Table of contents

Preface

01 Basic information of the Tranchess project

02 Tranchess product architecture and operational status

03 CHESS Token Model and Valuation Analysis

04 Risk Classification Agreement Competitive Product Analysis

05 Tranchess development prospects

Preface

DeFi is a new deconstruction of the traditional financial world. It uses blockchain technology to enable financial activities to operate more efficiently, openly and transparently. Previously, financial products such as banks, exchanges, insurance, derivatives, etc. were all mapped in the DeFi field. With the advent of Tranchess, hierarchical funds have also been implemented in the crypto world. Hierarchical funds were originally a relatively complex financial derivative. They emerged to meet the investment needs of different types of investors with different risk preferences. Tranchess uses the characteristics of DeFi to reconstruct this product, lowering the threshold for use and making it more accessible. Multiple users can leverage this tool for asset management. Hierarchical funds generally consist of a parent fund and two parts of sub-funds. The sub-fund part is divided into high-risk and low-risk parts by dividing returns and risks. For the high-risk part, higher returns can be obtained by superimposing leverage, but at the same time it also bears more risks; for the low-risk part, the returns are more controllable and stable. These three parts can be split or combined according to investor preferences. As Tranchess enters the LSD track at the end of 2022, its unique tiered fund model brings more possibilities to this track. On the one hand, it increases the level of risk-free returns, and on the other hand, it reduces the risk under market fluctuations.

01 Basic information of the Tranchess project

1.1 Introduction to Tranchess

Tranchess is an asset price tracking and management protocol that runs on the BNB chain and Ethereum. It aims to provide different returns for users with different risk preferences, allowing them to have BNB, BTC, ETH or even stablecoins (such as BUSD or USDC) on hand. of users will be able to find the right product that best suits their needs in terms of risk profile and return. The concept for Tranchess was first conceived in early 2020 and has quickly grown to its current state. Inspired by the ability of tiered funds to cater to users’ different risk appetites, Tranchess offers different risk/return matrices through a main fund that tracks a specific underlying asset, such as BNB. For BNB and ETH funds, Tranchess enables the funds to obtain staking income by running PoS nodes.

1.2 Development history

The concept of Tranchess was first proposed in early 2020, and in Q2 2021, Tranchess was officially launched on the BSC mainnet and released the V1 version. The release of the V1 version quickly attracted a lot of attention, which was intuitively reflected in the TVL indicator. In just two months after its release, TVL successfully exceeded $1B and reached the highest TVL of nearly $2B in Q4. Its governance token CHESS was logged on Binance in October 2021.

As of April 2, 2023, CHESS is currently priced at US$0.25 (2023/4/3), with a circulating market value of US$30 million, a fully diluted market value of US$77 million, and a TVL of US$57.56 million.

In January 2022, BNB Fund was launched and became a Binance Chain validator, improving security and income. Currently, Tranchess has been stably maintained in the cabinet node.

The V2 version will be launched in June 2022. There have been significant improvements in liquidity and user management. An important update in V2 is the addition of 3 Bishop-BUSD pools and 1 nQueen-BNB pool. Through the AMM pool and automatically optimized trading lines, and the improved price calculation mechanism of QBR tokens to simplify the conversion process when the tokens are discounted, QBR tokens can be freely interchanged at any time under any circumstances. At the same time, QUEEN tokens also support real-time creation and redemption.

In December 2022, the qETH liquidity staking product was released.

1.3 Financing situation

In July 2021, Tranchess received US$1.5 million in seed round financing, led by Three Arrows Capital and Spartan Group, with participation from Binance Labs, Longhash Ventures, IMO Ventures and other institutions, as well as a number of crypto opinion leaders. This round of financing was mainly strategic investment, and the team focused on selecting institutions and individuals that could provide assistance for the project's start-up and initial growth. The average CHESS token price in the seed round was $0.1.

1.4 Team information

The Transchess team consists of a group of blockchain and financial experts from around the world with diverse backgrounds and experiences. According to the official website, the core team members come from the TradeFi field such as investment banks, asset management companies, and hedge funds. Their past industry experience includes but is not limited to traders, investment managers, and strategy researchers. The technical team comes from technology giants such as Google, Meta (Facebook) and Microsoft, and is experienced in network security of centralized exchanges and DeFi protocols.

The currently known public information is the founder @Danny Chong. Danny graduated from Nanyang Technological University in 2005 and has more than 16 years of banking experience. He once worked at Société Générale, responsible for Societe Generale's foreign exchange and emerging market business, and was also responsible for product research and development in the Asia-Pacific region. Later, he was responsible for the FX & Rates sales SEA department of Crédit Agricole CIB. One of his main duties was to be responsible for the development of new products in Asia and globally, including general products and structured products. During his tenure, he successfully led significant growth including sales, employees and digital operations. In addition to the financial industry, Danny has also created some healthy living concept brands in Singapore and Hong Kong.

