue multiple of 10 times, slightly lower than Coinbase's 12.7 times.

In contrast, Gemini is smaller in scale. Its average trading volume over the past year was $164 million, the lowest among these exchanges. Gemini's latest valuation dates back to $7.1 billion from its Series A funding in 2021, while private market estimates it at $8 billion. In addition to spot and derivatives business, Gemini also offers staking and credit card products, providing yield on user deposits, and is the issuer of the Gemini Dollar (GUSD), although its circulating supply has dropped to $54 million.

Bullish ranks among the top in trading activity, with an average trading volume of $1.95 billion over the past year. Bullish Exchange is central to its trading and liquidity infrastructure, focusing on institutional clients and is regulated in Germany, Hong Kong, and Gibraltar, while actively seeking licensing in the U.S. Additionally, Bullish has expanded into the information services sector by acquiring CoinDesk. According to the F-1 filing, the company reported a net profit of $80 million and a net loss of $349 million in 2024. Based on the canceled SPAC transaction in 2022, its initial valuation was nearly $9 billion, and it is currently reportedly seeking a valuation of $4.2 billion.

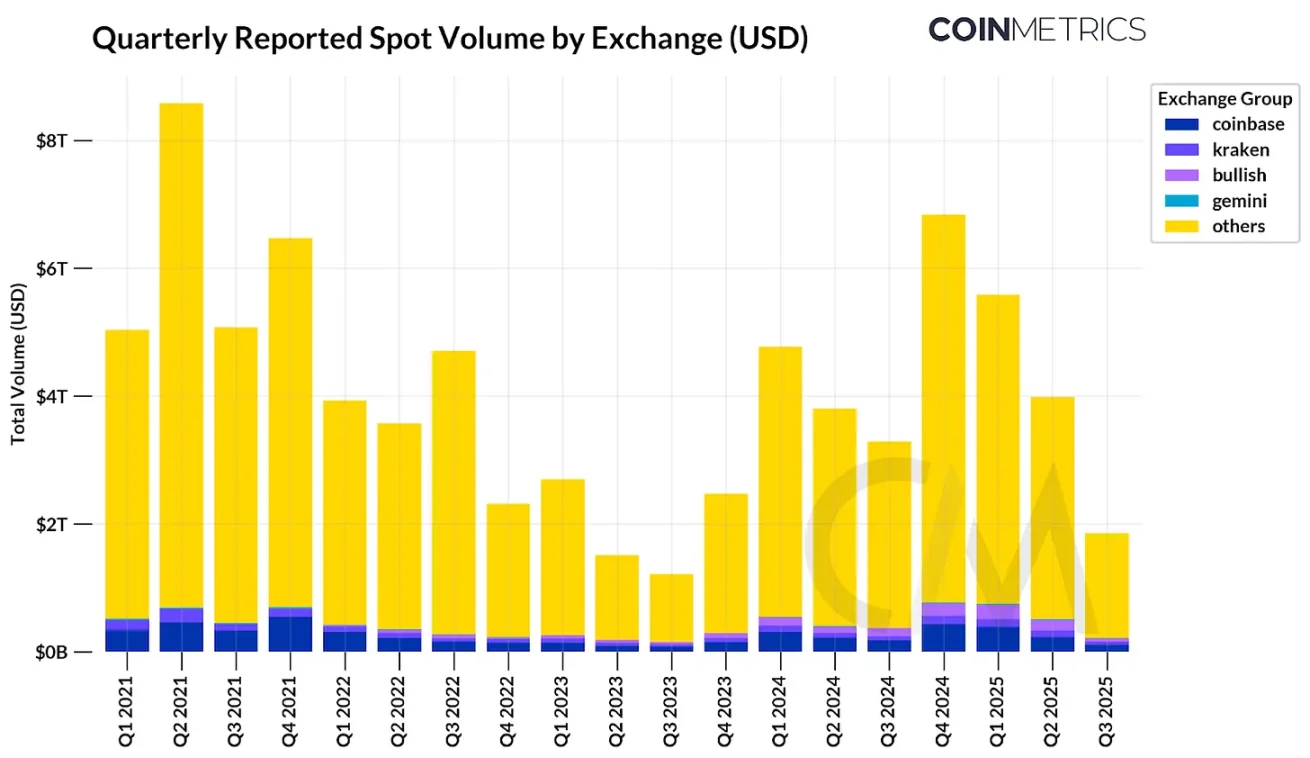

Exchange trading volume trends

Source: Coin Metrics Market Data Pro

