Author: MONK

Compiled by: ShenChao TechFlow

The trading code is $ETH.

Wall Street is experiencing a highlight moment for cryptocurrency.

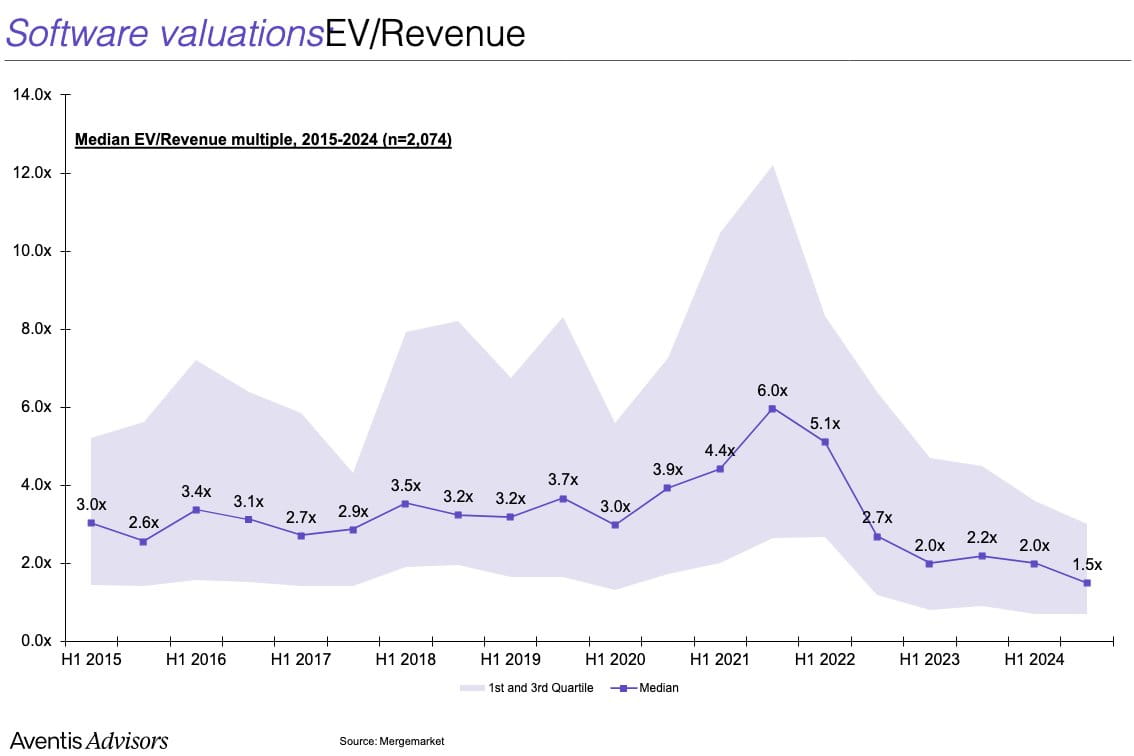

Traditional finance (TradFi) is exhausting the resources of growth narratives. Artificial intelligence has become the hot topic in the market, but the attention on it has become excessive, while software companies are far less attractive than they were in the 2000s and 2010s.

On a deeper level, growth investors who raise capital for innovative stories and large total addressable markets (TAM) know full well that most AI-related companies are valued at absurdly high premiums, and other so-called 'growth narratives' are no longer easily found. Once highly regarded FAANG stocks are gradually transforming into composite assets that are 'high quality, profit-maximizing, with moderate annual growth rates.'

For example, the median enterprise value to revenue (EV/Rev) multiple for software companies has fallen below 2.0 times.

At this moment, cryptocurrency made its appearance.

Bitcoin ($BTC) breaking through historical highs, the U.S. President heavily promoting our assets at a press conference, and a wave of favorable regulatory winds bringing the cryptocurrency asset class back into the spotlight for the first time since 2021.

