Author: Aki Chen Wu Discusses Blockchain

This article is compiled with the participation of GPT, intended for information sharing only, and does not constitute any investment advice. Readers are advised to strictly abide by the laws and regulations of their location and refrain from participating in illegal financial activities.

Introduction

On August 1, 2025, Hong Kong's (Stablecoin Regulations) officially came into effect. The regulation clearly stipulates that any institution issuing or providing fiat-backed stablecoins to local retail customers in Hong Kong must apply for a license issued by the Monetary Authority, strictly adhering to reserve mechanisms, AML/KYC obligations, and requirements for transparency. The Monetary Authority also announced the initiation of stablecoin license applications, with the first round of applications closing on September 30, and the first licenses expected to be issued in early 2026. This series of actions is viewed by the industry as an 'important milestone in the global compliance of stablecoins,' but due to its strong real-name (KYC) requirements and high barriers to entry, it is comparable to the strictest stablecoin legislation worldwide, triggering intense debate among Web3 project parties and the community. Meanwhile, the U.S. SEC has introduced the Project Crypto plan, proposing an 'innovation exemption' that contrasts sharply with Hong Kong's approach.

Overview of Core Stablecoin Regulations

According to the new regulations, all activities that issue, circulate, or provide fiat-backed stablecoins to local retail users within Hong Kong must obtain a special license issued by the Monetary Authority. Core requirements include:

· Capital requirement: Minimum paid-up capital of 25 million HKD;

· Reserve mechanism: 100% high-quality liquid assets support (cash, short-term government bonds), must achieve custodial isolation, and prohibition of re-mortgaging;

· Redemption mechanism: Users must be able to redeem at face value within one day;

· Real-name system (KYC): All user identities must be retained for over five years, with clear prohibitions on DeFi scenarios and access to anonymous wallets;

· Prohibition on advertising: Unlicensed stablecoins must not be marketed to the public, and violators may face fines and criminal penalties.

Among all regulatory provisions, KYC real-name verification requirements have become the focal point of the greatest controversy within the Web3 community. According to the Monetary Authority's requirements, stablecoin issuers must not only verify user identity information and retain data records for over five years, but also must not provide services to anonymous users. Additionally, initial identity verification is required for each compliant stablecoin holder in Hong Kong. In response, a member of the Hong Kong Legislative Council stated that the Monetary Authority would indeed implement KYC rules, although the specific implementation methods are not yet determined, with real-name systems being one of the proposed solutions. The Assistant Chief Executive of the Hong Kong Monetary Authority (Regulation and Anti-Money Laundering) Chen Jinghong also pointed out that this arrangement is stricter than the 'white list' mechanism proposed in earlier anti-money laundering consultation documents. However, he also indicated that as relevant technologies mature, there may be a possibility of moderate easing of regulations in the future.

This means that Hong Kong's stablecoins may initially lack the ability to interact directly with DeFi protocols, with decentralized wallets and permissionless addresses being isolated from the compliance system. Such interactions will also be legally regarded as 'unauthorized use.' It can be seen that compared to the scalability and freedom of on-chain protocols, Hong Kong regulators focus more on maintaining control over the circulation of stablecoins. This measure and attitude are viewed by some practitioners as a cold shower on the application of stablecoins in open financial scenarios on-chain. This creates a huge divergence compared to existing mainstream stablecoins (such as USDT, USDC), which allow free transfers between wallets and seamless integration with DeFi protocols, inevitably affecting user experience and adoption.

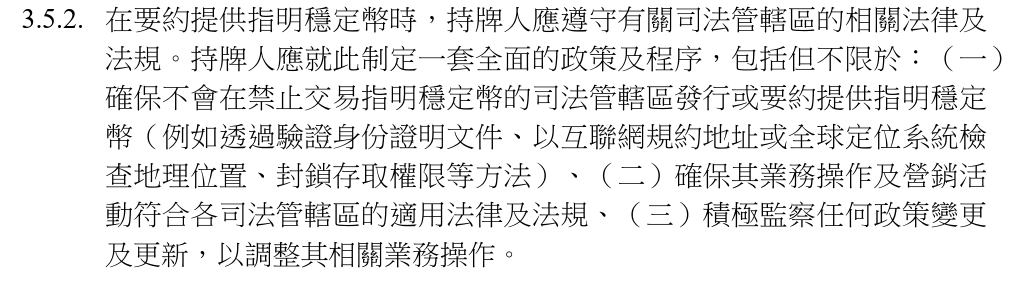

Adding to the woes, according to the Hong Kong Monetary Authority's (Stablecoin Issuer Regulatory Framework) provisions, when 'offering specified stablecoins,' license holders must comply with the laws and regulatory requirements of relevant jurisdictions. This provision emphasizes not only the need to ensure issuance compliance but also to establish a comprehensive set of institutional safeguards covering cross-border operations, identifying restricted zones, and proactively blocking access.

