In the early morning of June 16, Binance officially responded to the severe fluctuations of ZKJ and KOGE, and preliminary investigations indicated that the price turbulence was mainly caused by large holders concentrating their liquidity withdrawals, leading to a chain reaction of liquidations. To prevent similar incidents from happening again and to control the structural risks brought by Alpha incentives, Binance announced that starting from June 17, trading volume between Alpha tokens would no longer be counted as a basis for calculating Alpha Points.

Once regarded as the most popular choice for score manipulation within Binance Alpha, both ZKJ and KOGE collapsed in a flash.

Within Binance Alpha, this token combination was once regarded as the most cost-effective tool for score manipulation, with extremely high LP annual returns and very low slippage experience, quickly becoming the preferred pool for Alpha users. A large influx of funds and a surge in trading activity created an appearance of 'stable growth', which also laid the groundwork for subsequent systemic cascades.

To understand the starting point of all this, we must first return to the incentive mechanism of Binance Alpha itself.

Everything started from Binance Alpha.

Binance Alpha is an incentive mechanism launched by Binance at the end of 2024, where users can earn points by providing LP, participating in trading, and engaging with holdings, which can be used to participate in the platform's regular airdrops and exclusive events.

Due to its clear incentive ratio and distribution rhythm, since its launch, it has gradually become a focus for those looking to profit from the market changes, with volume manipulation and LP assembly becoming the most mainstream scoring methods, indirectly giving rise to token combinations specifically targeting Alpha optimization structures.

