Author: Tiger Research Reports

Compiled by: Deep Tide TechFlow

TL;DR

Regulation and Government: 1) Hong Kong will introduce stablecoin legislation in August to consolidate its status as a digital financial center. 2) Singapore enforces a strict licensing system, prohibiting unlicensed companies from operating overseas. 3) Thailand launches G-Tokens, becoming the first country to issue government-issued digital bonds.

Corporate Dynamics: 1) Japanese listed companies see a wave of Bitcoin funding strategies, driving a surge in institutional investment. 2) Chinese companies adopt a pragmatic approach, using Hong Kong licenses to circumvent domestic restrictions and accumulate Bitcoin.

Policy Shifts: 1) In South Korea, the emergence of won-backed stablecoins as a post-election agenda is offset by ongoing regulatory fragmentation. 2) Vietnam has achieved a historic shift from prohibition to full legalization. 3) The Philippines implements a dual-track strategy combining strict regulation with a sandbox framework.

1. Asia Web3 Market Q2: Regulation Stabilizes, Corporate Investment Increases

Although the focus of the Web3 market has clearly shifted to the United States, developments in Asia's key markets remain noteworthy. Asia not only possesses the largest cryptocurrency user base globally but also continues to be a core hub for blockchain innovation.

Therefore, Tiger Research has been conducting quarterly reviews of the major trends in Web3 across the Asia region. In the first quarter of 2025, regulators throughout Asia laid the groundwork—introducing new legislation, issuing licenses, and launching regulatory sandboxes. Efforts to strengthen cross-border cooperation are also beginning to take shape.

In the second quarter, this regulatory foundation facilitated meaningful business activities and accelerated capital allocation. Policies introduced in the first quarter have been tested in the market, prompting continuous refinement and more concrete implementation.

Institutional and corporate participation has significantly increased. This report will analyze these developments in various countries during the second quarter and assess how changes in national policies affect the broader global Web3 ecosystem.

