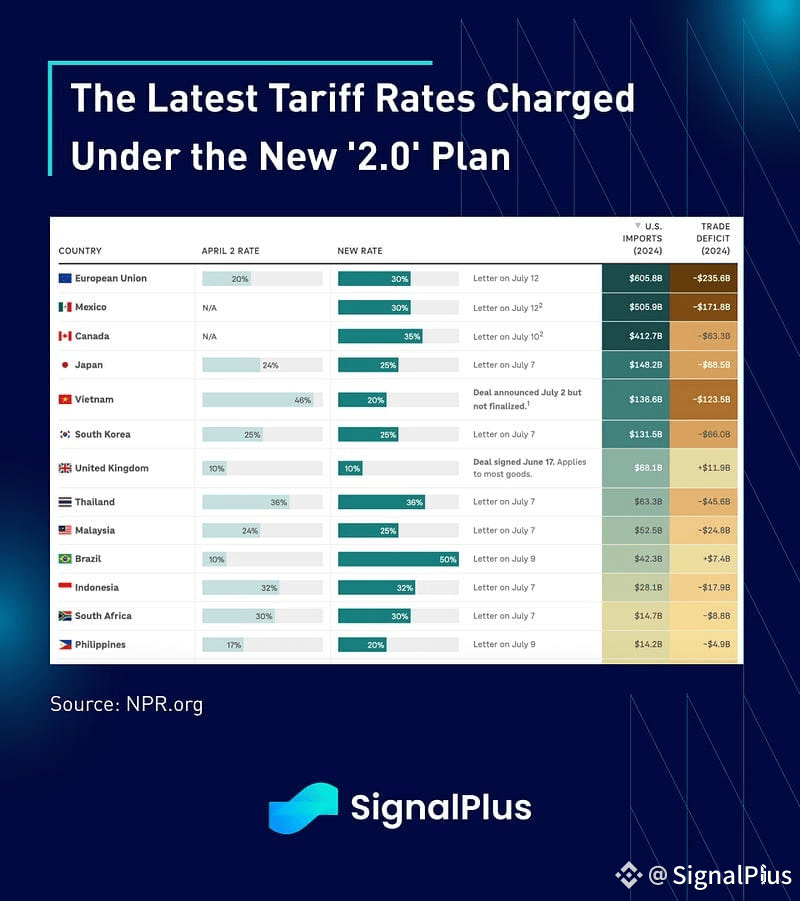

With geopolitical conflicts firmly in the rear-mirror, the most remarkable development over the past week was not the new tariff levels set under Trump’s ‘2.0’ revisions, but rather how the markets completed ignored this escalation.

The new administration has levered a new 50% tariff on Brazil, 35% on Canada, 25% on Japan & South Korea, and promised to apply a blanket tariff rate of 15–20% to all trading partners. This was certainly higher than market expectations, so is the market expecting another ‘TACO’ reversal before too long, or will the current stock market strength compell the President to push his hand more aggressively? We’ll find out soon enough…

