Ethereum, as a leading smart contract platform, has entered its second decade, evolving from a proof-of-work (PoW) blockchain into a wide-ranging economic network based on a proof-of-stake (PoS) consensus mechanism. By 2025, Ethereum will secure hundreds of billions of dollars in digital assets, settling millions of transactions daily, becoming a pillar of decentralized finance (DeFi), non-fungible tokens (NFTs), and an increasingly rich ecosystem of tokenized real-world assets (RWAs). Over the next decade, Ethereum's roadmap envisions significant protocol upgrades to vastly enhance scalability and security while solidifying its role as a yield-generating asset and financial layer.

This report provides a 10-year outlook analysis for Ethereum, focusing on technological developments, economic and competitive dynamics, DeFi/NFT infrastructure, institutional adoption, regulatory trends, and key metrics.

Technical roadmap: Ethereum's scaling for the next decade

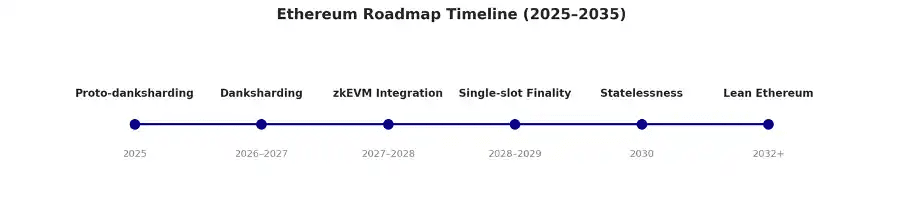

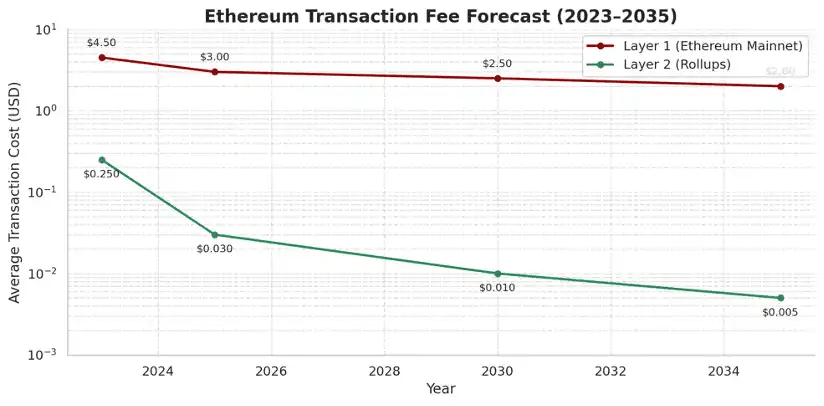

The core of Ethereum's technological roadmap for 2035 is to significantly increase throughput and user experience without compromising security or decentralization. Following the successful transition to the PoS consensus mechanism (the Merge) and the Shapella upgrade (enabling staking withdrawals from 2023), the network is currently undergoing a series of upgrades aimed at enhancing scalability. A key focus is danksharding, a redesigned sharding method that emphasizes data availability for Layer 2 aggregation. Unlike the original concept of introducing 64 independent 'shard chains,' danksharding distributes the storage burden of aggregated data across all nodes via data blobs, reducing the storage requirements for each node while increasing throughput. A temporary step proto-danksharding (EIP-4844) was deployed in the 2024 Dencun hard fork to introduce blob-carrying transactions and significantly lower aggregation fees. By the end of 2025, Ethereum plans to increase blob data capacity (e.g., doubling the number of blobs per block) to further reduce costs for Layer 2 (L2) transactions.

Another priority is improving the execution engine. Ethereum developers are exploring next-generation virtual machines based on RISC-V architecture, which could replace the EVM and achieve 3-5 times the smart contract execution efficiency with a 50-70% reduction in gas costs. This new execution environment is expected to be gradually rolled out between 2025 and 2030, maintaining EVM compatibility while leveraging modern hardware acceleration for better performance. Meanwhile, Ethereum's Layer 1 (L1) chain could directly integrate zero-knowledge EVM (zkEVM) proofs into its protocol. By 2025-2026, researchers aim to verify 99% of blocks within 10 seconds using succinct zero-knowledge (ZK) proofs. This could significantly enhance security and enable privacy-preserving transactions, giving institutions more confidence (for instance, ZK proofs could ensure compliance and privacy for financial transactions on Ethereum).

Data sharding combined with a zero-knowledge proof supported execution layer lays the groundwork for exponential throughput increases. In fact, Ethereum's long-term goals include achieving 'Beast Mode' performance of 1 Giga Gas per second on Layer 1 and 1 Teragas on Layer 2—several orders of magnitude higher than current capacity. The vision for Ethereum 3.0 is to integrate zkEVM rollups with sharding technology by 2027-2028 to reach speeds of millions of transactions per second (TPS) while reducing data costs by 99%, effectively preparing the network for global usage at Web3 scale.

Equally important is the upgrade of Ethereum's consensus and user experience. Plans are in place to implement single-slot finality, allowing blocks to finalize in just one slot (around 12 seconds) instead of the current 15 minutes, which will enhance security against reorganization and provide more convenience for applications. The experience for validators will also improve: by 2025-2026, Ethereum intends to lower the minimum staking requirement from 32 ETH to (potentially) 1 ETH and optimize validators' duties for lighter hardware. This can significantly increase the number of validators and promote decentralization. Notable proposals aim to raise validators' annual yield from about 4-6% to 6-8% by adjusting incentives, although in practice the yield percentage depends on the total amount of staked ETH (more stakers dilute protocol issuance) and fee revenue.

Ethereum's roadmap also encompasses account abstraction, thus natively supporting smart contract wallets. Starting with the 2025 Pectra upgrade, users will be able to attach smart contract logic to externally owned accounts (EOA), unlocking features like batch transactions, sponsored fees, and social recovery wallets. This development blurs the lines between user accounts and contracts, enhancing the security and usability for mainstream users. Furthermore, statelessness achieved through Verkle trees and historical record expiration features (Verge and Purge milestones) will streamline the chain's state size, allowing even resource-constrained devices (like smartphones) to verify the chain without storing its entire history.

