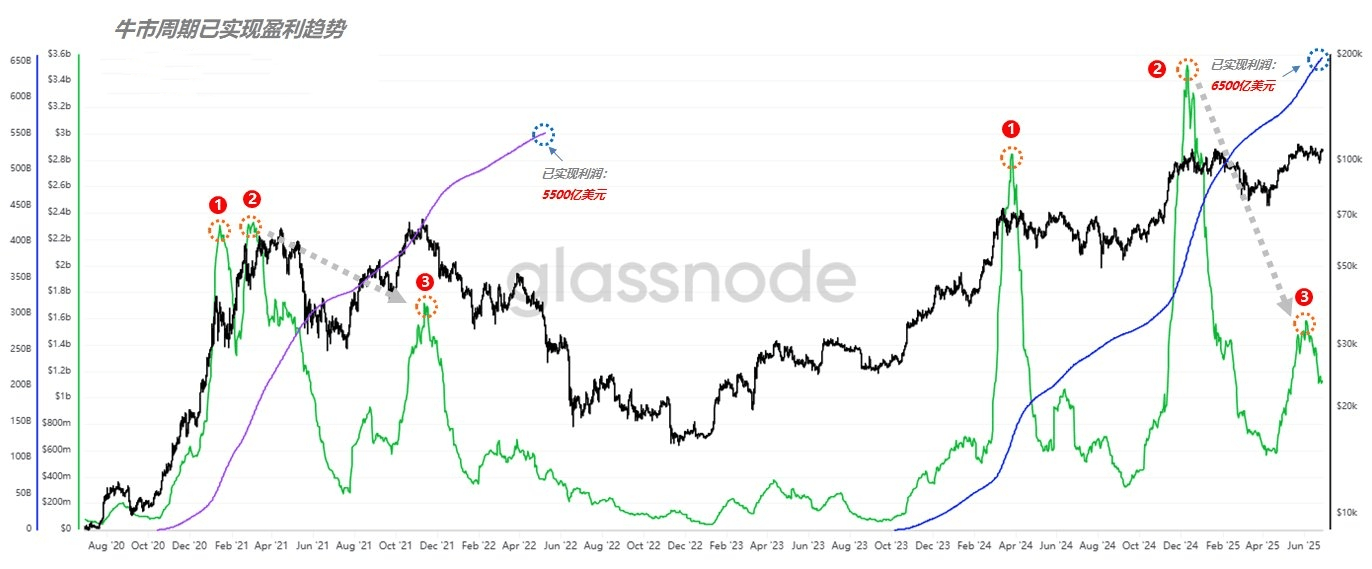

Market profitability has always been the core indicator of the activity level of cryptocurrency players. Comparing Bitcoin's data from the last two cycles, players realized profits of approximately $550 billion during the bull market of 2020-2022, while in this cycle, it has reached $650 billion to date—this leap in capital participation scale indicates that the market ecology has fundamentally changed (see Figure 1).

(Figure 1)

If we observe the cycle pattern using the 30-day moving average of realized profits (30D SMA), the last bull market had three significant profit realization points: January 2021 (Bitcoin around $42,000), March 2021 (around $60,000), and November 2021 (around $68,000). Additionally, the market momentum was strong during the first two price peaks, while the third realization saw a significant decline in profitability, directly leading to a sharp decrease in player participation, marking a critical turning point from bull to bear market.

However, this round is breaking the old logic. The current market has entered a phase similar to the previous round's 'third profit realization period': the first two were in March 2024 (Bitcoin around $70,000) and December 2024 (around $100,000), and the profitability momentum also declined during the third realization. According to the old cycle logic, this seems to be a bear market warning, but the disruptive changes in chip structure are rewriting the market script.

