Original title: Crypto & Blockchain Venture Capital - Q1 2025

Original author: Alex Thorn

Original source: https://www.galaxy.com/

Translated by: Daisy, Mars Finance

introduction

Cryptocurrency venture capital remains below the previous bull market level. Although the investment amount this quarter hit a new high since the third quarter of 2022, more than 40% of the funds came from a single investment of US$2 billion in Binance by the UAE sovereign-linked fund MGX. Macroeconomic concerns continue to suppress allocators' interest in venture capital, and the cryptocurrency market continues to show a differentiated trend - Bitcoin is particularly strong, while altcoins and basic platforms in the previously popular crypto venture capital field are relatively weak.

Even without Binance, overall startup investment is still above the trough in 2023. Trading, infrastructure, tokenization, payments, and artificial intelligence remain hot. Given the new U.S. administration’s push for bitcoin, cryptocurrency, and blockchain technology, the country’s long-standing dominance in the field may be further strengthened.

Core Data

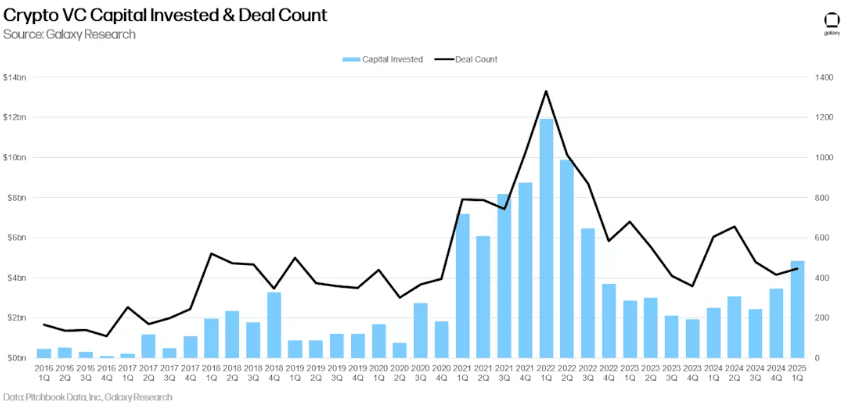

• In Q1 2025, venture capital investment into cryptocurrency startups totaled $4.9 billion (up 40% QoQ) in 446 deals (up 7.5% QoQ)

• Late-stage projects attracted the majority of funding (65%), while early-stage projects accounted for 35%. This is the first time since the third quarter of 2020 that late-stage investment has surpassed early-stage investment

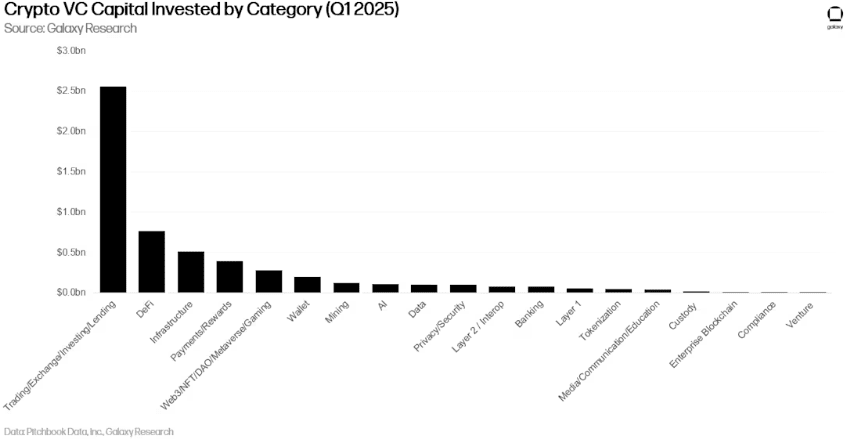

• Trading companies ranked first in terms of funding (Binance received $2 billion in funding from MGX), followed by DeFi protocols ($763 million) and infrastructure companies ($506 million)

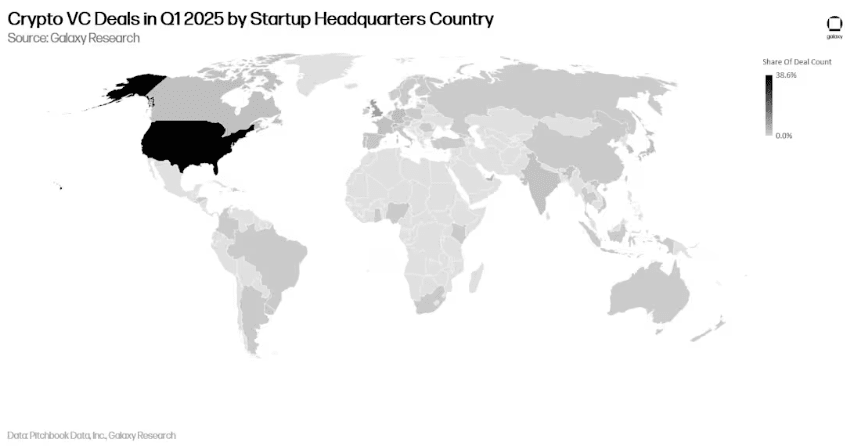

• Influenced by Binance financing, Malta-based companies received the highest proportion of investment (36.8%), followed by the United States and Hong Kong. In terms of transaction volume, the United States leads with 38.6%, followed by the United Kingdom and Singapore.