In summary, Ethereum's technological development trajectory over the next decade is ambitious: cheaper transactions, higher throughput, faster finality, and more user-friendly wallets—while enhancing security against evolving threats.

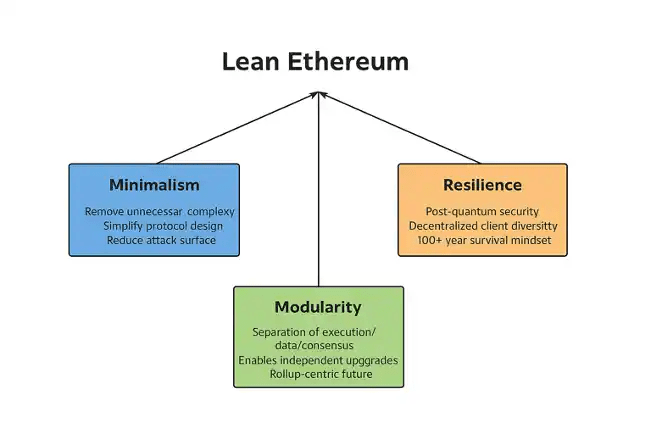

Ethereum's Lean vision: Resilience for the next century

In July 2025, Ethereum's core researchers introduced a strategic shift called 'Lean Ethereum,' redefining the long-term roadmap around maximum resilience and modular simplicity. This vision articulated by Ethereum Foundation researcher Justin Drake essentially represents a fortress-like approach to ensure that Ethereum can 'withstand any challenge' (from nation-state attacks to quantum computing) and 'achieve all scaling' (avoiding unnecessary complexity). Lean Ethereum is an evolution of the early concept Beam Chain, which was a comprehensive overhaul of the consensus layer, now expanded into an overall redesign of Ethereum's core layers (consensus, data, execution) based on three pillars: minimalism, modularity, and resilience.

In 'fortress mode,' Ethereum prioritizes decades of durability. This means strengthening the network to withstand even theoretical threats, such as quantum attacks. For instance, the Ethereum community is evaluating whether to abandon cryptographic primitives like BLS signatures and KZG commitments (used for today's staking and data availability) in favor of simpler, hash-based alternatives that are resistant to quantum attacks. The philosophy is to minimize external dependencies: if a component is not absolutely necessary, it should be simplified or removed to reduce the attack surface. At the same time, Ethereum's development process itself has evolved into a decentralized, multi-team collaborative platform, which core developers believe is key to maintaining resilience.

Since its launch in 2015, Ethereum has maintained 100% uptime, withstanding countless attacks and major upgrades without interruption to block production. As pointed out by an Ethereum core engineer, this reliability has built trust and will continue to do so. The 'lean' roadmap further reinforces this principle, planning for post-quantum cryptography, ultra-light clients, and diversified clients to ensure Ethereum thrives even in the face of the 'harshest adversaries' and exists longer than its creators.

At the same time, the 'Beast Mode' of Lean Ethereum recognizes that to maintain dominance, the protocol must actively scale performance while remaining decentralized. The ideal throughput targets mentioned above (1 Giga throughput per second on Layer 1) provide direction for how to achieve this goal:

Lean consensus means a streamlined beacon chain with near-instant finality and upgraded signature schemes.

Lean Data expands the original danksharding model using variable-sized blobs and post-quantum secure complex data availability sampling.

Lean execution envisions a minimized execution environment, potentially a RISC-V instruction set supporting SNARKs, which remains compatible with the EVM but has higher verification efficiency. Essentially, execution can be redesigned from the ground up to be more provable and lightweight.

These ideas align with ongoing work (like the zkEVM and RISC-V plans mentioned earlier) and suggest that by the early 2030s, Ethereum could have a very different underlying architecture.

Importantly, the Lean plan is now publicly tracked through a community-driven website (leanroadmap.org) to coordinate the R&D work of various teams. The Ethereum Foundation has not imposed a rigid roadmap but has provided guidance for the evolution of the protocol by articulating this vision, enabling it to far exceed the 2020s and move toward a 'century of security and scalability.' This transformation signals that Ethereum is entering a new stage of architectural maturity, with a focus not just on the next upgrade but on how to build a robust modular base layer that becomes critical infrastructure for generations to come.

For traders and investors, the 'Lean Ethereum' strategy conveys a message: the protocol is being built for longevity. The network may undergo years of restructuring (including progressive hard forks like the Glamsterdam in 2026 and subsequent hard forks) aimed at making Ethereum simpler, more secure, and better equipped to tackle unpredictable challenges. If this vision comes to fruition, by 2035, Ethereum will become a lean, highly scalable settlement layer, with most complexity abstracted into Layer 2 rollups—essentially a 'resilient layer' constituting the pillars of Web3 and global finance.

ETH as a yield asset and economic layer

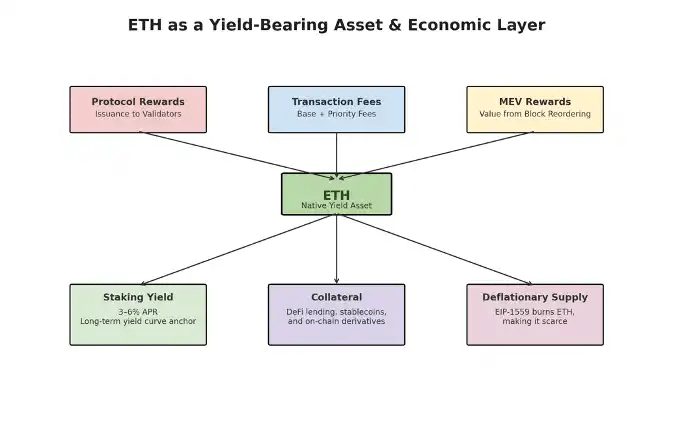

A significant feature of Ethereum's transition to PoS is that ETH can now generate yields for holders who participate in staking and maintain network security. This staking yield effectively makes ETH the first mainstream crypto asset with bond-like or dividend-equivalent native yields, establishing ETH's status as the de facto benchmark yield in crypto economics. By mid-2025, the annualized staking reward yield for validators hovers around 4%-5%, comprising multiple components:

New ETH issuance (protocol inflation)

Priority fees ('tips')

MEV extraction rewards

For example, by the end of 2024, the base issuance yield will be around 2.8%, with approximately 22% of the ETH supply staked, plus about 0.5% from fees and 0.5% from MEV, resulting in a total annual rate of about 3.8%-4%. These numbers will adjust with changes in participation—if the amount of staked ETH increases, the issuance share for each validator will decrease, thus lowering yields; while increased network activity (higher fees/MEV) can boost yields. It is noteworthy that Ethereum's monetary policy includes a 1.5% annual minimum issuance floor (only achievable if 100% of ETH is staked and transaction volume is zero), meaning there will always be some benchmark yield to ensure the blockchain's security.

From an investment perspective, ETH yields have begun to emerge as the 'risk-free rate' of the crypto ecosystem. In traditional markets, U.S. Treasury yields set the yield benchmark denominated in dollars. Similarly, the yield from staking ETH is increasingly viewed as a benchmark capital cost for DeFi. Researchers at ARK Invest believe ETH is acquiring bond-like attributes: investors can hold ETH and stake it for predictable returns, or use liquid staking tokens to earn yields while maintaining liquidity. This dynamic is influencing other networks, as many alternative Layer 1s must offer higher yields or incentives to attract capital, given ETH's relatively low-risk profile and deep liquidity.

ETH staking and yields

In fact, Ethereum's staking rates and yields may become a benchmark for the crypto financial yield curve. Lending rates in DeFi are typically priced based on staking yields (as staking ETH represents an opportunity cost), which is one example of this influence. Some analyses suggest that ETH staking yields could even guide expectations for economic conditions, similar to the influence of U.S. Treasury yields on macro prospects. For instance, when on-chain transaction fees (and staking rewards) surge, it may indicate bubble activity and high demand for block space—an example of a crypto-native economic indicator.

Crucially, after EIP-1559 (implemented in 2021), Ethereum's design not only makes ETH yield-bearing but also potentially deflationary, reinforcing its status as a unique economic asset. Under EIP-1559, a portion of each transaction fee (the base fee) is burned. During peak usage, the burn rate may exceed the issuance rate of staking rewards, resulting in a decline in the net supply of ETH (as seen during NFT and DeFi booms). This 'ultrasound money' dynamic means that ETH holders benefit from both yields and value appreciation through scarcity.

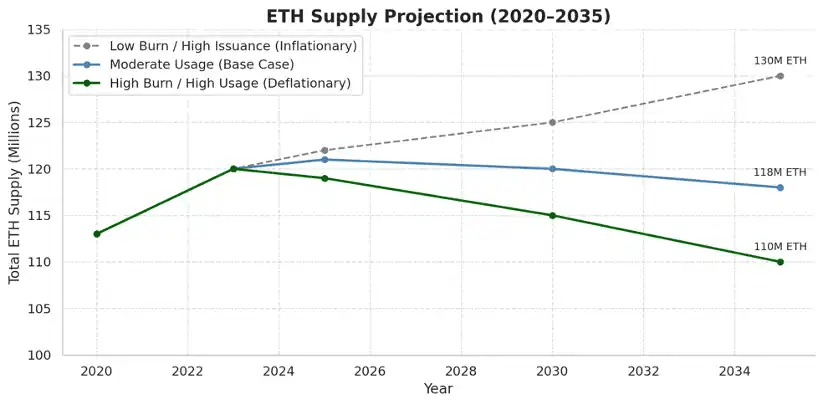

For instance, network revenue (converted into fees burned plus MEV) is expected to grow significantly. A detailed valuation model from VanEck predicts that by 2030, Ethereum's annual network revenue could reach $51 billion, up from $2.6 billion in 2023. If this growth materializes, a significant portion of that revenue will be burned, increasing the scarcity of the remaining supply. VanEck's baseline scenario anticipates that due to the offsetting effects of issuance and burning, the total circulating supply of ETH will remain relatively stable (around 121 million ETH by 2030, roughly similar to 2023 levels). In a scenario of extremely high fees during a bull market, by 2030, ETH's supply could even dip to around 113 million. This means that Ethereum essentially becomes a platform similar to stocks, as token holders can derive value from network use—contrasting sharply with Bitcoin's fixed supply but zero yields.

ETH as a yield-bearing token

For traders and exchanges, the yield characteristics of ETH carry multiple implications. It introduces an arbitrage trading element for holding ETH: investors shorting ETH must pay staking yields (similar to shorting dividend-paying stocks), while long-term holders can gain returns that offset some volatility. This often encourages holding ETH, and as more investors lock their tokens in staking contracts, the circulation of tokens on exchanges will decrease. For example, following the Shanghai upgrade in April 2023 (allowing withdrawals), staking participation surged: by 2024, around 20%-25% of ETH will be staked, and by the end of the decade, this figure may climb to 40% or higher. If the minimum staking threshold is lowered to 1 ETH, we could see millions of small holders stake their ETH, further boosting participation rates. Higher staking rates would reduce circulating supply, potentially increasing price stability (or upward pressure), but this also means exchanges must innovate to maintain high trading volumes, even as the number of tokens available for speculative trading decreases.

Many exchanges have responded by launching liquid staking products or derivatives that allow users to stake ETH through exchanges while still trading their corresponding tokens. Furthermore, an ETH yield market may emerge on exchanges—such as futures or swap contracts tied to staking yields (similar to interest rate swaps), which traders can use to speculate on or hedge against changes in ETH yields.