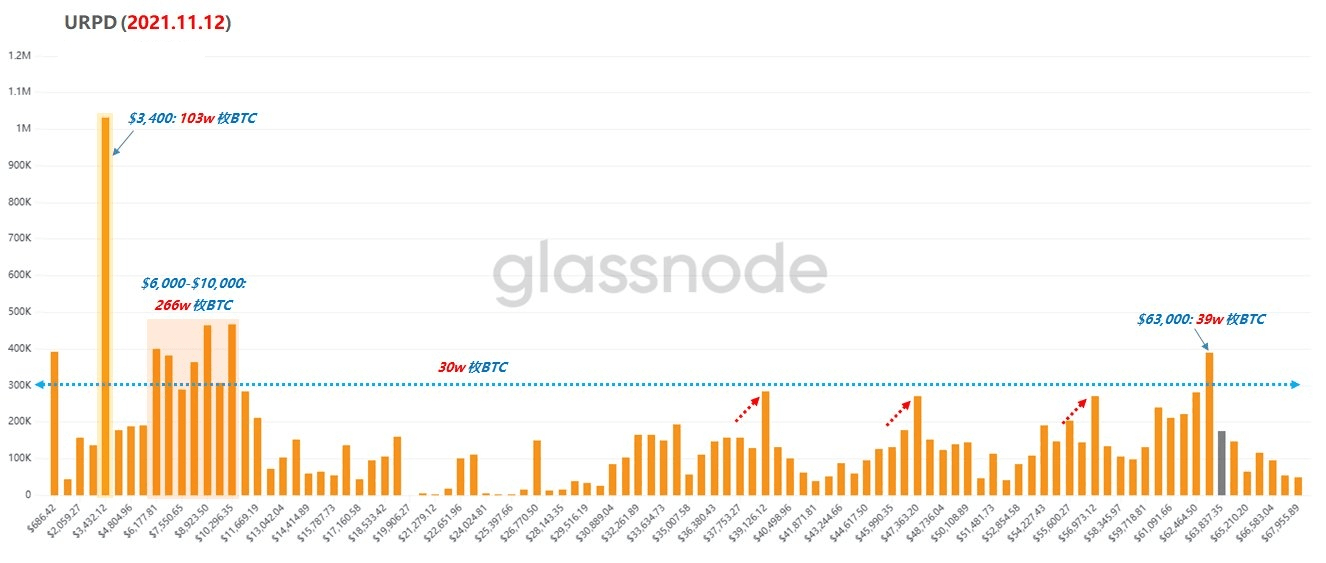

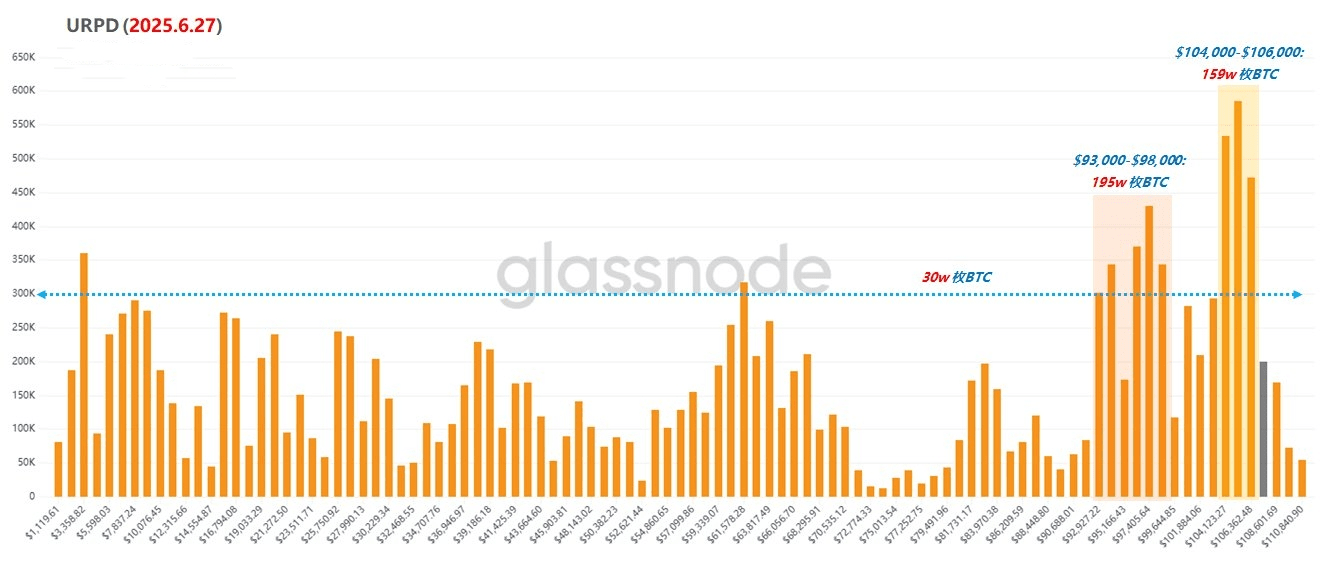

Comparing the Bitcoin holding distribution between November 2021 and June 2025 (see Figures 2 and 3), the difference is obvious:

At the last peak (November 2021), aside from 390,000 Bitcoins at the peak of $63,000, the number of chips in other high-price ranges was below 300,000, with a large number of chips piling up at $3,400 (1.03 million chips) and in the range of $6,000 to $10,000 (2.66 million chips). This means the market lacks absorption capacity, and low-position chips are 'unable to sell,' leading to an excess supply that ultimately triggers a deep pullback.

(Figure 2)

At the peak of this round (June 2025), the number of chips in the price range of $40,000 to $90,000 did not exceed 300,000, while dense holdings formed in the high price ranges of $93,000 - $98,000 (1.95 million chips) and $104,000 - $106,000 (1.59 million chips). Due to a large number of chips traded above $93,000, the overall market cost has risen, and the decline in realized profits at this point is not due to 'unable to sell,' but rather because holders 'do not want to sell'—this is the core logic that indicates the bull market is not over and the pullback is limited.

(Figure 3)

Key point: When the price of Bitcoin breaks through historical highs, if realized profits do not rise and continue to decline, be wary of whether 'not wanting to sell' will turn into 'unable to sell.' However, the current chip structure shows that the resilience of high-position holdings is supporting the market entering a new cycle phase, and the old cycle rule of 'profit realization equals bear market' is no longer applicable.