Stablecoins, as a special form of cryptocurrency, differ from volatile crypto assets like Bitcoin and Ethereum. By pegging to fiat currencies, they significantly reduce price volatility risks. This characteristic allows stablecoins to gradually expand from being "in-house payment tools" in the crypto industry to broader commercial and consumer scenarios.

In recent years, as global digital payment acceptance has increased, especially driven by hot topics like DeFi and NFTs, ordinary users' acceptance of crypto wallets and stablecoins has rapidly risen. Mainstream stablecoins, including USDT and USDC, are increasingly used in scenarios such as e-commerce, subscriptions, gig payments, and international remittances.

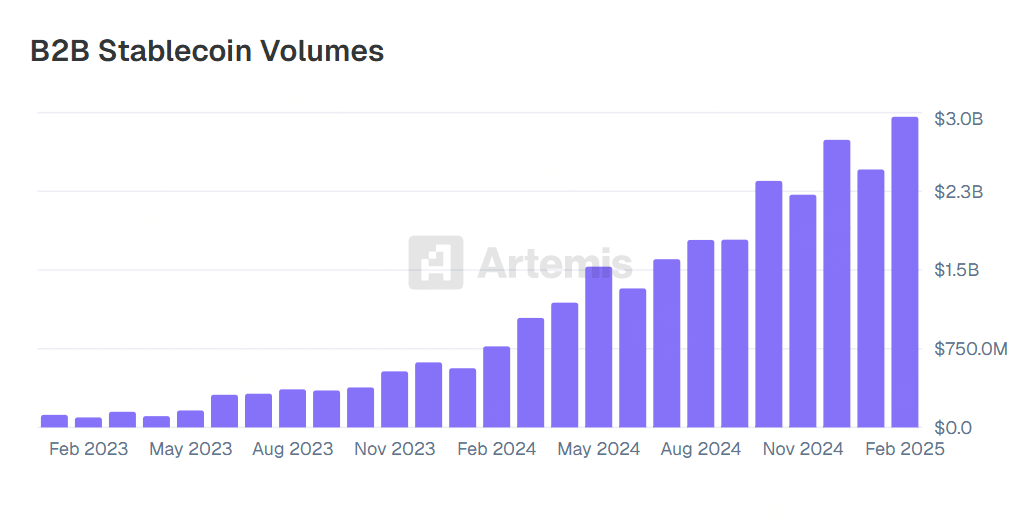

Compared to C-end payments, B2B enterprises are more eager for low-cost, high-efficiency global payment solutions. Due to characteristics such as instant settlement, low costs, and transparency and traceability, stablecoins are gradually becoming a new choice for inter-company settlements. According to the report (Stablecoin Payments from the Ground Up) released by crypto risk analysis company Artemis and crypto investment firms Dragonfly and Castle Island Ventures, the scale of B2B stablecoin payments surged from $100 million in January 2023 to $3 billion by February 2025, a 30-fold increase. Stablecoins are gradually becoming a core financial segment for companies and sparking a vast market space.

The rise of stablecoins: From niche cryptocurrency to the core of future finance.

In recent years, the stablecoin market has seen explosive growth. According to the report (Stablecoins: The Emerging Market Story) jointly released by Castle Island Ventures and Brevan Howard, the global circulation of stablecoins skyrocketed from less than $1 billion in 2017 to over $160 billion in 2024. In 2023 alone, the settlement amount of stablecoins reached an astonishing $3.7 trillion, with $2.62 trillion already in the first half of 2024 (annualized at $5.28 trillion). These figures indicate that stablecoins are no longer merely tools for cryptocurrency trading, but have become essential media for global value exchange.

This has also forced major global market regulators to take clear regulatory stances on stablecoins. On May 21, 2025, the Legislative Council of Hong Kong officially passed the (Stablecoin Regulation Draft), establishing a licensing system for fiat currency stablecoins; on July 28, the US House of Representatives passed three pieces of crypto-related legislation: (CLARITY Act), (GENIUS Act), and (Anti-CBDC Surveillance National Act). These regulatory advancements send a clear signal that stablecoins are moving out of the gray area and into the fringes of the mainstream financial system.

