Original article title: Convergence and Divergence: US, China, CeDeFi Original author: @0xtony0x Original translation: zhouzhou, BlockBeats

Editor’s note: This article explores the changes in the global financial system, particularly the integration of cryptocurrencies with traditional financial systems. As geopolitical tensions rise and the dollar's dominance wanes, blockchain technology is becoming a neutral financial infrastructure, promoting the development of crypto assets, stablecoins, and tokenized RWAs. Through the integration of CeFi, DeFi, and TradFi, capital flows and interest rate markets are gradually converging, attracting more institutions into the blockchain world.

The following is the original content (reorganized for readability):

U.S.-China Discrepancies and Dollarization

Recently, the extreme fluctuations in the foreign exchange market have underscored the intensifying global macroeconomic tensions and the significant changes occurring in the financial landscape. The dollar surged against the yen (USD/JPY) to the 145 level, primarily driven by the Bank of Japan's continued dovish stance—maintaining interest rates unchanged and not signaling any rate hikes—coupled with a rapid unwinding of previously bullish positions on the yen. The interest rate differential between the U.S. and Japan remains substantial, making the dollar more attractive as the Federal Reserve maintains relatively high interest rates while Japan continues its loose monetary policy.

Meanwhile, the New Taiwan Dollar (TWD) surged over 8% against the U.S. dollar in two days, an extremely rare '19 sigma' event. This sudden movement stemmed from local Taiwanese institutions rapidly adjusting positions and reducing exposure to the dollar, highlighting increasing market concerns over geopolitical risks and vividly reflecting the direct impact of escalating U.S.-China tensions on the global forex market.

TSD/USD price chart

Earlier this month, geopolitical tensions between the U.S. and China escalated sharply. President Trump raised tariffs on Chinese imports to an unprecedented 145%, and China quickly retaliated with a 125% tariff on U.S. products, further deepening the economic rift between the two sides. This escalation echoes the classic 'Thucydides Trap' theory, which posits that conflict is often unavoidable when a rising power challenges an existing hegemon.

But this time, it's not just about trade barriers; it represents a systemic decoupling between the two major economies, with the resulting 'second-order effects' creating a chain reaction in global liquidity and the dollar's dominance.

For a long time, the dollar’s dominance in global trade and finance has relied on deep trust in the American system—this trust is based on political stability, predictability of foreign policy, and openness of capital flows. As noted by Bipan Rai, managing director at BMO Global Asset Management: 'There are clear signs that this trust is eroding... global asset allocation trends are gradually shifting away from the dollar.'

In fact, the foundation of dollar hegemony is quietly eroding due to geopolitical turmoil and the increasingly unpredictable U.S. diplomatic and economic policies. Notably, despite President Trump's stern warnings to other countries against abandoning dollar-denominated trade or facing economic penalties, the dollar experienced significant volatility during his term—experiencing its most severe depreciation since the Nixon era in the first 100 days of his administration. This symbolic moment highlights a broader, accelerating trend: multiple countries worldwide are actively exploring alternative paths to de-dollarization, marking a gradual shift away from dollar dependence in the global financial system.

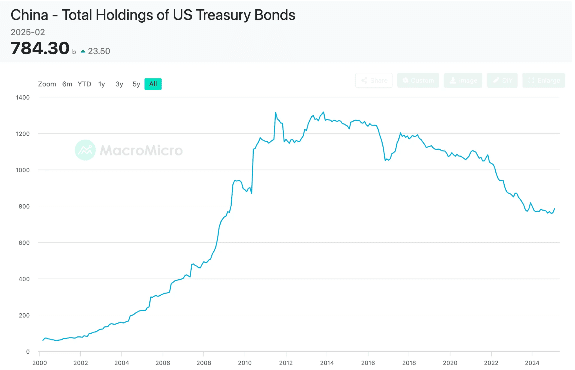

For decades, the surplus dollars from China's trade have continually flowed back into U.S. Treasuries and financial markets, sustaining dollar hegemony since the collapse of the Bretton Woods system. However, with the sharp deterioration of strategic trust between the U.S. and China in recent years, this long-standing capital cycle is facing unprecedented disruption. As one of the largest overseas holders of U.S. assets, China has significantly reduced its exposure to U.S. Treasuries, with its holdings falling to approximately $760.8 billion by early 2025, a nearly 40% decline from the peak level in 2013.