Overall, Coinbase and other exchanges planning to go public account for only about 11.6% of the reported spot trading volume of centralized exchanges. Binance alone accounts for 39%, while other offshore exchanges also hold significant shares. Among the exchanges of interest, Coinbase accounts for 49% of spot trading volume, while Bullish and Kraken each represent 22%. Since its launch in 2022, Bullish's market share has steadily increased, while Kraken's has slightly diminished amidst rising competition.

Trades on the order book: Analyzing the economic activity of exchanges

As mentioned, trading volume is one of the most predictive indicators for estimating valuations. However, reported trading volumes can vary by exchange, becoming a potentially misleading data point.

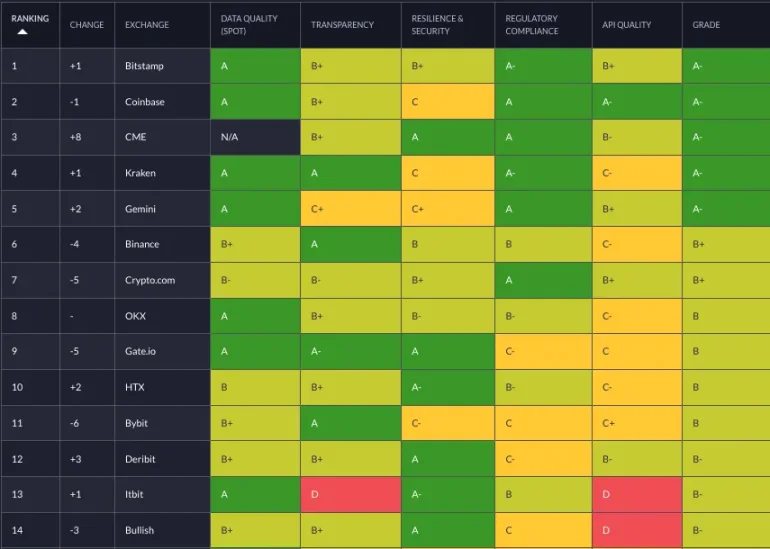

Although most major cryptocurrency exchanges have cracked down on wash trading, there are still some irregularities. Our trusted exchange framework method details how to detect abnormal trading activities and evaluates qualitative factors such as regulatory compliance.

Source: Trusted Exchange Framework

A more robust signal we have developed for detecting buy-sell trades is calculating the frequency of duplicate trades. Our testing method is as follows:

We randomly sampled 144 five-minute periods from January to June 2025, resulting in nearly 20 million trades.

For each exchange and period, select one trade.

If there is another trade within 10 trades or 5 seconds, and the direction is opposite, with nearly identical amount and price (at 1%), then label these two trades as duplicate trades.

Repeat this for each trade. If a trade has been marked as a duplicate, skip it.

Calculate the volume of trades marked as duplicates and divide by the total volume.