In this trend, traditional financial giants are accelerating their embrace of stablecoin technology, with Visa and Mastercard also launching settlement functions integrating stablecoins. This will further promote the application of stablecoins in the B2B payment sector, providing companies with more efficient and lower-cost payment solutions.

B2B scenario implementation: New solutions brought by stablecoins.

Compared to traditional bank wire transfers, stablecoins show significant advantages in the B2B payment sector.

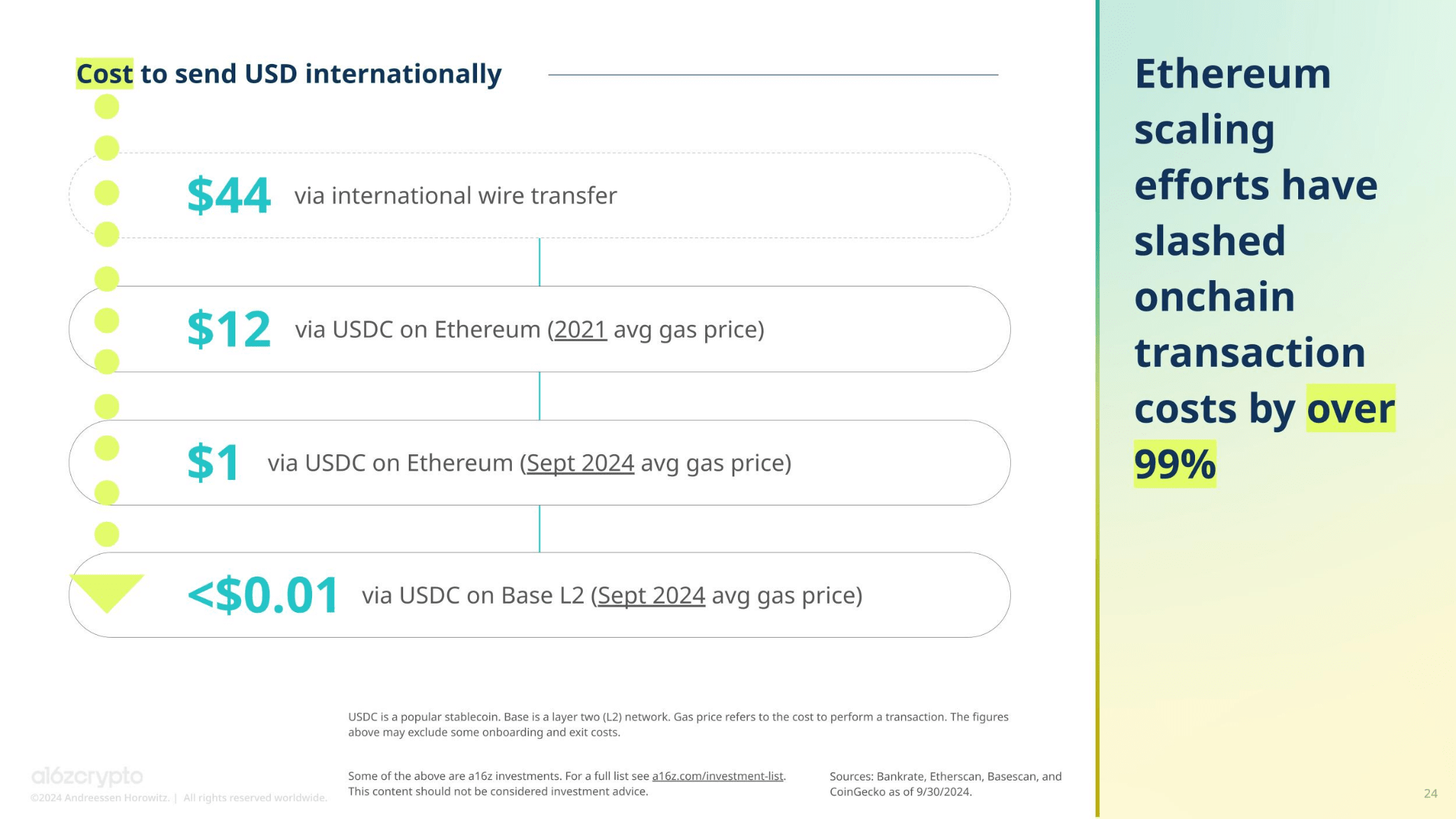

Firstly, in terms of speed, traditional cross-border payments typically require 1-5 working days to complete settlement, while stablecoin transactions can achieve near real-time clearing on the blockchain, significantly shortening the capital turnover cycle for businesses. Secondly, regarding costs, traditional cross-border payments involve multiple intermediary banks, each charging fees, with total costs reaching 3-5% of the transaction amount, while stablecoin transaction fees are usually below 0.1%. Additionally, the blockchain-based characteristics of stablecoins also offer high transparency, strong programmability, and year-round availability, which are hard for traditional financial institutions to match.

With the gradual improvement of Web3 financial infrastructure and risk compliance capabilities, stablecoins are rapidly penetrating the B2B payment sector and entering the stage of practical business implementation, especially in regions like Latin America and Southeast Asia, where currency value fluctuations are significant. Many companies have begun to utilize stablecoins for cross-border payments, salary distributions, procurement settlements, etc., thereby optimizing payment processes, reducing operational costs, and improving capital efficiency.

Case 1: Cross-border trade settlement, taking Latin America's import and export business as an example.

In traditional cross-border trade, especially transactions involving emerging market countries, the payment process is often lengthy and complex. Assume Colombia imports medical equipment from the United States; the Colombian importer needs to purchase US dollars through a local bank, often facing strict foreign exchange controls and limits; then remittance is done through the SWIFT network, passing through multiple intermediary banks, each service provider charging fees and requiring processing time; ultimately, the US exporter receives the funds 2-3 working days later, but the amount has been reduced due to various intermediary service fees.

