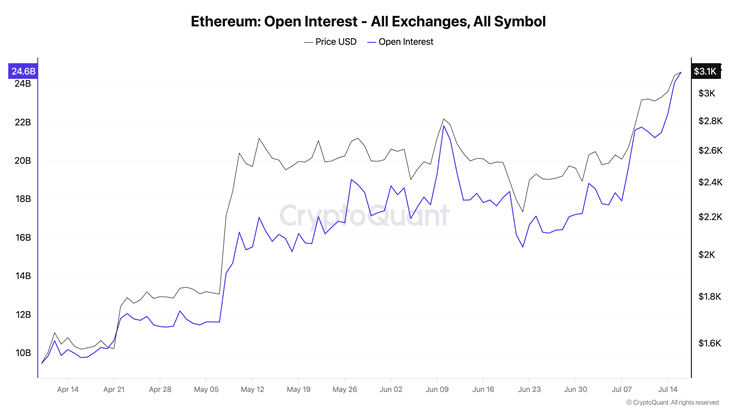

The Ethereum (ETH) derivatives market is showing clear signs of excessive speculation, with increasing leverage ratios, open interest (OI), and funding rates. Over the past 30 days, ETH has risen more than 24%, leading to a strong expansion of derivatives positions, now surpassing the $24.5 billion OI mark – an all-time high.

This has pushed the estimated leverage ratio (ELR) close to historical peak levels, while the funding rate for perpetual futures has surged to levels not seen since early 2022.

The current structure of the derivatives market reflects traders betting heavily on ETH's continued price rise. However, this also creates fragility – if spot prices stagnate or adjust, the market could quickly reverse. As traders increasingly rely on margin to maintain positions, the risk of large-scale liquidations will rise.

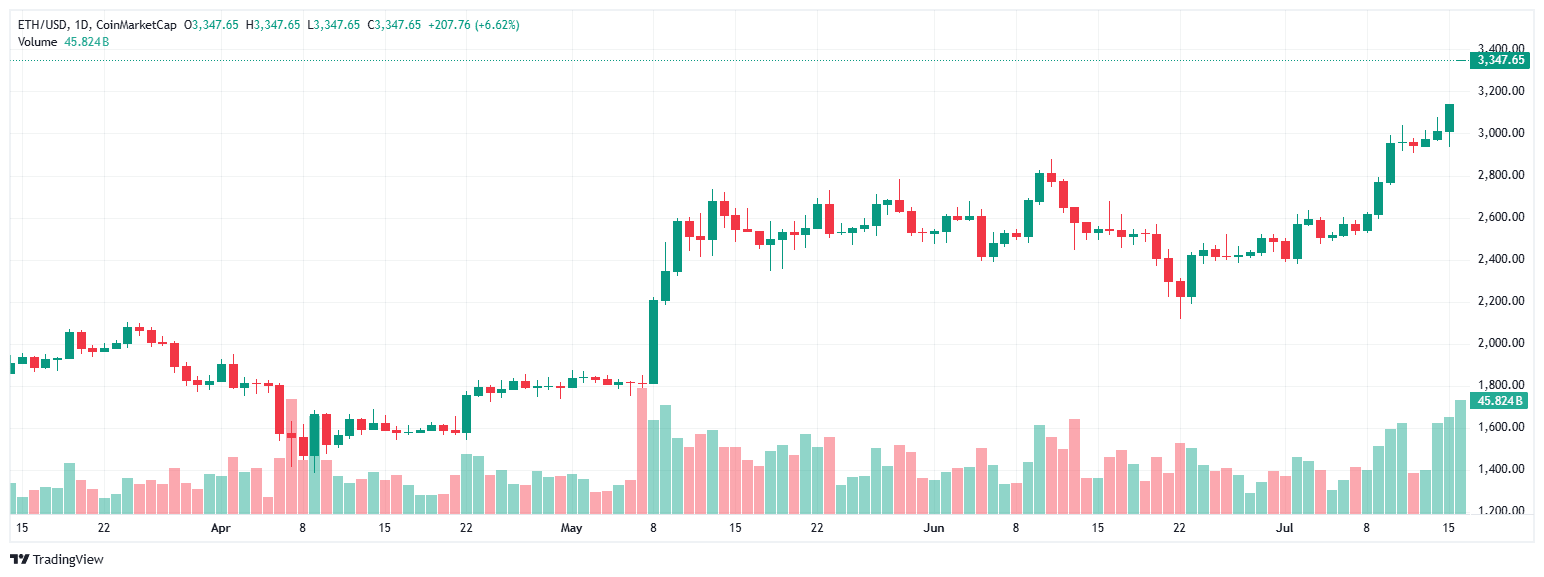

The total ETH derivatives OI across all exchanges has reached $24.5 billion, a 37% increase in just 30 days. In the past week alone, an additional $2.9 billion has been recorded. This spike in OI occurred against the backdrop of ETH rising sharply from below $2,600 to over $3,160, indicating that the market is attracting significant speculative capital.