2. Major Developments in Asia's Key Markets

2.1. South Korea: A crossroads of political transformation and regulatory adjustment

Source: Tiger Research

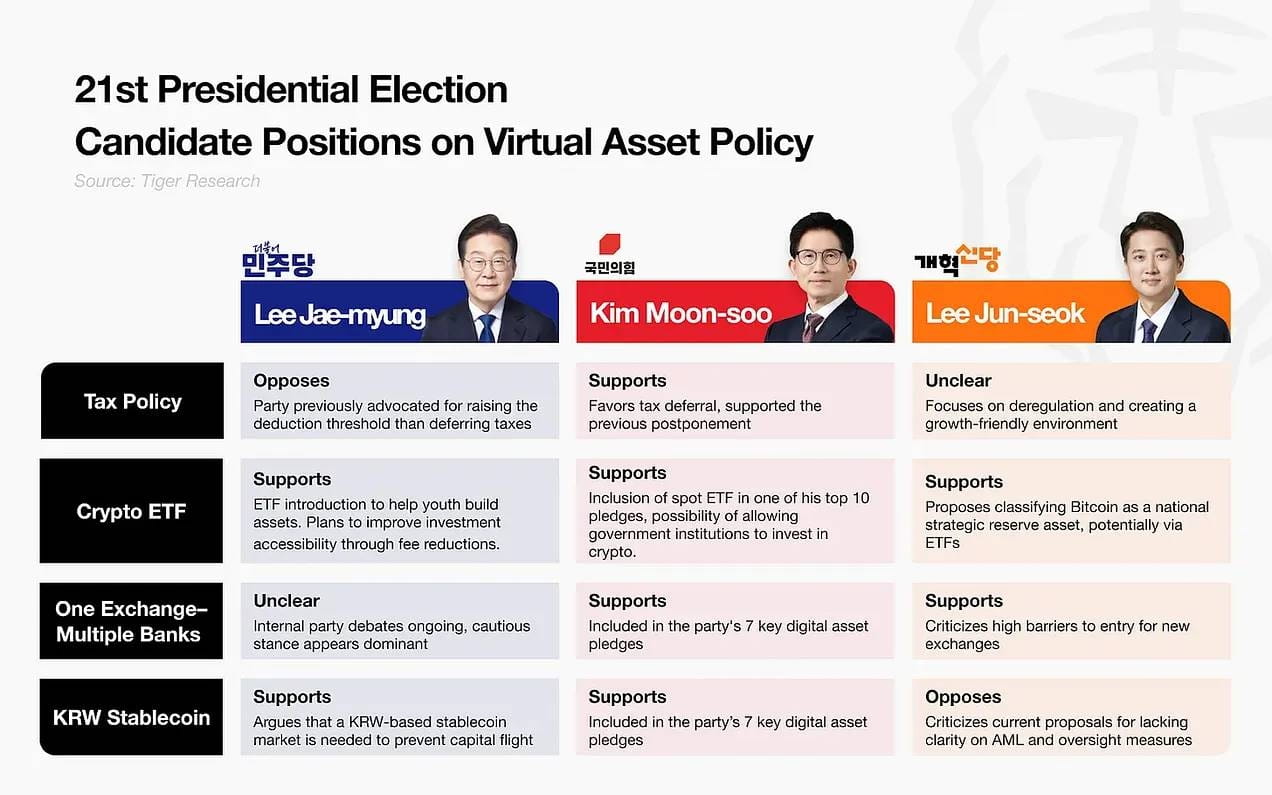

In the second quarter, cryptocurrency policy became a hot topic ahead of the June presidential election in South Korea. Candidates actively shared commitments related to Web3, and with Lee Jae-myung's victory, the market expects a significant policy shift.

One of the core topics of the meeting was the launch of won-pegged stablecoins. Stocks related to Kakao Pay surged, and traditional financial institutions have also begun applying for Web3-related trademarks in hopes of entering the market.

However, some conflicts arose during the policy-making process, most notably the jurisdiction dispute between the Bank of Korea and the Financial Services Commission (FSC). The Bank of Korea advocates for early involvement in the approval process, positioning stablecoins as part of a broader digital currency ecosystem alongside CBDCs.

In July, the Democratic Party announced a delay of one to two months for the introduction of the Digital Asset Innovation Act. The lack of a clear lead policymaker appears to be a major bottleneck, with negotiations among departments still operating independently. Thus, despite the focus on won-backed stablecoins, specific regulatory guidance remains lacking.

Nevertheless, the gradual improvement in institutional frameworks continues. In June, new regulations allowed non-profit organizations and exchanges to sell donated crypto assets and permitted immediate settlement. The rule also requires sales to be conducted in a manner that minimizes market impact.

Throughout the second quarter, interest in the South Korean market remained strong. Global exchanges continued to show sustained investment: Crypto.com Korea has completed integration with Upbit and Bithumb for the Travel Rule, while KuCoin has indicated plans to return to the Korean market after meeting regulatory standards.

Offline activities have also significantly warmed up. The number of meetups has increased dramatically compared to last year, with more international projects visiting Korea even outside of major conferences. However, the rise of promotional events (focusing more on giveaways than participation) has left local builders in Korea feeling fatigued.

