Introduction

Recently, financial regulatory authorities across the country have successively issued documents warning the public to be vigilant against illegal financial activities disguised as 'stablecoins.' In fact, the concept of stablecoins has existed for a long time, but it has been largely confined to a small circle. However, after the news that the US is passing the 'Genius Act' and that JD and Alibaba are about to issue stablecoins in Hong Kong, the mainland public has begun to learn about stablecoins and even other virtual currencies, either actively or passively.

Some self-media accounts have begun to transform into web3 'evangelists,' frequently outputting content related to stablecoins and other virtual currencies. In the context of limited traditional investment channels, new phenomena are often the most attractive. However, the so-called cryptocurrency sector is inherently prone to harboring dirt. After being continually cracked down upon since the 'September 4 Announcement' in 2017, funds in the cryptocurrency sector have begun to awaken again. Thus, it is not surprising that financial regulatory authorities have taken notice and remain vigilant.

But if you think about it a little deeper, the mainland regulatory authorities' 'aversion' to virtual currencies is not only because they breed illegal activities; the fundamental reason is that there is no survival soil for virtual currencies in mainland China.

In simple terms, blockchain technology can be developed in mainland China, but virtual currency cannot.

1. What have financial regulatory authorities in various places said?

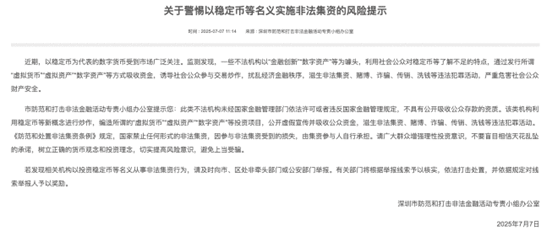

(1) Shenzhen: A risk warning regarding illegal fundraising disguised as stablecoins

The 'Special Task Force Office for Preventing and Cracking Down on Illegal Financial Activities' established by the Shenzhen Financial Committee, Financial Management Bureau, and other departments issued a document on July 7. Interestingly, it pointed out that 'digital currencies represented by stablecoins have attracted widespread market attention.' This statement does not deny the existence of stablecoins; it merely warns that there are some illegal institutions in the market that use 'financial innovation' and 'digital assets' as a gimmick to absorb funds through the issuance of 'virtual currencies,' 'virtual assets,' 'digital assets,' etc., inducing speculation and fostering illegal activities.

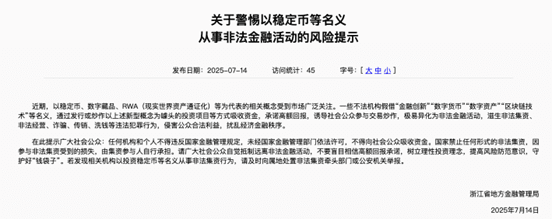

(2) Zhejiang Province: A risk warning regarding illegal financial activities disguised as stablecoins

On July 14, the Zhejiang Provincial Local Financial Management Bureau issued a document also warning the public to be vigilant against illegal financial activities disguised as stablecoins.

However, the warning from Zhejiang Province is clearly different in style from that of Shenzhen: 'Related concepts represented by stablecoins, digital collectibles, RWA, etc. have attracted widespread market attention...' In the eyes of the financial management department of Zhejiang Province, stablecoins, etc., can only be regarded as a concept. The implication is that it does not comply with our country's financial policies.

This is actually closely related to the performance of virtual currencies in mainland China: Shenzhen and Hangzhou are absolutely the two hottest places for web3 entrepreneurship in the country. My personal feeling is that Shenzhen has the best atmosphere, followed by Hangzhou. Of course, the illegal activities related to virtual currencies in these two places are more than in other areas (but not all businesses involving currencies are illegal activities).

