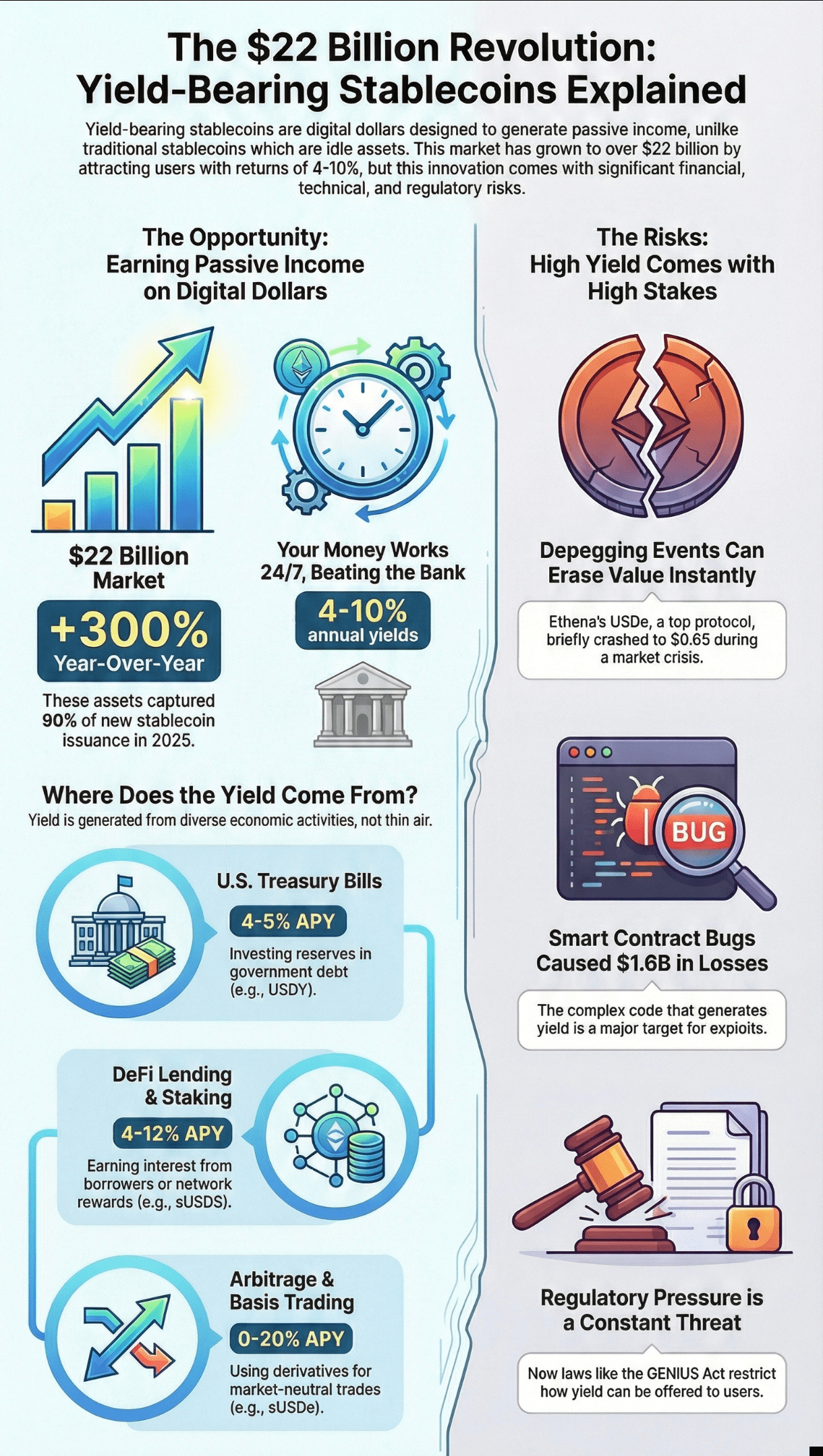

$22 billion. That's how much money is now parked in yield-bearing stablecoins as of November 2025, up 300% year-over-year. To put this in perspective, that's like every person in Florida suddenly deciding to stuff their mattresses with crypto that pays them to sleep on it.

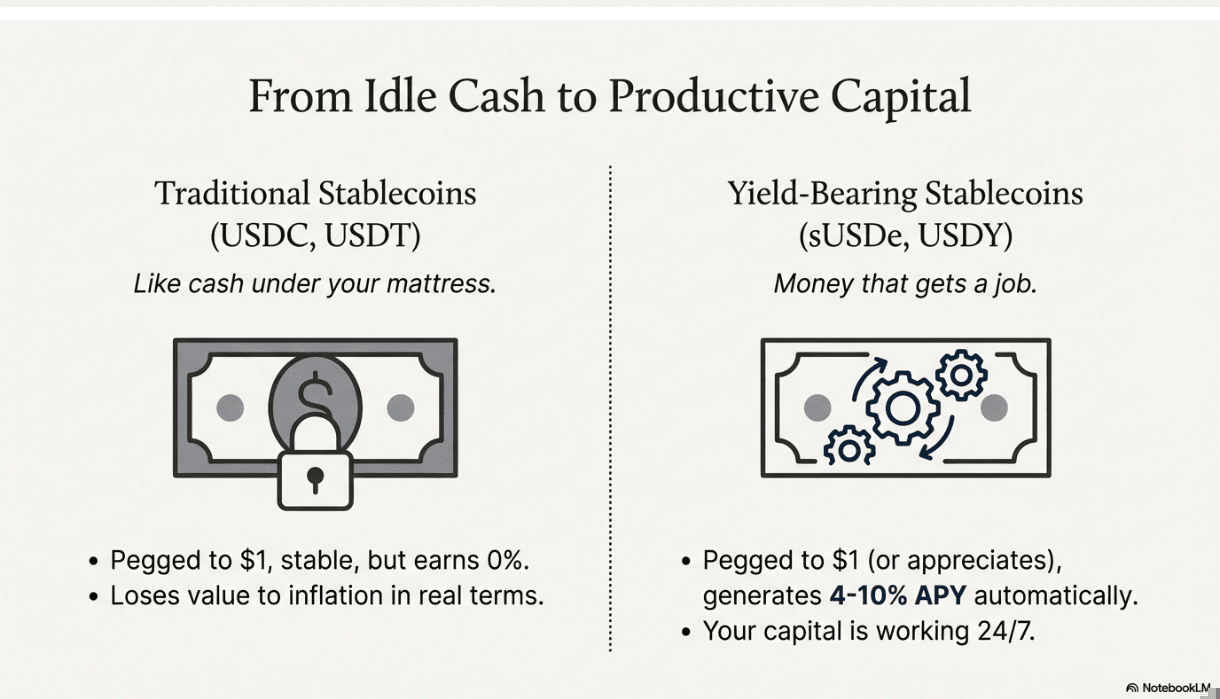

While traditional stablecoins like USDT and USDC just sit there doing nothing,like cash under your mattress,yield-bearing stablecoins are working 24/7, generating returns that make your bank's 0.01% savings account look like a bad joke. We're talking about 4-10% annual yields on dollar-pegged assets, in an economy where finding decent returns feels impossible.