2.2. Japan: Institutional and corporate adoption drives Bitcoin strategy expansion

Source: Bitcoin Treasury

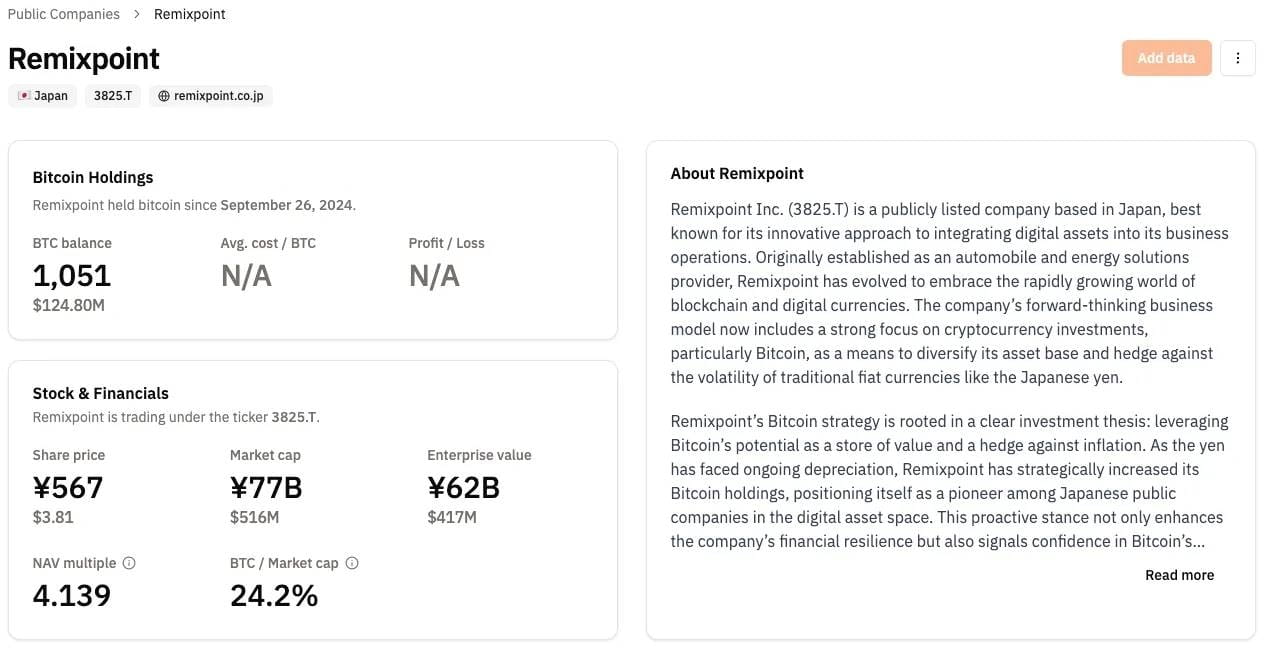

In the second quarter, Japanese listed companies experienced a wave of Bitcoin adoption, primarily driven by MetaPlanet, which saw about a 39-fold return after its initial Bitcoin purchase in April 2024. The performance of MetaPlanet has become a benchmark, prompting companies like Remixpoint to follow suit by allocating their own Bitcoin.

Meanwhile, progress has been made in building stablecoins and payment infrastructure. Sumitomo Mitsui Financial Group has begun collaborating with Ava Labs and Fireblocks to prepare for the issuance of stablecoins. Additionally, Mercoin, a cryptocurrency subsidiary of Mercari, has started supporting XRP trading, significantly enhancing the accessibility of cryptocurrency on the platform (with over 20 million monthly active users).

As private sector initiatives continue to advance, regulatory discussions are ongoing. The Financial Services Agency (FSA) of Japan has introduced a new classification system that divides crypto assets into two categories: the first category includes tokens used for financing or business operations; the second category refers to general crypto assets. However, most of these regulatory updates remain in discussion stages, with limited concrete amendments so far.

Retail investor participation remains sluggish. Japanese retail investors traditionally favor conservative strategies and are still cautious about crypto assets. Therefore, even with new market participants entering, retail capital is unlikely to flow in immediately.

This contrasts sharply with markets like South Korea, where active retail participation directly facilitated early liquidity for new projects. In Japan, institutional-led investment models provide greater stability but may limit short-term growth momentum.

2.3. Hong Kong: Expansion of regulated stablecoins and digital financial services

In the second quarter, Hong Kong improved its stablecoin regulatory framework, consolidating its position as the leading digital financial center in Asia. The Hong Kong Monetary Authority (HKMA) announced that new stablecoin regulations will take effect on August 1. A licensing regime for stablecoin issuers is expected to be introduced by the end of the year.