1.5 Audit and Security

Tranchess places project security and user asset security in a very important position, both in terms of external publicity and internal community communication. Due to its strict security requirements, it has put forward higher requirements for cross-platform project cooperation, which once made the community think that it was overly cautious. However, with the occurrence of a series of black swan events since last year and the loss of user property caused by star projects being hacked and implicated in other cooperative projects, the community has gradually recognized the significance and value of Tranchess’s risk management requirements.

Every major code update of Tranchess will go through three stages of testing and review before it is officially launched:

1. Internal cross-self-assessment within the technical team;

2. The Tranchess team uses the inside;

3. Audit report from an external audit firm.

On the homepage of Tranchess, there are links to all historical audit reports for users to learn about. At the same time, Tranchess has participated in ImmuneFi’s bug bounty project since its inception, with a bounty of up to US$200,000 (or 10% of the potential maximum loss that the vulnerability may cause) depending on the risk level. Recently, Tranchess also synchronized the repair process of an ImmuneFi reported vulnerability in detail on its Medium.

02 Tranchess product architecture and operational status

Tranchess borrows three chess pieces to imply product features. The Queen is the strongest chess piece in chess, and the Bishop and Rook are the bishop and rook respectively, representing stability and attack. In Tranchess, Queen is the parent fund, and Bishop and Rook are sub-funds evenly separated from the parent fund, which are fixed income funds and leveraged funds respectively.

2.1 Product logic

Tranchess has been deployed on the BNB chain and Ethereum, and users can deposit tokens in both networks to mint corresponding QUEEN tokens. For funds on the BNB chain, the corresponding QUEENs are bQUEEN, eQUEEN and nQUEEN respectively. On Ethereum, in order to allow users to more clearly understand the characteristics of LSD, the QUEEN token of its ETH fund is named qETH.

QUEEN tokens are split into 0.5 BISHOP tokens and 0.5 ROOK tokens through the Split function. Correspondingly, 0.5 BISHOP tokens and 0.5 ROOK tokens can also be merged into 1 QUEEN token.

The essence of BISHOP token is fixed income, and the essence of ROOK token is 2x leverage token. ROOK tokens borrow half of the underlying assets belonging to BISHOP from BISHOP by paying interest, thereby obtaining leveraged exposure and amplifying risks and returns.

With the launch of Tranchess's BNB fund on BNB Chain, node staking has gradually become the third most important component of Tranchess's product design. By building nodes and participating in staking, the Tranchess team not only participates more deeply in the construction of the BNB Chain ecosystem, but also brings stable long-term returns to the fund.

In the current V2 version, Tranchess has launched Ethereum’s ETH liquidity staking fund. Tranchess's ETH liquidity staking product, its underlying nodes are not operated and maintained by the Tranchess team itself like the BNB fund, but are handed over to the major professional technical teams on the market for maintenance in a more decentralized manner. However, based on the past experience in The rich experience accumulated in operating BNB nodes allows the team to evaluate it from a more professional and safer perspective when selecting nodes, thereby avoiding risks as much as possible and ensuring the safety of fund funds while obtaining high-level pledge reward returns. .

Currently, Tranchess's ETH liquidity staking token qETH on Ethereum has two qETH-WETH AMM pools, one on Balancer and the other on Aura. Both pools currently maintain high double-digit LP returns through subsidized vote-buying through bi-weekly staking node voting.

2.2 Revenue model from user perspective

1. Obtain parent fund income: Holding Queen tokens can obtain Queen tokens by casting them in the primary market or buying them in the secondary market. By holding Queen tokens, you can gain BTCB/ETH/BNB risk exposure, and ETH/BNB's Qtoken on their respective mainnets (for example: qETH on Ethereum and nQUEEN on the BNB chain) can also obtain PoS staking benefits.

2. Obtain fixed income: Hold BISHOP tokens. There are two ways to obtain Bishop Token. One is to subscribe for Queen Token and then split it, and the other is to buy it in the secondary market. Holding Bishop Token can obtain fixed income and corresponding PoS staking income.

3. Obtain leveraged income: hold ROOK tokens. There are two ways to obtain ROOK Tokens. One is to purchase Queen Tokens and then split them, and the other is to purchase them in the secondary market. Holding ROOK Token can obtain the same risk exposure as the parent fund, and in addition, you can obtain corresponding PoS pledge income.