(3) Regulations from other places

On July 11, 'Suzhou Finance' (the hosting authority is the Suzhou Municipal Financial Committee) issued a risk warning regarding illegal fundraising under the guise of 'stablecoins'; on July 9, the Beijing Internet Finance Industry Association released the aforementioned notice of the same name, and similar notices or warnings have also been issued in Gansu Province, Chongqing, Ningxia, and other places, targeting illegal fundraising activities under the name of stablecoins.

Does this feel a bit like the atmosphere of the 'September 4 Announcement' in 2017 or the 'September 24 Notice' in 2021?

The policy logic here is actually quite simple. Since September 15, 2021, mainland China has not changed its policy of strict regulation of virtual currencies. Although Bitcoin recently surged to $120,000 each and Ethereum also returned to the peak of $3,000, many speculate that the reasons behind this include the current Chairman of the Federal Reserve Powell's impending departure, as well as the collective learning of cryptocurrencies by the State-owned Assets Supervision and Administration Commission of Shanghai.

But as a web3 lawyer, Lawyer Liu can most acutely feel the attitude of mainland China's judicial authorities and even financial regulatory authorities towards virtual currencies during his practice: if saying 'to eradicate completely' is too severe, at least it is not allowed to flourish. We will analyze the specific reasons below.

2. The competition between the 'blockchain sector' and the 'cryptocurrency sector'

As early as 2013, after the central bank and other departments issued a notice on preventing Bitcoin risks, the crypto field in the mainland has diverged into two paths: the 'blockchain sector' and the 'cryptocurrency sector.'

The blockchain sector focuses on developing blockchain technology, especially consortium chains and public chains. This circle is mainly composed of technical programmers, relatively pure, and has a certain threshold attribute. They do not have much respect for those in the cryptocurrency sector who rely on investment and speculation.

The meaning of the cryptocurrency sector is also easy to understand. Broadly speaking, all businesses related to virtual currencies can be summarized under the umbrella of the 'large cryptocurrency sector': in addition to investing in virtual currencies, it includes issuing virtual currencies, exchanging RMB for virtual currencies, exchanging between virtual currencies, and buying and selling virtual currencies as a central counterparty (most of these businesses can be covered by the functions of cryptocurrency exchanges, so any cryptocurrency exchanges operating in the mainland are strictly prohibited). In addition, quantitative trading, 'haircutting,' etc., are also closely related to virtual currencies and even include people who engage in illegal activities using virtual currencies, who also claim to be part of the cryptocurrency sector. An important feature of the cryptocurrency sector is that you do not need to understand much about networks and computer knowledge to enter; the threshold is relatively low. Of course, many investments and transactions in virtual currencies are essentially derivatives of traditional financial transactions, such as spot trading, perpetual contracts, staking, lending, etc.

On September 15, 2021, mainland China officially announced that cryptocurrency-related businesses are considered illegal financial activities, 'all are strictly prohibited and resolutely cracked down upon.' Since then, the competition between the blockchain sector and the cryptocurrency sector has come to an end: developing blockchain technology in China is completely fine, and many regulators even welcome it; however, activities related to virtual currencies are strictly prohibited. The only small loophole is that the mainland does not explicitly prohibit investment in virtual currencies and their derivatives, but our laws do not recognize their legal validity and do not provide legal protection for investments in virtual currencies. Objectively, regulators have cut off all paths for investing in virtual currencies (for example, prohibiting cryptocurrency exchanges from operating in the mainland, prohibiting banks and third-party financial institutions from providing financial services for virtual currency transactions, etc.).

3. There is currently no survival environment for virtual currencies in China

If everyone understands the strong centralization of social governance in the mainland, it is easy to understand the logic path of 'as long as there is blockchain, there should be no virtual currency.' Although in terms of technical realization, blockchain technology is just one of the conditions for the birth of Bitcoin. For blockchain technology, especially public chains, token incentive strategies are the cornerstone of their survival and development. In simple terms, a blockchain without virtual currency is like an oasis without a water source; it’s difficult to even survive small grasses, let alone grow big trees. But the reality is such that no one can change it. For those truly engaged in web3 construction, if they cannot adapt, they can only develop overseas.