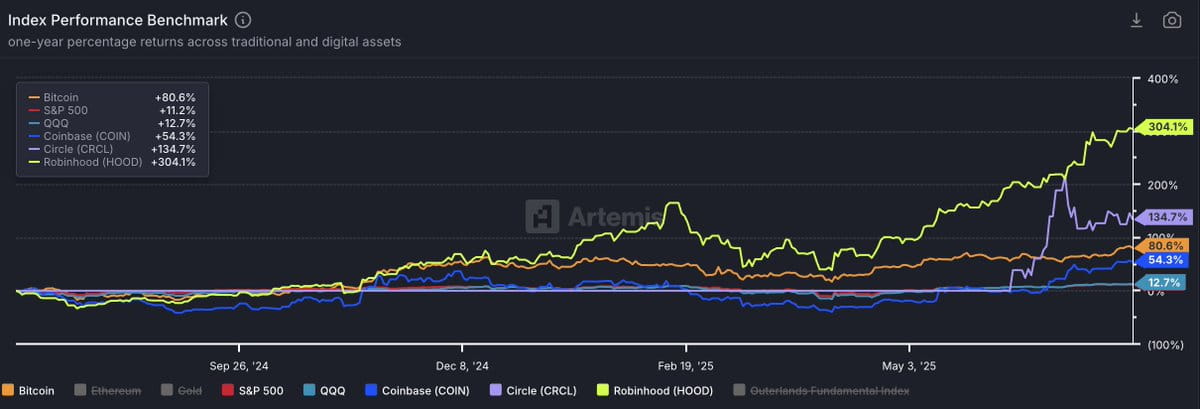

BTC, COIN, HOOD, CIRCLE vs. SPY and QQQ (Source: Artemis)

This time, the main characters are no longer NFTs and Dogecoin. This time, it is the era of digital gold, stablecoins, 'tokenization,' and payment reform. Stripe and Robinhood are claiming that cryptocurrency will be the core focus of their next growth round; $COIN (Coinbase) has successfully joined the S&P 500; Circle is demonstrating that cryptocurrency is attractive enough for growth stocks to ignore earnings multiples again.

But how does all of this relate to $ETH?

For us cryptocurrency natives, the realm of smart contract platforms looks very fragmented. There’s Solana, Hyperliquid, and a dozen emerging high-performance blockchains and Rollups (on-chain scaling solutions).

We know that Ethereum's leading position is genuinely challenged, and it faces an existential threat. We also know it has not yet resolved the issue of value capture.

But I am very skeptical that Wall Street understands these. In fact, I could boldly say that most Wall Street investors know almost nothing about Solana. To be honest, XRP, Litecoin, Chainlink, Cardano, and Dogecoin may have higher recognition in the external market than $SOL. After all, these people have been indifferent to the entire cryptocurrency asset class for several years.

What Wall Street knows is that $ETH is a representation of the 'Lindy Effect' (the idea that things that have existed for a long time are more likely to continue to exist); it has been tested in the field and has long been the primary 'beta investment choice' for $BTC. What Wall Street sees is that $ETH is the only other cryptocurrency asset with a liquid ETF. Wall Street is keen on the upcoming catalysts and classic relative value investing.

Those suited investors may not know much about cryptocurrency, but they know that Coinbase, Kraken, and now Robinhood have all decided to 'build on Ethereum.' With minimal due diligence, they can find that Ethereum has the largest stablecoin pool on its chain. They will start calculating 'moon math' and soon realize that while $BTC has reached an all-time high, $ETH is still over 30% lower than its peak in 2021.

You might think that relatively poor performance looks pessimistic, but these people have different investment approaches. They prefer to buy lower-priced assets with clear targets rather than chase high prices that make them question whether they have 'missed the opportunity.'

I think they are already here. Investment authorization is not an issue; any fund can push cryptocurrency exposure with the right incentives. Although Crypto Twitter (CT) has claimed for more than a year that they won't touch $ETH again, that trading code has performed exceptionally well over the past month.

As of this year, $SOLETH has fallen nearly 9%. Ethereum's market dominance hit a low in May, after which it established the longest upward trend since mid-2023.

If the entire Crypto Twitter (CT) has labeled $ETH as the 'cursed coin,' why does it still perform well?

