Written by: Alex Liu, Foresight News

From JLP to Neutral

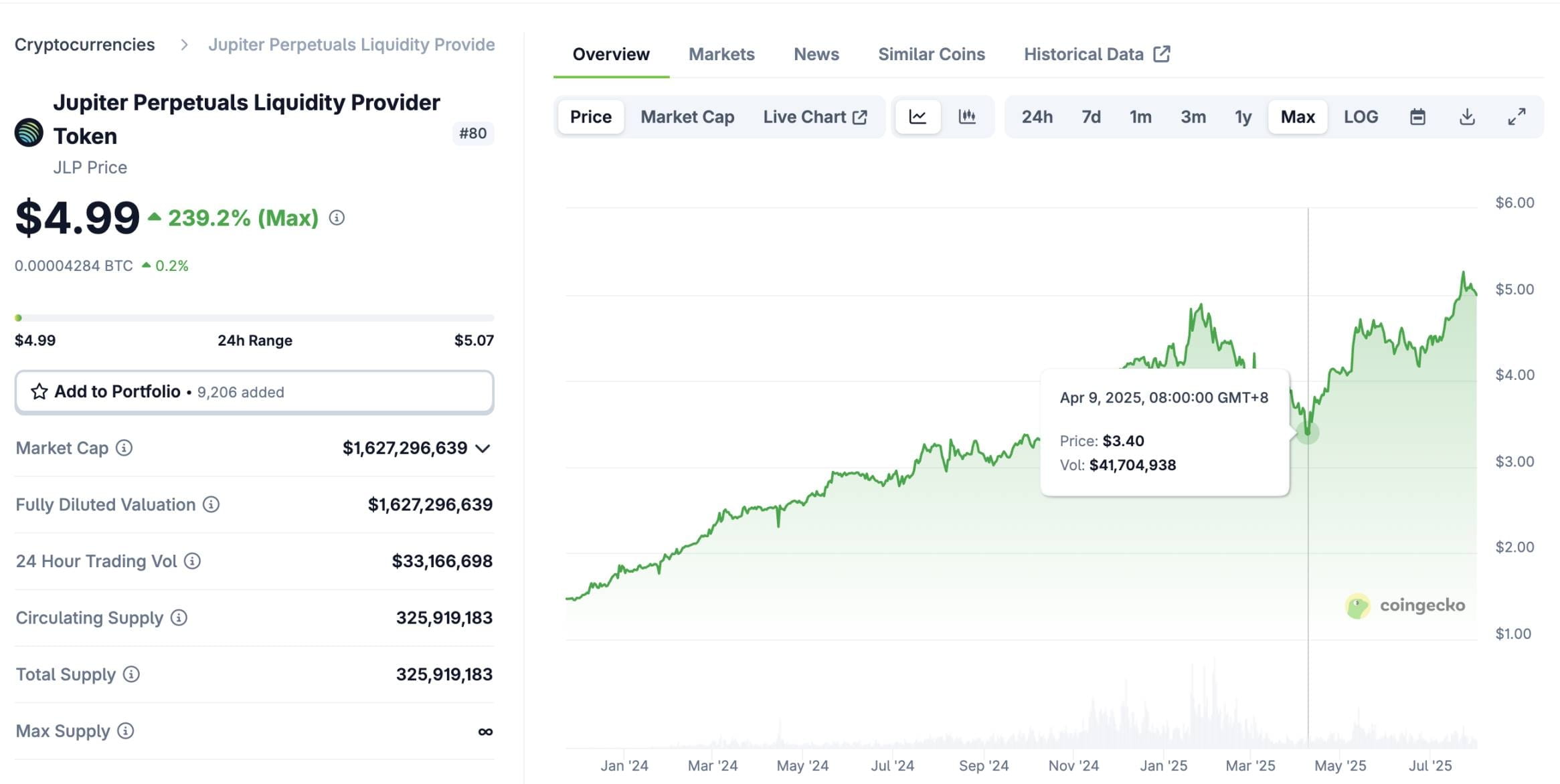

To make money, the first step is often to find quality assets. It is not an exaggeration to say that even looking at the entire cryptocurrency world, JLP is one of the top quality assets. It has increased threefold in one year, with a maximum drawdown of 30% in the subsequent three months. While performing excellently, it has a capital size of over $1 billion, which is extremely large. How did it achieve this?

Price trend of JLP, data: coingecko

JLP stands for Jupiter Perpetual Liquidity Provider Token. Holding JLP is equivalent to depositing money into Jupiter as a counterparty for contract traders. When contract traders profit, JLP will incur losses, and vice versa. After countless similar products have been repeatedly validated, and when looking at a longer time scale, contract traders always end up losing money; this is the first source of income for JLP.

Additionally, 75% of the trading fees from Jupiter perpetual contracts will return to JLP, and the substantial fee income allows JLP's annualized income to remain above 30% for a long time, sometimes even exceeding 50%.

