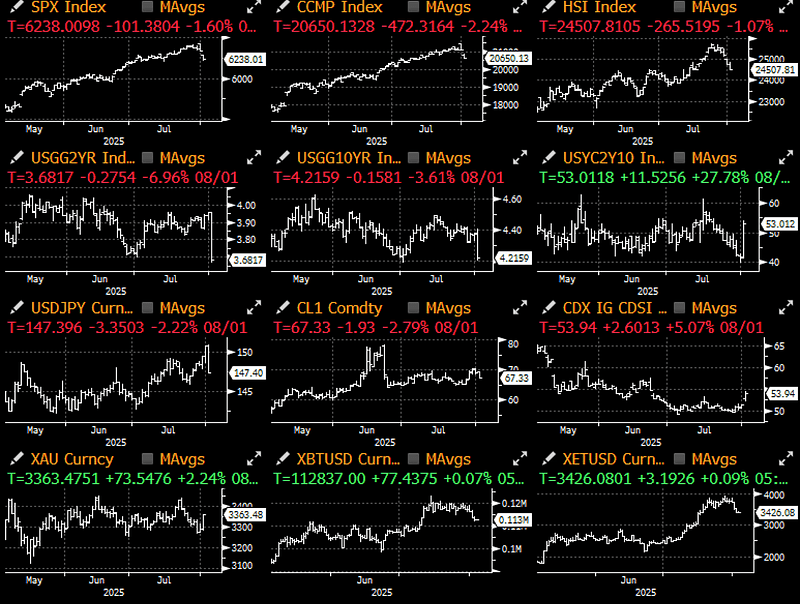

After a period of only rising prices, risk assets fell sharply under the impact of disappointing non-farm payroll data. Overall employment data was weak (the unemployment rate rose from 4.117% to 4.248%), further confirming the trend of a slowing job market. Furthermore, the US Bureau of Labor Statistics also released the largest downward revision of two months of employment data in recent years (excluding the pandemic period) at -258,000.

Compounding the issue, the ISM manufacturing employment index fell to its lowest level since the second quarter of 2020, and other leading indicators also suggest that the job market may further deteriorate.

The market reacted quickly and violently, with US stocks closing down 2% to 3%, and the dollar falling 2.2% against the yen to 147. Compared to the previous day, the interest rate market pricing reflected an increase of nearly 25 basis points in the expectations for rate cuts before the end of the year.

