What does it imply that Solana, Cardano, and BNB are declared 'securities' or 'auxiliaries'?

What does it imply that Solana, Cardano, and BNB are declared 'securities' or 'auxiliaries'?

ADA

ADA SOL

SOL SEC

SEC ADASOL

ADASOL BNB

BNB

Investors in altcoins like Solana (SOL), Cardano (ADA), and BNB, the native token of the BNB Chain, must closely follow the debate on the legislative proposal called Responsible Financial Innovation (RFI Act).

This initiative could establish a key distinction in the United States by classifying crypto assets, including Bitcoin (BTC), into two categories: securities or auxiliary assets, which would have significant implications for their regulation and use.

According to the bill, auxiliary assets are defined as intangible and commercially fungible (similar to digital commodities) that are offered, sold, or distributed in relation to an investment contract. And as already reported by CriptoNoticias, Bitcoin is a strong candidate to be classified in this category due to its decentralized nature and absence of a central originator.

However, altcoins like Solana, Cardano, and BNB would have to undergo a validation process before the Securities and Exchange Commission (SEC), which would become the main regulator.

Achieving classification as an auxiliary asset would exempt projects from the heavy securities regulations. The originators of auxiliary assets (those who initially offer, sell or distribute it) could even submit a self-certification to the SEC, supported by evidence, that certifies that the asset does not grant financial rights that disqualify it from this category.

And if the agency does not refute it within 60 days, it would gain a status of relative legal certainty. However, it is not a free pass because still, their founders or issuers would have to comply with periodic disclosure requirements, although less strict than those of a security.

According to Criptopedia, the Bitcoin education academy of CriptoNoticias, securities, known in Spanish as títulos de valor, are tradable financial instruments.

This is a category that encompasses all assets traded on stock exchanges, brokerage firms, and financial markets. Its main characteristic is the expectation of generating profits derived, primarily, from the efforts of a third party.

Being classified as a security implies complying with the strict regulations established in U.S. securities laws, such as the Securities Act of 1933 and the Securities Exchange Act of 1934, regulations that have been in effect for over 90 years.

Subscribe

Join us to discover the cryptocurrency revolution, one newsletter at a time. Subscribe now to receive daily news and market updates directly in your inbox, along with our millions of subscribers (that's right, millions want us!), what are you waiting for?

Solana and Cardano: securities or auxiliary assets?

Achieving classification as an auxiliary asset will be a key goal for projects in the digital assets ecosystem that focus on being decentralized.

In the case of Solana and Cardano, both are projects that could demonstrate their decentralization. This is because they have validators and an active community, not by a single central entity.

However, the SEC could question the efforts of Solana's founders to demonstrate that their project is decentralized. This is largely due to recurring criticisms about the level of decentralization of the network.

For example, in a recent incident, SOL faced a vulnerability that could have compromised user funds, which was resolved discreetly. Corrections were made privately, generating discomfort among ecosystem participants due to the lack of transparency and its possible impact on decentralization, as reported by CriptoNoticias.

At that time, some data indicated that four main validators of Solana control nearly 80% of SOL in staking, which facilitates unilateral decisions and reinforces the complaint about the centralization of those participants.

However, other data throwers pointed out that of the 1,300 validators of Solana, platforms like Helius, Binance Staking, Galaxy, and Coinbase held the highest percentages of SOL staking, each representing between 2% and 3% of the total SOL in staking.

Therefore, it is necessary to wait for the SEC to analyze the data that the project founders can provide to know if Solana qualifies as an auxiliary asset, provided that the RFI initiative becomes law.

On the other hand, the SEC could argue that its initial token sales or the ongoing role of its foundations (Solana Foundation or IOHK) constitute an 'investment contract'. If this were the case, they would face disclosure requirements, although adapted and less burdensome.

In contrast, Cardano might have an easier path when it comes to qualifying as an auxiliary asset. That is if the SEC approves the process that the project initiated in December last year, seeking to consolidate the decentralization of the network.