4. Obtain LP incentive income. There are currently 3 AMM pools on Ethereum: eBISHOP-USDC and eROOK-USDC on the Tranchess platform; qETH-WETH on Balancer. There are 4 AMM pools on the BNB chain: nBISHOP-BUSD; bBISHOP-BUSD; eBISHOP-BUSD; nQUEEN-BNB. Provide liquidity to the AMM pool and earn trading fees and CHESS token rewards.

It should be noted that LP pledged in the qETH-WETH pool on Balancer will not directly receive CHESS incentives. Tranchess uses these CHESS incentives to vote for Balancer staking nodes as bribes in the hope of obtaining higher BAL returns. In this way, the project party attracts more external investors to pledge qETH-WETH LP to obtain more sufficient liquidity, ensure the trading depth of LP, and prevent the de-anchoring of qETH and ETH.

5. Obtain platform governance token CHESS staking income. Staking Queen, Bishop and Rook can all obtain CHESS staking income.

2.3 Strategy risk and return analysis

ROOK achieves a leveraged portfolio by borrowing assets from BISHOP. ROOK's income = profit and loss of the parent fund * leverage multiple - interest paid to BISHOP. When the underlying price rises, ROOK multiplies the gains. When prices fall, compared with leveraged lending, ROOK does not have the risk of forced liquidation. Bishop obtains fixed income by lending assets, and by adding PoS staking income, Bishop expects the APR to reach nearly 7%, which is a very impressive level of risk-free income.

When the fund of funds is initially established, the net worth of Rook and Bishop is both 1. Rook borrows twice as much as Bishop, giving a leverage of 2. When the price of the underlying asset rises, due to leverage, the net value of ROOK increases by twice the increase of the underlying asset. At this time, the leverage ratio of the newly minted Rook decreases, and as the price rises, the leverage ratio continues to decrease, even approaching 1, causing the Rook leverage to fail. . When the price of the underlying asset falls, the net value of Rook drops by twice the decline of the underlying asset. At this time, the leverage ratio of newly minted Rook increases, and as the price drops, the leverage ratio rises sharply. At the same time, the net value of Rook will accelerate its decline.

In order to avoid the failure of Rook's leverage during continued rise, or the sharp decline in Rook's net worth during continued decline, Tranchess uses the Rebalance mechanism to restore the leverage ratio. The specific approach is to restore the Rook and Bishop net worth to 1 by allocating Queen tokens and changing the holding amounts of Rook and Bishop while keeping the asset value unchanged, thereby restoring the Rook leverage. The condition for triggering Rebalance is that the ratio of the net value of Rook and Bishop tokens exceeds 2 or is lower than 0.5, that is, if the underlying asset rises by more than 100%, or falls by more than 25%, Rebalance will be triggered. After superimposing the PoS staking model, the return rate of the fund of funds has a safety cushion, while providing more space for Rook holders in the event of a decline.

Judging from historical data, during the nearly 2 years of operation from V1 to V2, the market experienced several large fluctuations, and a total of 13 rebalances were performed, and the protocol ran smoothly.

Note: After the V2 upgrade optimizes the QBR price calculation mechanism, the number of Qtokens is no longer affected by Rebalance.