• In terms of fundraising, investors allocated $1.9 billion to 18 new crypto venture funds

Venture Capital

Number of transactions and investment amount

In Q1 2025, venture capitalists invested $4.8 billion (up 54% QoQ) in startups focused on cryptocurrencies and blockchain, across 446 deals (up 7.5% QoQ).

While Q1 2025 was the highest quarter in terms of investment since Q3 2022, one large deal accounted for more than 40% of the total: MGX invested $2 billion in Binance. Excluding this deal, total investment in Q1 2025 would have been $2.8 billion (down 20% from Q4 2024).

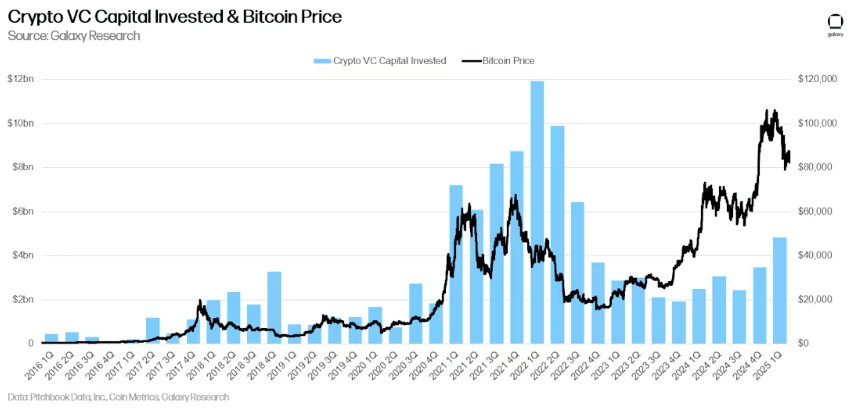

Investment amount and Bitcoin price

The cyclical correlation between Bitcoin prices and investment in crypto startups over the past few years has struggled to recover over the past year. Since January 2023, Bitcoin prices have risen sharply while venture capital activity has failed to grow in tandem. This divergence is partly explained by allocators’ lackluster interest in crypto venture (and the venture capital sector as a whole), as well as the current crypto market narrative that favors Bitcoin over many of the hot concepts of 2021. While the recovery in investment in the first quarter of 2025 has somewhat reestablished this correlation, more than 40% of the investment volume in that quarter involved a large strategic investment in Binance.

Investment by stage

In the first quarter of 2025, 65% of the funds went to late-stage companies, while 35% went to early-stage companies. This is the first time that late-stage investment has exceeded early-stage since the first quarter of 2021. If MGX's $2 billion investment in Binance is excluded, early-stage investment will still dominate the quarter.

In terms of the number of deals, the share of pre-seed deals has slightly decreased, but remains healthy compared to previous cycles. We measure the activity of entrepreneurial activity by tracking the share of pre-seed deals. In the first quarter of 2025, the share of late-stage deals was higher, reflecting the overall maturity of the market.

Investment by sector

In our categories, trading/exchange/investing/lending companies raised the most crypto venture capital in Q1 2025, totaling $2.55 billion (47.9%), mainly due to MGX's $2 billion investment in Binance. If this transaction is excluded, DeFi will lead with $763 million in funding.

Over the past two quarters, funding in the DeFi and Infrastructure sectors has surpassed that of the Games/Web3/NFT/DAO/Metaverse/Games categories, which have now slipped to fourth place in terms of investment dollars.

Over the past two quarters, the DeFi and Infrastructure sectors have received more funding than the Games/Web3/NFT/DAO/Metaverse/Games category, which has now slipped to fourth place in funding share.

In terms of transaction volume, the Web3/NFT/DAO/Metaverse/Game category leads with 16% (73 transactions), followed by companies in the Trading/Exchange/Investment/Lending category, which completed 62 transactions in total.

In the first quarter of 2025, the number of transactions in the Transaction, Artificial Intelligence, and Payment/Rewards categories increased, while the Web3 category continued its downward trend that had lasted for several consecutive quarters.

Investment by stage and category

By breaking down the investment amount and number of deals by category and stage, we can get a clearer picture of what types of companies are raising funds in each category. In the first quarter of 2025, the vast majority of funds in the Web3/DAO/NFT/Metaverse, Layer 2, and Layer 1 sectors went to early-stage companies and projects. In contrast, the majority of crypto venture capital funds in the DeFi, Trading/Exchanges/Investing/Lending, and Mining sectors went to late-stage companies. This is expected given the relative maturity of the latter compared to the former.

