Recently, the Sa Jie team has continuously received a large number of RWA project inquiries, and the underlying assets are quite varied, including agricultural products, real estate, precious metals, and even some purely conceptual projects that sound quite fantastical...

In fact, the Sa Jie team has previously clarified that under the premise that our country's announcements on 9.4 and notifications on 9.24 remain valid, except for RWA projects strictly reviewed and issued under supervision through the Hong Kong Ensemble sandbox, which possess certain 'criminal risk resistance capabilities,' other types of RWA are very dangerous (especially RWA projects aimed at residents of mainland China).

Therefore, today the Sa Jie team will directly clarify which mainland assets can be used in the Hong Kong sandbox for RWA and which assets cannot be used, so that partners can conduct business more efficiently and save on consultation fees.

01 Basic Understanding: Restrictions and Judgment Standards for Mainland Assets Doing RWA

First, clarify: Assets whose 'physical bodies' are located in mainland China and primarily operated for mainland residents can be RWA. Several successful RWA projects previously can corroborate this point.

However, there are indeed restrictions on assets located in mainland China wishing to issue RWA in Hong Kong. Based on the Sa Jie team's practical experience, the following three types of assets cannot be RWA:

1. Assets that do not comply with the laws and regulations of Hong Kong;

2. Assets that do not comply with the laws and regulations of mainland China;

3. Assets that are currently not suitable for issuance in Hong Kong.

Mainland assets issuing RWA in Hong Kong must comply with the 'dual compliance principle'

In fact, this logic is easy to understand. The assets are located in mainland China, but the tokenized assets (tokenized traditional assets) are actually sold and operated in Hong Kong. The entire financing chain spans both mainland and Hong Kong, naturally requiring compliance with the "dual compliance principle"—the underlying assets must comply in both mainland China and Hong Kong.

1. Hong Kong regulatory aspects

Given that Hong Kong is primarily responsible for the tokenization and financial operation of RWA projects, we need to pay special attention to the requirements of financial regulatory laws and regulations regarding the underlying assets when issuing financial products, such as (Securities and Futures Ordinance), (Banking Ordinance), (Insurance Ordinance), (Anti-Money Laundering and Combating the Financing of Terrorism Ordinance), etc.

The Sa Jie team has previously mentioned that currently in Hong Kong, there are no clear normative legal documents issued regarding the issuance and regulation of RWA, and it is still in the exploratory stage. Therefore, current RWA projects still exist in a 'one project, one discussion' situation during the sandbox regulatory review process. However, the absence of clear normative legal documents does not mean everyone has to feel their way across the river. Understanding Hong Kong's consistent regulatory principles for financial assets and referring to the specific issuance rules of similar financial products can greatly increase the success rate.

In principle, Hong Kong has consistently adopted the 'substantial regulatory principle' (also known as 'perspective regulation') for financial assets, which means that compliance depends on the substance of the asset rather than its appearance. It is not feasible to cover an illegal core with a compliant exterior. In terms of specific regulations, it is necessary to judge based on the regulatory rules applicable to the physical assets corresponding to RWA. For example, if the underlying asset is a bond, the auditing norms applicable to the underlying asset are the (Securities and Futures Ordinance) and related normative documents in Hong Kong.

2. Mainland regulatory aspects

Since the 'physical body' of the tokenized underlying asset is in the mainland, it is crucial to focus on the legality of the underlying assets themselves and the legality of their operational methods, which needs to be viewed from two aspects.

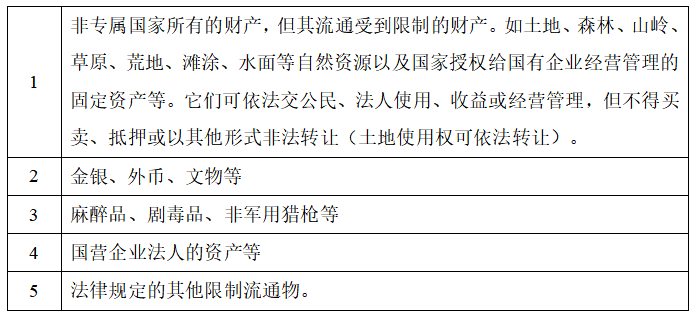

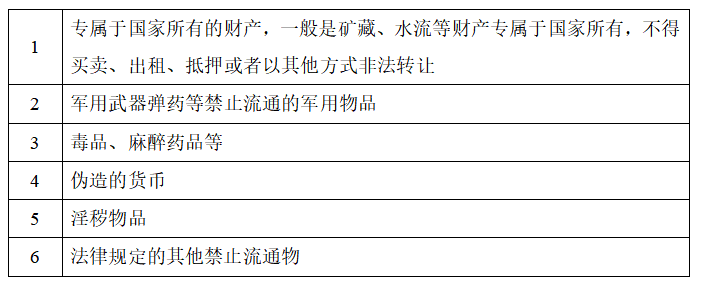

Regarding the legality of the underlying assets themselves, based on our country's (Civil Code) and relevant judicial interpretations and judicial practical experience, objects can be distinguished into three categories based on whether they can circulate and in what scope they can circulate:

Circulating Objects

Restricted Circulating Objects

Prohibited Circulating Objects

Circulating objects refer to objects that are legally allowed to circulate freely between civil entities; restricted circulating objects refer to objects that have certain restrictions on their circulation scope and extent; prohibited circulating objects refer to objects that are explicitly prohibited by law from circulating and transferring. In the opinion of the Sa Jie team, objects used for RWA should be 'circulating objects' or 'restricted circulating objects' with permission.