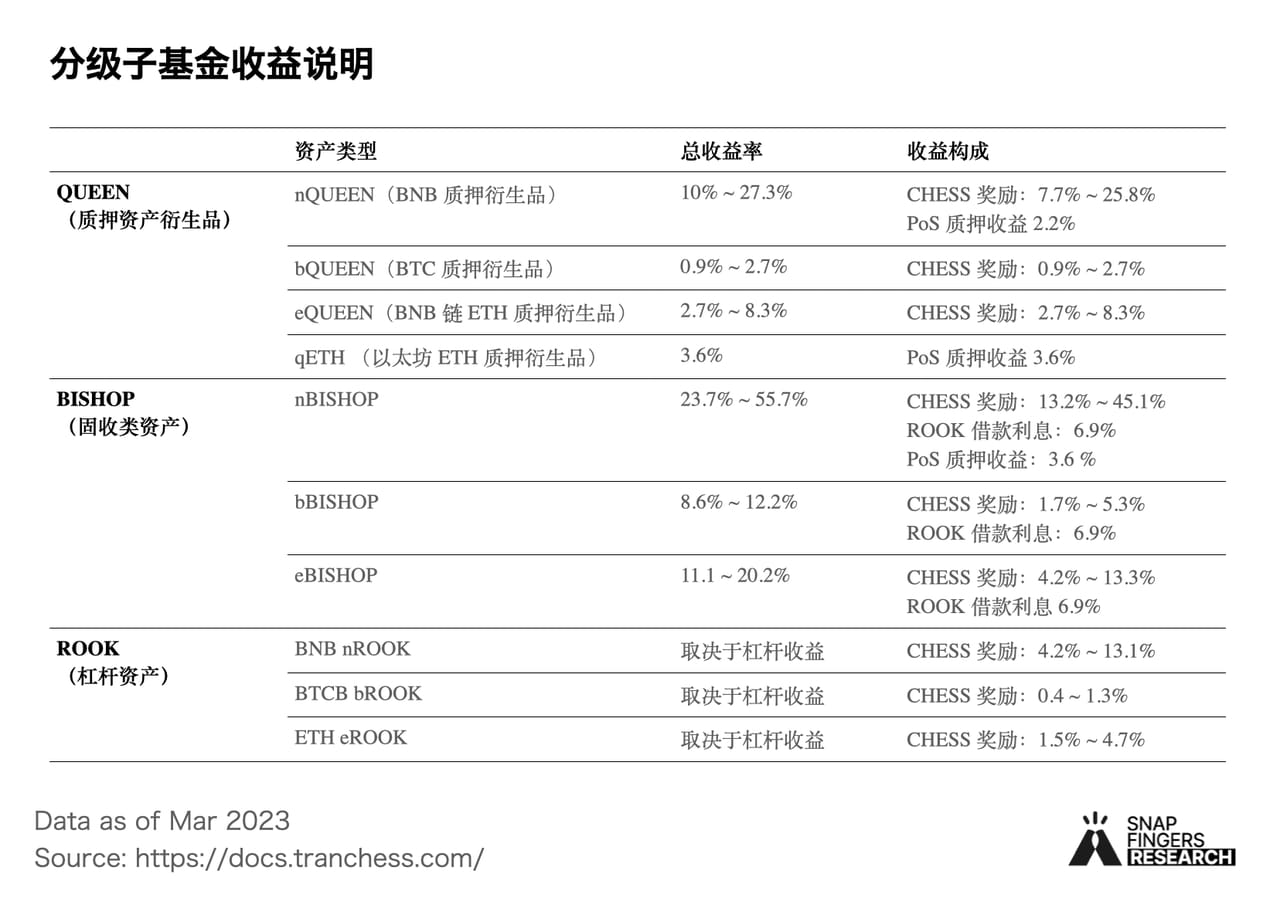

2.4 Actual income of the strategy

The size of the fund of funds

The BTCB fund size running on BNB Chain is 1340 BTCB, the ETH fund size is 1,854 ETH, and the BNB size is 54710 BNB.

ETH fund running on Ethereum, with a size of 213 ETH.

PoS staking income

The BNB fund running on BNB Chain has a PoS APR of 2.3% and a PoS utilization rate of 95.4%.

For ETH funds running on Ethereum, the PoS APR is 2.6% and the PoS utilization rate is 90%.

Liquidity pledge income

The qETH-WETH pool on Balancer has a TVL of about $425 K and an APR of 7.82% ~ 14.65%.

The qETH-WETH pool on Aura has a TVL of approximately $410 K and a real-time APR of 33.69% (historical APR is 15.75%).

Income of hierarchical sub-funds

Bishop’s income comes from three aspects:

Rook pays fixed interest of 7.3%.

Chess rewards obtained through staking reached a historical high of 63.8%

PoS node income is currently 3.3% on the BNB chain.

Rook’s income is reflected in the change in net value. In addition, it can also obtain PoS staking revenue share and CHESS emission rewards.

2.5 Current status of platform development

Product operations and related data

Tranchess provides services in two networks, BNB chain and Ethereum, including:

A total of 3 fund of funds products are provided on the BNB chain: BNB (54707 BNB), BTCB (1340 BTCB), and ETH (1854 ETH).

ETH (213 ETH) fund of funds product offered on Ethereum

There are 4 AMM pools on Ethereum: eBISHOP-USDC, eROOK-USDC on the Tranchess platform; qETH-WETH on Balancer; and qETH-WETH pool on Aura.

There are 4 AMM pools on BNB Chain: nBISHOP-BUSD; bBISHOP-BUSD; eBISHOP-BUSD; nQUEEN-BNB.

According to DefiLlama platform data (April 3), Tranchess’s current TVL is US$57.75 million, of which BNB chain TVL accounts for 99%. Tranchess ranks 12th in the BNB chain ecosystem. Tranchess’ BNB staking pool accounts for 3.92% of the total BNB staking volume.