JLP itself is composed of 47% SOL, 8% ETH, 13% BTC, and 32% USDC, maintaining exposure to the risks of cryptocurrency assets. Thus, in the strong year of SOL in 2024, along with the returns from the first two assets, JLP increased more than threefold. During the three months when SOL fell from $295 to below $100, due to limited risk exposure of JLP and the cushion provided by the first two assets, the decline was 30%. After SOL's price rebounded, JLP set a new high ahead of time.

In this view, the scenarios for JLP losses are either contract traders profiting in extreme market conditions (but statistics show they will eventually lose it back...), or the long-term price weakening of cryptocurrency assets. It seems that the long-term risk is only the latter. As long as we can hedge this portion of risk, we can obtain a high-yield strategy based on quality assets.

Neutral is an institutional-level on-chain strategy hedge fund on Solana, providing this strategy plan:

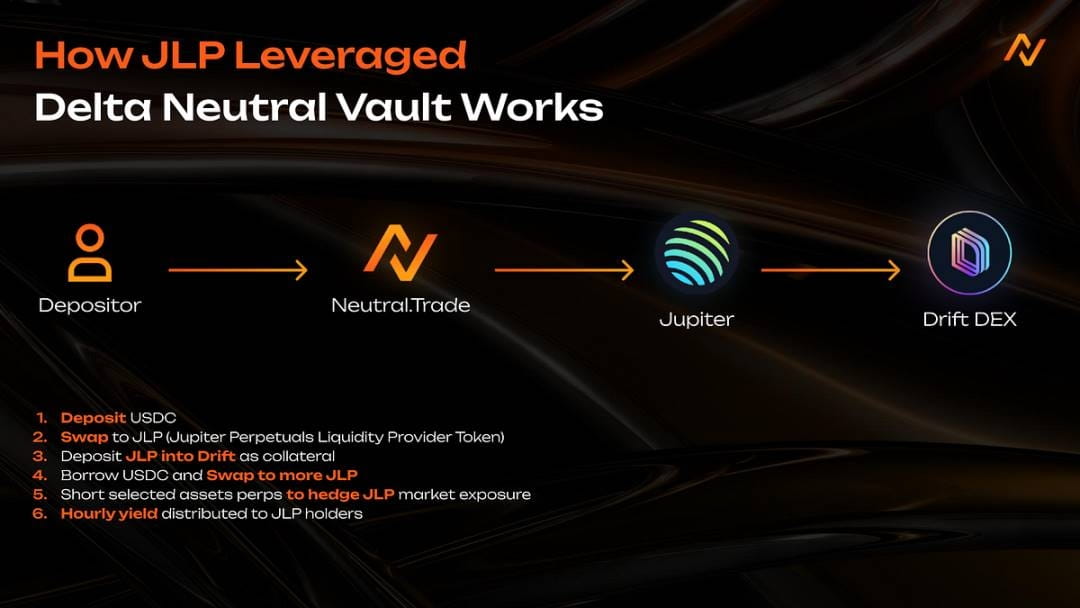

Users deposit USDC and convert USDC to JLP. They then use JLP as collateral in a lending protocol to borrow USDC and convert it back to JLP. (Profit is made when the annualized yield of JLP is greater than the borrowing interest), and finally use perpetual contracts (Drift) to short the corresponding cryptocurrency asset shares (SOL, ETH, BTC) of the held JLP to achieve risk neutrality in the strategy (theoretically, losses will not occur due to price fluctuations).

The Neutral treasury of this strategy now has a TVL (Total Value Locked) of over $12 million, with an annualized yield exceeding 15%, and the maximum drawdown is basically controlled within 2%.

Retail Risk vs Institutional Advantage

So why don't I execute this strategy myself and instead hand it over to products like Neutral? Doing it myself would not incur management fees (Neutral charges a performance fee of 10% to 25% for various strategies, deducted from the corresponding proportion of profits).

The reason is simple: retail investors often cannot effectively manage the risks associated with complex strategy yields.

In executing the above strategy, shorting hedges carry the risk of liquidation, abnormal funding rates, and the borrowing leverage portion carries the risk of losses due to long-term interest rate inversions. Even if one does not sleep and monitors the market, it does not necessarily mean there will be excess funds available to add margin in sudden situations or to untangle borrowing cycles.

On the other hand, institutional-level hedge funds benefit from team monitoring 24/7 and have rich experience and contingency plans for various systemic risks, making them indeed stronger than retail investors in terms of risk management. The premise for profits is the safety of the principal; whether one believes in adopting a Degen mode for the highest yields or sacrificing some yield for more secure risk management needs to be considered carefully based on individual circumstances.