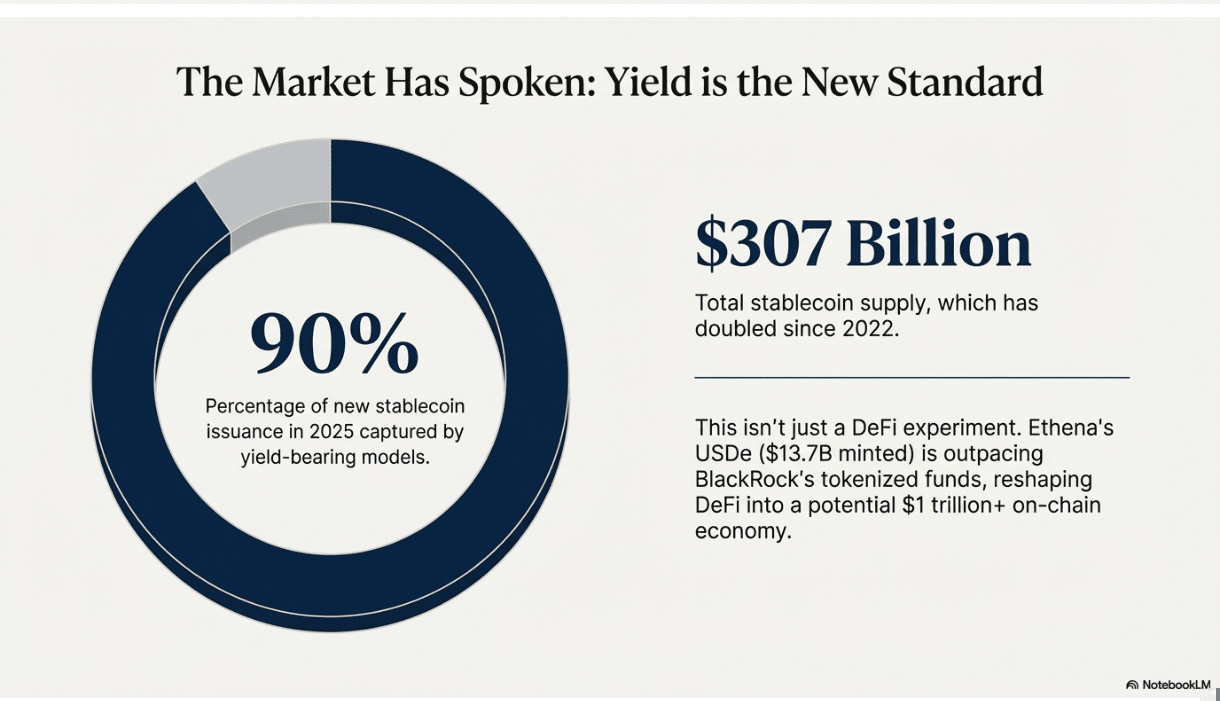

The numbers are honestly pretty wild when you think about it. Total stablecoin supply hit $307 billion in 2025, doubling since 2022, with yield-bearing models capturing 90% of new issuance. That means nearly every new stablecoin dollar minted this year is earning someone money just for existing.

But here's the thing that really gets me,this isn't just some DeFi experiment anymore. BlackRock's tokenized funds are getting outpaced by protocols like Ethena's USDe, which minted $13.7 billion in supply by becoming the backbone of modern arbitrage trading. Ethereum liquid staking tokens alone added $34 billion in value this year.

The regulatory landscape shifted dramatically too. The U.S. GENIUS Act passed in July, creating a framework that's actually letting institutions dive in without breaking compliance rules. This isn't hype,it's infrastructure reshaping DeFi into what's looking like a $1 trillion+ on-chain economy.

Yeah, there are risks. USDe depegged to $0.65 in October during a massive liquidation event. Stream Finance collapsed with $93 million in losses. But the resilience has been surprising,most of these assets recovered quickly, and the yield mechanisms kept working even under stress.

What we're seeing is the closing of what analysts call the "yield gap",where crypto's productive assets historically lagged traditional finance's 55-65% yield dominance by a factor of 5-6x. That gap? It's shrinking fast.

❍ What Are Yield Bearing Stablecoins?

Look, if you've been in crypto for more than five minutes, you know what stablecoins are. USDC, USDT, DAI,digital dollars that (usually) hold their $1 peg. But yield-bearing stablecoins? They're basically stablecoins that decided to get a job.

Think of regular stablecoins as your checking account,stable, boring, earning nothing. Yield-bearing stablecoins are like having that same stability but with your money automatically investing itself while you sleep. They maintain their dollar peg (well, most of the time) while generating passive income for holders.

The magic happens because these aren't just sitting in bank vaults collecting dust. The protocols behind them deploy reserves into productive strategies,lending pools, U.S. Treasuries, arbitrage trades, even staking rewards. Then they pass those returns back to holders, either by increasing your token balance (rebasing) or by letting the token price slowly drift above $1 as yields accumulate.

Here's where it gets interesting though. These aren't like traditional finance yield products where you lock up money for months. Most yield-bearing stablecoins are composable,you can use them as collateral, trade them, provide liquidity, or loop them for leveraged yields. Try doing that with a CD.

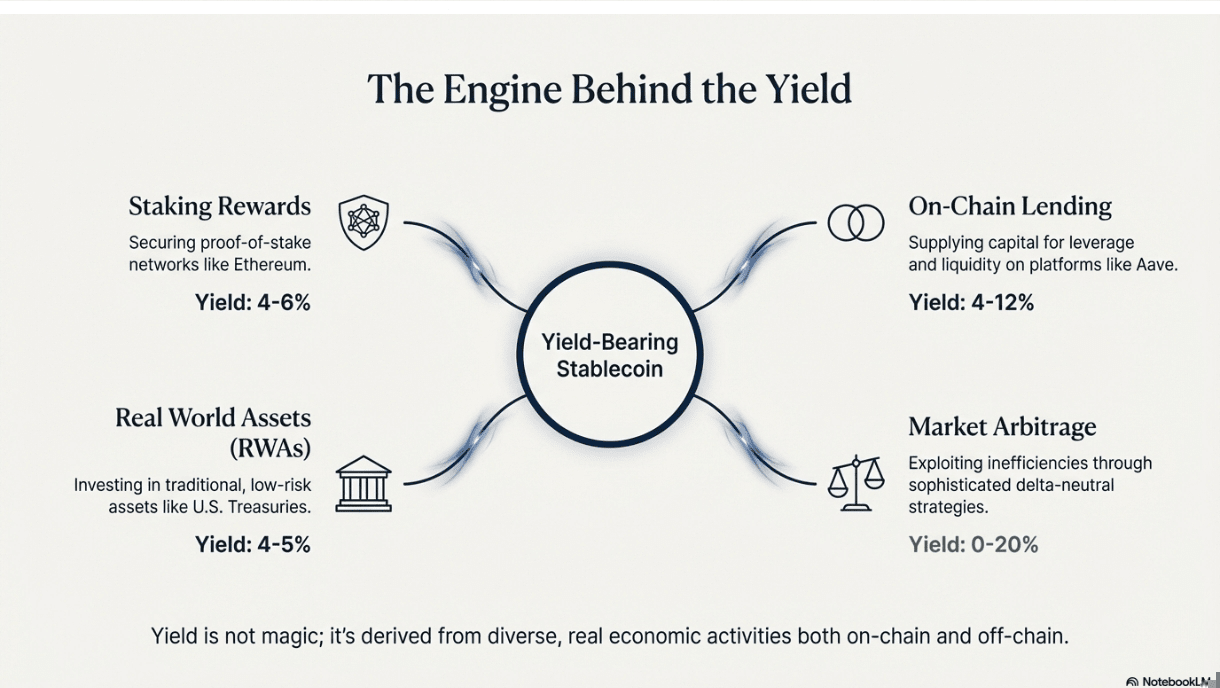

The yield sources vary wildly:

DeFi-Native Models tap into the crypto economy's natural demand for leverage and liquidity. When someone wants to borrow USDC on Aave to buy more ETH, your yield-bearing stablecoin might be earning the interest they're paying. Simple supply and demand.

RWA-Backed Models work more like traditional money market funds, except on-chain. Your stablecoins get invested in U.S. Treasuries or bank deposits, earning whatever the Federal Reserve's interest rates allow. Currently that's around 4-5%, which honestly beats most savings accounts.

Synthetic Models get weird,in the best way. They use derivatives and arbitrage to create dollar exposure without actually holding dollars. Ethena's USDe, for example, buys ETH and simultaneously shorts ETH futures, creating a delta-neutral position that earns funding rates when traders are bullish.

