Author: thedefireport

Compiled by: Blockchain in Plain Language

Stablecoins—long regarded as the pillar of on-chain finance by the cryptocurrency community—are about to gain legitimate recognition from US regulators.

As Tom Lee said, this is the 'ChatGPT moment' for cryptocurrency— the first crypto product with mainstream utility and institutional clarity.

Summary of new legislation

(Guiding and establishing the US Stablecoin National Innovation Act) (GENIUS Act) may be the most influential legislation in the history of cryptocurrency.

This bipartisan bill establishes the first federal framework for payment stablecoins, aiming to inject confidence, clarity, and institutional legitimacy into the stablecoin market worth over $260 billion.

Key points:

Asset backing: Issuers must fully back stablecoins 1:1 with high-quality liquid assets. Permissible reserve assets are limited to cash, insured bank deposits, money market funds, or short-term government bonds. USDT currently does not meet this requirement (more details later).

Payment only: Issuers may not pay interest to stablecoin holders, ensuring stablecoins serve solely as digital cash equivalents (avoiding becoming bank-like products). This is a 'strategic concession' to banks, buying time for them before stablecoins provoke deeper financial system disruption.

Bankruptcy protection: If the issuer goes bankrupt, stablecoin holders have priority claims on reserve assets (prioritized over the issuer).

Transparency and auditing: Issuers must disclose reserve status monthly and undergo regular audits.

Anti-money laundering compliance: The bill requires strict AML (anti-money laundering) and KYC (know your customer) measures, and issuers must implement compliance programs, verify customer identities, and report suspicious activities.

Regulatory structure: The bill authorizes federal and state (asset size < $10 billion) regulators to oversee issuers, with the US Treasury as the primary regulatory agency.

Issuer qualifications: Banks, fintech companies, and even large retailers (like Walmart) can issue stablecoins, but publicly traded companies primarily engaged in technology, social media, or e-commerce are prohibited from issuing.

By combining the reliability of the dollar with modern public blockchain networks, the bill lays the foundation for the widespread adoption of stablecoins in business and finance, while being under strict supervision by US regulators.

Impact on USDC and USDT

Does the GENIUS Act favor Circle?

We do not believe that is the case. Although the bill requires stablecoins to be backed 1:1 by dollar assets (cash, money market funds, government bonds), Tether's (USDT) current asset composition (80-85% compliant with the requirement, the rest including gold, bitcoin, and corporate debt) does not meet the bill's standards, but this is not fatal for Tether.

Why is Tether unaffected?

According to the bill, if offshore issuers (like Tether) wish to enter the US market, the Treasury can conduct compliance comparison tests. As long as their rules are consistent with US standards, Tether can continue to operate in the US market. Therefore, Tether has multiple ways to achieve compliance, and we expect they will do so.

Who will dominate the US market, USDC or USDT?

Perhaps the more important question is: Which fintech company will be the first to integrate stablecoins into mainstream products? Circle? Tether? Stripe? Paypal?

The answer is still unclear, and it is unknown how the product will be formed. But it is expected that there will be a large number of stablecoin issuers, and competition will drive down issuance costs. The ultimate winners may prevail through services surrounding stablecoins, such as:

Payroll payments: Smart contracts + stablecoins can be used for payroll/contractor payments, automatically triggering milestones or delayed payments, simplifying management and accounting processes.

Faster payment speed: Increased currency circulation speed brings income-generating currency.

Emerging markets

Emerging markets are not 'race to the bottom'. These markets are full of potential blue oceans, and Tether occupies a dominant position in them.

In emerging markets, stablecoin holders do not need to earn returns because holding stablecoins is valuable in itself. For example, in Argentina, stablecoins protect holders from double-digit or even triple-digit inflation.

[Personal observation: Last year I spent 5 weeks in Buenos Aires and witnessed the proliferation of stablecoins firsthand. Many locals exchanged Argentine pesos for USDT through crypto trading platforms (like BN) as a 'store of value' tool.]

We believe Tether will continue to dominate emerging markets while its relationship with the US government will become closer (see subsequent analysis for details).

Impact on fintech companies

We expect that in the coming years, every major fintech company will launch its own stablecoin. Paypal has taken the lead, and Stripe may be next.