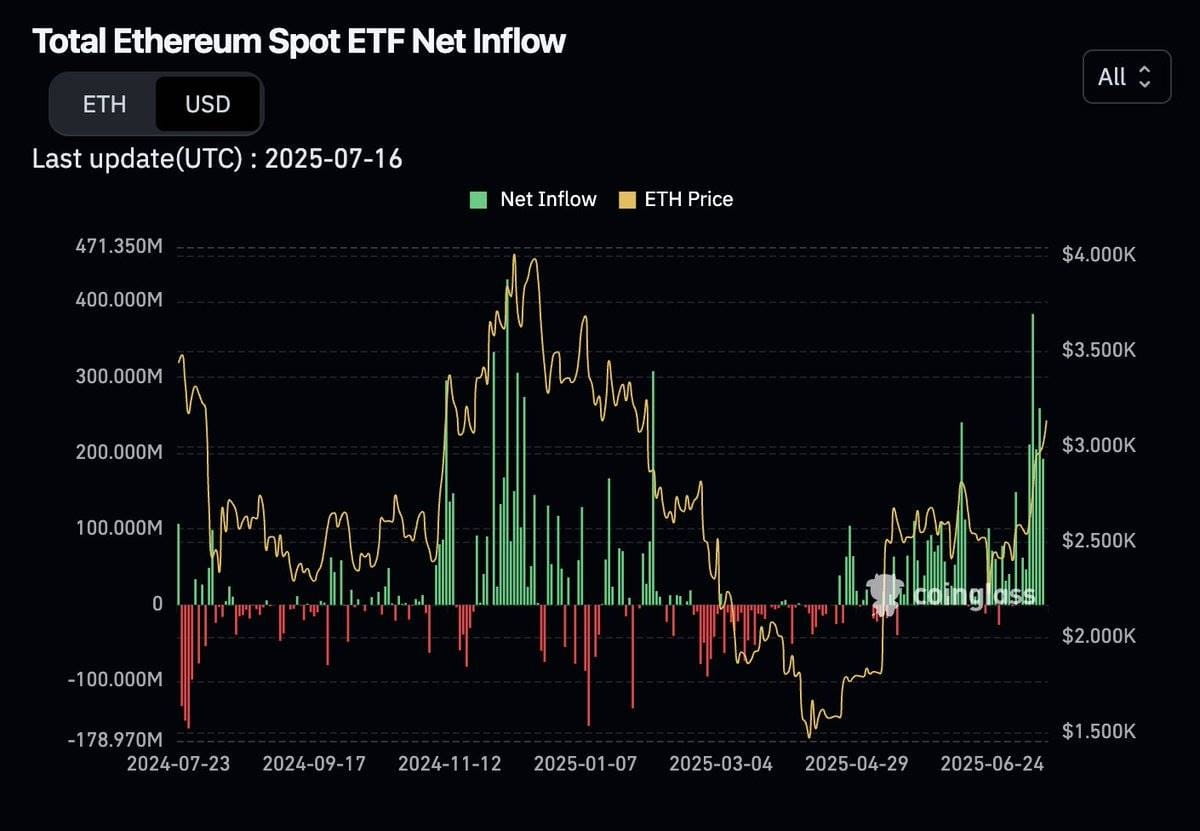

The answer is: it is attracting new buyers.

Since March of this year, spot ETF inflows have shown a one-way growth trend.

Source: Coinglass

Microstrategy clones similar to $ETH are aggressively accumulating, adding early structural leverage to the market.

Perhaps some cryptocurrency natives realized their exposure to $ETH was insufficient and began to rebalance their positions, possibly exiting from $BTC and $SOL, which performed well over the past two years, in favor of Ethereum.

I am not saying Ethereum has solved its existence issues. What I think might happen at this stage is that $ETH as an asset starts to decouple from the Ethereum network itself.

External buyers are driving a paradigm shift in $ETH assets, challenging our inherent perception that it 'can only go down.' Short sellers will eventually be forced to cover. After that, cryptocurrency natives will start chasing the upward momentum until a comprehensive speculative frenzy around $ETH occurs, ending with a spectacular peak.

If all of this really happens, then a new all-time high (ATH) won't be too far away.