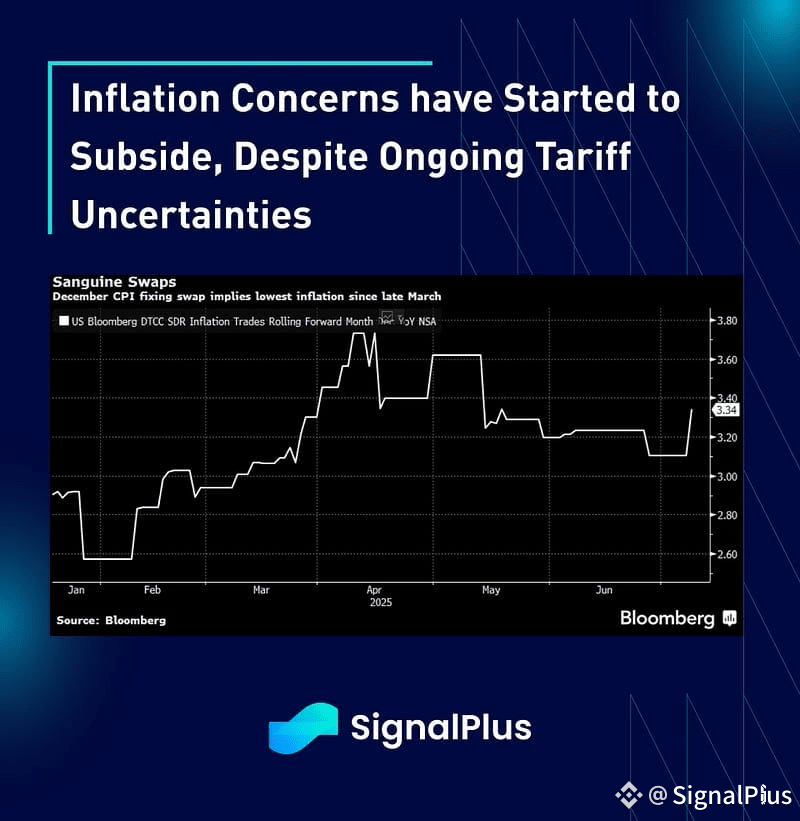

Economic data was uneventual against the recent Goldilocks narrative, and the June FOMC minutes provided little further insight as well. The FOMC ‘dot-plot’ was held unchanged with 2 cuts priced in for this year, albeit with split decision amongst Fed members. Some notable quotes include:

“A few participants noted that tariffs would lead to a one-time increase in prices”

“Most participants noted the risk [of] more persistent effects”

“Most participants assessed that some reduction in the target range for the federal funds rate this year would likely be appropriate”

“A couple of participants noted hey would be open to considering a reduction as soon as at the next meeting”

The weakening labour market took over as the chief worry over inflation, with members noting that higher tariffs and policy uncertainy would weigh on labour, and acknowledging that some indicators are already showing “signs of softness”.