Block (Square/Cash App), Robinhood, SoFi/Chime, and international fintech companies (like Revolut, Wise, MercadoPago) are all potential candidates.

Reason?

These companies have large user bases, global infrastructure, and strong balance sheets and banking partners.

Stablecoins provide a global 24/7 payment channel, lowering costs for merchants and e-commerce customers while bringing new revenue sources (according to the GENIUS Act, fintech companies can retain profits).

Impact on American banks

Banks are in trouble. We believe the future of banking will be fintech companies built on cryptocurrency rails, fundamentally different from today’s banks.

But just as the post office still exists after the popularity of email, banks will not disappear. Innovative banks and fintech companies will thrive, while slow-moving banks will become 'post offices' in five years.

Why are American banks in trouble?

Lack of innovation: Banks are large and bureaucratic, and employees lack incentives to take risks.

No motivation to issue stablecoins: Stablecoins will disrupt the banking business model. Banks profit from deposits, investments, and net interest margins. If they issue stablecoins, funds cannot be used for lending and become 'dead capital'. Although banks may issue stablecoins for interest income, they will ultimately need to share profits with holders.

Banks will not disappear, but the GENIUS Act accelerates the crisis for the slow movers.

Impact on Visa/Mastercard

Reminder: Stablecoins can settle almost instantly, supporting global peer-to-peer transactions at low cost.

Traditional card payment fees can be as high as 200-300 basis points (including issuing/acquisition fees, exchange rate spreads, and transaction fees), and settlement takes 2-3 days.

Stablecoins are clearly a superior product and will be used for:

Merchant payments, e-commerce, remittances, subscriptions, cross-border payments, payroll, etc.

This will completely bypass card payment rails and pose a significant threat to the $200 billion card payment fee industry.

Reason?

Anyone can build services on public blockchains, and Visa/Mastercard cannot control the infrastructure.

Fintech companies, wallets, and stablecoin issuers can directly tap into global funding flows without card network membership.

Visa/Mastercard's countermeasures:

Transform 'card payment only' into a multi-rail infrastructure supporting stablecoins as settlement currency.

Provide compliance services: fraud detection, refund/dispute handling, identity verification.

Launch USDC and PYUSD-backed stablecoin branded cards to maintain front-end competitiveness.

What does this mean?

Stablecoins are forcing Visa/Mastercard to transform from 'value transfer' networks to 'trust and tool' providers. The saved card payment fees will benefit merchants, stablecoin issuers, consumers, and fintech companies integrating new services.

Impact on the dollar's dominance

Stablecoins are extremely beneficial for the US and the dollar, regarded as a 'godsend for cryptocurrency'.

Reason?

Tether was the fifth-largest buyer of US debt last year!

If Tether were a country, its holdings of US debt would rank 18th globally!

This trend has only just begun (thanks to the new regulatory framework).

Bold prediction: Tether could become one of the most important innovations in the dollar's growth history.

We believe the current government wants to support Tether's development both domestically and internationally. Tether is provided reserve custody by Cantor Fitzgerald and has 450 million global users (most outside the US).

When international users purchase USDT as a store of value, Tether buys US debt, thereby diversifying the holders of US debt from sovereign nations to global individuals. This is undoubtedly welcomed by the US government.

Stablecoins not only expand the global network effect of the dollar but also diversify the holding base of US debt.

Scott Bessent understands this well, which is why he is an active promoter of stablecoins and the GENIUS Act.

All stablecoin issuers are critical to the dollar, but offshore issuers (like Tether) are especially key—they bring new US debt buyers, expand the dollar's network effect, and provide financial services to the unbanked.

We believe the relationship between Tether and the US government will become increasingly close and is worth watching closely.

How to invest in stablecoins

Stablecoins are primarily distributed on Ethereum (including L2, accounting for 55%). Tom Lee referred to Ethereum as the 'home of stablecoins' on CNBC.

Personally, I prefer USDC on Solana for its better user experience, but currently only 4.2% of stablecoins are on Solana.

Investment advice:

ETH/SOL: The safest long-term stablecoin investment choice.

COIN and HOOD: Considered alternative options, but both are at historical highs.

Circle: Overvalued (TTM P/E 2612), not recommended to chase high.