Data from CryptoQuant shows that ETH's OI currently equates to about 7.7 million ETH, or approximately 6.4% of the circulating supply. This percentage helps us better understand the market's exposure to leverage relative to the amount of tokens in circulation. Historically, when nominal OI exceeds 6%, the market often experiences significant corrections, indicating an overreliance on derivatives to drive spot prices.

The 90-day correlation between ETH prices and OI is currently 0.96. Such a high correlation often indicates a feedback loop between rising prices and the deployment of leverage. As ETH rises in price, traders open more contracts, creating additional buying pressure until margin limits or profit-taking disrupt this cycle.

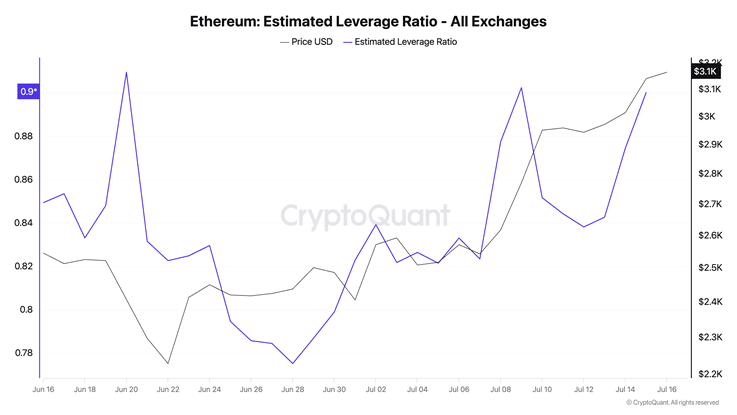

According to data from CryptoQuant, the estimated leverage ratio (ELR), which measures the ratio between OI and ETH balances on exchanges, has returned to high levels. With a rate of 0.90, it is only slightly away from the historical peak of 0.916 (set in early June).

This suggests that traders are increasingly using margin or borrowed funds to maintain trading positions. At the same time, it implies that a large portion of ETH held on exchanges is being 'locked' in derivatives contracts, rather than being used for spot trading or withdrawn from exchanges.

An increasing ELR often reduces the market's resilience to price fluctuations. In a high-leverage environment, even slight price drops can trigger a wave of liquidations when collateral levels are breached.

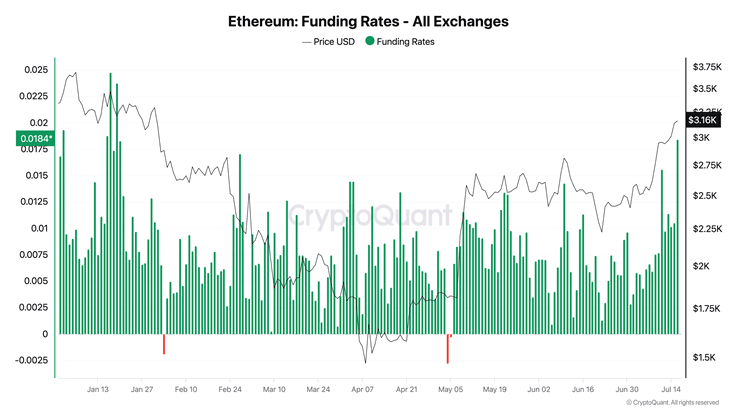

The funding rate for ETH perpetual futures has also surged. On July 16, the average daily funding rate across all major exchanges reached 0.018%, equivalent to a cost of holding a long position of about 6.7% per year. This is a significant increase from the previous week's average of 0.0075% and much higher than the 30-day average of 0.0073%.

The funding rate has only turned negative for 2 days since the beginning of the year, indicating a continuous long position trend from traders. The pressure from the funding rate is primarily concentrated on near-term perpetual swaps, especially on platforms with many retail investors like Binance, Bybit, and OKX.

In contrast, long-term ETH futures on CME and institutional exchanges are trading at more modest spreads to spot prices. This divergence indicates that the current price increase is primarily driven by short-term traders, rather than traditional asset management funds or macro trading desks.

The current expansion of the derivatives market is not occurring in a vacuum. The spot trading volume of Ethereum has also increased significantly, somewhat confirming the bullish momentum. In the past week, the average daily spot trading volume reached 874,000 ETH, 25% higher than the 30-day average.

The increase in spot trading indicates that new capital is genuinely flowing into the market, rather than merely circulating through derivatives contracts. However, the scale and speed of the derivatives market expansion still notably outpace the spot capital inflows, increasing the likelihood that a large portion of ETH's recent price increase is amplified by leverage.

Currently, the derivatives market is dominating a significant portion of ETH's price action. While this reflects market maturity, it also makes the market more fragile. High leverage, stretched funding rates, and large nominal exposure indicate that ETH is trading within a narrow equilibrium range. If spot prices continue to rise, the derivatives ecosystem may maintain self-support in the short term, attracting further capital and continuing to push leverage higher.

However, any sudden decline could cause this structure to collapse quickly. A high ELR means many positions are undercapitalized, and a sharp drop could trigger mass liquidations, causing prices to fall even further – creating a classic domino effect.