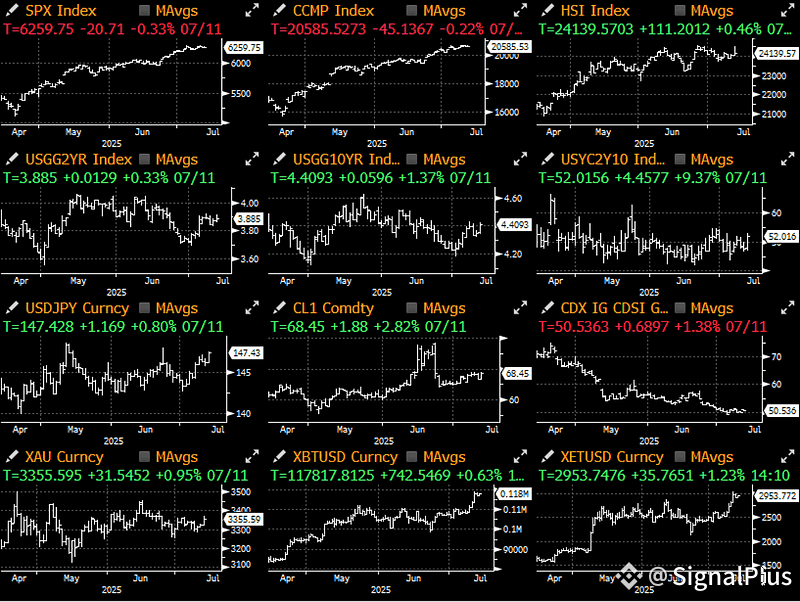

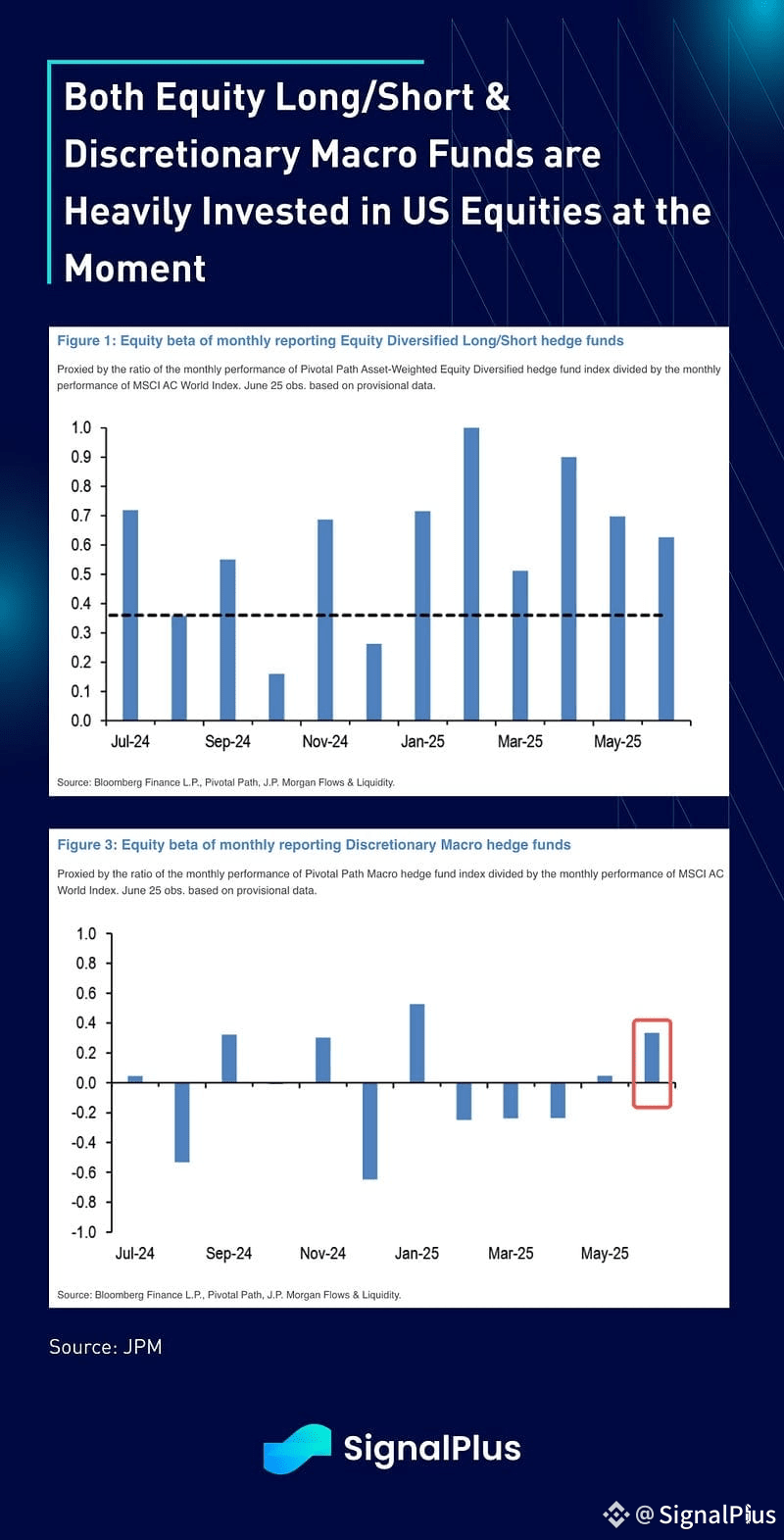

Equity markets and Bitcoin both stormed to new highs this week, with the former seeing positive inflows from all sources. Long/short hedge funds have stayed fully invested for pretty much the entire year, including the Liberation Day shocks, while discretionary macro funds have added positive equity exposure for the first time this year, and at the highest pace since the Trump election win.

