Written by: Luke, Mars Finance

On the weekend of early August, the crypto world felt a chill overnight. In just 24 hours, over $600 million in long positions vanished in a chain of liquidations. The market's panic spread rapidly, like ignited wild grass. The price of Bitcoin fell from a high of nearly $119,000, breaching the $114,000 mark. Social media was filled with wails, confusion, and blame. People were eager to know, where did this sudden storm come from?

This is not an isolated 'crypto-native' event, but a chain reaction ignited by external macroeconomic shocks that exposed the internal structural vulnerabilities of the market. The spark of geopolitical events and the paradox of economic data jointly ignited the fuse, detonating a market already saturated with dangerous high leverage. The entire liquidation waterfall's path seemed to be precisely guided by the gravity of an existing CME futures gap. This is a 'perfect storm' where macro, micro, and technical factors resonate perfectly.

External Shock: The Trigger for Global Risk Aversion

The root of this crash is deeply embedded in the soil of the traditional financial world. Two almost simultaneous macro events acted as catalysts for a comprehensive market sell-off, clearly demonstrating the increasingly close linkage between crypto assets and the pulse of the global economy.

First came the geopolitical clouds. On August 1, the Trump administration suddenly announced extensive new tariffs on imports from 92 countries and regions, with rates ranging from 10% to over 40%. This action immediately triggered a classic 'risk-off' mode globally. Capital fled risk assets and surged into gold, perceived as a 'safe haven,' pushing gold prices to break above $3,350 per ounce. The Chicago Board Options Exchange Volatility Index (VIX), Wall Street's 'fear index,' also surged sharply. In this environment, institutional capital did not view Bitcoin as 'digital gold,' but classified it as a high-beta risk asset similar to tech stocks. Therefore, the tariff news directly put pressure on cryptocurrency prices, becoming a key external factor for Bitcoin's drop below $115,200.

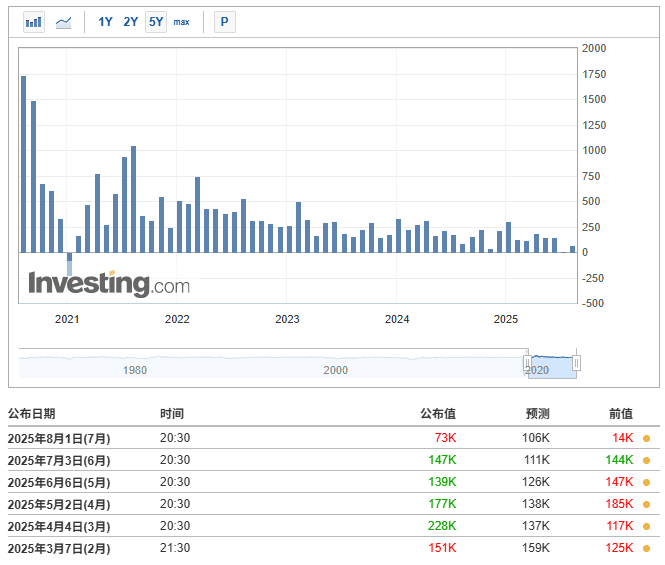

Adding insult to injury, the U.S. Bureau of Labor Statistics released the July Non-Farm Payroll (NFP) report on August 2, showing only 73,000 new jobs added that month, far below the market's expectation of 106,000. More shockingly, as noted by John Williams, president of the New York Fed, the 'real news' in the report was the 'abnormally large' downward revisions of the May and June data, indicating that the actual state of the U.S. labor market was much weaker than previously imagined.

This weak report triggered a contradictory reaction in the market. On one hand, it exacerbated concerns about an economic recession, directly fueling sell-offs under risk-averse sentiment. On the other hand, it dramatically changed the market's expectations for Federal Reserve monetary policy. According to CME's FedWatch Tool, the market's prediction of a 25 basis point rate cut by the Fed in September surged from less than 40% a day earlier to 89.8%.

This forms the most subtle core driving mechanism of this event: the market is forced to price between two completely opposing narratives. The first is the 'fear narrative': tariffs and weak employment data point to risks of economic recession, and the instinctive reaction of fund managers is to reduce risk exposure by selling high-volatility assets like Bitcoin. The second is the 'hope narrative': the same weak data is interpreted by another group of algorithms and analysts as forcing the Federal Reserve to take action, stimulating the economy through interest rate cuts. The liquidity increase from rate cuts has historically been 'rocket fuel' for risk assets. As a result, the market fell into a dilemma, and this profound uncertainty gave rise to extreme volatility, laying the groundwork for the subsequent large-scale liquidations.

Internal Detonation: A Market Prepared for a Crash

If macro shocks are the igniting match, then the internal structure of the crypto market is a barrel full of gunpowder. In the run-up to the crash, extreme optimism and rampant leverage had created perfect conditions for a catastrophic implosion.

In the days leading up to the crash, the derivatives market had already issued a clear red alert. The total open interest (OI) of Bitcoin futures skyrocketed to its highest level since the end of 2024, exceeding 300,000 Bitcoins, with a nominal value of $42 billion. This indicates that huge capital was locked into futures contracts, and the market's leverage level was extremely high. More critically, the funding rates on major exchanges remained positive, a clear signal: the market was dominated by leveraged long positions. Bullish traders were so confident that they were willing to continuously pay fees to bearish shorts to maintain their long positions.