This shift reflects China's broader strategic response to the growing risk of U.S. economic sanctions—after all, the U.S. has frozen foreign assets multiple times in the past, with the most notable example being the freezing of approximately $350 billion in Russian central bank reserves in 2022.

As a result, Chinese policymakers and influential economists are increasingly advocating for the diversification of China's foreign exchange reserves, gradually reducing dependence on dollar assets, fearing that these assets are evolving into potential geopolitical liabilities. This strategic adjustment includes the addition of approximately 144 tons of gold reserves in 2023, as well as promoting the internationalization of the RMB and exploring digital currency alternatives.

This systemic 'de-dollarization' is tightening global dollar liquidity, raising international financing costs, and posing severe challenges to markets that have long relied on China to recycle its surplus dollars back into Western financial systems.

Additionally, China is actively advocating for the establishment of a multipolar financial order, encouraging developing countries to use local currencies or the yuan more for trade settlements, rather than relying on the dollar. The core of this strategy is the Cross-Border Interbank Payment System (CIPS), which is explicitly designed as a comprehensive alternative to the existing SWIFT and CHIPS systems globally, covering both information transmission (SWIFT functions) and settlement (CHIPS functions).

Since its launch in 2015, CIPS has aimed to simplify international transactions denominated in yuan, thereby reducing global reliance on dollar-dominated financial infrastructure. Its increasingly widespread acceptance signifies a systematic shift in the global financial system towards multipolarity: by the end of 2024, CIPS had 170 direct member institutions from 119 countries and regions and 1497 indirect members.

This stable growth peaked on April 16, 2025—according to unverified reports, CIPS's daily trading volume exceeded SWIFT for the first time that day, processing a record 12.8 trillion yuan (approximately 1.76 trillion USD). Although this milestone has yet to receive official confirmation, it still highlights the transformative potential of Chinese financial infrastructure in reshaping the global monetary landscape—from a dollar-centric system to a decentralized, multipolar system centered around the yuan.

As London School of Economics economist Keyu Jin remarked at a forum held by the Milken Institute: 'In the past decade, trade denominated in yuan has grown from 0% to 30%, and now half of China's capital flows are settled in yuan, a proportion far higher than in the past.'

Liquidity must flow: The integration of CeDeFi.

However, as geopolitical boundaries become increasingly rigid and traditional financial channels narrow, a parallel phenomenon is quietly occurring: global liquidity is gradually converging into a borderless decentralized financial network. The liquidity integration among CeFi (centralized finance), DeFi (decentralized finance), and TradFi (traditional finance) marks a reconstruction of capital flow patterns and is pushing blockchain-based networks towards a new core financial infrastructure status in reshaping the global economy.

Specifically, the trend of CeDeFi (the fusion of centralized and decentralized finance) is being driven by various 'gravitational' forces:

·Stablecoins as payment means bring B2B and B2C liquidity on-chain.

·CeFi institutions simultaneously provide both crypto and traditional financial products.

·DeFi protocols bridge on-chain and off-chain yields, creating new interest rate arbitrage paths.

Stablecoins as payment infrastructure

Payments have long been the 'Holy Grail' of the crypto space. Tether, as the de facto shadow bank of offshore dollars, has become the most profitable financial institution when calculated by average profit per employee. Recent geopolitical turmoil will only further drive demand for stablecoins, as global capital increasingly seeks dollar exposure through a non-censorable, borderless platform.

Whether it's Argentine savers using USDC to combat inflation or Chinese merchants settling trade with Tether while bypassing the banking system, the underlying motivation is the same: to obtain reliable value without relying on traditional financial systems.