Specifically, this includes the following three obligations:

1. Prohibition on providing services to specific regions

License holders must ensure that they do not engage in issuance or offering activities in jurisdictions where trading stablecoins is prohibited. Regulatory suggestions for achieving this include: verifying user identity documents (such as ID cards or passports) to identify nationality or residence; using IP addresses or GPS positioning technology to determine users' real geographic locations; applying technical restrictions on access from restricted areas to prevent download, registration, or purchasing activities. This requirement essentially mandates that license holders act as a 'geographic risk firewall,' cutting off potential outreach pathways to restricted areas from the point of issuance to prevent violations of foreign laws or triggering cross-border regulatory disputes.

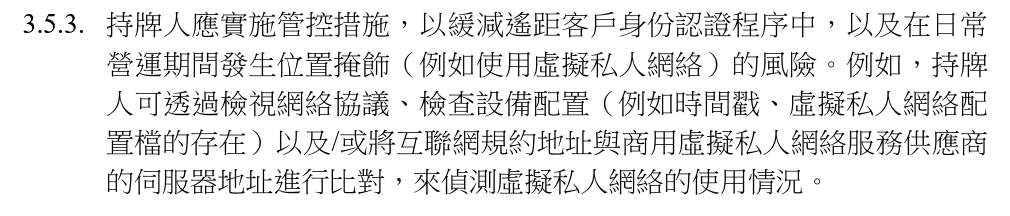

3.5.3 also clearly states that license holders need to detect whether users are using virtual private networks to determine whether a stablecoin is allowed in their location. Even if a virtual private network is used, it would still be considered a violation if stablecoins are not permitted in that jurisdiction. This significantly raises the user threshold, requiring each user to submit identification, with a cumbersome process that eliminates the 'use immediately upon wallet creation' experience. It may also make it difficult for global users to access; non-Hong Kong local users who are not explicitly included in the policy scope may not be able to use stablecoins issued by Hong Kong in practice. Transfers are also strictly limited; stablecoin license holders will be treated as financial institutions and must comply with FATF's relevant requirements regarding the transfer of funds. Before any transfer, they need to ensure that both the recipient and the initiator have completed KYC and provided relevant information; otherwise, the platform or contract may prevent the execution of the transaction.

This requirement from Hong Kong's regulation essentially transforms 'stablecoins' into controlled circulation electronic currency or bank token forms of electronic certificates, characterized not as decentralized assets universally applicable on-chain, but rather as: a digital tool with real-name binding, geographical restrictions, and regulatory attributes.

2. Overseas marketing and operations must be fully compliant

In addition to the obligation to block jurisdictions where trading is prohibited, the provisions also require license holders to ensure that all business operations and marketing activities (such as advertising, promotional collaborations, application deployment, etc.) comply with the relevant laws applicable to the target market. This means:

· Marketing content must not be pushed to unlicensed regions;

· Overseas partners must be assessed for compliance qualifications;

· Caution should be exercised when handling the language versions of websites, terms of service, etc., to avoid constituting the legal fact of 'actually providing services.'

3. Continuous Monitoring and Dynamic Adjustment Mechanisms

Regulators further require license holders to establish continuous monitoring mechanisms, closely monitoring policy changes across countries/regions, and timely adjusting their business strategies and technological measures. For example, if a country introduces a new ban on stablecoins, the issuer should immediately terminate related services; if regulatory standards are raised (such as requiring additional licenses or real-name requirements), KYC processes and compliance review systems should be updated accordingly.

In this regard, Dr. Xiao Feng, Chairman and CEO of HashKey Group, previously stated that in the traditional financial sector, anti-money laundering mechanisms heavily rely on identity-based information retrieval and account information connectivity. However, in practice, this system faces severe bottlenecks in scenarios involving multiple banks, regions, and cross-jurisdictional boundaries. In contrast, the on-chain tracking and address labeling mechanisms developed by the crypto industry in recent years provide another approach to anti-money laundering. In blockchain systems, every transfer is transparent, and the historical flow of funds for any address can be traced throughout the process. From token issuance, the first circulation, cross-chain transfers to final ownership, on-chain information has the characteristics of being immutable, globally readable, and synchronously updated in real-time, enhancing the efficiency and accuracy of identifying money laundering pathways.