When the macro-driven sell-off began, it triggered a domino effect. Data from Coinglass shows that a total of $396 million in leveraged positions were liquidated, of which $338 million (85%) were long positions. Data from other sources indicates total liquidations reached between $635 million and $726 million, with long positions accounting for nearly 90%. This waterfall of liquidations was not coincidental, but a brutal yet necessary self-correcting mechanism of the market. The logic is as follows: first, the market accumulated a massive 'leverage imbalance.' Next, an external shock arrived, causing initial price declines. Then, this drop triggered the forced liquidation of the first batch of highly leveraged long positions. These forced sell orders injected more supply into the market, further driving down prices, thus triggering the liquidation of the next tier of slightly less leveraged longs. Ultimately, a vicious cycle formed: each wave of liquidations led to further price declines, triggering the next wave of larger liquidations.

Technical Resting Place: The Pull of the CME Gap

Users' initial judgment — the market decline is to 'fill the gap' — touches on a key technical aspect of this event. The CME futures gap played a black hole-like role in this chaotic market, providing a clear destination for the price's free fall.

As a regulated traditional financial exchange, the CME's Bitcoin futures product is closed on weekends. However, the cryptocurrency spot market trades 24/7. This leads to a common phenomenon in CME charts, where there is often a gap — an area with no trade records — between Friday's closing price and the following Monday's opening price. A well-known theory among traders is that market prices tend to 'fill' these gaps.

In a chaotic market, the CME gap acts as a 'Schelling Point' — a natural focal point that parties can find without communication. For sellers and liquidity-hunting algorithms, it is a predictable, perfect target. When macro news provides a catalyst for selling, the sell behaviors of these algorithms are not random. They exert pressure along the path of least resistance and greatest impact. Targeting a known gap ensures they can accurately trigger stop-loss and liquidation orders clustered around that level. As the price is pushed toward the gap by algorithms, human traders who also focus on the gap join the sell-off out of fear that the gap will be completely filled, further enhancing the downward momentum. Thus, the gap is not the cause of the crash, but it becomes the destination of the crash.

Capital Game: Whales' Sell-Off and ETFs' Accumulation

Beneath the surface price collapse in the market, a silent war over capital flows is unfolding. On-chain data reveals starkly different behavior patterns among various market participants.

Data from on-chain analysis platforms like CryptoQuant and Lookonchain showed that in the hours and days leading up to the crash, large holders of Bitcoin, known as 'whales,' were actively transferring tokens to exchanges. A notable example is the well-known trading firm Galaxy Digital, which deposited over 10,000 Bitcoins (worth about $1.18 billion at the time) into exchanges such as Binance, Bybit, and OKX in less than 8 hours. This behavior is a typical signal of 'smart money' distribution.

In stark contrast to the distribution behavior of giant whales, newly established spot Bitcoin ETFs continued their systematic buying pace. Analysts pointed out that 'institutional demand continues to absorb supply,' and these ETFs played a crucial support role during the market downturn, preventing further price collapse. This represents a powerful, non-discretionary buying force in the market. Unlike whales that trade based on tactical needs, ETFs' purchasing behavior depends on the inflow of client funds, thus creating a stable and continuous demand stream that provides solid bottom support for prices. The game between short-term tactical sellers (whales) and long-term systematic buyers (ETFs) clearly reveals the market's inherent resilience and answers a key question: 'Why didn't prices fall lower?'

Long Road Ahead: Navigating the Crossroads

After this storm, the market did not experience calm, but instead entered a crossroads filled with confusion and divergence. Analyst comments also showed serious disagreement. Some, like Nathan Peterson from Charles Schwab, advised investors to 'sell high.' Others believe the market is in a 'healthy buy-low zone.' Ran Neuner, founder of Crypto Banter, even predicted that Bitcoin might reach $250,000 by the end of the year, while Michael Saylor, founder of MicroStrategy, called this drop 'a gift from God.'

Currently, the market is weighing short-term fears of an economic recession against medium- to long-term bullish expectations of Federal Reserve rate cuts and a new round of liquidity injections. This crash fundamentally reset market dynamics, forcing every participant to re-examine their investment logic. The future path will depend on which type of capital group — short-term traders scared off by macro fears or institutional investors committed to long-term accumulation — can exert greater influence. The large-scale liquidation events have washed away the most reckless leverage in the market, making the market structure 'cleaner' but also more cautious. This post-crash era is a high-risk test of the maturity and institutionalization of the crypto market.

Conclusion: Lessons from the Storm

The 'August Storm' of 2025 is a multi-act play. It began with shocks from macro politics, amplified infinitely by a fragile and over-leveraged derivatives market, and ultimately found its technical resting place at a CME gap. This event provides profound lessons about the modern crypto market, revealing its inherent duality. On one hand, its increasingly close integration with the global financial system offers long-term growth momentum and potential price floors. On the other hand, the same integration also makes it highly susceptible to shocks from traditional markets and geopolitical events. The 'August Storm' is the ultimate embodiment of this tension — a direct collision between old-world macro fears and new-world digital asset accumulation. The future of cryptocurrency will be defined by how it navigates between these two powerful and often opposing forces.