Source: HKMA

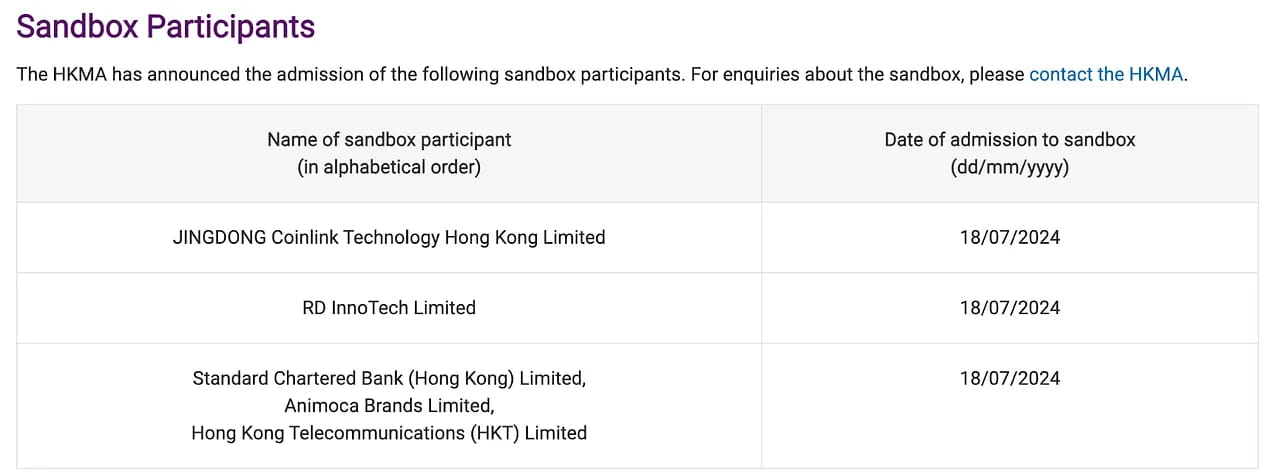

Consequently, the first regulated stablecoins are expected to launch in the fourth quarter, potentially as early as this summer. Companies that previously participated in the HKMA regulatory sandbox are expected to be the frontrunners, making their progress worth following.

The scope of digital financial services has also significantly expanded. The Securities and Futures Commission (SFC) announced plans to allow professional investors to trade virtual asset derivatives. Meanwhile, licensed exchanges and funds are permitted to offer staking services.

These developments reflect the regulators' clear intention to establish a more comprehensive and institution-friendly digital asset ecosystem in Hong Kong.

2.4. Singapore: Regulatory tightening between control and protection

Source: MAS

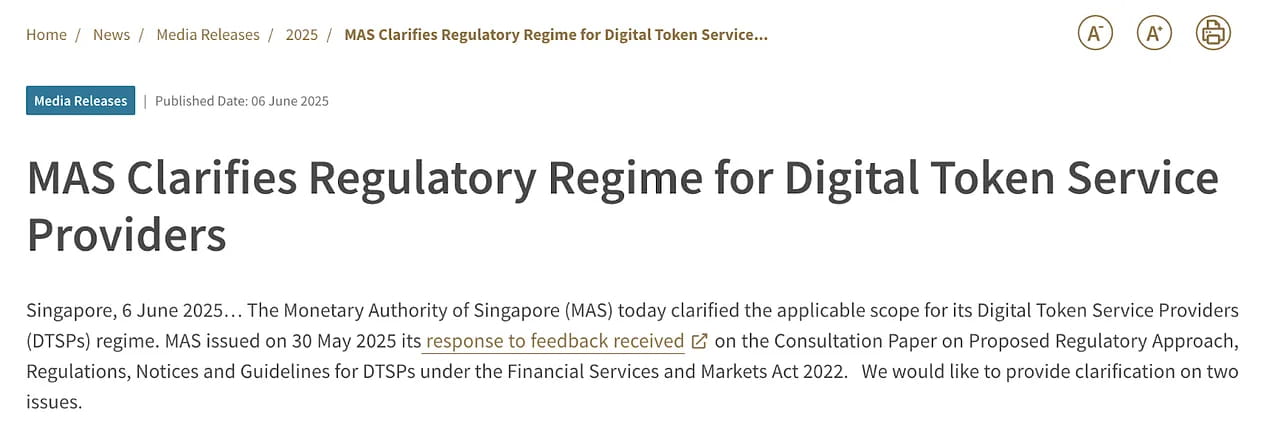

In the second quarter, Singapore adopted significant tightening measures regarding cryptocurrency regulation. Most notably, the Monetary Authority of Singapore (MAS) has comprehensively banned unlicensed digital asset companies from conducting business overseas, indicating its strong opposition to regulatory arbitrage.

The new regulations apply to all entities providing digital asset services to global users in Singapore, effectively mandating the formal issuance of licenses. The environment has changed: simple business registration is no longer sufficient to maintain operations.