In an era of heightened geopolitical tensions and financial uncertainty, the demand for 'trading autonomy' is highly appealing. In 2024, the trading volume of stablecoins surpassed that of Visa. Ultimately, digital dollars (stablecoins) operating on crypto networks are rebuilding the offshore dollar system of the 20th century—providing dollar liquidity to markets concerned about U.S. hegemony without relying on the U.S. banking system.

CeFi institutions simultaneously provide traditional finance and crypto products.

In addition to allowing global liquidity to continue being settled in dollars, we also see CeFi platforms vertically expanding into the crypto space, and vice versa:

·Kraken acquired Ninja Trading to expand its traditional financial asset product line, ultimately achieving cross-product margin trading between traditional finance and crypto trading.

·In China, major brokers like Tiger Brokers and Futu (often referred to as the 'Chinese Robinhood') have begun accepting cryptocurrencies such as USDT, ETH, and BTC as deposit methods.

·Robinhood has made its crypto business a core growth focus, planning to launch products such as tokenized stocks and stablecoins.

With the regulatory clarity brought about by new market structure legislation, the horizontal integration between traditional finance and crypto products will only become more important.

DeFi protocols bridging crypto and traditional financial yields

Meanwhile, we also see DeFi protocols leveraging high crypto-native yields to attract traditional finance or off-chain funds, enabling TradFi institutions to access global on-chain liquidity for executing their off-chain strategies.

For example, our invested projects BounceBit (@bounce_bit) and Ethena (@ethena_labs) offer 'basis trading yields' to traditional financial institutions. Due to the programmability of on-chain dollars, they are able to package these basis trading products into on-chain 'synthetic dollars', directly targeting the $13 trillion fixed-income market. Such products are particularly attractive to traditional financial institutions, as basis yields are negatively correlated with treasury yields. Thus, they effectively open new paths for interest rate arbitrage, further driving the capital flows and interest rate market integration among CeFi, DeFi, and TradFi.

Furthermore, Cap Lab (@capmoney_) allows TradFi institutions to borrow from on-chain liquidity pools to execute off-chain trading strategies, thereby providing retail investors with unprecedented high-frequency trading (HFT) yield channels. It also effectively extends EigenLayer's economic security scope from on-chain activities to off-chain yield generation strategies.

These developments collectively drive liquidity convergence, narrowing the gap between on-chain yields, off-chain yields, and traditional risk-free rates. Ultimately, these innovative solutions become powerful arbitrage tools, aligning capital flows and interest rate dynamics across DeFi, CeFi, and TradFi sectors.

CeDeFi liquidity convergence —> CeDeFi product offerings

The convergence of liquidity between CeFi, DeFi, and TradFi into blockchain networks signifies a fundamental change in the role of on-chain asset allocators—from primarily crypto-native traders to a growing number of complex institutions seeking diversified investments beyond crypto-native assets and yields.

The downstream effect of this trend is the expansion of the on-chain financial product suite, particularly with the introduction of more RWA products. As more RWA products enter the on-chain space, it will attract even more institutions from around the world to join the on-chain market, creating a self-reinforcing cycle that ultimately brings all financial participants and assets onto a unified global ledger.

Historically, the trajectory of cryptocurrencies has gradually incorporated higher quality real-world assets, evolving from stablecoins and tokenized treasury bonds (such as Franklin Templeton's Benji and Blackstone's BUIDL) to increasingly complex financial instruments, such as Apollo's recent tokenized private credit funds, with potential further expansion into tokenized equities.

The decline in interest from marginal buyers in speculative crypto-native assets highlights a significant market gap and presents opportunities for institutional-grade tokenized RWA. Against the backdrop of escalating global geopolitical uncertainty—such as the economic decoupling tensions between the U.S. and China—blockchain technology is gradually becoming a credible neutral financial infrastructure.

Ultimately, all financial activities will converge onto this verifiable and borderless global financial ledger, fundamentally reshaping the global economic landscape—from trading crypto-native altcoins to payments, tokenized treasury bonds, and equities.

‘Original link’