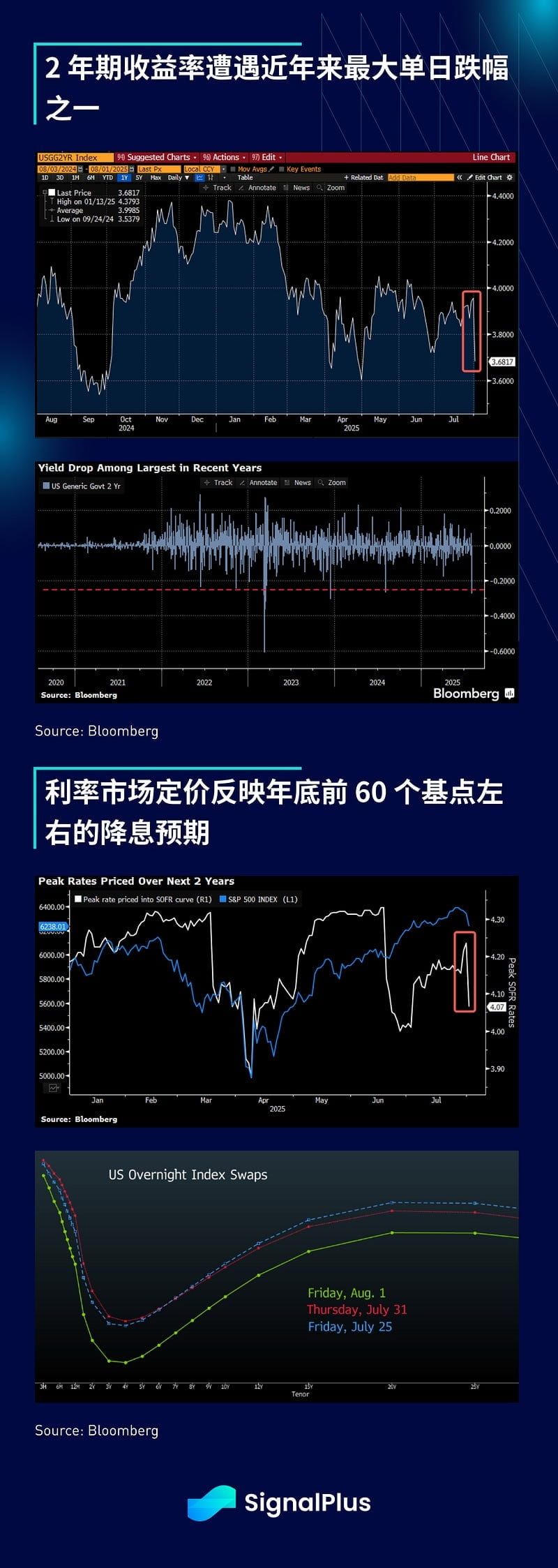

Yield changes are particularly significant, with the 2-year yield crashing nearly 30 basis points in one day, one of the largest single-day declines in five years. By the end of last week, the market's expectations for rate cuts this year rose to about 60 basis points, compared to only around 35 basis points the day before, prompting President Trump to harshly criticize Fed Chair Powell for failing to cut rates in a timely manner and to criticize the 'inaccurate' employment data released by the US Bureau of Labor Statistics.

"We need accurate employment data... The current data is produced by people appointed by the Biden administration."

"In my view, the current employment data is manipulated, aimed at embarrassing the Republicans and me." — President Trump

Last Friday's sharp market reaction also overshadowed the recent hawkish content of the Federal Reserve's meetings. During the meeting, Powell emphasized that the Fed is trying to address commodity inflation by maintaining interest rates. Meanwhile, with the resignation of Fed Governor Kugler, President Trump may nominate a new candidate soon, increasing pressure on the Fed.

Regarding policy impacts, President Trump has once again postponed the implementation of a new round of tariffs from the originally scheduled August 1 to August 7, paving the way for intensive negotiations this week. The focus of the negotiations will be on Switzerland (with tariffs as high as 39%), Taiwan, Canada, and Brazil, while the market will continue to monitor the escalating situation between Russia and Ukraine, as well as the subsequent developments of US submarine deployments.