Hybrid Models combine multiple strategies because, honestly, why pick just one? They might allocate 50% to Treasuries for stability and 50% to DeFi lending for higher yields, rebalancing based on market conditions.

The beauty of this setup is automation. Smart contracts handle everything,minting, burning, yield distribution, rebalancing. No human intervention needed, which means lower fees and 24/7 operation. Your money literally works weekends.

But let's be real about the trade-offs. Traditional stablecoins are boring by design,their only job is staying at $1. Yield-bearing stablecoins have to juggle peg stability AND yield generation, which means more complexity, more smart contract risk, and more ways things can go wrong.

The regulatory picture is getting clearer though. The GENIUS Act created a framework where yield-bearing stablecoins can operate legally in the U.S., as long as they follow certain reserve requirements and avoid direct interest payments to consumers (hence the wrapper tokens). Europe's MiCA regulations are similar,strict but workable.

What's really driving adoption is the realization that idle capital is expensive capital. If you're holding USDC that's earning 0% while inflation runs 3%, you're losing money in real terms. Yield-bearing stablecoins fix that without forcing you to take on the volatility of actual crypto investments.

❍ Types of Yield Bearing Stablecoins

Alright, so you want to understand the different flavors of yield-bearing stablecoins? Think of it like ice cream,they're all cold and sweet, but the ingredients and how they're made determine everything else.

I. LST-Backed Stablecoins (Liquid Staking Token Collateral)

These are like the chocolate vanilla of the space,familiar ingredients, reliable results. LST-backed stablecoins work by taking your volatile crypto (usually ETH) as collateral, but way more than needed (think 150% overcollateralization), then using that collateral to earn staking rewards.

How it works: You deposit $150 worth of ETH to mint $100 worth of stablecoin. The protocol stakes your ETH, earning around 4-6% annually from Ethereum's consensus rewards. That yield gets passed to stablecoin holders. If ETH crashes hard enough to threaten the peg, liquidation bots sell your collateral to maintain the backing ratio.

Real Example - sDAI (Sky Protocol): This is probably the most battle-tested example. sDAI takes DAI (which is already overcollateralized with ETH and other assets) and wraps it in a yield-bearing token that earns from MakerDAO's Dai Savings Rate (DSR). Currently earning 5.57% APY with $98.82 million in TVL. The yield comes from protocol fees generated by the broader MakerDAO ecosystem,when people borrow DAI, they pay interest, and some of that flows to sDAI holders.

Historical performance has been solid: averaged 6-8% through 2024, peaked at 16% during the ETH bull run earlier this year, though it's settled down as staking rewards normalized. The peg held even during October's crypto crash, though it did briefly dip to $0.99.

Analogy: It's like putting your car up as collateral for a loan, but instead of borrowing money, you're creating digital dollars. While your car sits in the lot, it's somehow earning rental income that gets paid to you. If your car loses too much value, they sell it to protect the lender, but until then, you're earning steady returns.

Risks: ETH volatility is the big one. If ETH drops 50% overnight (it's happened before), you might get liquidated even with overcollateralization. Smart contract bugs are another concern, though MakerDAO has been around long enough to iron out most issues. The yields also fluctuate with staking demand,bear markets mean lower returns.

II. RWA-Backed Stablecoins (Real World Asset Collateral)

These are the "boring but dependable" option. RWA-backed stablecoins invest in traditional financial assets like U.S. Treasuries, money market funds, or bank deposits. Think of them as on-chain CDs that you can actually use.

How it works: You deposit USDC, the protocol uses that money to buy Treasury bills or park it in bank accounts, and you get yield-bearing tokens representing your claim on those assets. The yield comes from whatever the U.S. government is paying on short-term debt (currently 4-5%) minus small management fees.

Real Example - USDY (Ondo Finance): Backed by short-term U.S. Treasuries through BlackRock's BUIDL fund. Currently earning 3.99% APY with $667.5 million in TVL across multiple chains. You can redeem daily, and the peg has been rock-solid at $1.11 (reflecting accumulated yield) with zero significant depegs.

What's cool about USDY is the regulatory compliance,it's structured to meet U.S. securities requirements while still being composable in DeFi. You can use it as collateral on Aave, provide liquidity on Uniswap, or just hold it for the yield.

Another Example - USDM (Mountain Protocol): Similar Treasury-backing but fully regulated in Bermuda, earning around 5% fixed with ~$500 million TVL. The regulatory clarity actually matters here,institutions trust it more than experimental DeFi protocols.

Analogy: This is like having a high-yield savings account that you can actually spend from. Your money goes into government bonds (the safest investment on Earth), you earn the bond interest, but unlike traditional bonds, you can access your money anytime and use it like cash.

Risks: The yields are tied to Federal Reserve policy, so if rates drop, your returns drop. There's also custodial risk,someone has to hold the actual Treasury bills, and if that custodian fails, you're in trouble. Regulatory changes could impact operations, though recent frameworks have been favorable.

III. Synthetic (Delta-Neutral) Stablecoins

Here's where things get spicy. Synthetic stablecoins don't actually hold dollars or dollar-backed assets. Instead, they create dollar exposure through derivatives magic, earning yield from market structure inefficiencies.

How it works: Take Ethena's USDe as the prime example. The protocol buys ETH (creating upward exposure) and simultaneously shorts ETH futures (creating downward exposure). The long and short positions cancel out price-wise, but the short position earns funding rates when the market is bullish (longs pay shorts). Plus, the ETH collateral gets staked for additional yield.

Real Example - USDe (Ethena): Currently earning 5.25% APY with $8.5 billion in TVL (down from a peak of $15 billion). The yield comes from two sources: ETH staking rewards (~4%) and perpetual futures funding rates (variable, but positive when traders are bullish). Total revenue over the past year was $450 million, all flowing to stakers.

The genius is in the arbitrage opportunity. When USDe trades below $1, arbitrageurs can buy it, redeem for exactly $1 worth of collateral, and pocket the difference. This keeps the peg tight without requiring traditional reserves.

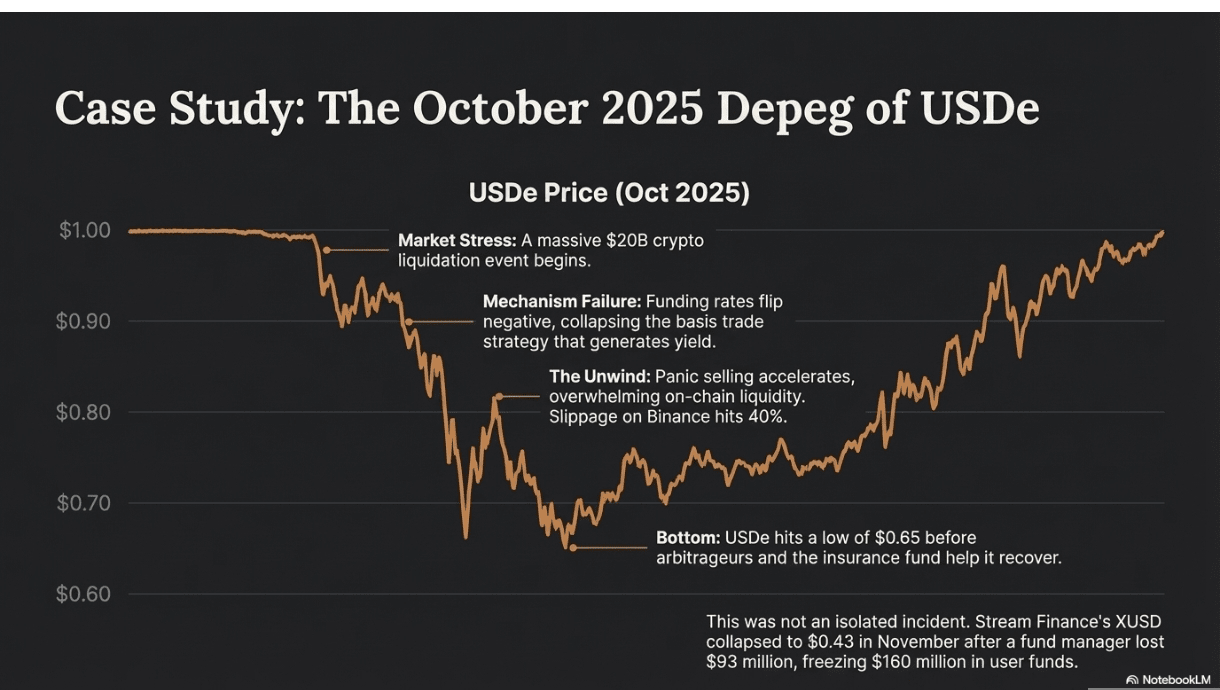

But October's crash showed the risks. When $20 billion in crypto got liquidated, funding rates went negative (shorts started paying longs), and USDe briefly depegged to $0.65 as the model's assumptions broke down. It recovered, but not without sweating.

