Everyone is talking about OKX and Coinbase's compliance and the expulsion of unqualified customers, forgetting the path they took.

Let me say this: Crypto exchanges can be compliant in China.

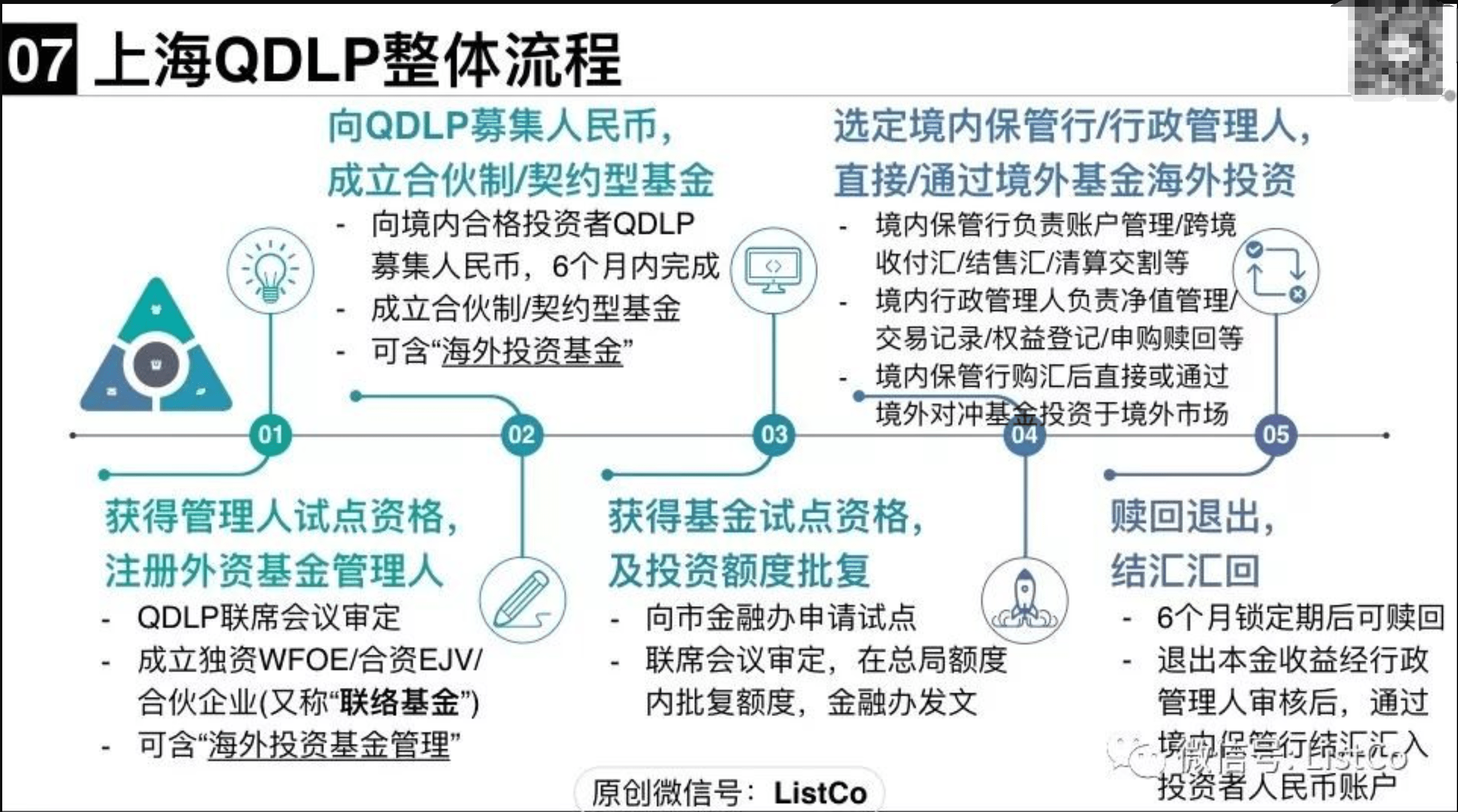

RMB subscription/redemption, overseas asset net value settled in RMB, no physical delivery is allowed.

In simple terms, it means using RMB to participate in crypto investments and earn profits, but you cannot take the spot assets out.