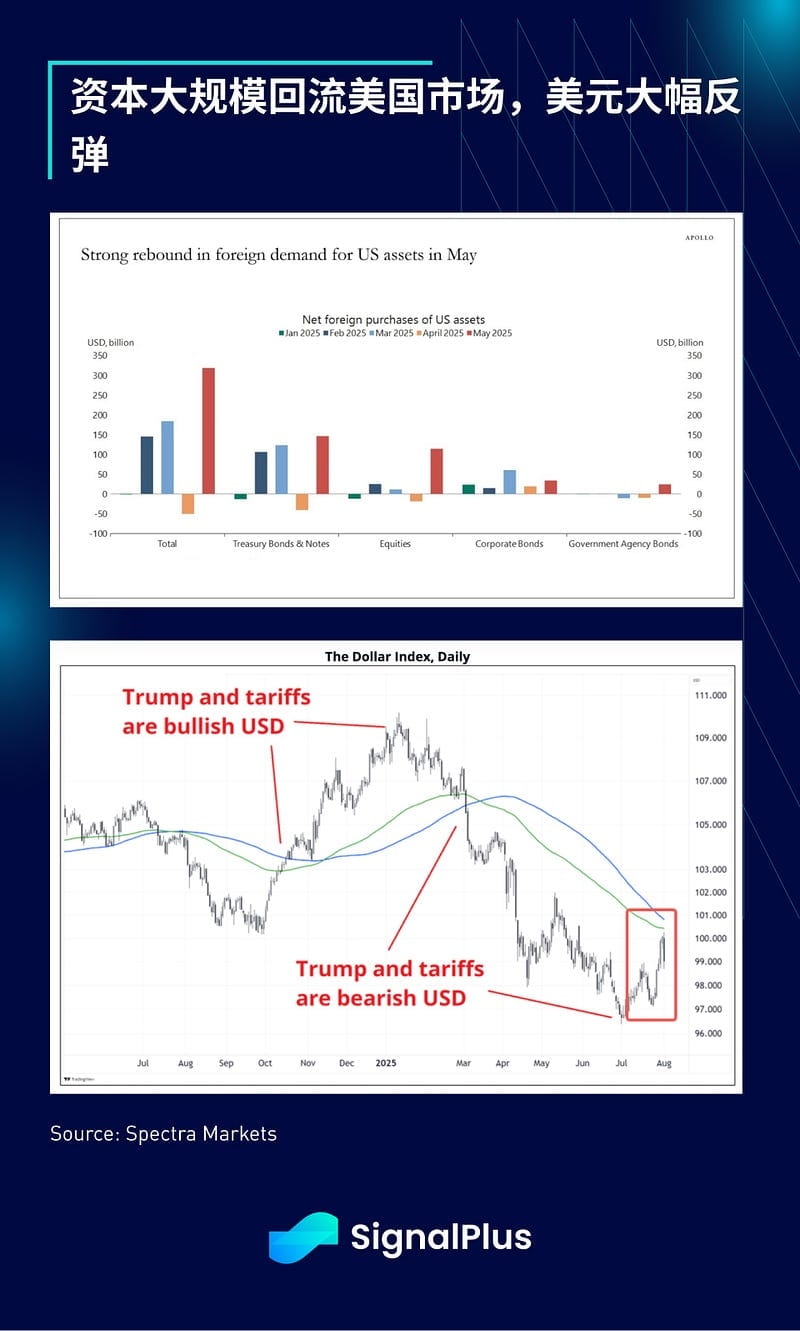

Despite various opinions and ridicule regarding tariff negotiations, US revenues in July did reach a record $150 billion, with a surplus of $27 billion the previous month, significantly reversing a $71 billion deficit a year ago. Additionally, with the narrative of American exceptionalism returning, demand for US assets has rebounded significantly since May, and concerns about capital outflows have dissipated.

The dollar also rebounded accordingly, with the dollar index rising more than 3% from recent lows, while safe-haven assets like gold began to weaken.