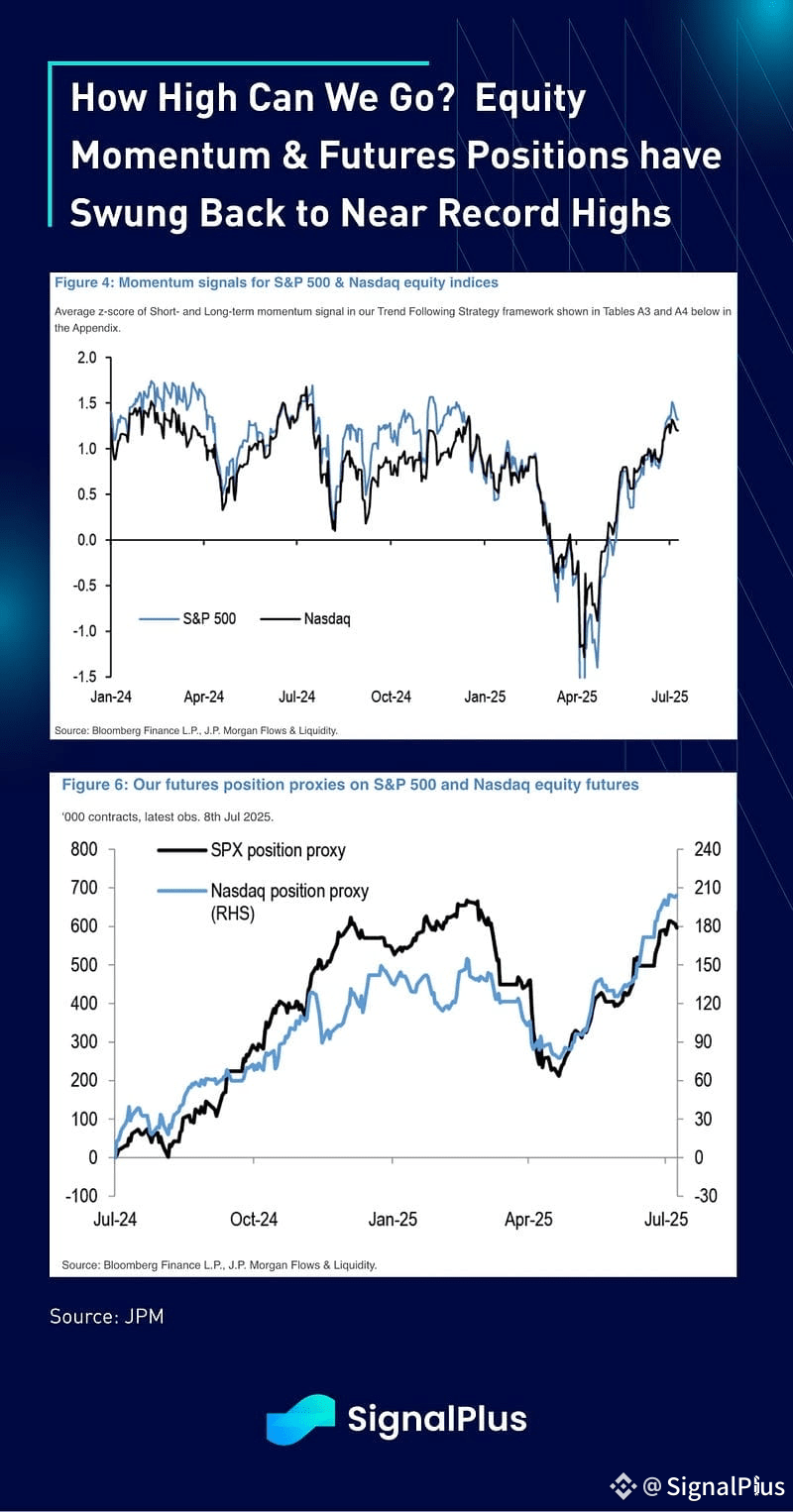

Momentum & CTA funds are most likely positioned long as well, given the extremely positive signals from the market’s rally as of late, and reflected in near-record long levels in US equity futures.