Using stablecoin payments disrupts this process, allowing importers to exchange stablecoins like USDC through compliant Web3 payment institutions, which can be directly transferred to the US exporter's crypto wallet, arriving almost in real-time, with costs less than one-tenth of traditional methods.

Case 2: International salary payments, stablecoin salary solutions for global enterprises

For companies with global teams, traditional salary payments also face many challenges: high remittance fees, exchange rate losses, long processing times, and low bank account penetration rates in certain countries. Especially in countries like Nigeria, ordinary bank accounts cannot receive international currency transfers, forcing companies to seek alternative solutions.

In the context of international salary payments, stablecoins also provide an efficient solution. Companies can pay employees' salaries distributed across multiple countries using stablecoins like USDT, and employees can exchange them for fiat currency through professional compliance service providers or directly use stablecoins for consumption. Compared to traditional international wire transfers, this solution has clear advantages: first, costs are significantly reduced, especially for small payments, with fees dropping from a fixed range of tens of dollars to around 0.5%; second, the speed of receipt is fast, with employees able to receive their salaries within minutes; third, there is strong financial inclusivity, as employees without bank accounts can also receive salaries through cryptocurrency digital wallets. Especially in countries with strict foreign exchange controls, such as in Latin America, stablecoins have become a practical solution for companies to pay international employees and outsourced teams. According to the report (Stablecoins: The Emerging Market Story), 25% of respondents have received or paid salaries through stablecoins, with this figure reaching 37% in India.

A comprehensive analysis of the above cases summarizes the advantages of stablecoins in the B2B sector as follows:

● Settlement efficiency: Transactions are completed in real time or within minutes, greatly shortening the capital turnover cycle.

● Cost structure: Eliminating intermediary banks reduces costs to 1/10 or even lower than traditional methods.

● Global reach: Breaking through the limitations of traditional bank accounts, particularly suitable for areas with weak banking infrastructure.

● Transparency: All transaction records are verifiable on the blockchain, facilitating audit trails.