Community operations

The official Trunchess Twitter currently has 42,000 followers and 60 users in 30 days. It is worth mentioning that in the update to the V2 version, the UI and user interaction have been upgraded specifically. The upgrade of the UI not only significantly improves the functionality, but also simplifies the process that some users found to be complicated before into a more understandable interactive operation method. Most of the suggestions come from the community. It can be said that the team attaches great importance to the voice of the community, so it has adopted many important and friendly suggestions from the community. The team’s understanding of DeFi is also reflected in the product usage level. With the overall development of DeFi and the digital currency industry, more and more "newcomers" in non-traditional blockchains are beginning to observe and even enter the field of DeFi. Therefore, any change that makes it simpler, more convenient and intuitive for users to use the product is worthwhile. It is something that users will be willing to get familiar with and understand. In the half year since Tranchess V2 was launched, it seems that the user experience and feedback are still very positive.

03 CHESS Token Model and Valuation Analysis

3.1 CHESS Token Economic Model

CHESS is the governance and utility token of Tranchess. According to CoinGecko data, the total supply of CHESS is 300 million pieces, with a current circulation of 115 million pieces and a market value of approximately $34.5M. Of the 300 million total supply of CHESS, 50% will be used for community distribution and incentives, of which 120 million will be released on the official Tranchess platform (the specific weekly emission plan is announced on the official website page). CHESS tokens will be released on a decreasing schedule over 4 years. The total number of CHESS tokens is 300 million, distributed as follows:

In addition to purchasing CHESS tokens on the secondary market, users can also obtain CHESS emission rewards in four ways:

Stake QUEEN, BISHOP or ROOK tokens on the official platform to receive CHESS emission rewards.

Stake CHESS on the official platform to create veChess and get weekly rebates.

Stake CHESS on Binance or Pancake Swap to get CHESS rewards.

Providing liquidity to the AMM pool can earn CHESS rewards.

3.2 CHESS Token Function

The main functions of CHESS are implemented through veCHESS, and staking CHESS can obtain veCHESS. The lock-up mechanism design of CHESS is similar to the more mainstream designs on the market: the lock-up time ranges from 1 week to 4 years. The longer the lock-up time/the larger the lock-up amount, the more veCHESS you will get (for example, 1 CHESS is locked up for 1 year) You can get 0.25 veCHESS, and if you lock up for 4 years, you will get 1 veCHESS).

Currently, the Tranchess platform only offers lock-up options of 1 week, 1 month, 3 months, 6 months, and 1 year. Longer lock-up options will be opened in the future. veCHESS function includes the following 3 aspects:

Governance: Holding veCHESS can participate in platform governance, such as deciding the emission ratio of each fund or AMM pool, the distribution ratio of PoS staking income between Bishop and Rook, and proposing adjustments to Bishop’s interest rate premium.

Dividends: Weekly dividends, which come from 50% of all handling fees in the Tranchess platform. Among them, the BNB chain distributes dividends to BTCB, ETH, BNB and BUSD; the Ethereum chain distributes dividends to qETH and USDC.

Increase staking income: Staking Queen, Bishop, and Rook fund tokens can obtain CHESS token rewards, and holding veCHESS can increase this reward.

3.3 CHESS Token Valuation Analysis

The agreement generates revenue through fees and revenue commissions, including:

Fund of Funds management fee: 1% per year for BTCB and ETH funds, 2% per year for BNB funds

Queen Creation: 0

Redeem fee: 0.2%

Split fee: 0

Merge fee: 0.1%

AMM pool: 0.1%

Income commission: 20% BNB node staking income, 10% ETH node staking income

Different from traditional finance, DeFi is a growing and very young industry. On the one hand, there is the explosive growth of data, and on the other hand, there are extremely fast iterative updates in the industry. Therefore, there is currently no perfect valuation system to study and judge. However, for DeFi projects, project market value and TVL are important indicators for judging market value, so the following focuses on these two indicators and compares them with other DeFi project data to conduct a valuation analysis of Chess.

Data shows that the total supply of CHESS tokens is 300,000,000, and as of the end of March, the circulating supply was approximately 117,099,737, accounting for 39%. The current CHESS price is $0.258 and the token’s market cap is $30,203,840, which is $77,373,468 when fully diluted. The 24-hour trading volume is $2,943,074. The CHESS agreement has a TVL of $57,561,773.