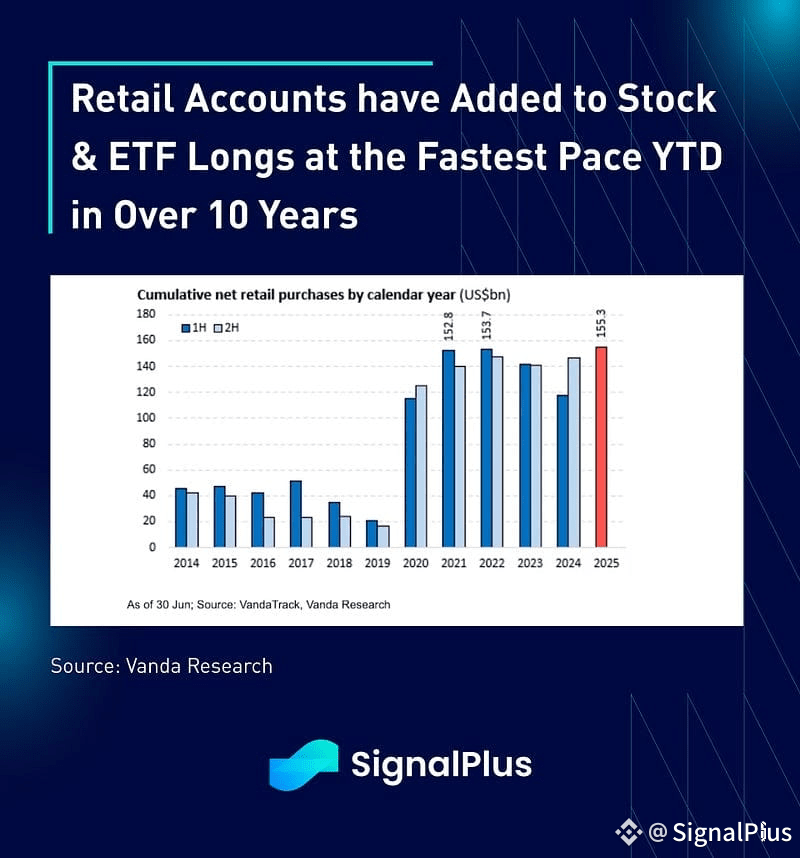

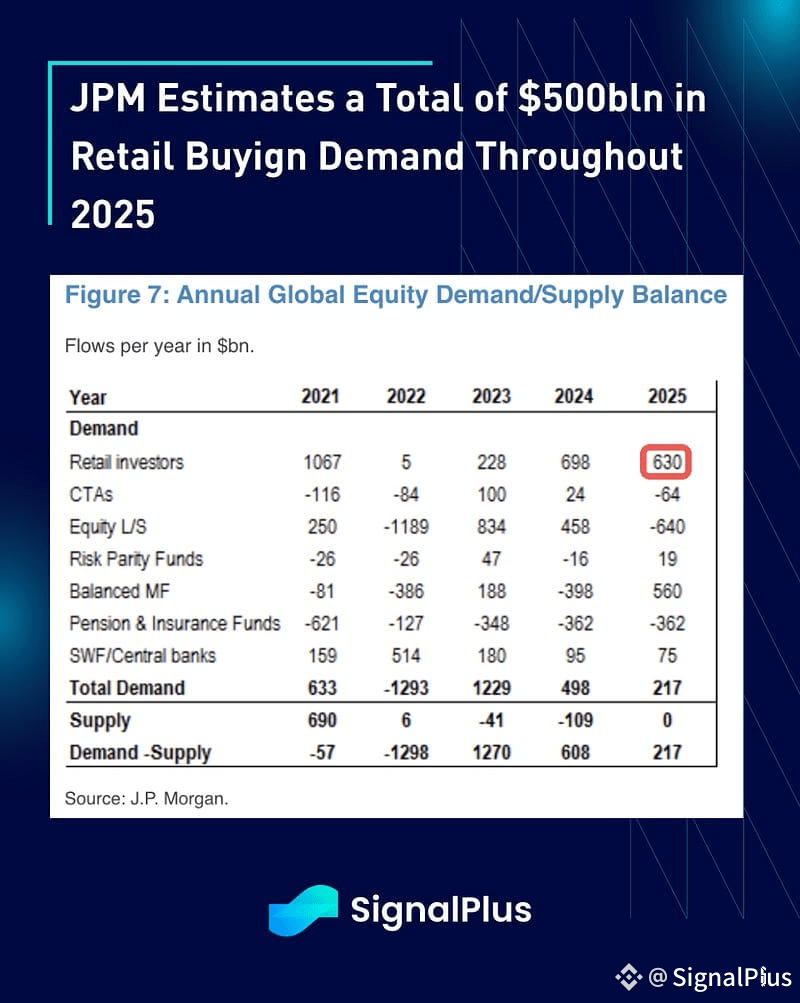

Not to be left behind, our fearless retail investors have already been piling into equity longs all year, with data from Vanda Research suggesting that retail’s cumulative net purchases of stocks and ETFs have added $155bln YTD, the highest pace in over 10 years.

As if that’s not enough, JPM estimates that retail will be buying a total of $500bln in equity