Overall, ETH as a yield-generating asset solidifies its status as a key economic player in the crypto industry, comparable to reserve assets underpinning DeFi, serving both as collateral and a source of returns.

Competitive Landscape: Ethereum vs. Other Layer 1 Chains

Although Ethereum dominates the smart contract platform space, it still faces ongoing competition from other Layer 1 blockchains pursuing higher performance or specific niches. The multi-chain landscape may persist over the next decade, with Ethereum striving to maintain its preferred settlement layer status while competitors challenge it on throughput, cost, or community appeal.

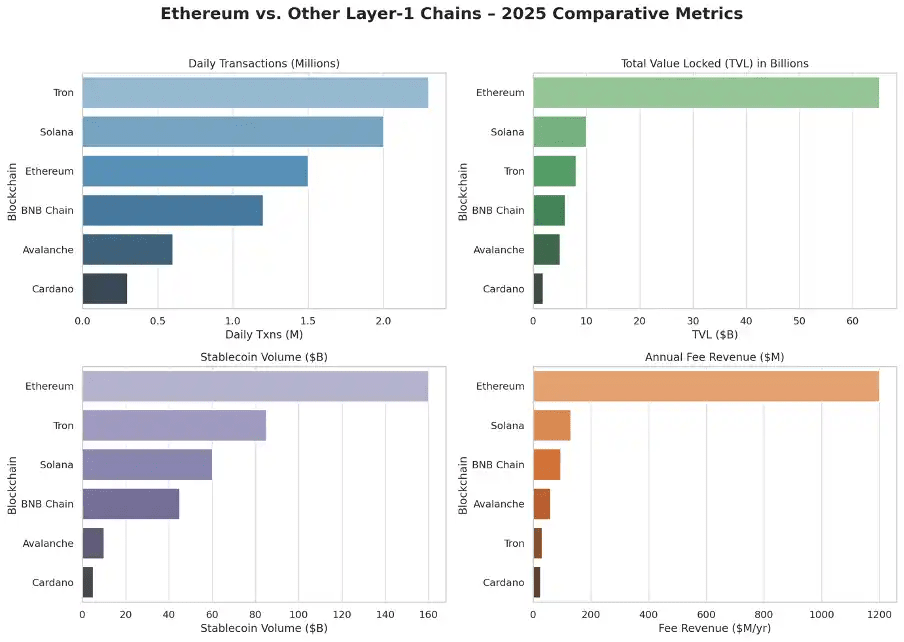

As of 2025, Ethereum continues to lead on numerous fundamental metrics—it has the largest developer community and highest value secured. It is estimated that the Ethereum ecosystem (including Layer 2 and EVM-compatible blockchains) has 10,955 active developers each month, far exceeding any single competitor, indicating that Ethereum's network effect in developer talent is unparalleled. Correspondingly, Ethereum captures the largest share of total value locked (TVL) in DeFi and dominates the NFT market.

However, some competitors have already captured significant markets. For example, Solana, a high-throughput chain with unique proof-of-history consensus, once had on-chain activity that rivaled or even surpassed Ethereum. By mid-2025, Solana accounted for about 44% of the comprehensive 'on-chain activity' index (weighted by transaction volume, number of transactions, and fees), while Ethereum's share in that metric has been declining. This shift is partly due to the explosive growth of low-cost meme token trading on Solana (and specific applications driving high transaction volumes). Additionally, Solana's ability to process high TPS at low fees has attracted usage in speed-sensitive areas, such as trading and gaming. However, it is worth noting that much of Solana's surge is driven by short-term speculative activities (like meme coins), and maintaining this dominance requires expanding into more sustainable use cases.

Competing L1 platforms

Other Layer-1s focus on different trade-offs. BNB Chain (Binance Smart Chain) uses a centralized validator set to provide cheap, fast transactions, primarily supporting Binance's application ecosystem. It has a large user base (especially in gaming and simple DeFi), but relies on Binance's support. TRON (TRX), often overlooked in the West, has become a major player in stablecoin transfers (especially USDT) due to its extremely low fees and consistently ranks high in transaction volume and value transfer. In fact, TRON and Solana sometimes surpass Ethereum in raw transaction numbers or stablecoin throughput, although fee revenue is much lower (due to their low fees).

Cardano (ADA), Polkadot (DOT), Avalanche (AVAX), and Cosmos (ATOM) represent alternative approaches—from Cardano's research-driven slow roadmap to Polkadot's multi-chain sharding network, Avalanche's subnets, and Cosmos's interoperable zones. Individually, these projects cannot compare to Ethereum's DeFi or NFT activity, but they compete with Ethereum in governance, flexibility, and/or specific use cases. For instance, Avalanche's subnets allow institutions to run customized Layer 1s, while Cosmos supports multiple application-specific chains (like those for trading or gaming) that together form an alternative network. By 2030, a few of these chains may maintain robust ecosystems, forming a multicultural landscape composed of multiple Layer 1s, each serving different market segments or geographic user groups.

Ethereum's blockchain dominance

That is to say, Ethereum's strategic bet is on a rollup-centric scaling model, which effectively absorbs demand through L2 networks instead of shifting users to other Layer 1 chains. This approach leverages Ethereum's strongest moat: security and decentralization. We have already seen many so-called 'Ethereum killers' pivot to become complements to Ethereum. For instance, some alternative Layer 1s now offer EVM compatibility and even serve as data availability layers for rollups. Over 90% of smart contract developers work on EVM-compatible platforms, indicating that Ethereum's technological standard (EVM) even extends to competitors. The rise of L2 solutions (like Arbitrum, Optimism, zkSync, Starknet, etc.) has started to reclaim use cases that may have left Ethereum during high fee periods. By 2025, Ethereum's L2s will collectively handle a significant volume of transactions (often 5-10 times that of Layer 1) and continue to grow.