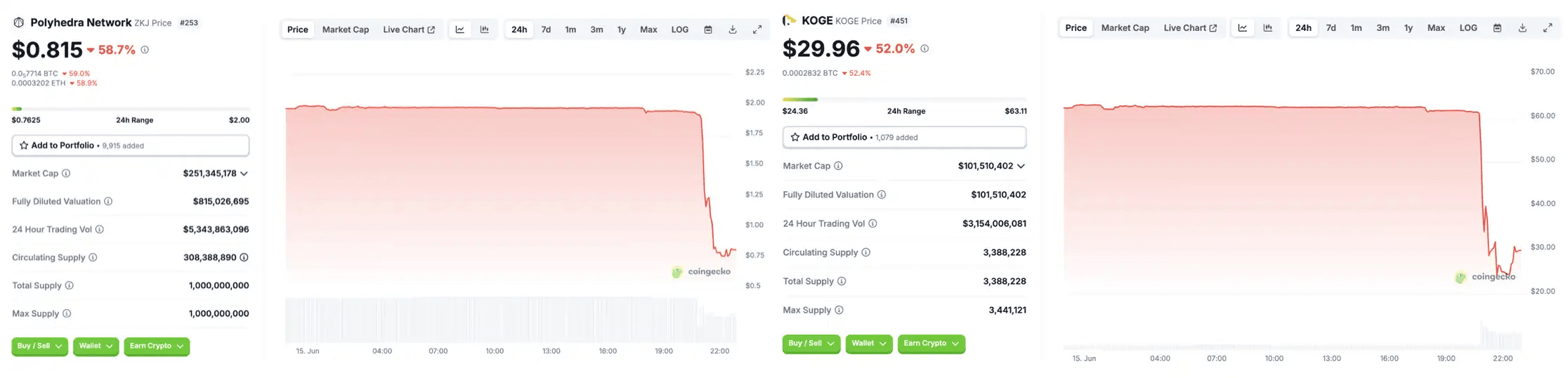

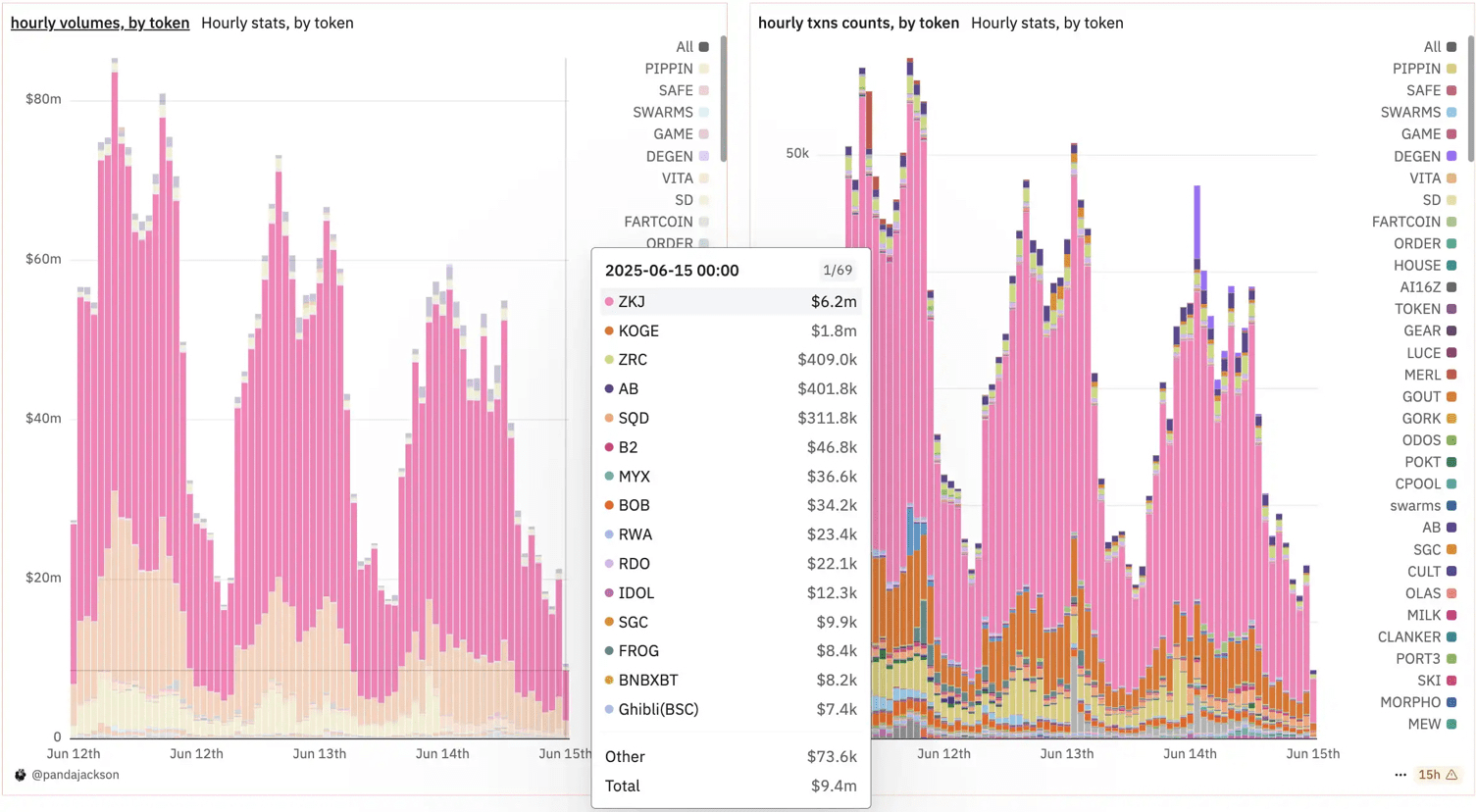

According to the data panel of @pandajackson42, on June 14 alone, the total trading volume of Binance Alpha reached $987 million, with ZKJ and KOGE trading volumes of $703 million and $159 million, respectively, occupying the top two spots on the leaderboard.

However, since June 8, when trading volume peaked at $2.04 billion, Alpha activity has continued to decline, with trading volume on the 14th dropping more than 50% from the peak. On the same day, Binance announced that it would soon adjust its airdrop distribution mechanism, dividing it into 'standard receipt' and 'first come, first served' stages, a change seen by some community members as an indirect catalyst for large holders' early exits and LP withdrawals.