demand for all of 2025, good for another ‘5–10%’ rally based on their calculations. This would make them the largest demand category across all the major investor groups — remind who the ‘smart money’ is again?

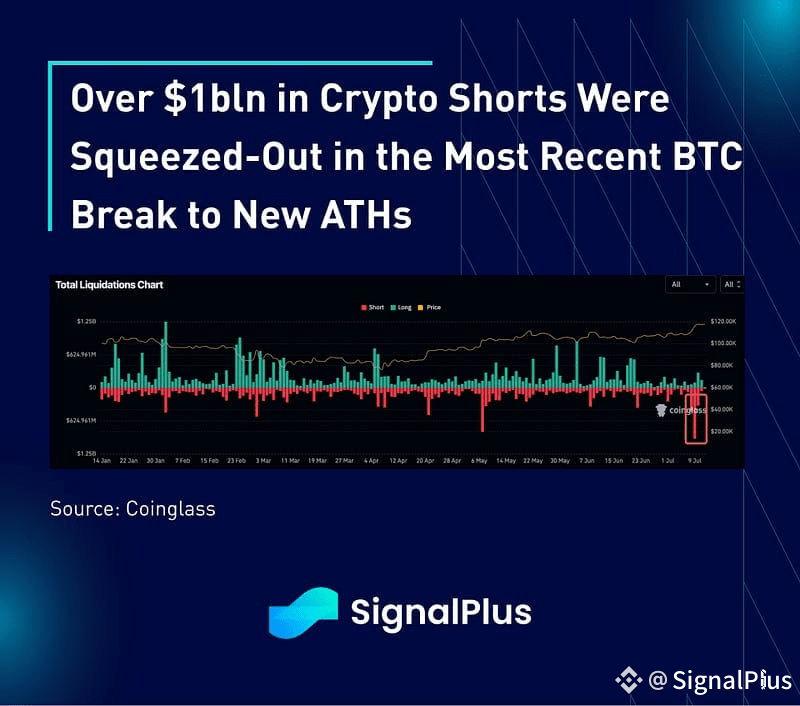

Crypto prices benefitted from the major melt-up fervor with BTC trading up to the high $118k area, liquidating over $1bln in crypto shorts for the biggest short-squeeze in recent memory.