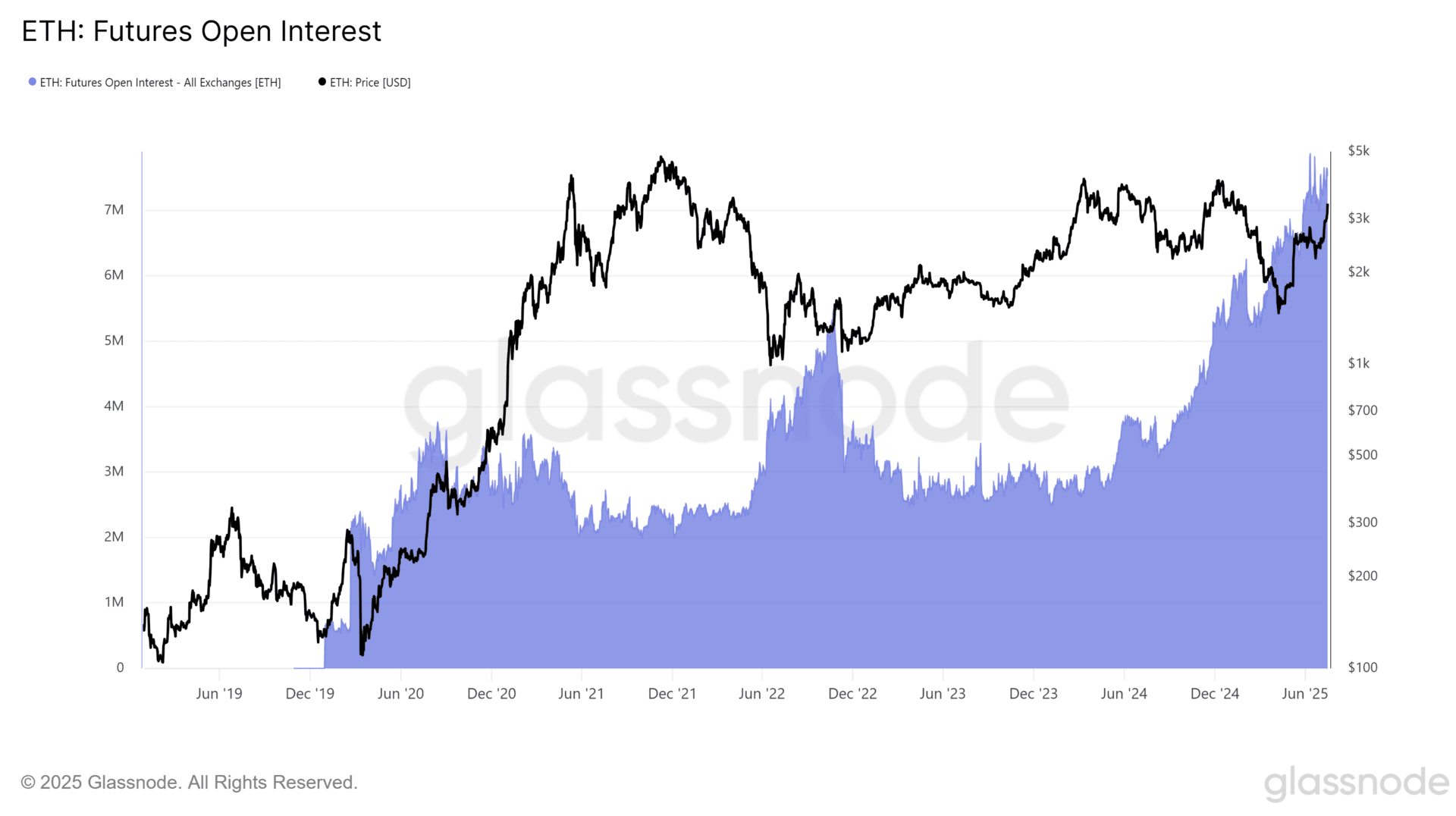

High risk/high reward: Ethena and Sky (MakerDAO). Ethena is attractive due to regulatory arbitrage from the GENIUS Act (offshore profit sharing), and USDe demand, ENA prices, and ETH open interest are positively correlated.

Data: Glassnode

In summary, the supply of stablecoins, on-chain transaction speeds, prices, and volatility are all on the rise.

Buckle up!