Analogy: Imagine you run a casino where you bet on both red and black in roulette, so you can't lose on the outcome. But you earn money from the house edge and from the excitement fees charged to other gamblers. You're market-neutral but still profitable,until something weird happens with the roulette wheel itself.

Risks: Basis trade unwind is the big scary one. If futures markets break down or funding rates go persistently negative, the yield disappears and the peg comes under pressure. There's also counterparty risk from the exchanges where the hedging happens. Ethena mitigates this with an insurance fund, but it's still experimental compared to traditional models.

IV. Hybrid Models

The "why choose?" approach. These protocols blend multiple strategies to balance yield and stability, often using AI or algorithmic rebalancing to optimize allocations.

Real Example - SIERRA (Avalanche): Combines U.S. Treasuries with DeFi lending (Aave, Morpho) using algorithmic rebalancing. Currently earning 5-8% APY with significantly lower volatility than pure DeFi strategies. The AI adjusts the Treasury/DeFi allocation based on market conditions,more conservative during stress, more aggressive during calm periods.

Analogy: It's like having a robo-advisor for your stablecoin that automatically moves money between bonds and higher-yielding investments based on market conditions, always trying to maximize returns while keeping risk manageable.

Risks: Complexity is both a feature and a bug. The algorithmic rebalancing could malfunction, or the protocol could be exposed to multiple failure modes at once. But the diversification also provides some protection against any single strategy failing.

❍ How Stablecoins Generate Yields

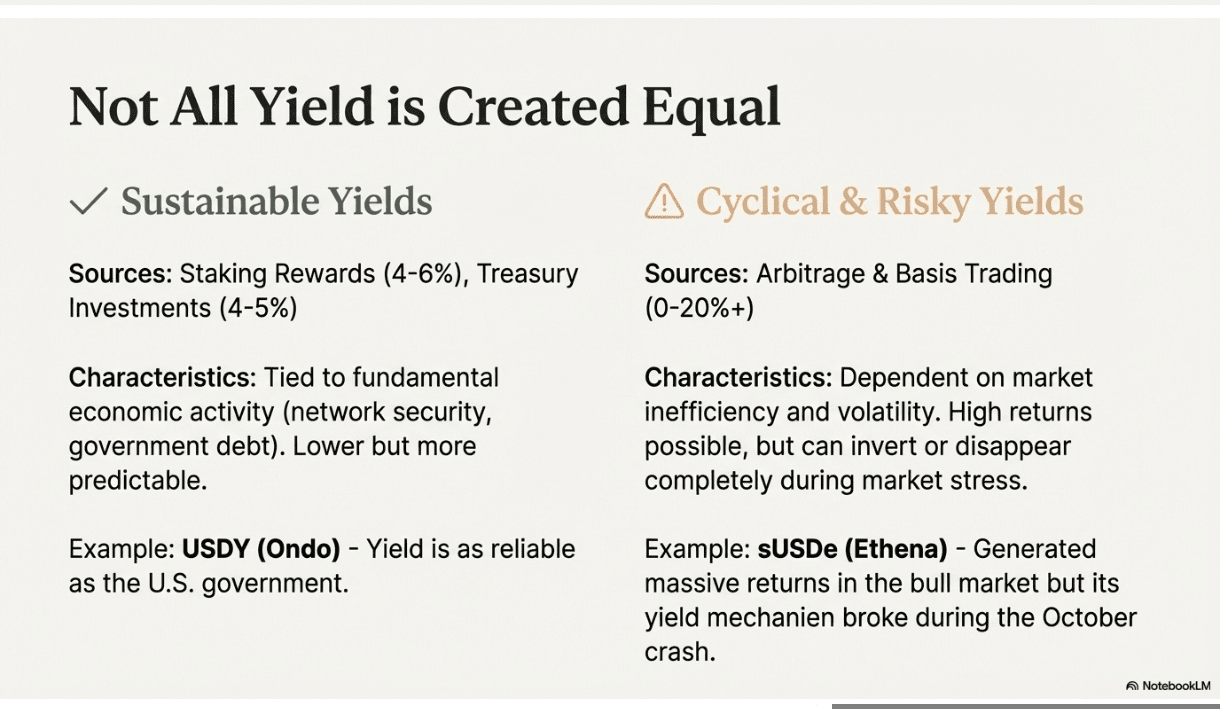

The dirty secret of yield-bearing stablecoins is that the "yield" isn't coming from nowhere. It's coming from real economic activity, and understanding where it comes from is crucial to evaluating whether it's sustainable.

I. Staking Rewards

This is probably the most straightforward source. When you stake ETH or other proof-of-stake tokens, you're essentially getting paid to help secure the network. The blockchain inflates the token supply to reward stakers, and that inflation becomes your yield.

Real Data: Ethereum staking currently yields about 4-6% annually, though it fluctuates based on how much ETH is staked and network activity. When gas fees are high, stakers earn more from transaction tips. During the bull run earlier this year, yields peaked around 8-9% before settling back down.

sDAI leverages this through MakerDAO's broader strategy. The protocol stakes a portion of its collateral and passes those rewards to sDAI holders. With $98.82 million in TVL earning 5.57% APY, that's about $5.5 million annually flowing to holders from staking activities.

Sustainability: This is probably the most sustainable yield source because it's directly tied to blockchain security economics. As long as Ethereum exists and needs validators, staking rewards will exist. The yields might fluctuate, but they're not going to zero unless the entire blockchain fails.

Analogy: Think of it like earning dividends from owning shares in a utility company. The company needs to exist to provide electricity, and shareholders get paid for providing the capital that keeps the lights on.

II. Lending and Borrowing

DeFi lending is basically traditional banking without the bank. Borrowers pay interest to access capital, lenders earn that interest minus platform fees.

Real Data: Aave, the largest DeFi lending platform, currently offers 4-7% APY on USDC deposits, fluctuating based on borrowing demand. During peak leverage periods (like when everyone wants to buy ETH with borrowed USDC), rates can spike to 12%+ before cooling down.

The yields come from real demand for leverage. Traders borrow stablecoins to buy crypto without selling their existing positions. Institutions borrow for arbitrage or yield farming. Even traditional businesses might borrow USDC for working capital if it's cheaper than bank loans.

Historical Performance: Lending yields averaged around 5% through 2024, but spiked to 15-20% during the spring bull run when leverage demand exploded. They've since normalized, but the baseline yield reflects genuine economic activity.

Sustainability: This depends on continued demand for crypto leverage and DeFi adoption. Bear markets hurt because fewer people want to borrow, but the yields never go completely to zero as long as there's any economic activity.

Analogy: It's like peer-to-peer lending, but automated and transparent. Your money gets lent to people who need capital, they pay interest, and you earn most of that interest while the platform takes a small cut.

III. Liquidity Provision and Market Making

DEXs (decentralized exchanges) need liquidity to function. Liquidity providers deposit tokens into pools and earn fees from trading volume plus any additional incentives.