This change has put increasing pressure on local Web3 companies. These companies now face a binary choice—either establish fully compliant operational entities or consider relocating to more lenient jurisdictions. While this move aims to enhance market integrity and consumer protection, it is undeniable that its impact on early and cross-border projects is limited.

2.5. China: Internationalization of digital yuan and corporate Web3 strategy

In the second quarter, China advanced the internationalization of the digital yuan, with Shanghai being the center of this effort. The People's Bank of China announced plans to establish an international operation center in Shanghai to support the cross-border application of digital currency.

However, a gap still exists between official policy and actual operations. Despite a nationwide ban on cryptocurrencies, reports indicate that some local governments (such as Jiangsu Province) have liquidated confiscated digital assets to fill budget gaps. This indicates a pragmatic approach by the Chinese government that diverges from the official stance.

Chinese companies have also demonstrated a similar pragmatic spirit. Logistics group AdanTex and others have begun to follow the example of Japanese companies by increasing their Bitcoin holdings. Some other companies are using Hong Kong's licensing system to bypass mainland restrictions and enter the global Web3 market—effectively breaking regulatory boundaries and participating in the digital asset economy.

Market interest in renminbi-pegged stablecoins is also growing, especially in the latter half of this quarter. Concerns about the dominance of U.S. dollar stablecoins and the depreciation of the renminbi have intensified these discussions.

On June 18, Pan Gongsheng, the Governor of the People's Bank of China, publicly articulated a vision for building a multi-polar global monetary system, hinting at an open attitude towards issuing stablecoins. In July, the Shanghai State-owned Assets Supervision and Administration Commission initiated discussions on the research and development of stablecoins pegged to the renminbi.

2.6. Vietnam: Legalization of cryptocurrency and enhanced digital control

Vietnam officially announced the legalization of cryptocurrency in the second quarter, marking a significant policy shift. On June 14, the National Assembly of Vietnam passed the Digital Technology Industry Law, which recognizes digital assets and outlines incentives for areas such as artificial intelligence, semiconductors, and digital infrastructure.

This marks a historic reversal of Vietnam's cryptocurrency ban, positioning the country as a potential catalyst for widespread cryptocurrency adoption in Southeast Asia. Given Vietnam's previous restrictive stance, this move represents a significant adjustment in regional cryptocurrency policy.