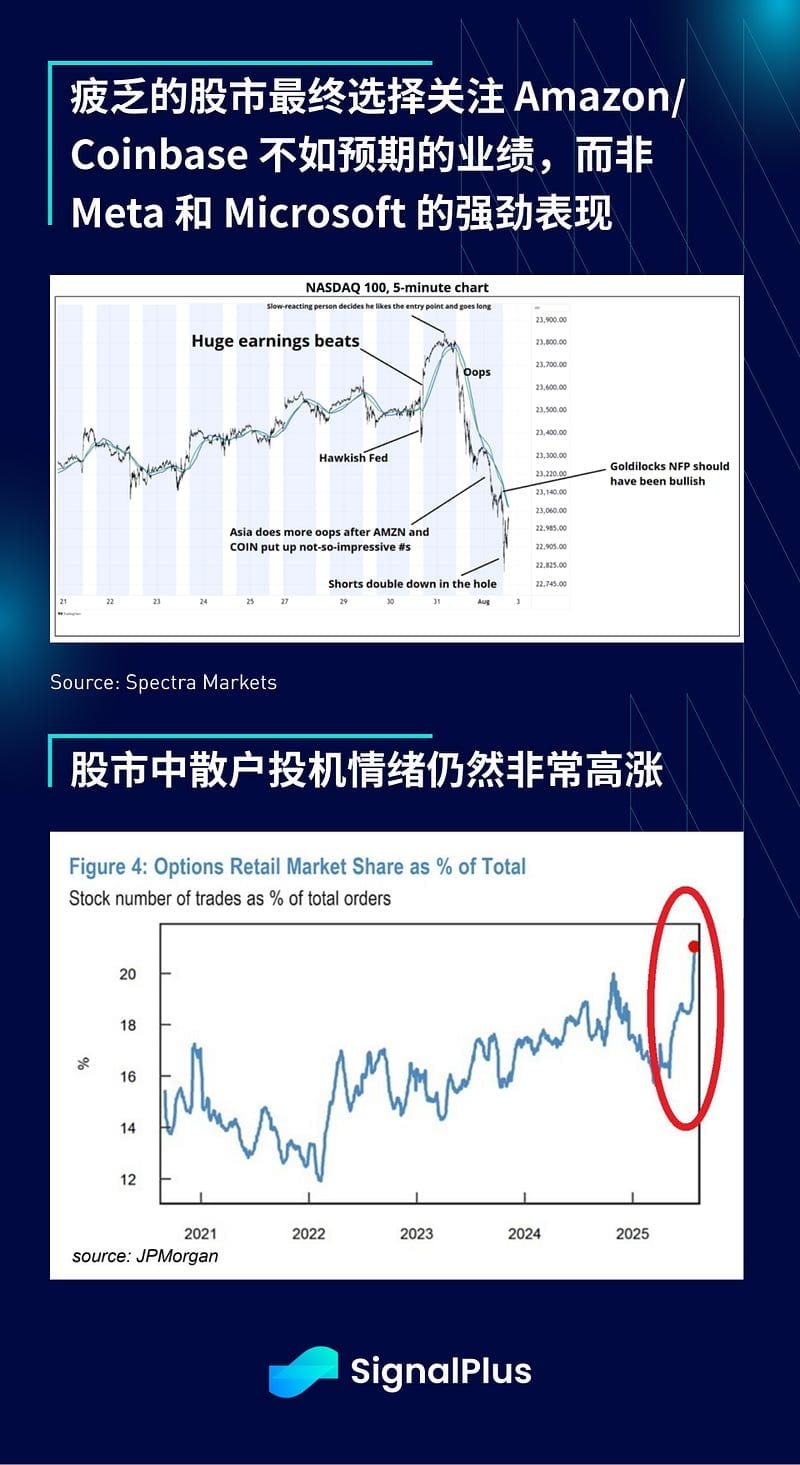

In the stock market, the earnings season has performed well so far, with Visa, Mastercard, and Amex all reporting robust growth in payment volumes and consumer momentum, while bank earnings generally met expectations. In the tech sector, consumers continue to show resilience in goods and transportation, with strong earnings from Meta and Microsoft, but ultimately dragged down by disappointing earnings from Amazon and Coinbase.

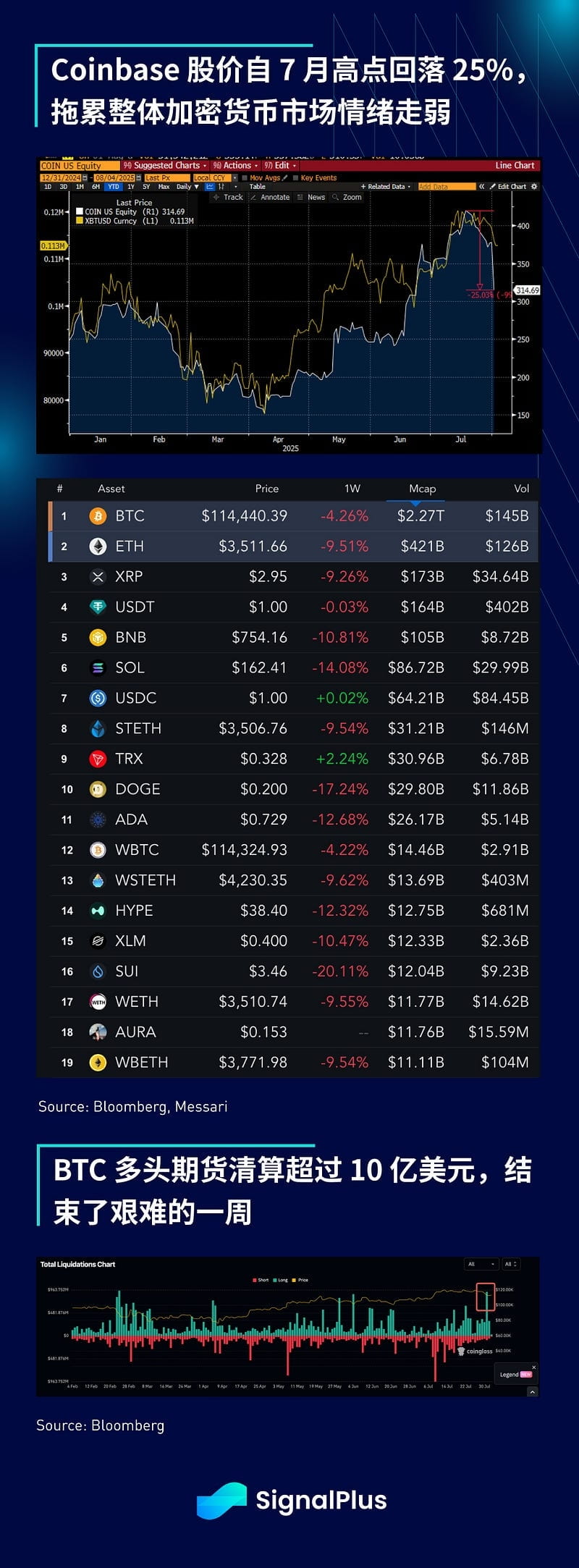

Finally, in terms of cryptocurrencies, Coinbase's revenue grew 3.3% year-on-year to $1.5 billion, but fell short of analysts' expectations and was below the $2 billion projected for Q1 2025. Net profit was boosted by unrealized gains in cryptocurrencies and Circle holdings; however, global and US spot trading volumes were generally weak in the second quarter.

