Currently, #区块链 technology is becoming increasingly mature, the application of stablecoins is also becoming more widespread, and crypto assets are evolving from 'speculative assets' to useful 'production tools'. Meanwhile, #Web3 is no longer a distant future; it is gradually entering our everyday payments, inter-enterprise settlements, and digital consumption domains.

According to the Chainalysis 2024 report, the number of people holding crypto assets worldwide has exceeded 300 million. Among them, about 60% have started using cryptocurrencies for everyday shopping or cross-border transfers. This clearly indicates that the use cases for #加密资产 are becoming increasingly diverse.

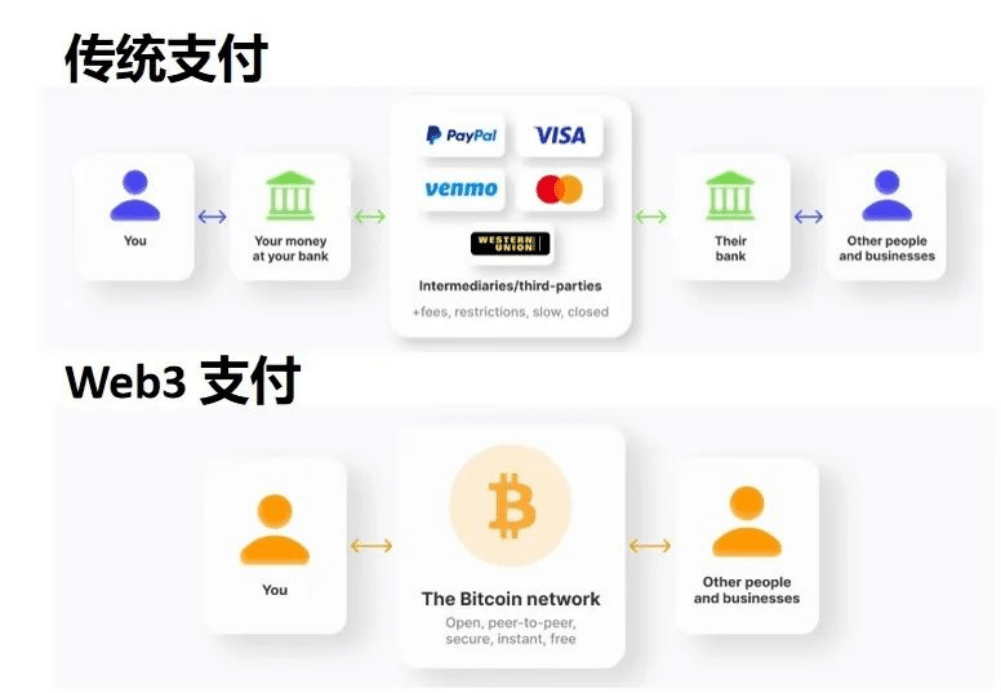

However, some basic concepts of #Web3支付 itself, such as wallets, public chains, transaction fees, and on-chain data, remain complex and unfamiliar to most ordinary people and merchants. To truly achieve the integration of Web3 with the real world, the key lies not in the chain itself, but in the 'bridge'.

It is against this backdrop that a type of financial payment company focused on bridging Web2 and Web3 has rapidly emerged. They are changing our financial system in various aspects such as payment models, user experiences, and product technologies, and have become an important force driving the real-world application of crypto assets.

Widespread adoption of crypto payments: as easy as swiping a card

In real life, ordinary consumers are not willing to accept a higher operational threshold just because transactions occur 'on-chain'. On the contrary, consumers only care about whether using crypto assets is as convenient as swiping a card.

Therefore, payment companies bridging Web2 and Web3 need to hide the complexity of crypto assets 'in the background'—while providing the same simple experience as traditional Web2 payments in the foreground. Behind this is a deep integration of various technologies such as multi-chain wallets, secure custody, security risk control, and payment channels, enabling 'on-chain wealth' to achieve 'seamless payment' in the real world.