In the Alpha points acquisition mechanism, trading volume and liquidity provision have excessively high weights, leading to the prevalence of the 'market making - volume manipulation - wash trading' trifecta, with the ZKJ and KOGE dual-currency pool being a typical example.

The large holders' conspiracy?

Previously, the project team created a dual-currency trading pair of KOGE/ZKJ and opened permissions to external liquidity studios, guiding large-scale funds to participate in volume manipulation. Meanwhile, KOGE's liquidity in BNB and USDT pools remained relatively shallow, which means that even if large funds wanted to exit, it would be difficult to directly convert KOGE into mainstream assets.

During the period of high APY, large holders of KOGE and ZKJ pushed up pool liquidity by continuously adding LP and encouraged more users to join. Their core logic is that KOGE itself lacks sufficient trading scenarios and external demand and cannot be sold directly. However, ZKJ has a huge open interest in the contract market, providing stronger monetization capabilities. Based on Router's automatic path selection mechanism, constructing a KOGE/ZKJ trading pair can enhance liquidity and lay down paths for subsequent sales.

According to community user Emilia's observations, the KOGE project team has been continuously adding unilateral liquidity, controlling the rise in coin price, which has also resulted in KOGE/USDT liquidity being much smaller than perceived. Once a large holder sells off KOGE, the remaining LP cannot exit through the KOGE/USDT pool and will inevitably have to exchange for ZKJ, further forming a cascade.

Meanwhile, some large holders established short positions for ZKJ on CEX, preparing for subsequent hedging. As market activity slowed down, APY declined, and the volume of funds decreased, large holders began to withdraw from LP one after another, converting their KOGE into ZKJ, and then concentrated on selling ZKJ, completing their capital exit. The spot price quickly fell as a result, and many long positions in ZKJ contracts were liquidated, further amplifying the downward movement.

Price volatility causes more liquidity to withdraw, forming a typical negative feedback loop. Due to the insufficient depth of the KOGE/USDT pool, the exit path for subsequent users can almost only be realized through ZKJ, further crushing the ZKJ price. Throughout this process, the KOGE project team continuously added unilateral liquidity to KOGE, creating a false appearance of price support, but in reality, this compressed the actual realizable space, exacerbating the financial predicament. Once there is concentrated selling pressure in the market, the remaining LP cannot exit smoothly through the original path, and funds can only flow to ZKJ, forming a chain reaction.

Ultimately, this structurally fragile design, combined with LP arbitrage, high leverage contract positions, and high return inducements without actual value inflows, quickly evolved into a typical liquidity crisis, leading to the collapse of both KOGE and ZKJ.

Is the Binance Alpha dividend fading?

This type of liquidity structure driven by short-term incentives can easily evolve into 'targeted harvesting' under extreme conditions. The project's fundamentals have not undergone substantive changes, but due to the end of incentives, structural squeezes, and market exits, external factors can cause prices to plummet, ultimately resulting in losses borne by ordinary users without hedging mechanisms.

Especially since KOGE does not have hedging tools, most participants hold LP or market-making positions without coverage, leading to significant losses. In contrast, some experienced users mainly operate around ZKJ and have configured derivative short positions to avoid some risks.

After the incident, the community reflected on the Binance Alpha incentive mechanism, with many suggestions focusing on weakening the single weight of trading volume and LP, increasing the correlation of points with interaction quality and holding duration, and implementing punitive downgrades for abnormal short-term wash trading and concentrated withdrawals.

For Binance, Alpha remains an important tool for enhancing on-chain activity and guiding quality projects to participate, but its sustainability will depend on better risk control and incentive design.

Looking back, the collapse of ZKJ was not a black swan event, but an inevitable result under the illusion of 'low fees'. Liquidity does not equal legitimacy; narratives can amplify risks, and coordinated exits are never coincidental. In the crypto market, high returns but lacking a value loop structure are scripts pre-set for cascades, and the ZKJ and KOGE events once again confirm this rule.