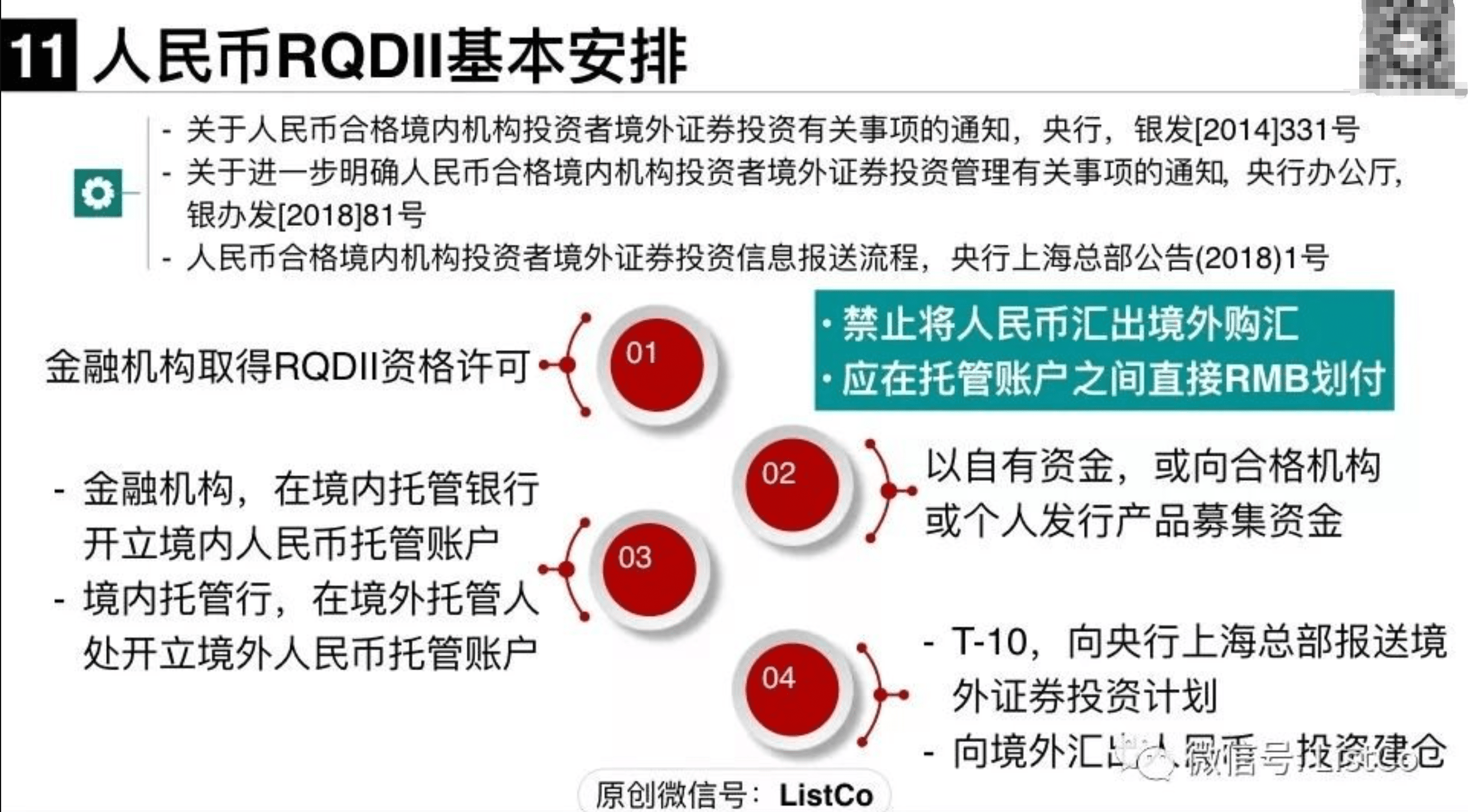

QDII, RQDII, and cross-border ETFs all use this scheme; I have bought E Fund's QDII for many years.

According to the current regulatory framework, it is completely possible to establish a closed entry and exit model for crypto exchanges that is the same as QDII funds and RMB-denominated cross-border ETFs.

Within China, deposit RMB → exchange for on-site stablecoins → conduct long and short trading on-site → ultimately settle profits and losses in RMB, and it is not allowed to withdraw crypto assets to an on-chain wallet.

QDII funds and US stock ETFs are also part of this scheme. You can participate in overseas asset investments using RMB, but physical delivery is not allowed.

Two scenarios for direct RMB investment in overseas financial products:

QDII securities investment funds

> Regulatory basis: (Qualified Domestic Institutional Investor overseas securities investment management measures) (CSRC Order No. 124) + State Administration of Foreign Exchange quota system

> Operation method: RMB subscription/redemption, overseas asset net value settled in RMB, no physical delivery is allowed

> Representative products: E Fund S&P 500 Index (QDII) 001592, Huaxia NASDAQ 100 (QDII) 000011

RMB-denominated cross-border ETF (RQDII/Shenzhen-Hong Kong Stock Connect ETF)

> Regulatory basis: (Cross-border ETF pilot notice) (CSRC/SAFE 2020)

> Operation method: On-site RMB trading, corresponding overseas fund shares are custodied in a custodian bank, and investors cannot withdraw overseas stocks

> Representative products: Huatai-PB NASDAQ 100 ETF 159941, Harvest Hang Seng Tech ETF 513130

If we apply this logic to crypto exchanges:

> RMB deposit → stablecoin: completed by licensed third-party custodians or clearing institutions, corresponding to the foreign exchange purchase by QDII fund custodians.

> On-site matching trading: Users can trade spot/derivatives, but can only circulate within the platform, similar to QDII and ETF which only trade on-site.

> RMB withdrawal: Settle profits and losses in RMB and return to the bank account, equivalent to QDII fund daily net value payment.

> Prohibition of on-chain transfers: Not providing on-chain withdrawal interfaces can satisfy the regulatory bottom line of not allowing physical delivery.

Question: Since the model is simple enough, why haven’t mainstream exchanges implemented it?

RMB in, RMB out, the design of not allowing withdrawals is not impossible in terms of regulations and practice; it is the crypto version of QDII/ETF.

Huobi hasn't done it, OKX hasn't done it, Binance hasn't done it, not even HashKey has done it.

The only reason I can think of is that the qualification threshold is high.

To obtain QDII + custody + clearing licenses, you need to meet multiple compliance requirements from the central bank, foreign exchange management bureau, and securities regulatory commission.

But with all these years of the Chinese crypto industry being half-hearted, is it really that difficult to clear these hurdles?

Is it that you can't shed the long shirt of decentralized fundamentalism, or is it that regulation won't let go?