The price-to-earnings ratio is one of the most basic financial measures and is often used to identify undervalued stocks or to examine a stock's profitability. Similar to the price-to-earnings ratio, the ratio of market value to 24-hour transaction volume in DeFi projects - NVT (Network Value to Transaction), can also reflect its investment value. Compared with the price-to-earnings ratio, NVT does not have compatibility issues caused by cross-industry, so even cryptoassets from different projects can be compared together. The figure below is an overview of NVT data produced based on the data of each token on March 1. It can be seen from the figure that the current NVT value of CHESS token is 6.56, which is at a low position. The ratio of leading DeFi projects such as AAVE is above 20. The lower the value, the lower the market valuation. Considering the launch time of the Tranchess project and the update time of the V2 version, the market actually entered a bear market as a whole last year, which to a certain extent indicates that the project has not yet fully developed or the market has not fully understood the potential value of the token.

In terms of TVL, TVL usually reflects market size and user participation. The CHESS protocol’s TVL once ranked third on the BNB chain, and is currently at an upper-middle level. Moreover, TVL is significantly higher than the market capitalization, indicating that most tokens are locked, which also indicates high user participation. The current ratio of market capitalization to TVL, that is, Mcap/TVL, is approximately 0.57. Usually a value less than 1 indicates that it is currently undervalued, which also indicates that Tranchess is a promising cryptocurrency protocol.

To sum up, the valuation analysis of the CHESS token shows that the market valuation of the token is relatively low, but its circulation value and TVL are high, which represents the higher token value and protocol market size in actual transactions.

04 Risk Classification Agreement Competitive Product Analysis

Tranchess operates both pledge nodes and hierarchical funds established on the basis of pledge nodes, achieving the composability of DeFi through cross-track integration. At present, most of the other on-chain hierarchical fund tracks were created based on lending protocols before the merger of Ethereum PoS. Since they do not use PoS pledge to provide them with a risk-free rate of return, they have no advantages in interest rates and risk control compared to Tranchess. . These include Saffron Finance, BarnBridge and 88mph. These protocols have had glorious pasts. Barnbridge reached $186 million in liquidity mining deposits a few weeks after it went online. Saffron went online two weeks after it, and TVL quickly reached 5,800. Ten thousand, the limelight lasted for a while. But now, one year after it went online, the Saffron page shows that TVL is only 300,000 US dollars, and the APR data can no longer be displayed. The project team is building a new Uniswap-based fixed income product. BarnBridge currently has 1.23 million TVL left, one product ( DAI on ETH) and 17 active users. By simply sorting out the design of each protocol, we try to analyze the reasons and countermeasures, and explore the possibility of the outcome of market competition.

4.1 Introduction and development status of competing products

Saffron

Saffron Current Situation

Saffron Finance is a peer-to-peer risk trading protocol that allows liquidity providers to stake crypto assets on its platform, providing customized risk exposures based on their required risk and return expectations. The Saffron protocol will automatically connect liquidity to third-party DeFi lending platforms.

In other words, Saffron allows users to share deposit income under different risk levels. Users who bear low risks can get fixed-rate returns, and users who bear high risks can get higher returns when the overall returns are higher. The overall income is less than expected. At this time, low-risk users need to subsidize fixed returns and record losses. In addition, Saffron subsidizes liquidity providers by the LP amount through the SFIs issued.

BarnBridge

BarnBridge status quo

BarnBridge offers interest rate swaps that allow any variable yield to be converted to a fixed rate. It allows users to execute simple interest rate swaps, with one party taking on more variable risk and the other taking on a fixed rate of return (sBond pool, low risk but fixed return; jTokens pool, high risk but unpredictable return).

The subsequent SMART Alpha upgrade allowed risks to be further subdivided. Users with low risk appetite can sell part of the downside risk to users with high risk preference to cover the downside risk of principal fiat currency at the expense of potential returns.

Then BranBridge launched SMART Exposure. Portfolio asset users can set specific ratios through SMART Exposure and automatically calibrate the balance ratio between assets based on price fluctuations.

Subsequently, BarnBridge became a closed pool, and deposits could not be withdrawn during the deposit period and withdrawal period, but new asset tokens minted by depositing the amount during the minted deposit period could be used to pledge loans from the relevant lending agreements.

88mph

88mph current situation

88mph is a regular fixed rate yield product that acts as an intermediary between users and third-party variable rate loan agreements, providing the best fixed rate of return for your capital, with deposit terms up to 1 year, in some categories of deposits, the protocol uses tokens to subsidize interest rates.

88mph offers two categories of products:

Fixed Interest Bond (FIRB) Currently, 88mph supports multiple token deposit services (including Dai/sUSD/USDC/UNI/yCRV, etc.). 88mph deposits deposits into Compound/Aave/Harvest/YFI to earn income in the form of fixed interest. Paid to depositing users.

