In money laundering involving virtual currency black and gray industries, we often hear a term: fourth-party payment.

What is fourth-party payment? In practice, how do the black and gray industries launder money through fourth-party payment platforms? Let’s explore it together today.

What is fourth-party payment?

Before understanding fourth-party payment, let’s first take a look at what first-party payment to third-party payment is all about.

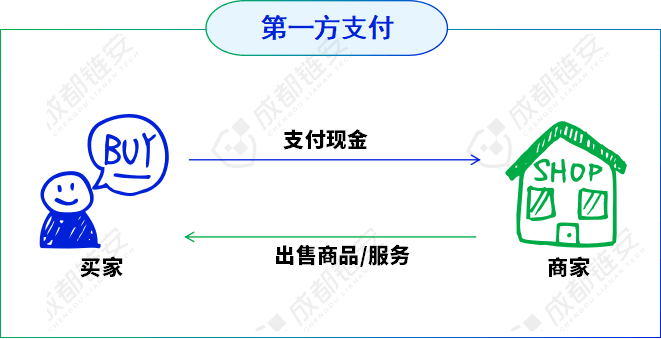

01First-party payment:

First-party payment is cash payment. The buyer and seller settle directly in cash, with one hand paying the money and the other hand delivering the goods, and there is no involvement of any intermediary agency in the transaction process.

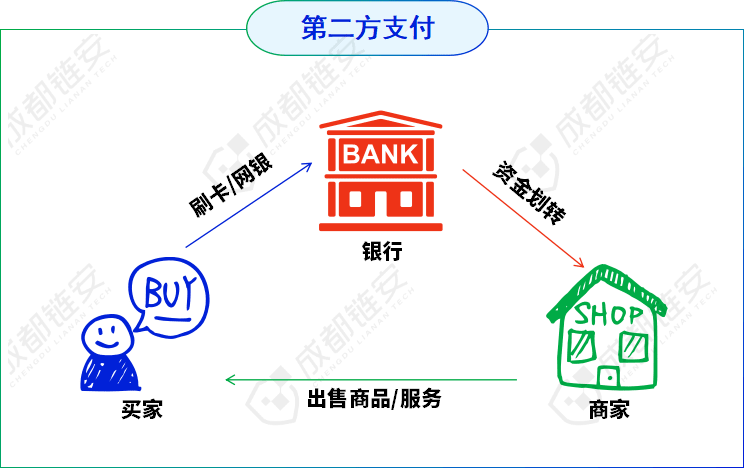

02 Second-party payment:

Second-party payment is a payment method that relies on bank accounts (for example: UnionPay POS card, online bank transfer, remittance, etc.). Buyers and sellers transfer transaction funds through banks, and the security of funds is also guaranteed by the banking system. Its essence is that banks act as fund intermediaries and complete the fund transfer between buyers and sellers through their own clearing systems or the central bank's clearing system.

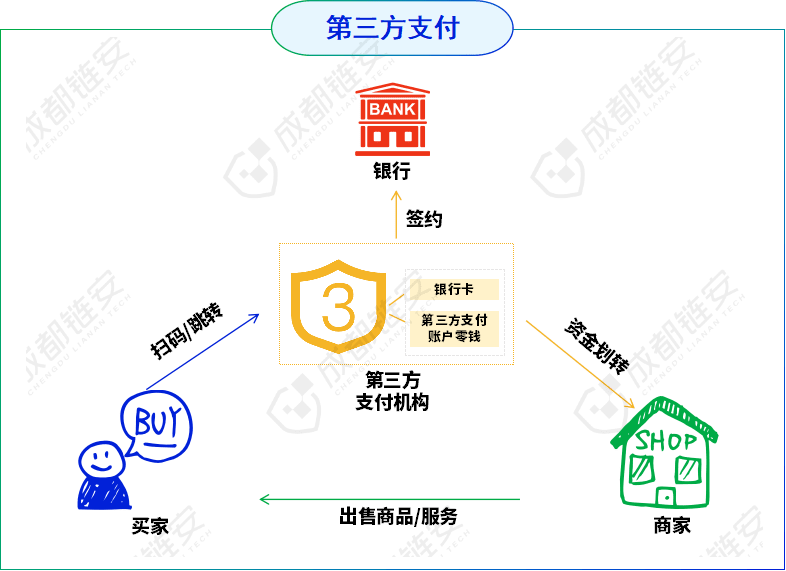

03Third-party payment:

Third-party payment is an online payment model conducted through non-bank third-party payment institutions. It has become increasingly popular with the development of online shopping and mobile payments, such as Alipay, WeChat, and UnionPay. Third-party payment institutions must obtain a (payment business license) (i.e., a "payment license") in accordance with the law.

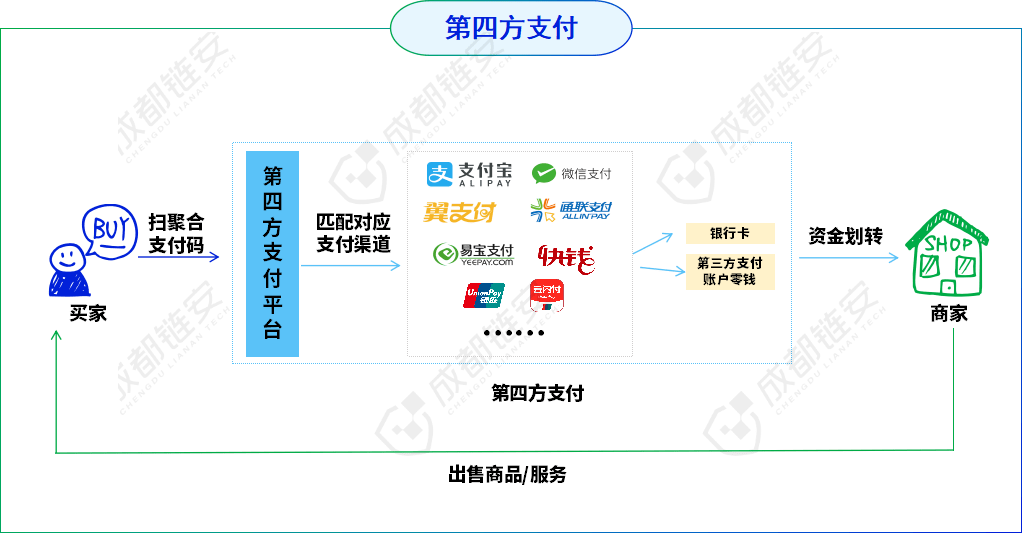

04Fourth-party payment:

Fourth-party payment is an aggregate payment developed on the basis of third-party payment. It is a comprehensive payment service that integrates multiple payment service methods such as banks and third-party payments through technical means. Common aggregate payment products include aggregate scanning, smart POS, scanning guns, scanning boxes, etc.

In my country, legal fourth-party payment (an acquiring outsourcing service agency registered with the China Payment and Clearing Association, and whose "business type" is aggregated payment technology services, and the payment services provided can be considered legal fourth-party payment) can only serve as a "acquiring outsourcing agency" for a third-party payment institution, and may not engage in core businesses such as qualification review, agreement signing, and fund settlement; it may not handle the settlement funds of designated merchants in any form, or engage in or engage in fund settlement in disguise.

While fourth-party payment improves payment efficiency, it is also used by criminals, who build illegal fourth-party payment platforms to launder money for upstream crimes such as online gambling and online fraud.

How does illegal third-party payment launder money?

Fourth-party payment platforms usually rely on third-party payment platforms (such as Alipay, WeChat Pay, etc.) for fund settlement, but they do not need to obtain a payment license to operate. This low threshold allows criminals to quickly build illegal payment channels for money laundering. The fourth-party payment platform plays the role of a "middleman" in the money laundering chain and can provide fund settlement services for upstream crimes (such as online gambling, telecommunications fraud, and the spread of obscene videos). Illegal elements "launder" illegal funds through fourth-party payment platforms, making the funds look like legal transactions, thereby evading supervision and crackdowns.