Real Data: Curve pools currently offer modest base yields (0-2%) but can reach 5%+ when you factor in CRV token rewards. The 3Pool (USDC/USDT/DAI) has about $1 billion in TVL and generates fees from the massive volume of stablecoin trading.

The beauty for yield-bearing stablecoins is minimal impermanent loss. When you're providing liquidity between different stablecoins or between a stablecoin and its yield-bearing version, price movements are tiny, so you keep most of the fee income.

Example: sDAI/DAI pools on Curve let you earn both the underlying DAI Savings Rate AND trading fees from people arbitraging between the two tokens. During high-activity periods, this can add 1-2% annually on top of the base yield.

Sustainability: Depends on trading volume and token incentives. Base yields are sustainable as long as people trade, but token rewards can dry up if projects stop subsidizing liquidity.

IV. Treasury Investments

The most boring but stable option. Protocols invest in U.S. Treasury bills, money market funds, or high-grade corporate debt, earning whatever traditional finance offers.

Real Data: USDY earns 3.99% APY by holding Treasury bills through BlackRock's tokenized fund. USDM does something similar with 5% fixed returns. These yields directly track Federal Reserve policy,when the Fed raises rates, yields go up, and vice versa.

What makes this interesting is the accessibility. Normally, you need $10,000+ to buy Treasury bills directly, and they're not exactly liquid. RWA-backed stablecoins give you Treasury exposure with $1 minimums and instant liquidity through DeFi protocols.

Sustainability: As sustainable as the U.S. government, basically. The yields will fluctuate with interest rates, but they're backed by the full faith and credit of the Treasury. The main risk is rates going to zero, but even then, you're not losing principal.

Analogy: It's like having a money market fund that you can spend like cash. Your money goes into the safest investments on Earth, but you can still use it to buy coffee or provide DeFi liquidity.

V. Arbitrage and Basis Trading

This is where things get sophisticated. Arbitrage involves exploiting price differences across markets, while basis trading captures the spread between spot prices and futures contracts.

Real Example: Ethena's USDe uses basis trading extensively. The protocol buys ETH at $3,000 and simultaneously sells ETH futures at $3,050. When both contracts expire, they pocket the $50 difference regardless of where ETH price went. Plus, they earn funding rates when futures are trading at a premium.

Real Data: USDe has generated $450 million in revenue over the past year using these strategies, with current yields around 5.25% APY. During high volatility periods, basis trades can yield 15-20% annualized, though they can also go negative during market stress.

The October crash demonstrated both the power and the risk. When crypto markets melted down, the basis trades initially performed well (volatility is good for arbitrage), but then funding rates flipped negative and futures markets became dislocated. USDe briefly depegged but recovered as markets normalized.

Sustainability: This depends on continued market inefficiency and volatility. As long as crypto markets aren't perfectly efficient (and they're definitely not), arbitrage opportunities will exist. But the yields are inherently variable and can disappear during extreme stress.

Analogy: It's like being a foreign exchange trader at an airport, making money on the spread between buy and sell prices. Most of the time it's profitable, but during chaos (like a natural disaster), the normal relationships can break down.

The key insight is that sustainable yields come from real economic value creation,securing networks, facilitating lending, or providing liquidity. The speculative stuff like basis trading can generate higher returns but tends to be cyclical and risky.

Most successful yield-bearing stablecoins blend multiple sources to balance return and stability. Pure plays on any single strategy tend to be either too risky or too low-yielding for mass adoption.

❍ Top 5 Yield Bearing Stablecoins

Let's get into the meat of what actually matters,which yield-bearing stablecoins have real scale, actual users, and aren't just marketing experiments with fancy whitepapers.