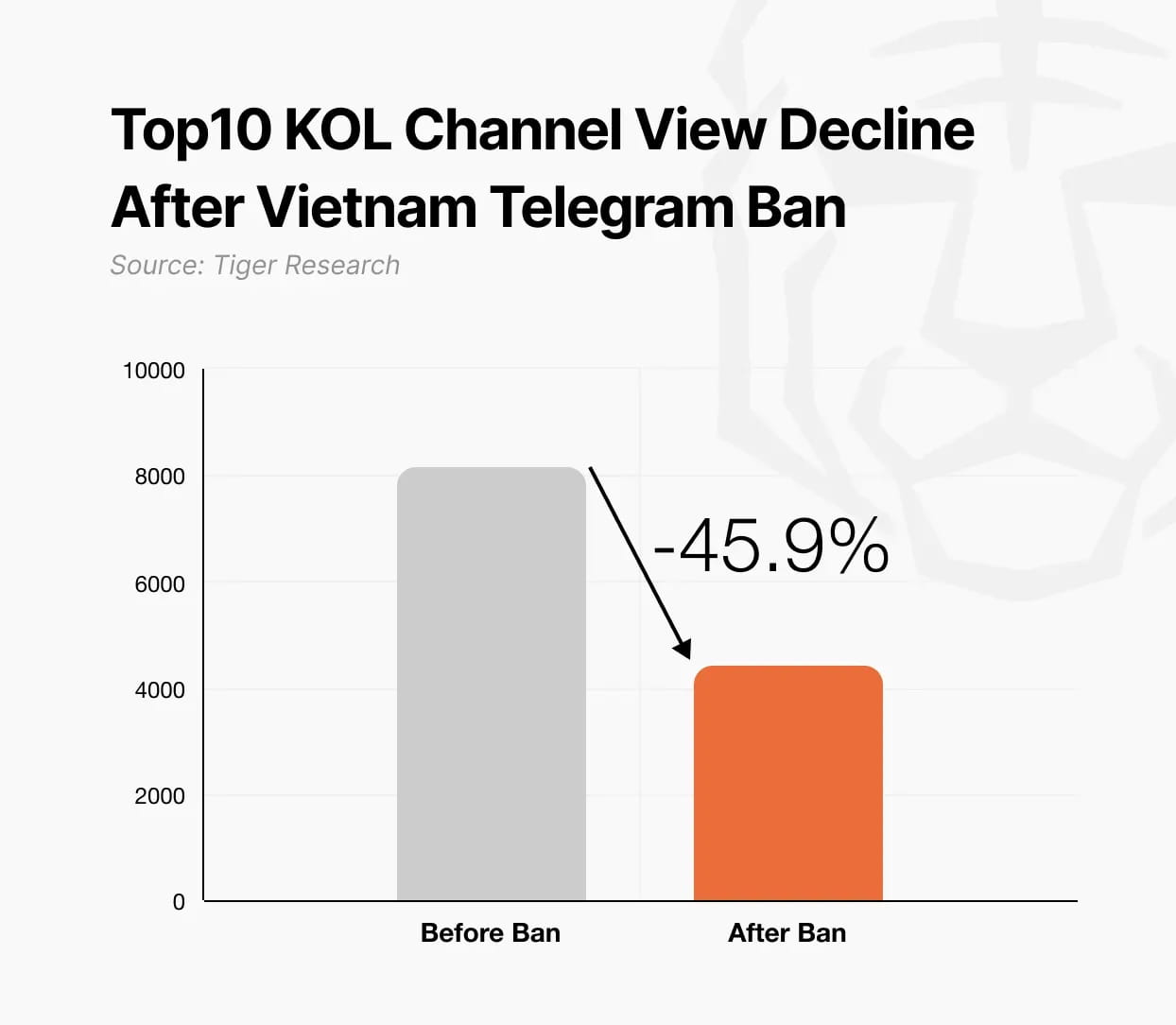

Meanwhile, the government has tightened control over digital platforms. Authorities ordered telecom operators to block Telegram, citing allegations that the app was used for fraud, drug trafficking, and terrorism. A police report found that 68% of the 9,600 active channels on the app were related to illegal activities.

This dual approach—legalizing cryptocurrency while combating digital abuse—reflects Vietnam's intention to allow innovation within a strictly monitored framework. While digital assets are now legally recognized, actions related to their use for illegal activities are facing stricter enforcement.

2.7. Thailand: State-led digital asset innovation

In the second quarter, Thailand advanced government-led initiatives in the digital asset sector. The Securities and Exchange Commission (SEC) of Thailand announced it is reviewing a proposal that would allow exchanges to list their own utility tokens—differing from previous strict listing rules, which is expected to enhance operational flexibility on the platform.

Notably, the Thai government announced plans to issue its own digital bonds. On July 25, Thailand will issue 'G-Tokens' through an approved ICO platform, with a total issuance scale of $150 million. These tokens will not be usable for payments or speculative trading.

This initiative is a rare example of direct government involvement in the issuance of digital assets. Globally, Thailand's approach stands as an early model of public sector-led tokenized financial digital innovation.

2.8. Philippines: A dual-track system of strict regulation and innovation sandbox

In the second quarter, the Philippines implemented a dual-track strategy that combines stricter regulation with support for innovation in the cryptocurrency space. The government has imposed stricter controls on token listings, with regulatory authority shared between the central bank and the U.S. Securities and Exchange Commission (SEC). Registration and anti-money laundering compliance requirements for Virtual Asset Service Providers (VASP) have also been significantly relaxed.

A particularly notable initiative is the introduction of influencer regulation. Content creators promoting crypto assets must now register with the relevant authorities. Violations may result in penalties of up to five years in prison, making it one of the strictest enforcement regimes in the region.

In addition to these measures, the government has launched a framework to promote innovation. The U.S. Securities and Exchange Commission (SEC) has begun accepting applications for 'StratBox,' a sandbox program designed to support crypto service providers in a controlled regulatory environment.