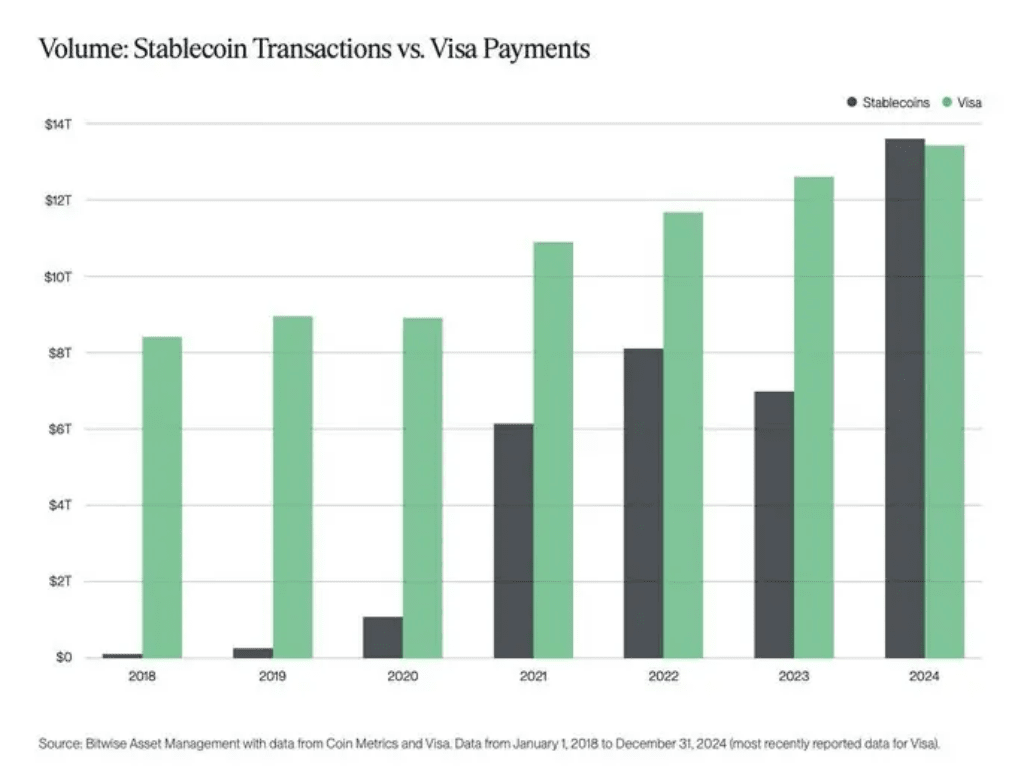

According to Cointelegraph data, the trading volume of stablecoins surpassed Visa's payment volume for the first time in 2024, fully demonstrating that crypto payments are rapidly gaining popularity. The core value of this service is not only to allow users to 'spend cryptocurrencies', but more importantly to enable merchants, platforms, and developers to easily integrate crypto payment functions without having to reconstruct an entire financial system on their own.

How to turn 'on-chain wealth' into 'real money': unlocking liquidity is key

Currently, many enterprises and individuals have already accumulated crypto assets through DeFi, GameFi, or Web3 projects, but the proportion of those that can be conveniently used for everyday payments or settlements remains very low. According to The Block 2024 research report, over 70% of crypto asset holders indicate that the lack of convenient payment channels is the main reason hindering their use of crypto assets.

The financial companies connecting Web2 and Web3 are significantly shortening the usage paths of crypto assets through means such as building cryptocurrency inflow and outflow, integrating enterprise accounts, and instant settlements (T+0). This liquidity mechanism gives on-chain wealth real-world value and is one of the core drivers of the Web3 economy.

For example, the financial innovation platform Interlace, which bridges Web2 and Web3, supports users in real-time exchanges between stablecoins such as USDC and USDT and fiat currencies through features like MPC wallets, fiat accounts, and CryptoConnect, enabling consumption, payroll, or cross-border transfers, thus creating a complete 'asset to payment' channel. Currently, this solution has been adopted by multiple Web3 enterprises, exchanges, and business travel platforms. For instance, Interlace assists a large Southeast Asian Web3 content platform in converting crypto revenue into fiat currency and distributing it to global creators through corporate cards, significantly enhancing funding efficiency and user stickiness.

The cornerstone of enterprises embracing crypto: compliance brings trust

In the payment field, compliance and trust are prerequisites for business expansion. In the past, the crypto industry was often plagued by issues of 'unclear regulation and high compliance costs'. Many enterprises and institutions, even if they wanted to try crypto services, often hesitated due to legal risks. According to Deloitte's 2024 crypto compliance survey, over 80% of institutional users regard compliance capability as the primary criterion for choosing a crypto payment service provider.

Therefore, Web3 payment companies need to not only understand blockchain technology but also be proficient in compliance regulations. Additionally, the current regional nature of industry regulation requires these financial companies to hold licenses from multiple countries and regions, support enterprise-level KYC/KYT processes, meet anti-money laundering (AML) compliance, and implement related risk control strategies to create a secure and compliant path for enterprises.