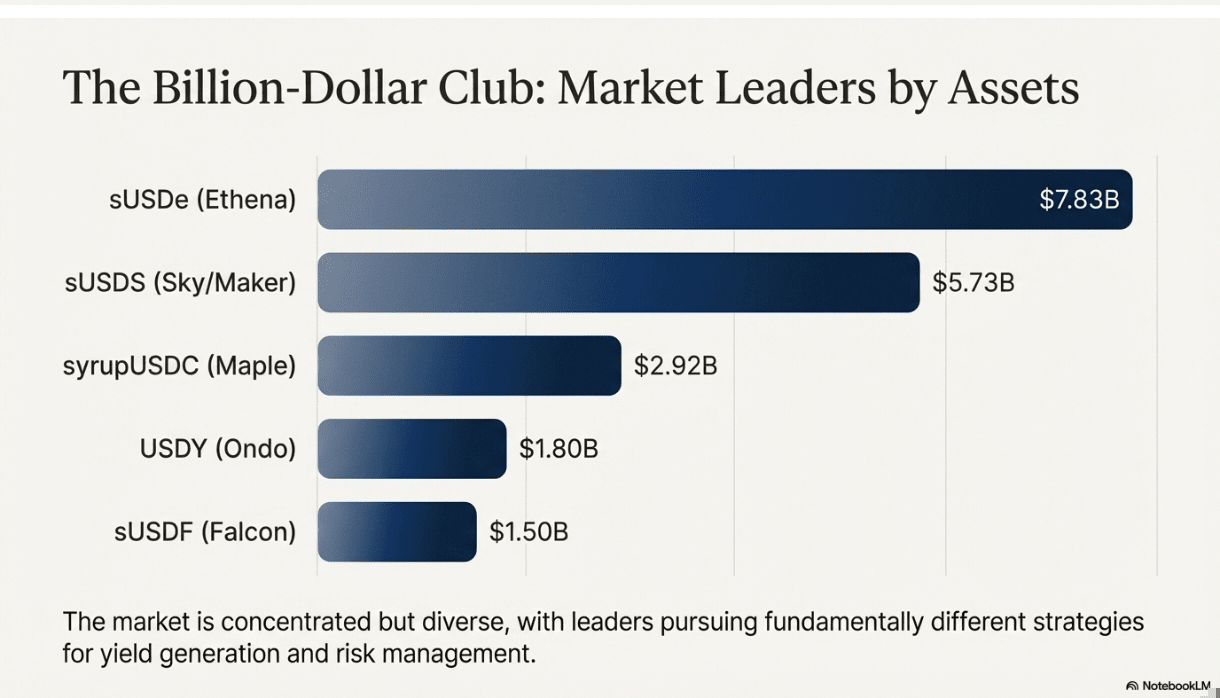

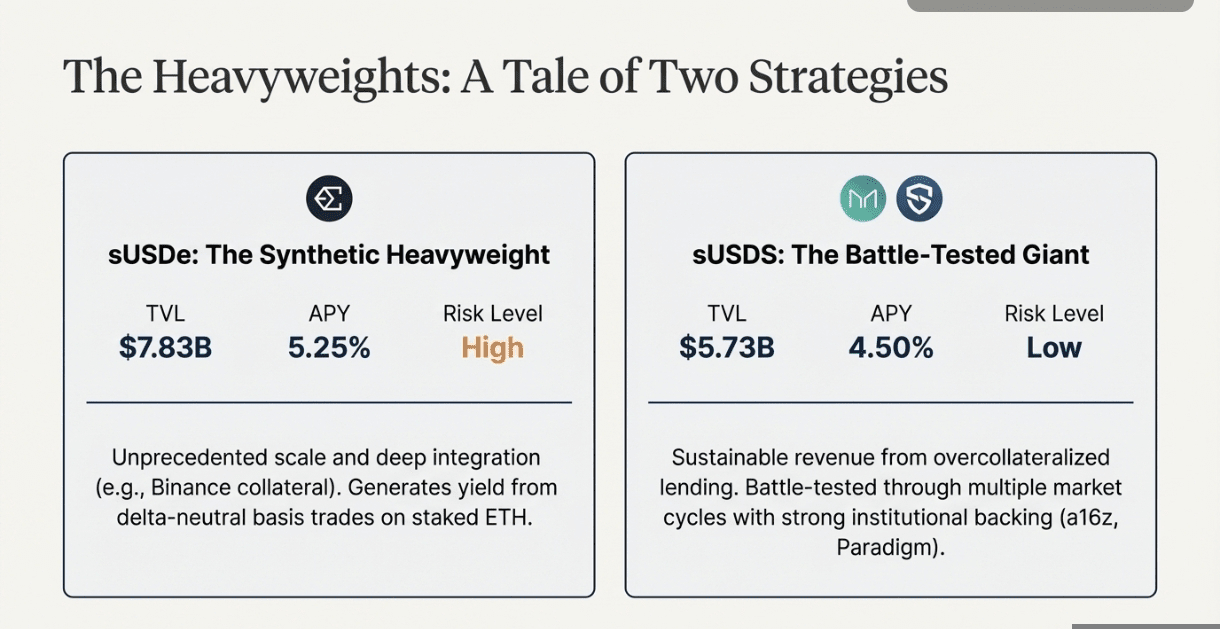

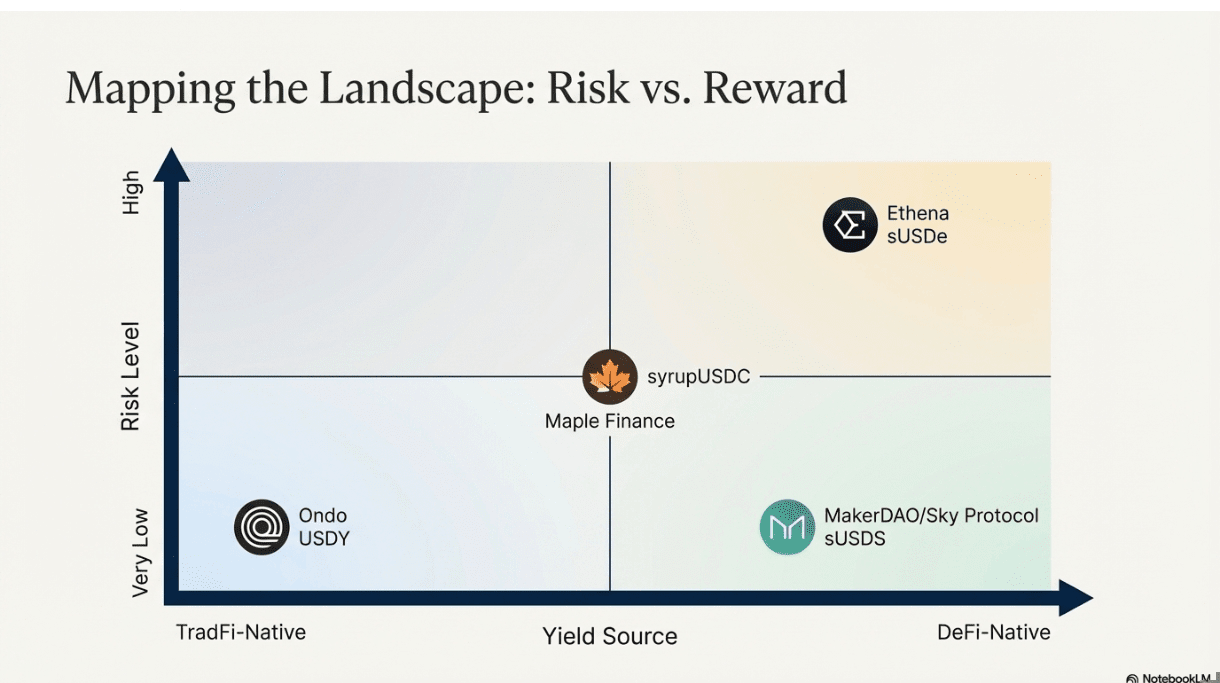

1. sUSDe (Ethena Protocol) - The Synthetic Heavyweight

TVL: $7.831 billion | APY: 5.25% | Circulating Supply: 8.395 billion USDe

sUSDe is basically the poster child for how crazy ambitious yield-bearing stablecoins can get. It's the staked version of Ethena's USDe, which creates synthetic dollar exposure through delta-neutral strategies that would make traditional finance risk managers break out in hives.

Here's the breakdown: Ethena deposits your money into staked ETH (earning ~4% base yield) while simultaneously shorting ETH perpetual futures on exchanges like Binance. The long ETH position and short futures position cancel out price-wise, but the short earns funding rates when traders are bullish. Add the two together, and you get that 5.25% yield.

Performance: This thing absolutely exploded in 2025. Supply peaked at $12 billion in August,that's 15% of USDC's entire supply, achieved in less than a year. Though it did pull back to $8.4 billion after October's market chaos when funding rates went negative and everyone remembered that synthetic stablecoins can be fragile. defillama

What's impressive is the integration depth. Binance uses USDe as collateral for their 280 million users with $190 billion in assets. Aave and Pendle let you loop the position for leveraged yields north of 20%. That's the kind of institutional adoption that separates real protocols from science experiments.

On-Chain Metrics: Transaction volume hit $366 billion year-to-date with 1.73 million transactions. For context, that's more volume than some entire blockchain ecosystems. The holder distribution is surprisingly decentralized,about 150,000 total holders with the top 10 controlling around 25% (mostly exchanges and protocols).

The Reality Check: October 2025 showed what happens when the basis trade breaks down. USDe depegged to $0.65 during a massive liquidation event when funding rates flipped negative. It recovered, but not before reminding everyone that synthetic stablecoins are only as stable as their underlying assumptions.

2. sUSDS (Sky Protocol, formerly MakerDAO) - The Battle-Tested Giant

TVL: $5.729 billion | APY: 4.50% | Circulating Supply: 9.143 billion USDS

If sUSDe is the flashy newcomer, sUSDS is the grizzled veteran. This is MakerDAO's yield-bearing wrapper for their newly rebranded USDS token, earning from the Sky Savings Rate (SSR) that's funded by one of DeFi's most sustainable revenue engines.

The mechanism is refreshingly simple compared to synthetic schemes: overcollateralized loans (mostly ETH and stablecoins) generate interest, liquidation fees, and protocol revenue, and some of that flows to sUSDS holders. No derivatives, no funding rate exposure, just good old-fashioned interest income from people borrowing money.

Performance: TVL grew 50% year-to-date to $5.7 billion post-rebrand, though it's had some adoption challenges as the market tries to figure out the difference between DAI, USDS, and sUSDS. That said, MakerDAO/Sky generated $104 million in fees during Q3 alone, providing real revenue to back the yields. defillama

The November announcement of a $2.5 billion RWA allocation with Obex is huge,that's protocols finally bridging the gap between DeFi yields and traditional finance stability.

On-Chain Metrics: $621 billion in yearly transaction volume across 1.01 million transactions. The holder distribution is healthier than most, with about 200,000 holders and only 20% concentration in the top 10 wallets.

Credibility Factor: This protocol has been battle-tested through multiple bear markets and black swan events. MakerDAO has $54.5 million in funding from a16z and Paradigm, and has been generating real revenue since 2017. If you want boring but reliable yields, this is probably your safest bet.

