Against the backdrop of ongoing geopolitical turbulence and increasing macro uncertainty, the sentiment in the Bitcoin options market is subtly shifting. Option traders are becoming more alert to downside risks, and the market pricing structure has also undergone significant adjustments.

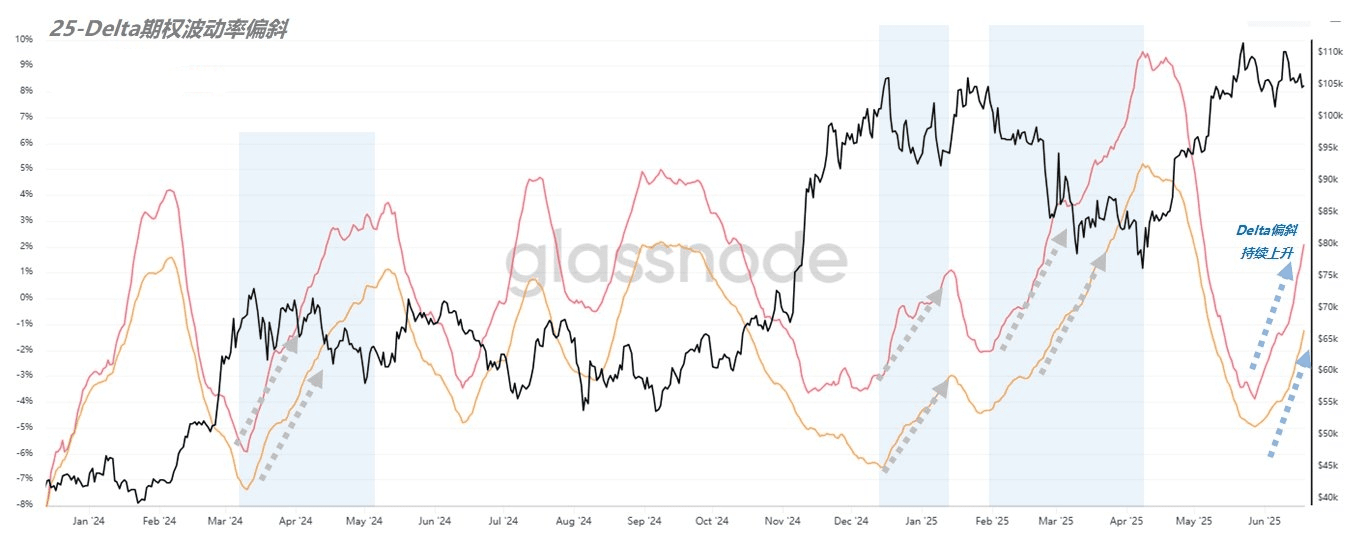

(Figure 1)

First, from the perspective of the 25 Delta implied volatility skew (25D Risk Reversal), this indicator has been continuously rising since May 27. This trend indicates that the implied volatility of put options remains consistently higher than that of call options with the same delta, suggesting that players are willing to pay a higher premium for downside protection. This reflects a growing concern in the market about potential pullbacks.

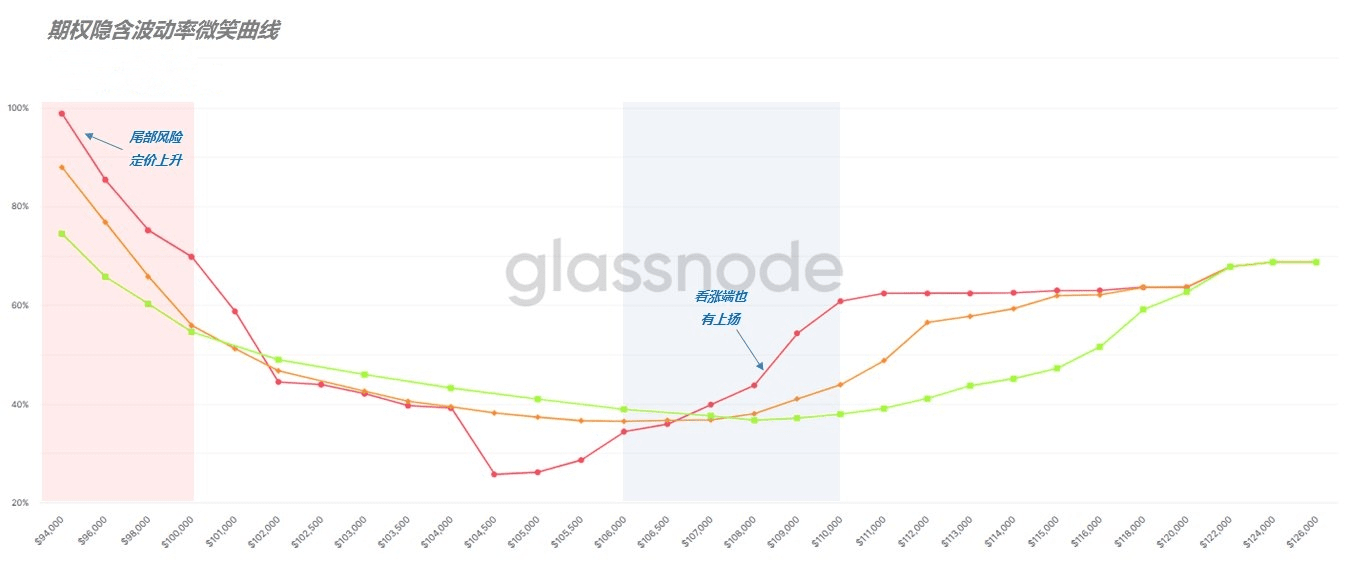

Further observation of the changes in the implied volatility smile curve reveals that the implied volatility of options in the $106,000 to $110,000 range has risen, indicating that some funds still maintain certain expectations for Bitcoin's upside and are engaging in related hedging operations. However, more noteworthy is the more significant rise in the volatility of put options in the $94,000-$100,000 price range, resulting in a steeper overall volatility curve that presents a more pronounced 'smile' shape. This reflects that the market's pricing of tail risks, particularly extreme downside volatility, is continuously increasing.

(Figure 2)

In other words, although some funds still focus on upside opportunities, most traders are positioning themselves in advance for a potential downward trend. This enhanced demand for hedging may stem from expectations regarding macroeconomic data or sudden policy changes.

Overall, the current structure of the Bitcoin options market has significantly tilted towards defensive positioning, with sentiment turning cautious. From hedging behaviors to changes in the volatility curve, everything conveys a key signal: the market is preparing to cope with potential downside risks.#比特币