In the crypto derivatives market, basis and funding rate are the two core indicators for understanding arbitrage logic. Mastering their relationship allows you to design risk-controlled market-neutral arbitrage strategies for stable profits.

This article will take you:

Understanding the causal relationship between basis and funding rate

Mastering the logic and sources of profit from two core arbitrage strategies

Understanding the practical points and risks under different market conditions

One, the core relationship between basis and funding rate

1️⃣ What is basis?

Formula: Basis = Perpetual contract price - Spot price

Positive basis (Contango): Futures price is higher than spot → Market is optimistic

Negative basis (Backwardation): Futures price is lower than spot → Market is pessimistic

Traditional futures have a delivery date, and basis naturally converges; perpetual contracts have no delivery date and require a funding rate mechanism to maintain anchoring.

2️⃣ What is the funding rate?

Funding rate is the fee that longs and shorts pay each other periodically in the perpetual contract market (usually every 8 hours),

used to push the price of perpetual contracts closer to the spot price.

Linkage mechanism:

Positive basis → Positive funding rate (longs pay shorts)

Negative basis → Negative funding rate (shorts pay longs)

3️⃣ Core conclusions

Basis is the cause, funding rate is the effect

Basis reflects market sentiment imbalance, while funding rate drives market correction through economic incentives.

Two, two core arbitrage strategies

Under the linkage of basis and funding rate, two market-neutral arbitrage strategies emerge:

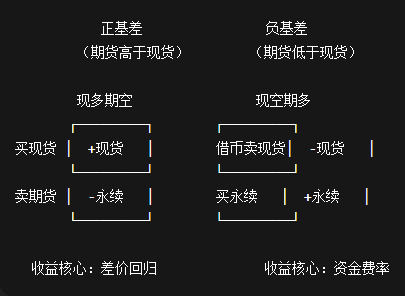

1️⃣ Current long and future short (Cash-and-Carry)

Applicable scenario: Positive basis (futures > spot), funding rate is usually positive

Operational steps:

Buy spot (current long)

Short perpetual contracts in equal amounts (future short)

Source of income:

1. Core: Basis regression income (spread arbitrage)

A positive basis means that the futures price is higher than the spot price

After the basis converges, the unrealized profit from shorting futures offsets the unrealized loss from the spot → Lock in the price difference

2. Secondary: Funding rate

Under positive funding rates, longs pay shorts → Futures shorts can additionally collect funding fees

✅ The essence is to earn the price difference between futures and spot, while the funding fee is just an added bonus.

2️⃣ Current short and future long (Reverse Cash-and-Carry)

Applicable scenario: Negative basis (futures < spot), funding rate is usually negative

Operational steps:

Borrow coins to sell spot (current short)

Buy perpetual contracts in equal amounts (future long)

Source of income:

1. Core: Funding rate income (rental arbitrage)

Funding rates are usually negative during negative basis

Perpetual contracts long can consistently collect funding fees paid by shorts

2. Secondary: Basis regression income

If the basis returns to zero, spot shorts profit, and futures longs incur losses, offsetting each other → Additional profit from price difference

✅ The essence is to earn funding fees, while price differences are just additional income.

3️⃣ Strategy logic diagram (illustrative)

Understand at a glance:

Left-side strategy earns price difference (basis regression)

Right-side strategy earns funding fees (rental arbitrage)

Three, strategy execution and risk points

1. Borrowing coin thresholds

Current short and future long must borrow coins; popular coins are often 'hard to find' during high volatility, so sufficient borrowing limits or VIP account resources are needed.

2. Fluctuations in funding rates

Funding rates adjust dynamically with market sentiment, and the difference may converge or even reverse rapidly during the holding period, requiring real-time monitoring.

3. Trading and slippage costs

Arbitrage involves opening and closing positions across multiple platforms, requiring at least four transactions. Excessive slippage or high fees can severely erode profits.

Choosing a stable and efficient arbitrage trading system, keeping slippage within acceptable limits, is key to improving profits. ✅

In terms of fee costs, you can choose trusted, reliable, and appropriately commission-sharing exchange referral links, which can save a lot of costs in the long run. ✅

4. Forced liquidation and ADL

Both sides are leveraged positions; if the margin is insufficient or volatility is extreme, it may trigger forced liquidation or ADL (automatic deleveraging)

Control the explosion rate, transfer funds in a timely manner, and prioritize arbitrage trading systems with ADL risk control features to significantly reduce unilateral risk. ✅

For cross-exchange fund transfers, it is recommended to use the Aptos chain, which is cheap and fast, significantly reducing funding costs. 🚀

⚡ Professional traders' tips:

"Choosing an arbitrage system with risk control and cross-exchange automation features is essential for stable arbitrage income."

Four, summary

Current long and multiple shorts (positive basis arbitrage) → Core profit from price differences, funding rate is secondary

Current short and future long (negative basis arbitrage) → Core profit from funding fee, price difference is secondary

Basis is the cause, funding rate is the effect, and arbitrage essentially involves using market-neutral strategies to collect structural income

Master this logic, and you can become a 'renter' in the crypto market, stabilizing profits from structural imbalances.