Floating interest bonds (FRB) If the user expects the overall market interest rate to remain at a high level, he only needs to bear fixed interest debt with a small amount of funds to obtain excess floating interest; otherwise, when the market interest rate is low, floating interest bonds are held The investor will also suffer losses as a result.

4.2 Summary of competitive projects

Problems with projects on the same track

At present, the operating conditions of the three protocols of the same type are not good. We can see that these three protocols are all based on simple lending protocols. They use interest rate swaps to combine the variable rate of return in the lending market with the fixed income of the users. In exchange for interest rates, the deposit interest of the lending agreement is divided into two parts, one part is low risk and low fixed income, and the other part is high risk and high return. This actually faces the following problems:

The interest rate on deposits in the lending agreement, which was the cornerstone of the previous project, was not high. Even now that the lending agreement benefits from LSD’s circular lending pledge, the interest rate in the lending agreement is not high. Before LSD, the borrowing demand was more based on headcount. Mining, high-risk investments and other short-term behaviors, the lender is not stable, the borrowing interest is lower, the construction of tiered products at low interest rates, whether it is split into two products, or the government will bear the inferior tier , The low interest rate situation has resulted in little room for maneuver in product design, and it is difficult for a clever woman to make a meal without rice. The founder of BarnBridge also admitted that DeFi fixed income has not taken off so far, and it is for this reason.

Most tiered funds require assets to be locked up for a long period of time. A lot can happen in the crypto world in the short term, which is itself a relatively high-risk activity, while most existing fixed income protocols offer terms of 90 to 180 days, and some even For up to a year, it is inconvenient for users to exit. Even in some agreements, user entry requires specific vault opening hours, which is also inconvenient.

Lack of liquidity. Most fixed income positions lack secondary market liquidity, and users cannot use them as collateral or quickly convert them into other assets.

Tranchess' solution

Tranchess provides new solutions based on existing problems, optimizing user returns of hierarchical funds and reducing user risks.

Tranchess's tiered fund is built based on LSD. It takes advantage of the fact that LSD pledge interest is much higher than the deposit interest in the lending agreement, making its income level more attractive than previous on-chain tiered funds. In addition, Tranchess is not simply It uses interest rate swaps to design structured products, and also takes advantage of the high interest rates of LSD to allow high-risk parts to increase leverage through internal borrowing, while low-risk parts obtain fixed income by providing loans to high-risk parts. At the same time, the two share the interest income of LSD in a certain proportion. This is a structured product based on LSD with better stability and higher user benefits.

The two structured products built by Tranchess both built a liquidity pool within the protocol, and users can enter and exit at any time, reducing user risks and improving the liquidity of pledged assets.

Tranchess' structured products are all built based on the U standard. Users can purchase them using USDC, and users can intuitively see the profit and loss of assets.

Final analysis of market competition

Classified funds essentially classify and sell investment products according to characteristics such as risk and maturity to meet the investment needs of different users. In the sales of wealth management products in the traditional financial field, fixed-income products are an important part of asset allocation, especially in economic downturns. At the end of 2021, in JPMorgan Chase’s managed asset structure, liquidity, fixed income, equity, The proportions of diversified and alternative assets were 28.2%, 20.7%, 23.2%, 23.2% and 9.9% respectively. In the crypto field, some investors often consider the risk of underlying volatility, and fixed-income assets allow risk-averse investors to participate in liquidity mining and cryptocurrency investment with minimal risk, while high-risk tiered funds Some can meet the needs of investors pursuing high returns.

Based on the above analysis, it can be inferred that the market will have the following trends:

The birth of liquidity collateral derivatives will bring more capital inflows: Since Ethereum has switched to PoS, liquidity collateral derivatives have provided higher low-risk interest rates for the entire DeFi industry, which will bring more capital inflows. Lay the foundation.

Hierarchical foundations have become one of the main targets for capital allocation: capital will be allocated in a balanced manner, taking into account returns and risk control, while fixed income products will become one of its main allocation targets, and the stability of fund operations will also become its main consideration. factor.

The model of tiered funds will be more diversified: DeFi is highly composable, and more tiered funds based on LSD will be born in the future to meet the investment needs of different users, such as LSD+leverage, LSD+options, etc.

As a pioneer in this field, Tranchess has seen no major risks in its economic model and protocol security during its two years of operation. At a time when LSD is just beginning to gain momentum and capital attention is being attracted, there is also a greater opportunity to develop in the on-chain hierarchical fund track. Be a leader.

05 Tranchess development prospects

5.1 Tranchess development prospects

Tranchess has advantages in both model innovation and risk control. With the improvement of macro liquidity and the development of the LSD track, Tranchess will have greater growth potential.