Industry Impact Analysis: Project Parties, Users, and Market Chain Reactions

According to a field investigation by Techub News reporters, on the first day of the Hong Kong (Stablecoin Regulations) officially coming into effect on August 1, some cryptocurrency OTC offline stores, including One Satoshi, temporarily ceased operations due to concerns about violating regulatory red lines. Meanwhile, some OTC stores chose to continue normal operations, reflecting divergent understandings of the applicability of the new regulations within the industry. After the regulation was introduced, reactions from the Hong Kong Web3 industry varied. Some said, 'Finally, there is regulation,' but others candidly stated, 'This is not the kind of regulation we wanted.' Real-name systems, licensing requirements, and high barriers to entry have kept many native projects out. Especially as stablecoins cannot directly interface with DeFi, anonymous wallets and open contracts are excluded from compliance, which essentially makes it clear: Hong Kong stablecoins will not support free circulation on-chain.

For some teams that originally hoped to make Hong Kong a base for Web3, this is clearly a setback. If you want to issue tokens, you need to apply for a license; if you want to create wallets, you must ensure that every address is real-name verified—this deviates from the traditional meaning of 'Web3' and resembles 'Web2.5' or 'permissioned chain finance.' The more realistic issue is that the regulations will exclude some small and medium-sized entrepreneurs. Although the Hong Kong Monetary Authority claims to welcome innovation, it appears to welcome banks and giants more, and only invited institutions or platforms are eligible to apply for licenses. The entire system design seems to be aimed at allowing 'established powers' to lead the development of stablecoins, leaving individuals and small projects either watching from the sidelines or opting to leave. If the previous Hong Kong Web3 ecosystem was a wild growth, it is now a complete 'remodeling of order.' However, in the pursuit of compliance and financial stability, Hong Kong may also be losing the freedom that initially attracted developers.

Comparison with Regulatory Frameworks in Other Regions

Compared to the 'innovation exemptions' proposed in the recently introduced Project Crypto plan across the ocean, the new Hong Kong stablecoin regulations are characterized by clear regulation, stringent KYC real-name requirements, and strong anti-money laundering measures.

It can be seen that Hong Kong's current strategy leans more towards constructing a 'quasi-sovereign settlement tool,' emphasizing regulatory dominance and financial security, effectively shielding core capabilities of the Web3 ecosystem such as permissionless structures, contract invocation, and decentralized wallets from the regulatory framework. This somewhat presumes that stablecoins 'can only serve regulated financial institutions,' rather than being used as neutral infrastructure within the on-chain ecosystem.

In contrast, while the EU's MiCA also emphasizes KYC, it allows for some flexibility—such as exemptions for low-value transactions or permitting anonymous wallets. Singapore's DTSP is closer to a 'layered sandbox' approach, welcoming DeFi projects with risk control capabilities to gradually test the waters. In the United States, although regulation has long lagged, the signing of the (GENIUS Act), the release of the (PWG Report), and the launch of the 'Project Crypto' initiative have signaled a strong shift towards modernizing on-chain systems while balancing financial innovation. The current SEC chairman has emphasized in public speeches: 'We introduce regulation for the sake of regulation, which is akin to cutting off one's feet to fit into shoes.'

This comparison reveals core differences: Hong Kong bets on the compliance infrastructure for stablecoins, the U.S. shifts towards on-chain system modernization, the EU seeks universal standards, and Singapore maintains an openness to financial experimentation. Hong Kong's current route is more suitable for serving offshore settlements as a 'permissioned chain finance,' while its compatibility and attractiveness are relatively limited for Web3 paths that emphasize open ecosystems and anonymous circulation.

Conclusion: Can Compliance and Openness Be Balanced? Hong Kong is Still Testing Boundaries

Regulation must progress, but it should also leave room for flexibility. Hong Kong, as a financial center in Asia, is not only a testing ground for technology and systems but also bears the responsibility of setting paradigms for the region and even the world. However, while promoting KYC real-name systems, anti-money laundering, and traceability mechanisms, how to avoid completely erasing the space for on-chain privacy and how to retain a certain degree of openness and scalability while ensuring financial safety are the real long-term challenges of this legislation. As Dr. Xiao Feng said, the essence of blockchain's development lies in its permissionless nature. Anyone can freely join or leave the network, while the current emphasis on real-name systems and approval mechanisms in Hong Kong's stablecoin regulations, in a sense, deviates from this open logic.

Stablecoins are essentially an institutional innovative tool that links on-chain and off-chain, bridging traditional and future finance. If excessively 'paternalistic' regulation is enforced, it will not only be difficult to integrate into the current DeFi ecosystem but may also jeopardize Hong Kong's critical position in the global reshaping of digital financial order. In the next phase of implementation and interpretation, how Hong Kong finds a balance between rigid regulation and technological flexibility is worthy of continuous attention from all sectors.