In practice, 'restricted circulating objects' generally include:

'Prohibited circulating objects' generally include:

In terms of the legality of operational methods, Hong Kong requires cash flow for the underlying assets of RWA projects (currently issued projects are all commercial projects with practical application scenarios). Therefore, the underlying assets must also comply with the laws of our country at the operational level: avoid red lines and obtain the necessary administrative permits for operation.

Assets that are currently not suitable for issuance in Hong Kong

This type of asset itself has already met the requirements of the 'dual compliance principle,' but it is currently not suitable for issuance in Hong Kong.

On the one hand, RWA in Hong Kong is still in the sandbox experimental stage, so the selection of underlying assets is cautious. The clearly recommended types of underlying assets are those with 'high-tech' and 'clean and green' attributes. Therefore, the Sa Jie team believes that at this stage, if one wants to issue RWA projects in Hong Kong, the underlying assets must at least meet one of the above two criteria, such as carbon emission rights and other property rights closely related to the green economy, even if they do not have a physical entity.

On the other hand, some assets that are intended to be activated through RWA but cannot generate good cash flow are also not suitable for RWA in the Hong Kong sandbox due to low probability. For example, some real estate with low economic value cannot change the reality of its market value gradually decreasing, no matter how much it is 'empowered' through emerging concepts. The possibility of issuing RWA for such assets is very low.

02 These specific mainland assets can hardly be RWA...

After partners understand the principles and standards for judging whether the underlying assets can issue RWA, we will focus on some recent inquiries or assets that need to be discussed separately to save everyone on consultation fees.

Jewelry and Cultural Collectibles RWA

Jewelry and cultural collectibles RWA is a category with a high volume of inquiries. It is also one of the most challenging categories to provide clear legal opinions on, mainly due to the variety and depth of jewelry and collectibles, with various special restrictions scattered across laws, judicial interpretations, administrative regulations, departmental rules, and national standards. For uncommon categories, significant legal verification work is generally required to provide opinions. Overall, at this stage, it is not recommended to use jewelry and collectibles as underlying assets for RWA.

If partners' assets fall into the following situations, they can be vetoed:

1. Gem products with gambling characteristics. Simply put, these are products whose quality cannot be judged by their appearance and must be cut to know the internal quality of the raw materials, such as jade raw stones, unpeeled green pine raw stones, unpeeled pearls, etc.;

2. Processed jewelry and jade, such as B-grade jade, C-grade jade, etc.;

3. National prohibition on the sale of biological products (organic gemstones), such as ivory, helmeted hornbill products, conch, queen conch, coral, rhino horn, tortoiseshell, copal resin, sea柳, amber pillows, amber powder, cinnabar, etc.;

4. Low-quality or processed jade or jade imitations, such as sodium feldspar jade, Guatemalan jade, heat-treated jade, etc.;

5. Pure gold, pure silver, and other precious metals that are specifically restricted or prohibited by national laws.

Intellectual Property RWA

Intellectual property, such as copyrights, trademarks, patents, etc., have actually seen many projects emerge in the overseas crypto asset sphere, and there are even several film and television projects that have realized short and quick financing through tokenization. Currently, we have not seen successful cases regarding RWA projects in Hong Kong, but the Sa Jie team believes that intellectual property is not an unexploitable underlying asset for RWA. Specific projects need specific analysis; if the intellectual achievement has significant commercial value, after clear regulatory norms, bold attempts to 'break through' can be made.

Agricultural and Agricultural Product RWA

'Can the sunny green grapes do RWA?' Not long ago, a partner consulted the Sa Jie team with promotional materials for a similar grape project in China. We do not comment on specific projects; we only abstractly consider agricultural and agricultural product RWA projects. If the project meets the ethical review standards of science and technology, has high technological content and research value, and has good commercial value, it can also be boldly attempted to 'break through' after regulatory norms are clarified.

Pure Concept RWA

Partners must understand one point: RWA is not crowdfunding. For such projects, the Sa Jie team generally directly gives a veto opinion.

03 Final Thoughts

To extend a point: For underlying assets that are neither in the mainland nor in Hong Kong, can they do RWA in Hong Kong? The Sa Jie team believes that there are currently no regulations stating that assets must be in certain locations to apply for Hong Kong RWA. From the perspective of Hong Kong's positioning as an 'international financial center,' the location of the underlying assets should not hinder RWA. Authenticity, credibility, compliance, and investment value are the hard indicators.