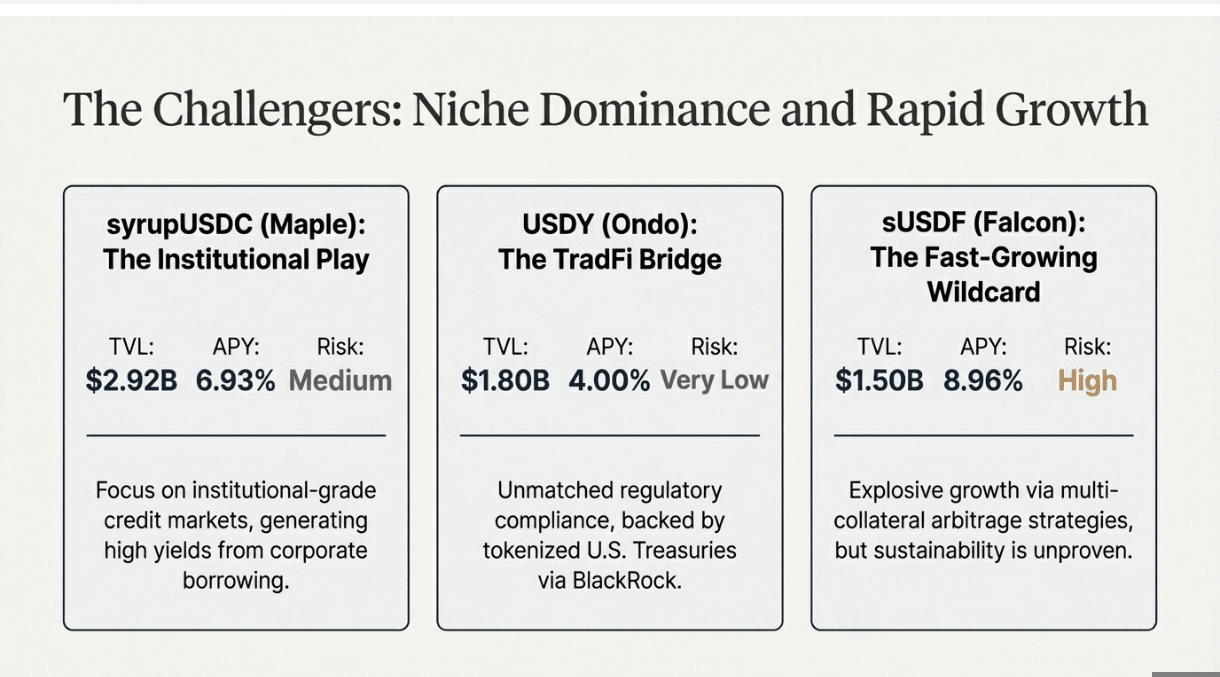

3. syrupUSDC (Maple Finance) - The Institutional Play

TVL: $2.92 billion | APY: 6.93% | Circulating Supply: 1.346 billion

Maple took a different approach,instead of trying to democratize yield access, they focused on institutional lending markets and just wrapped the whole thing in a user-friendly token. syrupUSDC deposits your USDC into institutional lending pools where companies and funds borrow at 9.2% average rates.

The institutional focus shows in the numbers. AUM hit $3.3 billion in October, up 2x from Q1, driven by partnerships with firms like BlockTower and GSR who need regulated, above-board lending. This isn't teenagers yoloing into leverage; it's actual businesses borrowing for actual business purposes.

Performance: TVL exploded 880% year-to-date from $0.3 billion, with Q3 revenue up 66% to $2.18 million. The expansion to Arbitrum helped them cross $1 billion in supply, proving the multi-chain thesis.

On-Chain Metrics: Transaction volume is lower,$2.9 billion annually with 69,000 transactions,but that reflects the institutional client base. These are large, infrequent transactions, not retail yield farming. About 50,000 total holders with 30% concentrated in the top 10 wallets (institutions and liquidity pools).

The Trade-off: Higher yields come with higher risks. The 6.93% APY depends on borrowers actually paying back their loans. Maple mitigates this through overcollateralization and active loan management, but there's still credit risk that pure Treasury-backed models don't have.

4. USDY (Ondo Finance) - The TradFi Bridge

TVL: $1.8 billion | APY: 4% | Circulating Supply: 624 million

USDY is what happens when you take the most boring investment strategy possible (short-term Treasury bills) and make it actually useful by putting it on-chain. It's backed by tokenized U.S. Treasuries through partnerships with BlackRock, earning whatever the U.S. government is paying on short-term debt.

The magic is in the infrastructure. USDY works across Ethereum, Stellar, and Sei, enabling cross-border payments and treasury management for businesses that need dollar exposure without the hassle of traditional banking. The September launch on Stellar and Sei specifically targeted payment corridors where traditional banking is slow and expensive.

Performance: TVL doubled year-to-date to $1.8 billion with $1.7 billion in net inflows, mostly from institutions looking for regulatory-compliant yield. Q4 earnings hit $3.25 million, which might not sound like much, but it's pure, low-risk yield backed by the U.S. government.

On-Chain Metrics: Transaction volume is modest,$685 million year-to-date with only 2,900 transactions,but that's intentional. This isn't designed for DeFi yield farming; it's designed for treasury management and payments. About 10,000 holders with 40% concentration in institutional wallets.

Regulatory Clarity: This is probably the most compliant yield-bearing stablecoin in existence, structured to meet U.S. securities requirements while maintaining composability. The partnerships with regulated entities like BlackRock provide institutional comfort that DeFi-native protocols can't match.

5. sUSDf (Falcon Finance) - The Fast-Growing Wildcard

TVL: $1.5 billion staked | APY: 8.96% | Circulating Supply: 2.008 billion USDf

sUSDf is the new kid making noise. Launched early 2025, it's already hit $1.5 billion in staked TVL by offering multi-collateral backing (12+ assets) and promising to expand into RWAs like T-bills and gold.

The yield mechanism blends basis trading and arbitrage similar to Ethena, but with broader collateral support beyond just ETH. The 8.96% APY is higher than most competitors, though that comes with the obvious question of sustainability,high yields in crypto often signal high risks.

Performance: Supply grew 9.2% month-over-month to $2 billion in October, with 59,000 monthly users. For a protocol that didn't exist a year ago, hitting $1.5 billion in TVL is genuinely impressive.

On-Chain Metrics: $2 billion in transaction volume year-to-date across 414,000 transactions shows strong retail adoption. About 100,000 holders with relatively low concentration (15% in top 10) suggests organic, distributed growth rather than whale-driven pumping.

Investment Backing: $24 million raised from World Liberty Financial and $10 million from M2 Group/Cypher Capital in October provides runway and credibility, though the protocol is still proving its long-term viability.

The ranking basically comes down to a risk-return spectrum. If you want maximum safety, go with USDY or sUSDS. If you want maximum yield and don't mind complexity, sUSDe and sUSDf are your options. syrupUSDC sits in the middle with institutional backing but credit risk.

What's clear is that this market has real scale and diversity now. These aren't just experimental DeFi protocols anymore,they're handling billions in institutional and retail capital, with real revenue and sustainable business models.

❍ Risks of Yield Bearing Stablecoins

Now we get to the part that makes lawyers nervous and risk managers reach for the antacids. Yield-bearing stablecoins offer returns that traditional finance can't match, but they're also introducing risks that didn't exist when stablecoins were just boring dollars sitting in bank accounts.

I. Smart Contract Vulnerabilities

The first thing to understand is that yield-bearing stablecoins are essentially software programs handling billions of dollars. And software has bugs. Unlike traditional banks that rely on legal contracts and human oversight, these protocols run automatically through smart contracts that are immutable once deployed.

Real-World Carnage: In September 2025, Sui-based yield protocol Nemo got drained for $2.4 million through a smart contract exploit that manipulated the yield calculation logic. The attacker basically convinced the contract that they deserved more tokens than they actually put in, and the code dutifully paid out. defisafety

This followed a pattern from 2024 where Origin Dollar (OUSD) faced repeated security failures in its DeFi wrapper functions, leading to $5 million in frozen funds and temporary protocol shutdowns. The problem wasn't malicious intent,it was code that didn't account for edge cases in yield distribution.

The Scale Problem: H1 2025 saw 344 crypto incidents causing $2.47 billion in losses industry-wide, with smart contract bugs responsible for $1.6 billion of that. Yield-bearing protocols accounted for 15% of DeFi exploits because their yield distribution mechanisms are inherently more complex than simple token transfers. certik

What This Means: Every additional feature,auto-compounding, cross-chain bridges, integration with lending protocols,is another potential attack vector. sUSDe's integration with Aave and Pendle creates more yield opportunities, but it also means more smart contracts that could fail simultaneously.