This means that while Solana or other solutions may lead in underlying throughput, Ethereum and its L2 architecture can achieve horizontal scalability. Binance Research projects that by 2027, seamless interoperation between Ethereum L1 and major L2s will likely unify cross-chain liquidity and reduce cross-chain friction by 90%. If realized, this means users may not need to leave the Ethereum ecosystem for cost or speed—they can operate on L2 while enjoying near-instant finality and very low fees, all while choosing Ethereum for secure settlements.

Ethereum's advantages

For Ethereum to withstand competition in the long term, the upcoming 'Beast Mode' upgrades (danksharding, zkEVM, etc.) are crucial. These upgrades will allow Ethereum Layer 1 to handle more data and serve as a high-capacity backbone for all Layer 2s. Of course, competitors' Layer 1s will not remain stagnant—e.g., Solana is planning its own upgrades (like a project named Alpenglow aimed at fundamentally reforming consensus and lowering validator costs), and new Layer 1s will emerge. But Ethereum benefits from a decade of real-world testing and community building. It has overcome the 'minimum viable decentralization' challenges (e.g., concerns over mining pool centralization or now over staking pool concentration) and is actively addressing these issues (encouraging solo staking, etc.).

Moreover, the Ethereum network's brand and Lindy effect attract institutional integrations that smaller chains find difficult to achieve. For example, almost all major DeFi protocols and stablecoins were first launched on Ethereum. Even projects on other chains often maintain Ethereum versions to gain liquidity. By 2035, Ethereum's competitive position may hinge on whether it can timely deliver on its scaling promises. If by 2020 Ethereum can provide a user experience comparable to Solana through L2 (fast and cheap), its network effects may overwhelm most potential competitors. If it fails to do so, we may see activity migrate to alternative L1s that optimize different priorities (some of which may not have launched yet).

As of mid-2025, there is evidence that Ethereum has declined in some metrics (like transaction share), but there are also signs that Ethereum is rebounding—despite the surge in Solana's activity, Ethereum still captures the majority of the total value locked (TVL) in DeFi and stablecoin liquidity, and its fee revenue—although less than its peak—still far exceeds that of smaller public chains. The next bull market cycle may be a true test, as it will reveal whether Ethereum's layered scaling approach can accommodate a new wave of users or whether competitors can genuinely replace its role. Traders should monitor on-chain adoption indexes: a report from Coinbase's institutional team indicates that Ethereum's share in meaningful activity is declining, highlighting that Solana and TRON are surpassing Ethereum on some revenue metrics. However, by mid-2025, Ethereum's trajectory shows an upward turn, with price and on-chain activity surging, marking a potential inflection point.

In short, Ethereum will enter the next decade as a Layer-1 leader, but not without challengers. Its ability to innovate and integrate new technologies (like zero-knowledge proofs) will likely determine whether it can maintain its lead in network effects or cede areas to specialized Layer-1s.

Institutional Adoption and Enterprise Use Cases

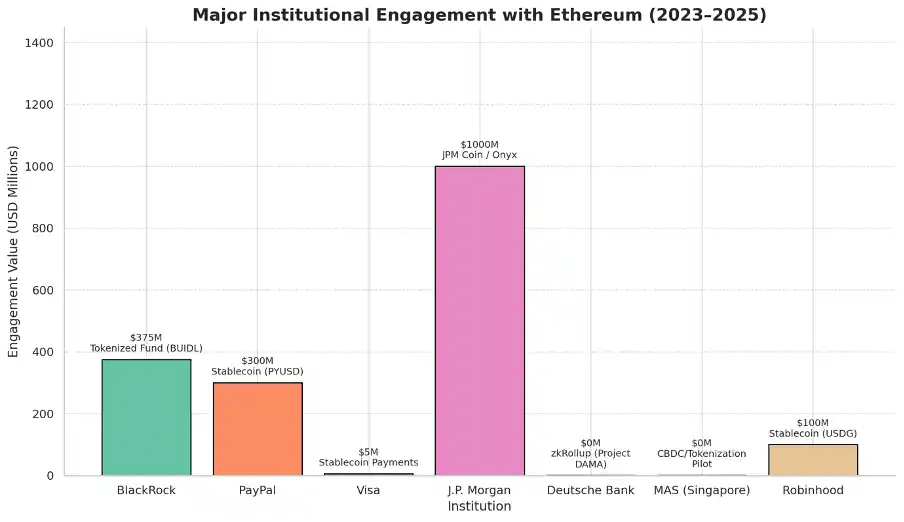

One of the most notable developments in recent years is the deepening involvement of institutional participants in the Ethereum ecosystem. Between 2023 and 2025 alone, we have witnessed household names in finance and technology launching Ethereum-based products or infrastructure pilots: such as BlackRock's tokenized fund, PayPal's stablecoin, Visa experimenting with stablecoin payments on Ethereum, and even central banks testing cross-border payments using Ethereum-compatible networks. Looking ahead to 2035, Ethereum is expected to become a key platform for enterprise and institutional use cases, spanning capital markets, supply chains, and Web3 gaming.

A clear indicator of institutional interest is the entry of major asset management firms and banks. In March 2024, BlackRock (the world's largest asset management firm) launched BUIDL, a tokenized money market fund initially launched on Ethereum. This fund provides investors with on-chain access to traditional off-chain products (money market yields) with the advantages of instant settlement and interoperability with DeFi. BlackRock's head of digital assets described it as 'wrapping traditional risk exposure in a crypto-native wrapper.' After launching on Ethereum, BlackRock expanded the fund to a few other networks (including three Ethereum L2s) to ensure broad accessibility. The fact that it started on Ethereum highlights its status as the preferred blockchain for tokenized securities. By early 2025, over 160 RWAs were issued on Ethereum, held by over 60,000 unique addresses—this number does not include stablecoins, indicating a thriving market for on-chain bonds, funds, and invoices. Consistent with this trend, six of the top ten protocols for RWAs are located on Ethereum or its L2.