Typical patterns of money laundering through illegal third-party payment platforms include:

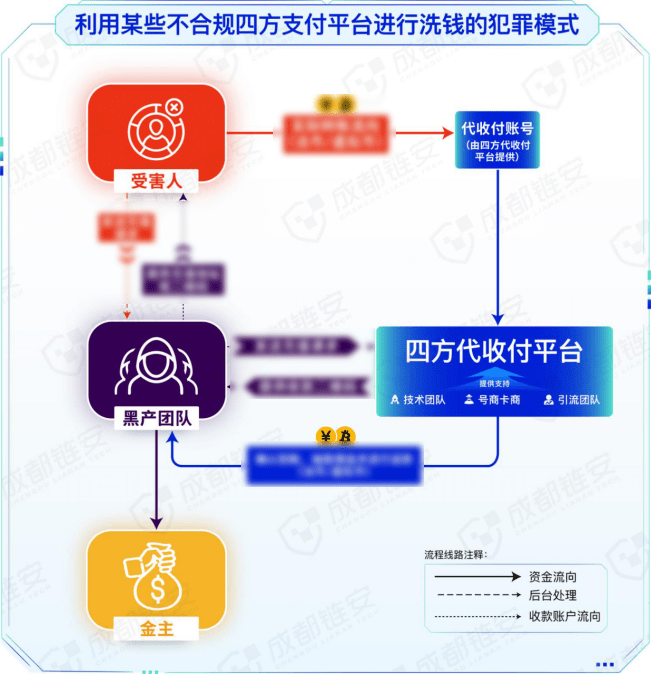

1. Fourth-party payment + fake merchant model:

Criminals build illegal fourth-party payment platforms, and then obtain a large amount of personal information of citizens through leasing, acquisition, information trafficking, etc., register e-commerce, entity and other corporate merchant accounts, open third-party payment channels and aggregate them to their own fourth-party platforms. When upstream crimes (online gambling, electronic fraud, pornography, etc.) have money laundering needs, they receive the stolen money through the third-party payment channels of the controlled merchants, and then transfer the funds to the accounts of upstream criminals through refunds, settlements, and multi-layer nested transfers between merchant accounts in different industries.

2. Fourth-party payment + virtual goods model:

This model is actually a fourth-party payment platform using e-commerce platforms + empty package logistics to launder money. Taking gambling as an example, criminals build fake e-commerce platforms or register online stores on legal e-commerce platforms. After the store registration is completed, fake products with corresponding prices will be put on the shelves according to the recharge amount of online gamblers (they will not actually be shipped), and part-time jobs will be used to recruit people to swipe orders. The order-brushing personnel take pictures of the goods in the store, and they do not need to pay for them themselves, but choose to find someone to pay for them. The fourth-party payment platform has already been connected with the upstream gambling gangs. When gamblers recharge, they actually pay the payment order generated by the order-brushing personnel. After the recharge is successful, the fourth-party payment platform informs the store that the payment is completed, and the store completes the entire money laundering process through false shipments.

In addition to fake goods, there are also various low-priced recharge services in online stores. One feature of this type of recharge service is that it is more favorable than the normal recharge price, but the recharge amount will not be credited immediately, but there is a certain time delay (because the recharge orders of real users need time to match the appropriate upstream money laundering needs).

3. Fourth-party payment + running point platform model:

This is one of the most typical money laundering models through illegal third-party payment. Criminals set up illegal third-party payment platforms, connect with gambling, fraud, pornography and other criminal gangs, provide them with aggregated recharge channels, and connect with running points platforms to issue recharge requirements, thereby laundering the stolen money.

Take gambling recharge as an example: criminals graft the fourth-party aggregate payment interface to the recharge channel of the online gambling platform. When the gambler recharges, the fourth-party platform issues a running task to the running platform. The runners use their own bank cards, WeChat/Alipay and other payment codes to receive the gambler's funds by grabbing orders. Finally, the received funds are transferred to the corresponding channels in legal currency or converted into virtual currency to complete the gambling fund laundering. Sometimes, the running platform will also directly transfer the deposit paid by the runner to the running platform to the corresponding channel.