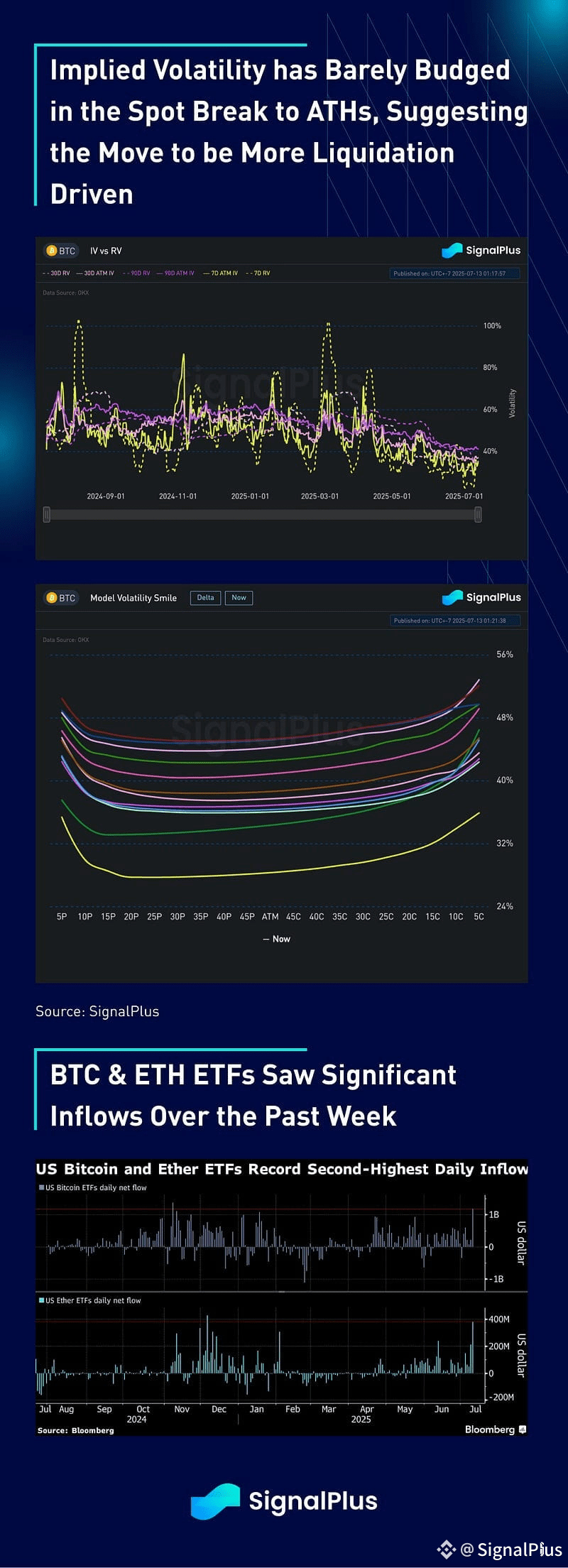

Interestingly, volatility has yet to make a big jump and remains pinned near cycle lows, suggesting little FOMO buying to the upside except for an understable tilt in vol skews as shorts scrambled for protection. The space continues to feel underowned with positions struggling to be rebuilt post the April shake-out, while TradFi ETF buying remains relentless and price insensitive as the mainstream narrative continues to strengthen.

Some observers have pointed to the recent mood-flip for Chinese regulators to be a catalyst for the rally, though we think it’s more of a symbolic gesture rather with substantial changes still some ways away. Underlying capital control restrictions remain an unresolved issue, while the recent passage of the HK stablecoin act suggests that pilot projects would likely be developed there first.

Looking ahead and at the risk of sounding like a broken record, market sentiment is likely to stay frothy into the summer, with the only real risk catalyst being a complete breakdown of tariff negotiations, but the ball is sitting with the President on how aggressive he wants to push his current hand.

In the meantime, enjoy the rally & try not to fight the market too much, as a quiet & boring market is often one of the most dangerous ones to short! Good luck and good trading.