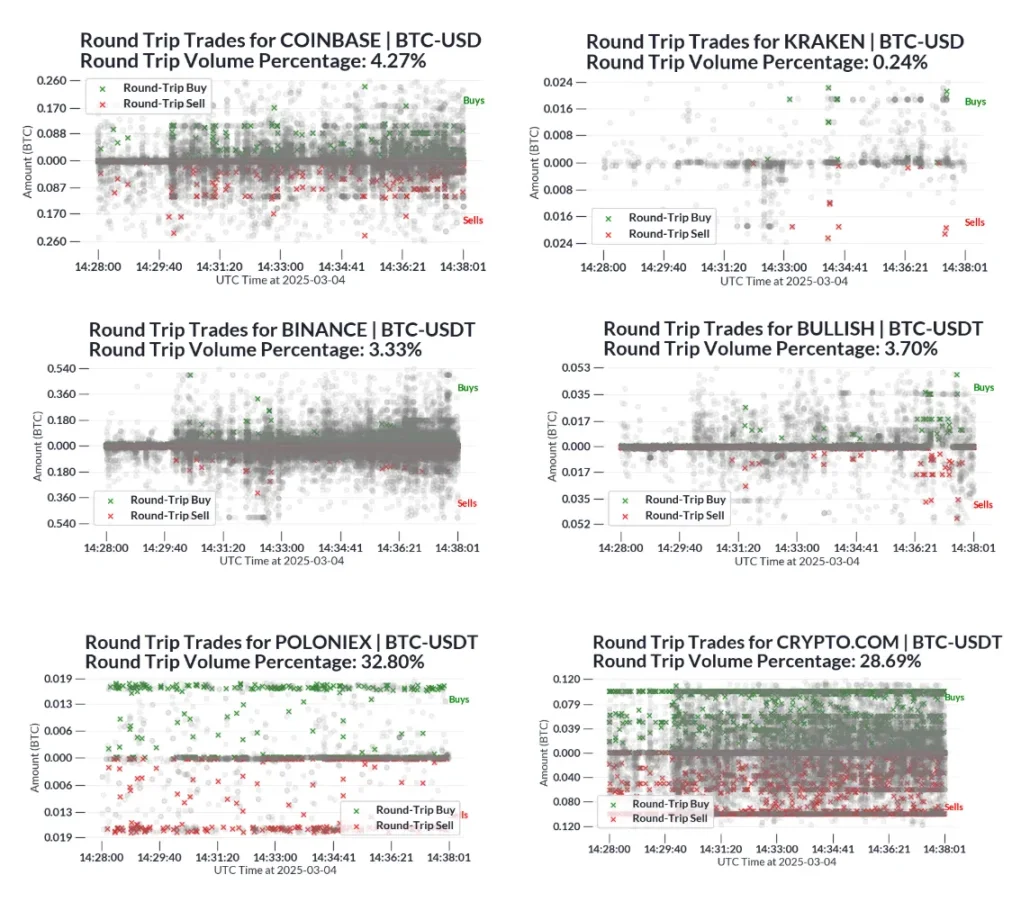

In the following figure, we plotted trade samples from a few exchanges within a period and marked suspected round-trip trades. Each gray dot represents a normal trade, while green and red markers indicate round-trip trades.

Source: Trusted Exchange Framework

Due to the approximate nature of this method, we expect some false positives, namely duplicate trades caused by normal market activities (such as market makers facilitating trades by providing liquidity on both sides of the order book). However, compared to industry baselines like Crypto.com and Poloniex, the high rate of duplicate trades raises concerns about the reliability of their reported trading volume data.

For example, we estimate that from Q1 to Q2 2025, Crypto.com's BTC-USD ($201 billion), BTC-USDT ($192 billion), ETH-USD ($165 billion), and ETH-USDT ($160 billion) trading volumes were approximately $720 billion. According to the estimated ratios, about $160 billion of the trading volume in these pairs came from duplicate trades.

Conclusion

As several cryptocurrency exchanges prepare to go public, it is essential for investors to understand the relative trading volumes of these platforms. While trading volume helps estimate trading revenue (which still makes up the majority of income), qualitative factors such as business diversification, the presence of duplicate trades, and regulatory compliance are also crucial considerations in assessing the quality of exchanges. This information can help market participants determine if valuations are reasonable.

Coinbase remains in the lead four years after its IPO, largely due to its diversification into revenue sources such as custody, stablecoins, and Layer-2 fees. However, competition in the exchange market is intensifying. Other exchanges must diversify their revenue sources away from heavily market sentiment-dependent trading fees. As market structures become clearer, exchanges are allowed to evolve from trading venues to full-fledged super applications. How these exchanges seize this opportunity and whether they can realize their vision and replicate the success of past groundbreaking IPOs will be an important development to watch in the coming year.