It is worth noting that in the fourth-party payment + running point platform money laundering model:

1. In addition to using bank cards, WeChat/Alipay and other QR codes to run points, it is increasingly common to use virtual currency to run points on the current running points platform. The runner submits a bank card and payment code to the running points platform for payment, and also needs to submit his or her virtual currency platform account address, and purchase virtual currency and transfer it to the running points platform as a deposit. After receiving the running points "task", the runner receives the stolen money and converts it into virtual currency and transfers it to the designated on-chain address.

2. In order to avoid risks, some illegal third-party payment platforms will directly recruit scoring platforms instead of building their own. The fourth-party payment platform only provides an interactive interface, connecting the scoring platform, gambling platform, online fraud and other project parties in series, and then act as a "middleman" to earn the difference.

3. The scoring platform turned to TG Guarantee Public Scoring, and transferred and laundered the stolen money through various fleets;

4. In addition, some places will be running points platform = fourth-party payment, in fact, there is still a certain difference between the two.

Money laundering model of virtual currency fourth-party payment platform:

With the rapid development of virtual currency, the black and gray industries are using virtual currency to launder money more and more widely. The virtual currency fourth-party payment platform mentioned here is not a fourth-party payment platform in the strict sense, but a variety of virtual currency wallet acceptance platforms that we often see in the black and gray industries. This type of platform is widely used in the current black and gray industries to launder money.

Most of these platforms are named "✲✲ Wallet" and "✲✲ Pay". In fact, they are not real virtual currency wallets, nor are they truly decentralized. These platforms were originally designed to facilitate the ups and downs of gambling platforms, but now they have become fund settlement platforms that provide virtual currency and legal currency exchange services for online gambling, electronic fraud, pornography and other black and gray industries. Common platforms of this type include: EBpay, OKpay, K-Bean Wallet, GOpay, Wave Coin Wallet, TOpay, NO Wallet, kolpay, ULinx, 808 Wallet, 988PAY, etc.

Generally speaking, these platforms will launch their own platform coins. For example, EBpay has issued EB coins, which are pegged to RMB at a 1:1 ratio, with 1EB = 1 RMB. Platform coins are limited to users' internal circulation and exchange within the platform, but some online gambling platforms can also directly use these platform coins to place bets.

Is it safe to buy coins on such platforms? What are you thinking? How do you know that the U you bought is not a black U from underground banks or other channels?

You need to be even more vigilant when selling coins. No matter it is platform coins or USDT, the funds for the transaction orders matched to you may come from stolen money such as cyber fraud, online gambling, underground banks, etc. Once the transaction is made, there is a risk of card freezing.

In addition, such platforms will use the gimmick of selling coins at high prices to attract users to buy mainstream virtual currencies such as USDT from legal channels to "move bricks" on the platform. When users put their U on the platform for sale, they are actually exchanging their clean capital for dirty money, helping criminals to launder the stolen money. And because the platform lacks a real-name authentication mechanism, you have no way of knowing who the real counterparty you are trading with is.

In reality, there are many cases where people’s credit cards were frozen and they were asked to refund money because they sold coins on such platforms. They originally wanted to make a profit from the price difference, but ended up becoming accomplices of money laundering in the black and gray industries.

It is worth mentioning that after users recharge their wallets to these black and gray production platforms, operations within the platform cannot query the flow of funds and information on the chain, which is similar to the black box of the exchange. The virtual currency recharged by users eventually goes to the official wallet address of the platform.

In recent years, in order to evade crackdowns and tracking, the money laundering methods of black and gray industries have been constantly changing and new money laundering methods have continued to emerge: from offline to online, and then to online and offline (such as various door-to-door cash laundering methods); from bank card money laundering to virtual currency, running point platforms, fourth-party payment, underground banks and other methods.

In this article, we briefly introduce some typical money laundering models of fourth-party payment, hoping to help you understand this type of money laundering. In practice, the means of money laundering through fourth-party payment platforms may be more complex and diverse, the money laundering chain is longer and more hidden, and it is more difficult to detect and combat.Welcome to join the chat room to communicate!