Coinbase's stock price has fallen 25% from its July high, and with overall market sentiment weakening, the BTC price has also dropped to $112,000. Over $1 billion in long futures positions were liquidated last Friday, marking the most severe liquidation since May.

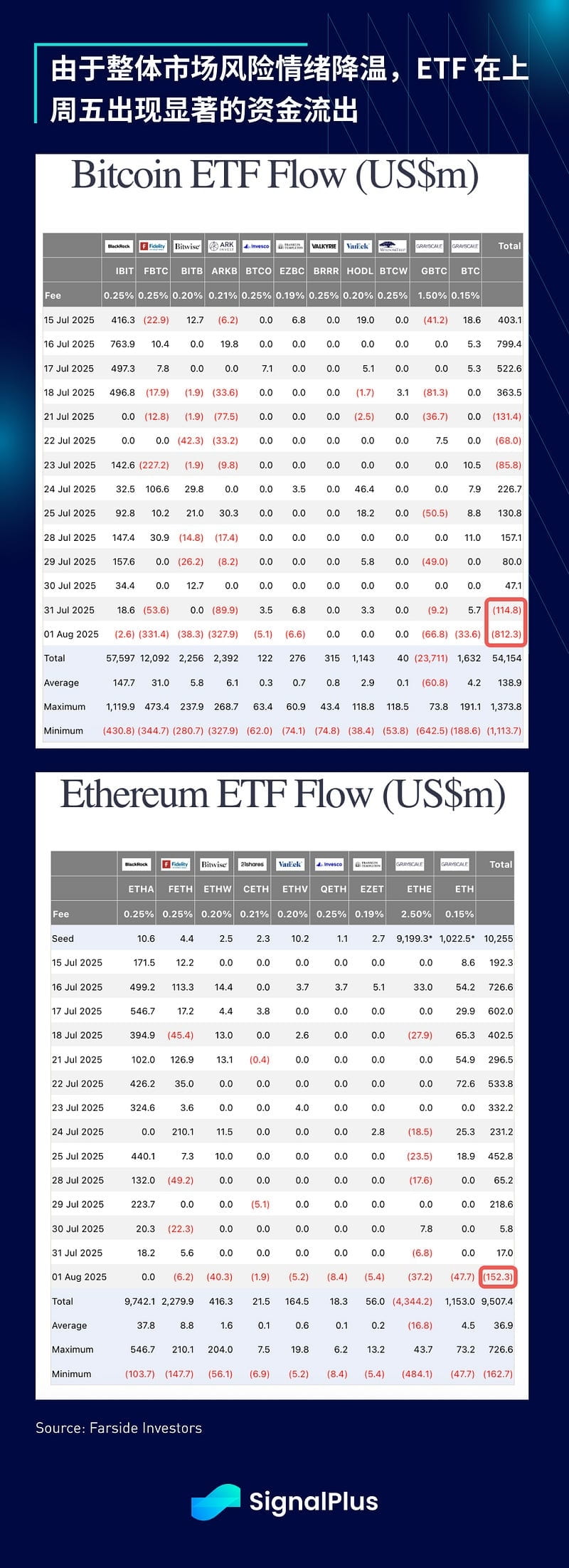

As expected, both BTC and ETH saw significant capital outflows last week, with BTC experiencing a $1 billion outflow on Thursday/Friday, marking one of the worst single-day performances of the year, while ETH ended nearly a month of continuous net inflows with an outflow of $152 million last Friday.

Overall, given the speed and scale of capital outflows, market performance has actually been more stable than expected, which is also related to the significant increase in market depth for BTC and altcoins. With institutional funds and professional investors joining, liquidity in the secondary market has improved, avoiding the drastic sell-off that occurred before the ETF launch.

Looking ahead, the market is currently at a delicate juncture, with both bulls and bears expected to be locked in a tug-of-war, making it difficult to determine a victor in the short term. The bulls believe the market is overreacting to non-farm payroll data, while the bears point out that given the overheated market over the past three months, this could be an initial signal for a market reversal. Ongoing tariff news and Trump's increasingly aggressive rhetoric will further exacerbate market noise, and as summer enters its later stages, overall trading activity may decline, potentially amplifying market volatility.

We do not expect a clear directional breakthrough in the short term, and this month's price movements will likely be more volatile than in July. The fourth quarter will be critical, as the Fed will fully resume operations, and the combined effects of tariffs and inflation will begin to impact the real economy. Against this backdrop, we believe now is a good time to moderately reduce risk exposure in anticipation of a busy September and year-end. Wishing you all successful trading!