Building Ethereum-based infrastructure

Financial institutions are not limited to issuing tokens: some are building Ethereum-based infrastructure. A notable example is Deutsche Bank's collaboration with ZKSync (Matter Labs) to develop a Layer 2 rollup, codenamed Project DAMA, aimed at institutional applications. This private rollup aims to create a scalable, auditable ledger that integrates with public and private systems—essentially a compliant global financial DeFi platform. The Monetary Authority of Singapore (MAS) has been coordinating such experiments (like the Guardian project), and the operation of Ethereum rollups by large banks like Deutsche Bank demonstrates confidence in the Ethereum tech stack in serious financial contexts.

Meanwhile, the CEO of the ZKSync team noted that institutions choose such solutions for 'privacy, scalability, and interoperability,' while still benefiting from Ethereum's security and ecosystem. Similarly, JPMorgan's Onyx platform (using a variant of Ether for interbank payments and issuing JPM Coin) and the Canton Network (an alliance using Daml smart contracts that can interoperate with Ethereum for on-chain finance) indicate that large consortia are satisfied with Ethereum's fundamentals, even in permissioned environments. By 2030, many banks and asset management firms may operate their own Ethereum rollups or sidechains, ultimately achieving finality on Ethereum's mainnet. This will create a center-radiating model centered around Ethereum, becoming the backbone of new financial market infrastructure.

Enterprises outside of finance are also adopting Ethereum. For example, Sony launched a universal Ethereum rollup (Soneium) in 2024, utilizing Optimism's tech stack to support a broad ecosystem of web3 gaming and entertainment applications. Large companies see blockchain as a way to enhance operational and/or product transparency and efficiency. Ethereum's robust toolset and developer base make it an attractive choice. By 2035, we may see supply chain coalitions using Ethereum L2 to track the provenance of goods, media companies issuing NFTs or fan tokens on a large scale, and tech companies implementing identity and authentication systems on Ethereum (for instance, Microsoft's experiments with decentralized ID involve Ethereum). The Enterprise Ethereum Alliance (EEA), established in 2017, continues to standardize enterprise-friendly scalability for Ethereum, which may lead to greater adoption in sectors like healthcare (for patient records), energy (for carbon credit trading), and government (for record-keeping and verification). Some countries are even testing central bank digital currencies (CBDCs) based on Ethereum-related technologies. For instance, Brazil's 2024 pilot CBDC utilized the Ethereum-compatible Hyperledger Besu network, and projects like the EU digital euro sometimes leverage Ethereum-derived technologies for prototyping.

Investment and regulatory landscape

A key catalyst for institutional adoption is regulatory clarity and investment products. By 2025, the U.S. is expected to have approved futures-based ETH ETFs, and a spot ETH ETF seems imminent. By 2030, jurisdictions such as the U.S., EU, and Asia are expected to launch multiple Ethereum spot ETFs, allowing pensions, endowments, and individuals to invest in ETH through traditional brokerage channels. In fact, some reports suggest that the initial phase of the ETH futures ETF in 2024 saw over $18 billion in inflows, indicating pent-up demand. Integration with Wall Street not only enhances Ethereum's liquidity and market capitalization but also further solidifies its status as an investable asset. When large asset allocators hold ETH within their portfolios (even indirectly through ETFs), they become stakeholders in the Ethereum ecosystem and are incentivized to support its growth—such as participating in governance or providing liquidity in DeFi.

In addition to investment, corporate finance adopting ETH is another emerging trend. Companies like SharpLink Gaming announced in 2024 that they would hold part of their treasury in ETH, viewing it as a reserve asset. Given ETH's yield and deflationary characteristics (which many fiat currencies lack), some companies may choose to allocate part of their cash reserves to ETH, akin to how companies hold BTC or gold.

Stablecoins, remittances, and bond issuance

A key area for enterprise use is stablecoins and payments. Businesses are actively using Ethereum to issue stablecoins (as noted by PayPal and Robinhood). Payment giants like Visa and Mastercard have been attempting to settle transactions via Ethereum, with Visa piloting automated payments using Ethereum L2, and Mastercard launching a blockchain-focused crypto credential standard. If regulatory conditions allow, banks could issue their own stablecoins on Ethereum (essentially tokenized deposits). For example, in 2023, ZA Bank in Hong Kong enabled retail customers to trade ETH and BTC directly with fiat currency, reflecting how crypto-friendly jurisdictions' fintech companies integrate Ethereum into banking applications. By 2030, stablecoins on Ethereum may be used for everyday business (possibly through an abstracted gas fee payment layer), and due to increased efficiency, businesses may frequently use stablecoins for B2B settlements, payroll, and more.

Institutional adoption of Ethereum is multifaceted and rapidly growing. Ethereum is no longer just the domain of crypto startups; it is part of the strategic roadmap for the world's largest financial and technology institutions. The network effects brought by this adoption are profound: as more blue-chip participants build on or use Ethereum, it solidifies Ethereum's position as the primary settlement layer of the new digital economy. For traders, increased institutional participation typically means higher liquidity and a stronger market (but may also be more correlated with traditional assets as institutions view ETH similarly to commodities or tech stocks). For the network, it means additional resources and validation—such as client teams funded by corporations or new use cases driving fundamental demand (like gas fees from tokenized asset transfers).

By 2035, Ethereum may be deeply intertwined with the global financial system, becoming open infrastructure for the daily interactions of many exchanges, banks, and corporations.

Key metrics and predictions for 2035

Predicting the developments of a fast-evolving network like Ethereum over the next decade is not easy, but we can outline key metrics and expected trends based on current data and planning. These metrics include network utilization and throughput, security and decentralization levels, economic factors (supply, staking rates, yields), and ecosystem health metrics. Below, we will discuss these metrics one by one and provide forecasts or ranges for 2030 to 2035 based on reliable sources' analyses.

