————————————————————

The traditional "real return" model, such as dividend or commission sharing, looks attractive, but in fact it may become a "cash machine" for foundations or big investors.

These insiders do not want to sell their core tokens directly (because on-chain operations will scare away the market), so they convert ETH or USDC into real money through dividends.

What about the community? It is almost impossible to see the money being reinvested in the project, and small retail investors are completely unable to compete with large investors in this "blood-sucking" ability. The seemingly harmless dividend model may actually be an invisible blood-sucking worm, allowing large investors to quietly squeeze the protocol income without having to bear much responsibility or public supervision.

1) Buyback and destruction = democratic dividends for small retail investors🔻

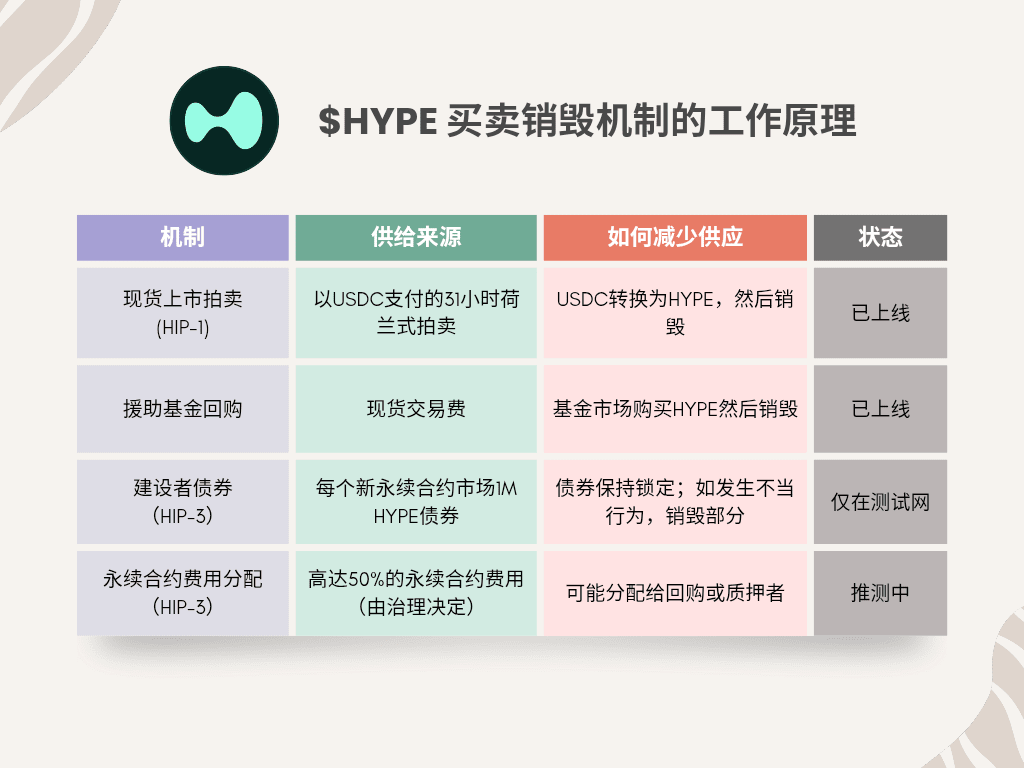

Hyperliquid completely subverted this logic and launched the "buyback and destroy" model. The protocol does not pay out the handling fees as dividends, but uses the income to buy back $HYPE tokens on the open market and then destroy them permanently.

This move is undoubtedly a big boon for small retail investors, because every time Hyperliquid buys back and destroys $HYPE, the circulating supply of tokens decreases, and the market tends to be scarce and expensive, which pushes up the price of tokens. Both large and small retail investors can sell at any time to make money, especially small retail investors can seize opportunities more flexibly.

On the other hand, it is not so easy for the foundation to sell off. Large-scale selling orders are clearly visible on the chain, which will immediately make investors lose confidence and damage the reputation of the project. Some people question that the protocol may raise the price by buying back and then take the opportunity to sell off to pit retail investors, but for a team that works hard, this is not cost-effective at all: buying back and then selling will destroy trust, and even the value of its own tokens will collapse. Even the Ethereum Foundation's selling of ETH has caused a community backlash, and Hyperliquid's operation is even more unacceptable.