1. Simple risk classification model

In order to meet the risk preferences of different groups of people, DeFi has developed a risk grading model. The underlying assets of the competing products reviewed above mostly use stable coins, and the main source of income is borrowing. Tranchess tracks large categories of assets, such as BTC, ETH, and BNB, which have growth potential compared to stablecoins and a certain degree of stability compared to general blue-chip assets. For users seeking low risk, Tranchess’ Bishop token can provide higher risk-free returns. For users seeking high risk, Tranchess’ Rook token provides a simple way to configure leverage and maintain positions without the need to replenish margin when the market moves downward.

2. The bull market is good for the growth of Tranchess

Tranchess's fund of funds mainly tracks asset prices. When asset prices rise or fall, the leveraged tokens in the sub-funds will amplify gains or losses. According to the development rules of tiered funds in traditional finance, tiered funds are the hottest investment variety in the market during a bull market, and the scale of tiered funds will also grow rapidly. This is due to the greater appeal of the leveraged token Rook when asset prices rise. The path behind purchasing Rook through instant exchange is to mint Queen tokens and split them into Rook tokens, which allowed the size of the fund of funds to grow rapidly during the bull market. In 2023, as macro liquidity is expected to stop tightening, the crypto market may usher in a recovery, which is undoubtedly a good thing for Tranchess.

3. Providing basic income with PoS pledge

With the implementation of the Ethereum Shanghai upgrade, ETH staking will usher in greater growth, and staking income will also bring a large inflow of funds to DeFi, further promoting the innovation of the DeFi model. Tranchess joining the LSD track has greatly expanded the imagination space of such products, and also enriched the possibility of LSD users' income combination; at the same time, the integration of Tranchess structure and LSD has also expanded the imagination space of Tranchess itself. If it can Maximizing your own strengths may bring more possibilities in future cooperation with various projects.

4. Risk control

As a structured financial product, the model of hierarchical funds is somewhat complex and requires protocol builders to have strong financial skills. Judging from its team background, information transparency and operations over the past two years, Tranchess has relevant strengths.

5.2 Tranchess risk points

The risk of de-anchoring between the underlying and Queen Token LP (for example: ETH/qETH).

Risk of rapid devaluation of Rook tokens.

At present, qETH is small in scale, market development expectations are unclear, and there is the risk of penalties caused by the default of pledge nodes.

policy risk

The crypto world has developed rapidly since the emergence of Bitcoin, but regulatory issues have been a difficulty in its development. In recent years, the U.S. Securities and Exchange Commission (SEC) has begun to understand and explore how to regulate the crypto world. Although still in its infancy in terms of regulation, regulatory trends in the field of cryptocurrency and DeFi (decentralized finance) have begun to emerge.

The Howey test is a legal test used to determine whether a transaction is considered a security and is also one of the important indicators for judging the compliance of DeFi projects. If a DeFi project or asset meets the four elements of the Howey test, it may be considered a security and needs to comply with securities laws.

From the previous BTC to Ethereum to the recent NFT and stablecoin regulation, the SEC is strengthening supervision to ensure compliance. While it currently seems likely that Tranchess Protocol meets the four elements of the Howey test, there are currently no cases of scrutiny for DeFi. On the other hand, the DeFi project itself still needs to be further strengthened in terms of security and compliance. Therefore, from the perspective of the sustainable and steady development of the DeFi industry and the interests of investors, DeFi projects need to formulate more comprehensive and effective compliance measures. However, supervision is not arbitrary restrictions, nor is it a political tool. Reasonableness, legality, and compliance are the key to promoting the industry. prerequisite for development.

This report is provided by SnapFingers Research for specific client use only. This report is only released under the permission of relevant laws, and the information provided comes from public sources. SnapFingers Research endeavors to ensure that the information is accurate and complete but does not guarantee its accuracy or completeness.

The complete views of this report should be based on the complete report published by SnapFingers Research. The views and information published by any media, social networking sites, etc. are for reference only.

The information, opinions and speculations contained in this report only reflect the judgment of SnapFingers Research on the day when this report is released. The relevant analytical opinions and speculations may be changed without notice based on subsequent research reports. Investors should Follow yourself for any updates or modifications.

The information or opinions expressed in this report are for reference only and do not constitute investment advice to anyone. Investors should not use this report as the only reference factor for investment decisions, nor should they think that this report can replace their own judgment. SnapFingers Research or its affiliates do not promise that investors will make profits, will not share investment income with investors, and will not be responsible for No one is responsible for any losses caused by the use of any content in this report.