Analyzing the distribution of investment amounts at different stages in each category can reveal the relative maturity of various investment opportunities.

Similar to cryptocurrency venture capital investment in Q4 2024, a significant portion of deals completed in Q1 2025 involved early-stage companies.

By analyzing the proportion of deals at different stages within each category, we can gain insight into the stage of development of each investable category.

Investment by Geographic Location

In the first quarter of 2025, 38.6% of deals involved companies headquartered in the United States. The United Kingdom followed with 8.6%, Singapore with 6.4%, and the United Arab Emirates with 4.4%.

Malta-based companies led in terms of investment amount, accounting for 36.8%, thanks entirely to MGX's $2 billion investment in Binance. The United States followed closely at 24.7%, Hong Kong at 13.4%, the United Kingdom at 6.6%, and Singapore at 3.2%.

Investment by year of incorporation

Companies founded in 2017 (primarily Binance) raised the most funds, while companies founded in 2024 took the top spot in terms of transaction number.

Venture Fund Financing Trends

Despite an increase in the number of new funds and the amount of funds allocated in the first quarter of 2025 compared to the same period last year, the fundraising environment for cryptocurrency venture funds remains challenging. The turbulence in the macroeconomic environment and the cryptocurrency market in 2022-2023 continued to prevent some capital allocators from returning to the level of commitment to cryptocurrency venture investors in early 2021-2022. The recent increase in attention to the field of artificial intelligence has also diverted some funds that were originally intended for crypto investments. In the first quarter of 2025, the total amount of venture funds focused on crypto rebounded to $1.9 billion, which was the same as the second quarter of 2024, and together became the highest quarterly fundraising scale since the third quarter of 2023.

Calculated on an annualized basis, the first quarter of 2025 marked a good start for the whole year, and the current growth rate is expected to exceed the total amount of funds raised in 2024.

Compared with the first quarter of 2024, the number of newly established funds and the scale of fundraising have both increased year-on-year, and the average fundraising amount of a single fund has also risen to US$130 million, but the median is still declining. The increase in this average is mainly due to the large-scale fundraising of institutions such as Ribbit Capital, Foundation Capital and Somnia Ecosystem Fund.

Summarize

Sentiment is improving and investment activity is increasing, but both remain well below all-time highs. While Bitcoin continues to perform strongly, liquidity prices for altcoins remain subdued. While funding for crypto startups in Q1 2025 was the highest since Q3 2022, nearly half of the funding came from a late-stage deal between Binance and Abu Dhabi fund MGX (a UAE government-linked fund). Excluding this deal, funding in Q1 2025 would fall to approximately $2.6 billion, the lowest level since Q3 2024 and close to a four-year low. Venture capital activity was highly correlated with crypto asset liquidity prices during the bull cycles of 2017 and 2021, but investment activity has remained subdued over the past two years despite rising crypto prices. This stagnation in venture capital is due to a combination of factors: the decline in the appeal of once-hot crypto investment areas such as gaming, NFTs, and Web3, competition for investment funds from AI startups, and a high interest rate environment that has suppressed venture capital allocation willingness.

For the first time since Q3 2020, late-stage deals dominated. While the surge in late-stage dollars was almost entirely driven by Abu Dhabi MGX’s large investment in Binance, late-stage companies also surpassed pre-seed in deal volume for the first time. Pre-seed deals continue to decline as the industry matures. The golden age of pre-seed investing in crypto may be over as traditional institutions gradually adopt crypto technology and a large number of venture-backed companies have achieved market fit.

Spot ETP products may put pressure on funds and start-ups. Several major investments by allocators in US Bitcoin spot ETP products indicate that some large investors (pension funds, endowment funds, hedge funds, etc.) may be deploying this field through highly liquid financial products rather than choosing early-stage venture capital. The market's interest in Ethereum spot ETPs is beginning to heat up. If this trend continues, new ETP products covering other Layer 1 blockchains may emerge. Market demand for areas such as DeFi or Web3 may flow to ETP products rather than venture capital systems.

Fund managers still face a tough environment. Although the amount of funds allocated in the first quarter of 2025 increased slightly month-on-month, the number of newly established funds has declined for two consecutive quarters and remained at a five-year low. Macroeconomic factors continue to constrain allocators, but substantial changes in the regulatory environment may rekindle their interest in this field.

The United States continues to dominate the crypto startup ecosystem. Despite facing an extremely complex and hostile regulatory environment, companies and projects headquartered in the United States still account for the majority of transactions and investment amounts. The new administration and Congress have begun to implement the most pro-cryptocurrency policies in history, involving multiple dimensions. We expect the United States' dominance to increase further - especially if regulatory matters such as stablecoin frameworks and market structure legislation are settled as expected, which will encourage traditional US financial institutions to truly enter the field.