However, companies also need to consider implementation thresholds when adopting stablecoin payments, including the cryptocurrency acceptance of transaction counterparts, compliance and risk control, price volatility risks (despite stablecoins being designed to maintain their peg), and the complexity of technical operations. Collaborating with professional crypto payment service providers instead of directly engaging in cryptocurrency operations is a more prudent choice for most companies. Companies like Interlace, which link Web3 to Web2, cover products and solutions such as global accounts, Infinity Card, CryptoConnect, CaaS API, providing fiat and stablecoin payment, settlement, and fund management solutions for Web3 institutions, crypto exchanges, cross-border e-commerce, B2B trade, and other enterprise transaction scenarios, covering over 180 countries and regions.

Regulation and compliance: Key thresholds and response strategies for enterprises adopting stablecoins.

Although stablecoins have brought significant efficiency improvements to B2B payments, companies still need to cautiously address various compliance risks and operational challenges in the actual adoption process. The primary compliance risk arises from regulatory uncertainty—different jurisdictions have vastly different legal definitions of stablecoins: some US states regulate stablecoins as money transmission tools, the EU defines them as "electronic money tokens" through MiCA, while some countries outright prohibit the use of stablecoin transactions. This fragmented regulatory environment requires companies to conduct thorough compliance assessments before cross-border use of stablecoins.

Additionally, anti-money laundering (AML) and KYC, KYB requirements are another major compliance challenge for businesses. For example, the Financial Action Task Force (FATF) has included virtual asset service providers (VASPs) in its international standards, requiring AML/CFT controls for cryptocurrency transactions that are on par with traditional finance. This means that if a business directly uses stablecoins for large B2B payments, it may have to bear corresponding customer due diligence and transaction monitoring responsibilities.

To address these challenges, companies may consider adopting the following compliance strategies:

● Collaborate with regulated stablecoin issuers (such as Circle's USDC) and trading platforms to ensure the compliance of underlying assets.

● Introduce licensed virtual asset service providers as compliance nodes in the transaction chain, responsible for AML/KYC.

● Establish a dedicated blockchain transaction monitoring system, or procure professional services like Chainalysis to ensure traceability.

Web3 financial companies like Interlace are helping businesses meet these compliance requirements. Interlace has integrated multiple protections such as smart risk control, compliance review, and user identity verification into product and solution designs, achieving KYC, KYB verification, and AML monitoring. Notably, for on-chain anti-money laundering, Interlace has also constructed KYT (Know Your Address) and KYA (Know Your Transaction) programs—risk rating on-chain addresses through a vast data label library, controlling high-risk transactions in real time. Continuous monitoring of crypto addresses is also conducted, along with regular retrospective screening and address rotation, ensuring the security of the platform and funds.

Currently, Interlace has obtained licenses and qualifications from multiple jurisdictions, such as Hong Kong TCSP, Lithuania VASP, and US MSB, complying with the highest security certification PCI-DSS Level 1 in the international card payment industry. This means that companies can focus on business development with the support of Interlace's compliance and risk control resources.

Future Outlook: A new landscape of corporate payments driven by stablecoins.

According to the report (Stablecoin Payments from the Ground Up), data analysis of 31 stablecoin payment companies shows that from January 2023 to February 2025, these companies completed over $94.2 billion in daily payment transactions. Among them, B2B payments are the main use case, with an annualized transaction scale of $36 billion, reflecting the actual application value of stablecoins in cross-border settlements, fund management, and supply chain payments. Meanwhile, stablecoin payments linked to bank cards are also showing rapid growth, with annualized transaction volumes exceeding $13.2 billion. With the stabilization of regulatory frameworks and advancements in blockchain technology, it is expected that by 2030, 40% of companies will adopt crypto payments.

In the long term, stablecoins and related blockchain technologies will profoundly reshape corporate payments and asset management. The flow of funds will shift from a reliance on traditional financial institutions' processing models to real-time liquidity available around the clock; payments, settlements, and clearances will merge into a single step; and companies' visibility and control over cash flow will significantly improve. These changes collectively point to a more efficient and inclusive global corporate payment system.

In today's irreversible wave of blockchain, companies that lay out stablecoin payment capabilities in advance will gain a significant competitive advantage—faster capital turnover, lower transaction costs, and better customer experience. Stablecoins represent not only an iteration of payment technology but also an important upgrade in global financial infrastructure.