Since then, its model reduces dependence on the founding entities (IOHK, Cardano Foundation, and EMURGO), which previously dominated decisions, and empowers users to influence the future of Cardano through vote delegation or direct participation. The transition, initiated with the Voltaire Era, seeks to ensure the sustainability and community leadership of the network.

For community members, Cardano aims for decentralization, so much so that ADA is considered an asset for digital reserves in the U.S., just like SOL and XRP.

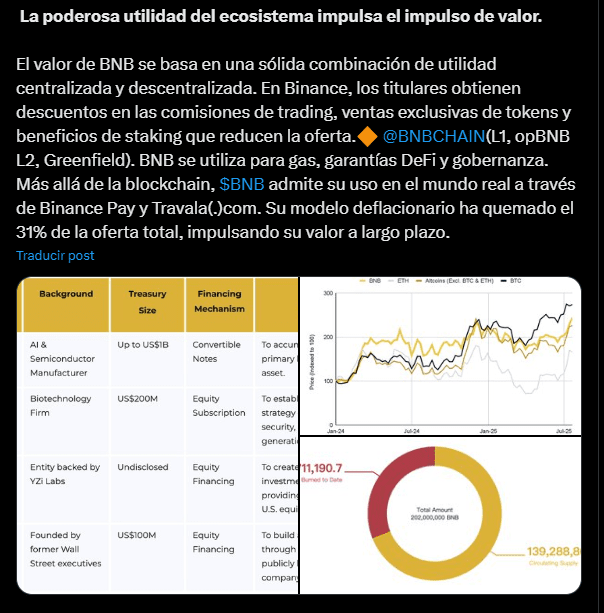

BNB trapped under the shadows of Binance

The case of BNB is much more complex and risky. Unlike Solana and Cardano, its fate is closely tied to that of Binance, the largest centralized cryptocurrency exchange in the world.

In case the company seeks classification of BNB as an auxiliary asset, the SEC could easily argue that the value of this asset directly depends on the managerial efforts of the exchange.

Its utility (discounts on fees, access to products) is anchored to the success and decisions of Binance and in that case, it would clearly qualify as a security. This centralized connection is precisely what the law seeks to differentiate from an auxiliary asset and is the central argument in the lawsuits that the SEC already has against Binance.

If BNB is declared a security, the consequences could be severe. This is because Binance would face strict registration and disclosure requirements for its cryptocurrency, which could limit its operations in the U.S., drive up its costs, and create great uncertainty in the market.

In any case, if Binance manages to convince regulators that the utility of BNB resides in the decentralized network (BNB Smart Chain) and not in the company, it could aspire to be an auxiliary asset. However, its challenge to demonstrate decentralization and end disclosure obligations is immensely greater than that of its competitors.

As strong points, in seeking to include BNB in the category of auxiliary asset, Binance could present the argument that the BNB Chain has functions that help distribute power in its community. For example, BNB holders can participate in network governance by voting on important decisions, such as the election of validators and the modification of network parameters.

In this way, it fosters a sense of ownership and participation among users, which is a fundamental principle of decentralization. Likewise, although the network has a limited number of validators, they are selected based on the amount of BNB they have in staking. This allows different participants to become validators, thereby promoting diversity and decentralization in transaction validation.

Beyond that, it must be noted that the Responsible Financial Innovation Act does not treat all cryptocurrencies equally. At its core, it rewards decentralization. But it still has to go through a long process to become law.

In itself, the RFI Act proposal must follow a rigorous legislative process that remains to be seen if it manages to pass. After its introduction as a draft by the Senate Banking Committee, it will be debated and potentially amended in committee before being put to a vote in the full Senate.

If approved, it will go to the House of Representatives, where it could be harmonized with proposals like the CLARITY Act or face modifications in a process that could take months or even years to be approved by the President of the United States.