Project Overview

Back to the Neutral project itself. It is not the only on-chain hedge fund in the market; the reason for introducing it is that it is collaborating with the Solana Chinese community for promotion and has relatively reliable backing. Additionally, it has an ongoing points system with expectations of token issuance, allowing users to earn strategy yields while also benefiting from project airdrops. (The point calculation rule is: 1 point is generated for every $1 of assets held for 1 year, equivalent to depositing $365 to earn 1 point per day.)

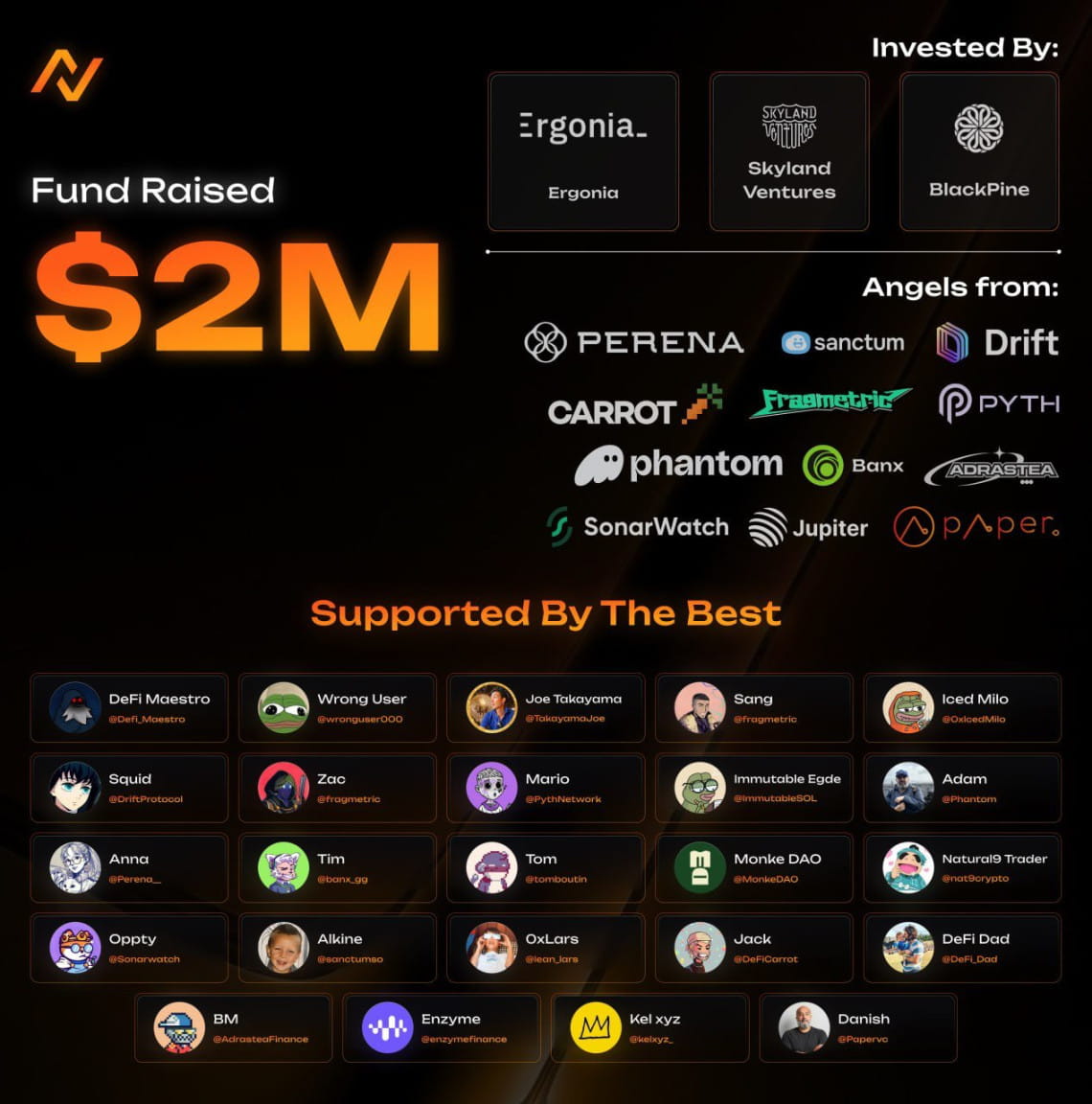

Neutral was initially a winning project at the Solana Radar hackathon and has now grown to nearly $36 million in TVL, generating close to $2.5 million in profits for users, and is an emerging protocol with considerable scale. The founders, Rick and Jared, are experienced quantitative traders from Goldman Sachs and one of the top three hedge funds in the world. On June 1st, Neutral announced it secured $2 million in funding from Cumberland and numerous Solana ecosystem projects and participants.

In addition to the main JLP neutral strategy, Neutral also has multiple yield strategies including Hyperliquid fee arbitrage. It is important to note that not all strategies are risk-neutral; those marked as Directional may experience significant fluctuations with market conditions, and interested readers can research them independently.