Throughput (transaction volume and capacity): Ethereum's Layer 1 currently processes about 1 to 1.5 million transactions daily (averaging around 12 to 15 TPS), typically constrained by gas limits. As rollups handle more load, Layer 1's usage rate has stabilized. For example, in July 2025, Layer 1 processed 46.7 million transactions (about 1.5 million/day). By 2030, following the introduction of prototype Danks sharding (proto-danksharding) and full Danks sharding (full danksharding), the underlying capacity could increase significantly. Vitalik Buterin's roadmap calls for Layer 1 to ultimately support around 100,000 TPS through sharding—though in practice, this mainly represents rollup data, not direct user cryptocurrency transactions (TXN). The goals for Lean Ethereum's Beast Mode are even more ambitious: 1 trillion gas per second on L1, assuming 1 gas = a simple computation, roughly translating to about 160,000 TPS. On L2, the target is 1 teragas—aggregating millions of TPS across rollups effectively. These are ideal targets (over a decade out). Conservatively, by 2035, Ethereum's L1 could handle 5,000-10,000 TPS of data availability for L2 (sufficient to support major global applications), while L2 will provide users with a total speed of around 50K-100K TPS. Essentially, most transactions will occur on L2. We have already seen post-merge rollup transactions exceed L1 transactions in 2024; by 2030, L1 may mainly be used for large settlement transactions and blob data, while daily user activity will be abstracted away. Another metric is data throughput—in July 2025, the monthly data usage of blobs on Ethereum L1 first exceeded 100,000 MB, and with full sharding implementation, this number could increase by orders of magnitude.

Gas fees and transaction costs: Users care about fees, and Ethereum's past high costs have forced many users to turn to alternatives. With scaling performance improvements, typical transaction fees are expected to decrease significantly. EIP-4844 (originally danksharding) can already reduce rollup fees by about 10 times by introducing cheap blob storage. The 2025 Pectra upgrade (doubling the number of blobs) will further reduce L2 fees. Combined with upgrades like sharding and the RISC-V engine (which will lower execution gas costs by 50-70%), we can predict that by 2030, the actual cost per transaction for users conducting simple transfers on rollups may be only a fraction of a cent, while the cost for complex smart contract calls will be only slightly higher.

However, on L1, direct use of gas prices can still be high—and likely only complex or high-value use cases will warrant execution on L1. The base fee mechanism will continue to adjust to keep Ethereum's L1 nearly always at full capacity (regardless of capacity). In absolute terms, if demand truly surges, L1 fees may still occasionally spike, leading to significant ETH burns. However, generally speaking, Ethereum's goal is to make transaction fees negligible for most users by pushing activity to L2. One thing to note is whether Ethereum will introduce a tiered fee market or blob space bandwidth auctions, as this could impact rollup operators' costs. Overall, by 2035, we foresee fee constraints no longer being a primary barrier to user adoption of Ethereum; user experiences on L2 will be akin to using Web 2.0 applications in terms of cost and speed.

Staking participation and validator numbers: Since the Merge, staking participation has been on the rise. By the end of 2024, about 20% of ETH will be staked, reaching around 25% by mid-2025. The following factors will encourage more ETH staking: the Shanghai upgrade allowing withdrawals, eliminating liquidity risk; the growth of institutional staking services; and potential protocol changes (like lowering the minimum staking amount to 1 ETH) that will reduce the barrier to entry. Binance Research predicts that several years from now, ETH staking participation will exceed 40% of ETH supply. By 2030, it would not be surprising if 50% or more of the total ETH is staked. The eventual total ETH supply may reach around 120 million, implying a staking amount of 60 million ETH. If the minimum number of ETH per validator remains 32 ETH, there would be about 1.9 million validators—but more likely, the entry threshold will decrease, or pooled solutions will remain popular, so the actual number of validators could be in the millions (especially if 1 ETH validators emerge—then tens of millions of validators become possible, although this may introduce network challenges). Researchers at the Ethereum Foundation have considered Distributed Validator Technology (DVT), which would allow many small stakes to securely act as a single validator. Therefore, a reasonable scenario is that by 2035, Ethereum may have 5 to 10 million active validators, which would increase its level of decentralization by several orders of magnitude compared to today’s 700,000 to 1 million. (Specifically, Token Terminal reports that by mid-2025, Ethereum will have around 1.1 million validators.) As participant numbers increase, rewards per validator will decrease: if participation is extremely high, the base issuance rate may drop to around 1.5%, but fees and MEV could rise by several percentage points. This leads to the next yield metric.

Staking yield: Currently, the annual yield is about 4%, and if the proportion of staked ETH increases, the yield will trend downward (the protocol issuance rate relative to the total staked amount is fixed—an increase in staking means each validator receives a smaller share). In extreme cases, such as if the staked ETH proportion exceeds 50%, the issuance yield could approach 2% or even lower. However, total rewards also include priority fees and MEV, which grow with usage rather than validator numbers. As Ethereum usage increases (especially during high transaction volume or ongoing high MEV activities like arbitrage), these additional rewards could be quite substantial. Binance analysts optimistically predict that by 2027, staking annual yields may rise to 6-8%, but this is likely based on assumptions of extremely high fee income distribution. A more balanced view is that by 2030, the base issuance yield may be around 2% (assuming participation exceeds 50%), with additional rewards potentially adding 1-3%, resulting in a total annual yield of 3-5% in ETH. It is important to note that if ETH is deflationary, even with relatively low yields, real yields could exceed inflation rates. If staking through liquid staking derivatives, there may be more composable yields (e.g., borrowing against staked ETH). For traders, a lower yield environment may imply insufficient motivation to stake unless they are bullish in the long term (as capital may flow to other yield opportunities). On the other hand, if ETH remains deflationary and yields reach 3%, it starts to behave like a high-grade asset in a portfolio (e.g., a mix of growth stocks and bonds).