Mitigation Reality Check: Audits help, but they're not magic. CertiK and Halborn can find obvious vulnerabilities, but they can't predict every possible interaction between complex protocols. Bug bounties are useful ($1 million for Ethena), but most white-hat hackers aren't going to spend months reverse-engineering yield mechanisms for a potential payout.

The harsh truth is that smart contract risk is existential. If the contract fails catastrophically, your money could just disappear with no legal recourse. Traditional banks have FDIC insurance; smart contracts have "code is law" and prayer.

II. Depegging Events

Depegging is when the stablecoin's price breaks away from $1, usually downward, turning your "stable" asset into a volatile mess. For yield-bearing stablecoins, this risk is amplified because the yield mechanisms can actually accelerate depegging under stress.

October 2025: The Reality Check: Ethena's USDe provided a masterclass in how quickly things can go wrong. During the October crypto liquidation event,$20 billion in positions getting closed,USDe depegged to $0.65 as its basis trade strategy collapsed. coindesk

What happened was that funding rates flipped negative (shorts started paying longs instead of the reverse), the delta-neutral strategy that generates USDe's yield stopped working, and panic selling accelerated the depeg. The token recovered to $0.95+ within days, but anyone who needed liquidity during the crisis got crushed.

Stream Finance: Total Collapse: November 2025 brought an even worse example. Stream Finance's XUSD depegged to $0.43 after their fund manager lost $93 million on leveraged trades, freezing $160 million in user funds. This wasn't a temporary liquidity crisis,this was protocol death. theblock

The Contagion Effect: Moody's reported 800+ depeg events in 2024-2025, up from 600 in 2023. When one yield-bearing stablecoin depegs, it creates doubt about the entire category. USDe's October crisis wiped $19 billion in crypto liquidations and reduced yield-bearing TVL by 40-50% temporarily.

Why Yield Makes It Worse: Traditional stablecoins like USDC can survive runs because they hold actual dollars. Yield-bearing stablecoins often hold more complex assets (staked ETH, Treasury tokens, basis trade positions) that can't be liquidated instantly at face value during stress.

The feedback loop is vicious: depeg concerns cause selling, selling creates liquidity pressure, liquidity pressure forces fire sales of underlying assets, fire sales worsen the depeg. Rinse and repeat until either the protocol dies or market conditions stabilize.

III. Yield Sustainability Collapse

High yields in crypto often signal high risks, and yield-bearing stablecoins are no exception. The yields come from real economic activity, but that activity can disappear quickly during downturns.

The Basis Trade Unwinding: Ethena's 25% yields earlier in 2025 came from basis trades that work great in bull markets but can invert during stress. When futures premiums disappear or go negative, the entire yield mechanism breaks down. October's event showed this clearly,funding rates that had been consistently positive for months suddenly flipped, wiping out the yield advantage overnight.

DeFi Lending Collapse: Yields from protocols like Aave fell from 12% to 4-6% during H1 2025 as borrowing demand dried up. When fewer people want leverage, lenders earn less. This affects protocols like syrupUSDC that depend on sustained borrowing demand from institutions.

RWA Interest Rate Exposure: Treasury-backed stablecoins like USDY are directly exposed to Federal Reserve policy. If rates drop to zero (like they did in 2020-2021), the yield advantage disappears. The protocol still works, but the economic incentive to hold yield-bearing stablecoins over regular ones evaporates.

Real Numbers: Basis trade failures contributed to 20% of 2025's $2.47 billion in crypto losses. Ethena's insurance fund had to cover $100 million in potential shortfalls when their strategies stopped working temporarily.

IV. Regulatory Pressure and Uncertainty

The regulatory environment around yield-bearing stablecoins is evolving rapidly, and not always in favor of innovation. The GENIUS Act passed in July 2025 created clarity but also restrictions that could limit future growth.

Direct Yield Bans: The GENIUS Act prohibits direct yield payments to consumers, forcing protocols to use wrapper tokens (like sUSDe wrapping USDe). This adds complexity and potentially reduces adoption among less sophisticated users who just want simple yield without understanding the technical differences.

EU Enforcement: Post-MiCA implementation, Binance delisted non-compliant USDT in the European Union, reducing its EEA trading volume by 20%. Circle's MiCA license helped USDC grow to $61 billion in supply, but compliance costs are substantial and favor large issuers.

Banking Industry Pushback: Traditional banks are lobbying aggressively against stablecoin yields, arguing they create unfair competition for deposit-gathering. The Bank Policy Institute proposed extending GENIUS Act restrictions to exchanges, which could effectively kill yield-bearing stablecoins for U.S. users.

Offshore Risks: Protocols operating offshore (like Tether's 4% yield programs) face increasing SEC scrutiny. Proposed fines exceeded $100 million in 2025, and global regulatory coordination could squeeze non-compliant issuers entirely.

Market Bifurcation: Regulation is splitting the market between compliant protocols (USDC, PYUSD) that captured 50% growth and non-compliant ones that lost 10% market share. This creates a two-tier system where regulatory compliance becomes the primary competitive advantage.

V. Counterparty and Custodial Risks

Yield-bearing stablecoins often depend on third parties,custodians, fund managers, exchanges,that introduce single points of failure absent in simpler protocols.

The Stream Finance Disaster: The $93 million fund manager loss wasn't a smart contract bug or market volatility,it was human error and potential fraud. Someone made leveraged bets with user funds and lost, highlighting how yield strategies can introduce counterparty risks that don't exist with simple stablecoin holdings.

Exchange Dependency: Ethena's delta-neutral strategies depend on exchanges like Binance and Bybit for futures positions. When Bybit suffered a $1.5 billion hack in February 2025, it didn't directly impact USDe (the positions were secured), but it demonstrated how dependent these protocols are on external infrastructure.

Custody Concentration: RWA-backed stablecoins like USDY depend on custodians to hold the underlying Treasury bills. If BlackRock's custody systems fail or face regulatory action, the entire protocol could freeze. This is traditional finance risk imported into DeFi.

H1 2025 Numbers: $2.47 billion in total crypto losses, with 60% attributed to counterparty issues including exchange hacks, custody failures, and fund manager fraud. Yield-bearing protocols were disproportionately affected because of their reliance on external partners.

VI. Liquidity Crises

During stress events, yield-bearing stablecoins can become illiquid precisely when users need to exit most urgently. This creates death spirals where illiquidity feeds depegging which feeds more illiquidity.

Market Depth Problems: USDe's October depeg saw 40% slippage on Binance because sell orders overwhelmed available liquidity. For context, USDC rarely sees more than 0.1% slippage even during major market events because of its deep, distributed liquidity.

Redemption Delays: Many yield-bearing stablecoins have redemption mechanisms that work fine during normal conditions but break down under stress. Daily redemption limits, processing delays, and minimum redemption amounts can trap users when they need liquidity most.

Cross-Chain Complexity: Multi-chain protocols face additional liquidity fragmentation. USDY operates across Ethereum, Stellar, and Sei, but liquidity isn't always balanced across chains. Users might find deep liquidity on Ethereum but thin markets on other chains.

Cascade Effects: When one major holder (like an institution) needs to exit, it can consume available liquidity and trigger a cascade of redemptions. This affected $300 million in TVL during 2025's depeg events.

The brutal reality is that yield-bearing stablecoins introduce multiple new failure modes while often providing only modest yield premiums over traditional alternatives. For institutional treasury management, the risk-adjusted returns might not justify the complexity.

But for users who understand the risks and size their positions appropriately, these protocols offer genuine innovation in programmable money. The key is avoiding the yield-chasing mentality that drove much of 2025's losses and focusing on protocols with sustainable business models and strong risk management.

The market is maturing,protocols with real revenue, conservative risk management, and regulatory compliance are separating from the yield-farming casinos. But caveat emptor remains the rule.