More importantly, selling will destroy the buyback and destruction mechanism, which is the core pillar of $HYPE’s value. Every time it buys back, the protocol is saying to the market: “We are confident in our project and are willing to take over at any time!

"This will not only boost investor confidence, but also trigger a market follow-up effect and drive long-term value growth.

In summary, although the foundation can also profit from the rise in $HYPE prices, small retail investors can earn more relatively. This is because they have no liquidity restrictions when selling, and they don’t have to worry about being accused of “cutting leeks” like big investors. Compared with the dividend model (big investors eat meat and small investors drink soup), buyback and destruction make the distribution of income more fair.

2) Recycle, not leak 🔻

The value of a token depends on supply and demand and expectations of future value. Although dividend-based tokens can attract "yield hunters", they are like a leaky bucket. The value generated by the protocol does not remain in the ecosystem, but flows to the outside. Dividend ETH or USDC is often directly cashed out by large investors, weakening the growth momentum of the project.

Hyperliquid currently has 422.6 million $HYPE staked, of which the foundation has staked 272.7 million (about 64%). If the dividend model is used, the foundation can theoretically get 14 million $HYPE (about 352 million US dollars, as of May 9, 2025). Although some dividends may be publicly reinvested, no one can guarantee that the money will not be quietly cashed out. Retail investors and the community have no idea where the funds have gone.

In contrast, buybacks and burns are like "recycling" revenue directly into tokens. Each buyback reduces the supply, which is equivalent to each holder's token share becoming larger. This triggers a positive feedback loop: investors expect the supply to continue to decrease, so they are even more reluctant to sell, and the price naturally rises.

The transaction and listing fees on Hyperliquid will eventually be used to destroy $HYPE. The higher the transaction volume, the more scarce the token. The dividend model is completely incomparable because it relies on the holders to use the dividends to buy back the tokens, which is inefficient and unstable. Hyperliquid's automatic destruction mechanism is direct and continuous, clearly converting the activity of the protocol into token scarcity.

3) Hyperliquid’s community-first principle 🔻

Hyperliquid chose to buy back and burn instead of dividends, reflecting its "community first" philosophy. When the project was launched, there was no VC share, but 310 million $HYPE (worth about $1.6 billion when listed) was directly airdropped to more than 90,000 users. This wide distribution of tokens avoided insider selling, cultivated a group of die-hard users, and provided sufficient liquidity to the ecosystem from day one.

More than 70% of $HYPE is left to the community through continuous airdrops and incentives, and the foundation has pledged a large number of tokens to protect network security. Hyperliquid explicitly avoids the "blood-sucking" model, ensuring that protocol revenue flows back into the tokens, allowing all participants to benefit from the increase in $HYPE prices. In particular, retail investors can more freely seize the rising opportunities brought by buybacks.

4) Looking to the future 🔻

After the "real income" craze in 2022, 2024-2025 proved the power of "the protocol itself is the best buyer". Projects like dYdX also began to join the buyback plan to keep more income in the token. The market evidence is becoming more and more clear: by buying back the tokens that capture income, people can believe that this is not a "virtual coin".

Hyperliquid has embraced this principle from the beginning. Using transaction fees to destroy tokens not only avoids large investors cashing out, but also circumvents the legal troubles that may arise from dividends. Every time the protocol earns transaction fees, holders can see a real financial impact.

However, not every token buyback is successful. Some projects have buyback mechanisms, but the value of their tokens still collapses due to lack of real demand, insufficient revenue sources, or weak community foundation. Buyback and destruction is not a panacea. It requires the project itself to have real use cases, stable revenue, strong product-market fit (PMF), and a user base that believes in the long-term value of the project.

From this perspective, buyback and destruction are a carefully designed core mechanism for token value. Foundations and large holders can only make money if all holders make money. Traders enjoy a CEX-like experience, knowing that their fees are feeding a persistent destruction cycle instead of going into the pockets of insiders. The end result is: a passionate user base, self-reinforcing growth, and a framework that rewards real activity.

In general, Hyperliquid's "buyback and burn" model is like a fair wealth distributor, which directly converts the success of the protocol into the income of each holder. Compared with the "big player feast" of traditional dividends, it allows small retail investors to eat meat, while motivating projects and communities to run towards long-term prosperity together.

In the long run, buyback and destruction may drive Web3's transformation towards a "sustainable economy", reduce dependence on external financing, and truly realize the vision of "the protocol is the company".