ETH supply and issuance/burning: The dynamics of ETH supply can shift from inflation (before 2021) to net neutrality or deflation. As mentioned, some forecasts (like VanEck) suggest a supply of about 121 million by 2030 (roughly in line with around 120 million in 2023). This assumes moderate usage and some deflation. In high usage scenarios, the amount of ETH burned could exceed the issuance rate, leading to a decrease in supply. We have observed some negative issuance periods (e.g., during the 2021 NFT craze and other times). By 2035, Ethereum's supply may range between 100 million and 120 million, depending on the frequency of network congestion (congestion triggers high burn rates). Given current parameters and expected demand, it is unlikely that ETH will exceed 120 to 130 million. A stable or declining supply of ETH is significant—as it means that long-term holders will not suffer massive dilution like most altcoins. As ETH's scarcity increases relative to the thriving on-chain economic activity, this could, in turn, support ETH's valuation (market cap).

Network revenue (fees) and economic activity: Network revenue (all paid fees) measures the value people place on block space. As mentioned, VanEck predicts that by 2030, Ethereum's total annual fees plus MEV could reach $51 billion, approximately 20 times the level in 2023. If Ethereum supports a significant portion of global finance (like tokenized assets), billions in fees are conceivable—though most fees will flow to Layer 2, with only a portion going to Layer 1 (however, Layer 1 will charge blob fees and some Layer 2 proof costs). On-chain transfer volumes (potentially reaching trillions of dollars annually if including stablecoin transfers) could also see exponential growth. By 2030, Ethereum may regularly settle value transfers equivalent to several percentage points of global GDP (via stablecoins, tokenized currencies, etc.). Another metric is DeFi's TVL (Total Value Locked), which currently stands at about $40 billion in the bear market of 2023, having exceeded $100 billion at its peak in 2021. With institutional adoption and tokenization, TVL could soar to hundreds of billions or more. Binance Research speculates that better integration between Layer 1 and Layer 2 could help boost the total TVL of DeFi from around $1.2 trillion to $2 trillion in the coming years (though the $1.2 trillion figure may refer to a broad cryptocurrency market metric, as the actual DeFi TVL is not that high; perhaps that number includes the total market cap of cryptocurrencies). In any case, if global assets shift on-chain—even if only a small fraction (for instance, if by 2030, assets reach $10 trillion)—it could push DeFi's TVL to trillions of dollars.

Decentralization and security: Ethereum's Nakamoto coefficient (the number of entities required to control more than 50% of the stake) is an important (but sometimes overlooked) metric. Currently, large staking pools (like Lido, Coinbase, etc.) hold a significant share. The community is driving further decentralization through solo staking and technologies like DVT. By 2035, if millions of validators exist, we hope for more decentralized control (ideally, no single entity owning more than 10% of the stake). This will depend on incentives, and perhaps actions at the community or protocol level; some participants have proposed ideas like limiting the dominance of pools through social consensus. From a security perspective, the total value staked in ETH (now over 20 million ETH) represents the economic security of the chain. If ETH's value increases, and more ETH is staked, the cost to attack the chain will become extremely high. Ethereum's economic security is already second only to Bitcoin; by 2030, if ETH's market cap surpasses Bitcoin's (if Ethereum's utility drives greater demand, some foresee this), it could become the most secure blockchain.

Growth of developers and ecosystem: A qualitative but still data-supported metric is the number of developers and projects. Electric Capital's developer report shows that the number of Ethereum developers has been steadily increasing year over year, with over 2,000 active developers monthly based on certain metrics (tens of thousands if part-time developers are included). If Ethereum continues to be the preferred platform, these numbers should increase or at least remain maximized. The number of deployed smart contracts and the number of contract calls are another metric; both could see exponential growth if adoption widens. By 2035, interactions with Ethereum for ordinary internet users (typically through L2 or integrated applications) could become as common as using email, even if they are not aware of it (especially if platforms like social media integrate NFTs or on-chain content).

To summarize the expectations: by 2035, Ethereum's base layer will operate at high capacity, primarily serving as a coordination and settlement layer for a vast multi-chain ecosystem (mainly its rollups). Key metrics like transactions and addresses may not see explosive growth on Layer 1 (as activity migrates to Layer 2), but Ethereum's connected network's total usage will soar. ETH supply will remain stable or decrease, staking will be ubiquitous, and yields will be moderate but stable. A large validator set and potential post-quantum upgrades will enhance security. Ethereum's network revenue (fees) will reflect its role as a pillar of the new financial system—potentially reaching billions of dollars annually, much of which will be returned to ETH holders through token burning or staking rewards. Many analyses from crypto research firms and investment banks support the notion that Ethereum's growth in usage will even outpace optimistic price growth, meaning that even if speculative cycles lead to valuation fluctuations, there will be more transactions, assets, and real economic value on-chain.

Essentially, these metrics indicate that by 2030, Ethereum will become an indispensable part of global infrastructure, measured by the economic throughput and user base it supports.

Final thoughts

Ethereum is expected to experience profound maturation on its development path from 2025 to 2035—technologically, economically, and in integration with the broader world. Over the next decade, Ethereum will transform into the largest and most resilient layer for decentralized applications (DApps) and digital finance. The network's ambitious upgrades (from danksharding and zkEVM rollups to the long-term 'Lean Ethereum' reconstruction aimed at post-quantum security) are designed to ensure Ethereum can serve billions of users and securely settle trillions of dollars in value. By 2035, Ethereum may process transactions at network speed and scale, with most activities occurring seamlessly on L2 networks based on its security.

Ether (ETH) itself may solidify its position as the premier yield asset in the crypto economy—it is a digital bond that can earn stock-like yields through network usage. As Ethereum's economic layer expands through DeFi innovation and the tokenization of real-world assets (RWAs), the value of ETH will continue to grow—not through speculative hype, but through real fee income and its critical role as collateral and stake in the system. Competing Layer-1s will ensure the ecosystem remains competitive, as Ethereum's unmatched developer base, first-mover advantage, and adaptability (embracing rollups and new technologies) firmly establish it as the preferred Layer-1, akin to open protocol standards for Web3, such as TCP/IP for the internet.