Taking Interlace as an example, it has currently obtained financial regulatory licenses in multiple locations including the United States, Hong Kong, and Lithuania, holding a compliance matrix that includes enterprise KYC, on-chain monitoring, and AML compliance processes, thus reducing the entry costs for enterprises accessing crypto services. Currently, Interlace has partnered with multiple Web3 wallets, crypto exchanges, and other institutions to provide on-chain deposit and withdrawal, as well as crypto card services for real payments/consumption, helping users expand their consumption scenarios beyond Web3 while ensuring asset security and compliance.

The 'fast track' for traditional business to enter Web3

For traditional e-commerce, content platforms, freelance platforms, or gaming companies, whether to integrate crypto is no longer a matter of willingness but rather a question of 'is there a mature infrastructure'.

According to McKinsey's 2024 report, over 65% of large enterprises plan to integrate some form of crypto payment service within the next two years, and 'lack of mature and user-friendly infrastructure services' is the biggest obstacle. Financial companies bridging Web2 and Web3 are playing this interface layer role: providing enterprise accounts, card services, fund distribution interfaces, stablecoin settlement solutions, and even quickly deployable white-label card APIs. Some platforms can achieve rapid customization of cards within 1-2 weeks, integrating various payment scenarios such as Apple Pay, Google Wallet, and ATMs, providing a practical path for Web2 platforms to expand their Web3 capabilities at low cost. These services not only solve the 'technical feasibility' issue but also reduce 'organizational costs' and 'compliance concerns', allowing more previously neutral or hesitant companies to take their first step.

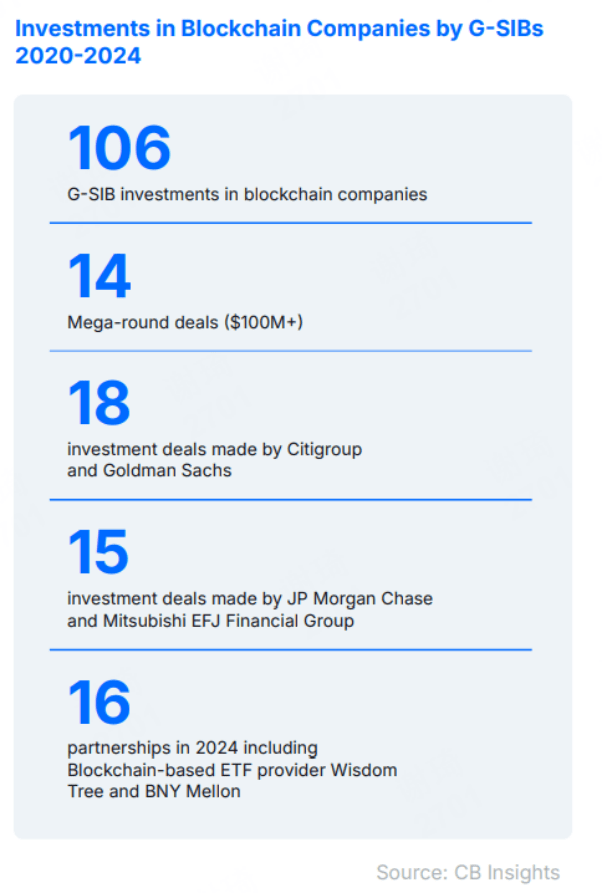

Observing platforms represented by Interlace, we find that they are evolving from 'crypto payment tools' to 'infrastructure for the new generation of financial systems': providing a complete service matrix including card services, fund inflow and outflow, account management, asset appreciation, and compliance clearing. From this perspective, they are not just simple 'connectors', but rather the prototypes of future banks and payment networks. They make 'on-chain finance' widely usable and integrate 'crypto assets' into enterprises' financial systems. According to a joint report by Ripple and CB Insights, from 2020 to 2024, global traditional banks have invested more than $100 billion in blockchain and digital asset infrastructure, with about 25% of the investment flowing to core infrastructure providers, significantly increasing market recognition.

Connecting Web2 and Web3 finance: bridging and paving the way, worth looking forward to

Web3 is not a replacement for traditional finance but a restructuring of financial structures. In this new system, these 'bridge builders' are not temporary transitional roles, but rather important builders. They connect user-friendly front-end experiences while deeply integrating back-end compliance capabilities and on-chain assets. In a sense, they are constructing a financial system that is faster than 'traditional banks', more robust than 'crypto wallets', and more compliant than 'exchanges'.

Platforms like Interlace represent this new type of infrastructure. Their existence provides a low-friction, high-efficiency, and trustworthy 'channel' for all enterprises, platforms, and users wanting to embrace Web3. This path is worth paying attention to and even more worth looking forward to.