We are coming up in the first 100 days of Trump's 2nd presidency, but the geopolitical world already feels unrecognizable versus just a few months ago. It's no longer a question of whether the US will decouple with the world, but how, and the US's 'exhorbitant privilege' when it comes to the USD reserve status is legitimately being challenged.Correlations are breaking, capital flows are reversing, Bitcoin is (finally) starting to diverge from equities, the President threatening to treat the FOMC Chair like a participant at the 'Apprentice', and the elephant US endowments are dumping illiquid private equity during one of the toughest times in the industry. Have we truly arrived at an inflection point in financial history?

Dollar-Based Safe Haven

The top of mind questions on everyone's mind right now - have USD and US Treasuries lost their long-held position and safe-havens? And has Trump inflicted irrecoverable damage to the post-war global security and financial infrastructure?

Investors have been fleeing the USD for the EUR and JPY, and selling US equities in favour of Chinese stocks. Uncertainty over the end of US exceptionalism has led to the USD falling to a 3-year low, and last week's Michigan Sentiment index falling to a near record low against rising inflation concerns.

Foreign investors have also dramatically slowed their investing in US equities, with ETF flows dwindling to near zero over the past 3 months.

Macro correlations are also breaking with the JPY seeing a substantial rally (~140 on USDJPY), but against a rising Nikkei, as the Yen rally is now a function of the weakening USD, rather than a conventional carry-unwind.

The most important 'known unknown' question surrounds US treasuries, where 10y yields have risen against a backdrop of weaker USD, equities, and the underlying economy, making the bond move seem 'EM-like'. While we don't subscribe to that call, US financial conditions are tightening and bonds are not playing its role as a safe-haven hedge. We don't see a clean resolution to this until we see a more conclusive dialing down of Trump's precarious tit-for-tat tariff negotiations.

Foreign Investors Have Been Net Sellers of Treasuries Over the Past 6 Months, with Central Banks Likely Liquidating their USD Positions to Defend Their Own Currency Moves

Despite the sell-off, US equities still enjoy a substantial premium over EM and global competitors, with the latter treading water (in terms of valuation multiples) ever since the GFC. As the trade war is unlikely to benefit any nation as a net winner, we doubt that foreign multiples will close the gap against the US on their own. In that case, a US 'catch-down' is probably not a great development given the implied wealth destruction.

Markets need to be careful with what they wish for.

Deal or No Deal

The tariff drama continues with President Trump flip-flopping between overt intimidation vs proclamations of imminent 'deals' with former partners & allies. Risk assets initially rallied on Friday as Trump stated that he was "very confident on trade deal with EU... Will make good deal with China...Everybody's on my priority list.", but that saw very little follow-through as the 1st trade deal remains elusive.

We continue to believe that the headline tariffs will matter less than the 'floor rates' that will be assigned on the initial agreements, and the fact that the administration is still unable to articulate a deal with Japan remains concerning. Have the negotiators even defined the goal posts yet?

Nevertheless, following President Xi's recent visa to SEA, the US meetings should pick up this week with Japan, South Korea, Thailand, and India confirmed to be holding sideline trade meetings during the IMF Spring meetings. The UK is also expected to reach a trade deal within 3 weeks based on local reports. Keep your eyes peeled for any positive trade progress over these next few weeks.

The Apprentice, Season 2

"Jerome Powell of the Fed, who is always TOO LATE AND WRONG, yesterday issued a report which was another, and typical, complete 'mess!' ... Powell’s termination cannot come fast enough!"

"The Fed really owes it to the American people to get interest rates down. That's the only thing he's good for... I am not happy with him. If I want him out of there he'll be out real fast believe me."

-- Trump via Truth Social, 17April2025

If we had a Fed chairman that understood what he was doing, interest rates would be coming down. He should bring them down."

-- Trump at the Oval Office on 19April2025

"With these costs turning so nicely downward, just what i predicted they would do, there can be almost be no inflation, but there can be a SLOWING of the economy unless Mr. Too Late, a major loser, lowers interest rates, NOW. Europe has already "lowered" seven times. Powell has always been "To Late,", except when it came to the Election period when he lowered in order to help Sleepy JOe Biden, later Kamala, get elected."

-- Trump via Truth Social, 21April2025

Contrary to earlier proclamations that the administration was ready to endure some economic pain in response to the tariff war, Trump has reverted to his old playbook of bashing the Fed for not lowering rates fast enough. While we appreciate the wisdom of jawboning down longer maturity rates as financial conditions ease, we fail to see the benefit of urging the Fed to cut against the backdrop of softer USD and import-led inflation.

The market would seem to agree, as the SPX traded down -2% on Monday with yields rising once again as participants didn't appreciate the latest threats.

On the other hand, Fed Chair Powell has been taking the situation in stride and has been professional in response, staying firm on the line of Fed independence.

Fed's independence is "very widely understood and supported in Washington and in Congress where it really matters."

"People can say whatever they want. That's fine. That's not a problem, but we will do what we do strictly without consideration of political or any other extraneous factors"

-- Powell at the Economic Club of Chicago, 17Apr2025

Nevertheless, the rates market pricing in substantially more rates before year end vs Fed projections (4 vs 2), due to concerns of an incoming recession. We don't think it's wise for the President to pressure the Fed anymore on this front, though crazier things have been said over the past 2 months.

Looming Slowdown

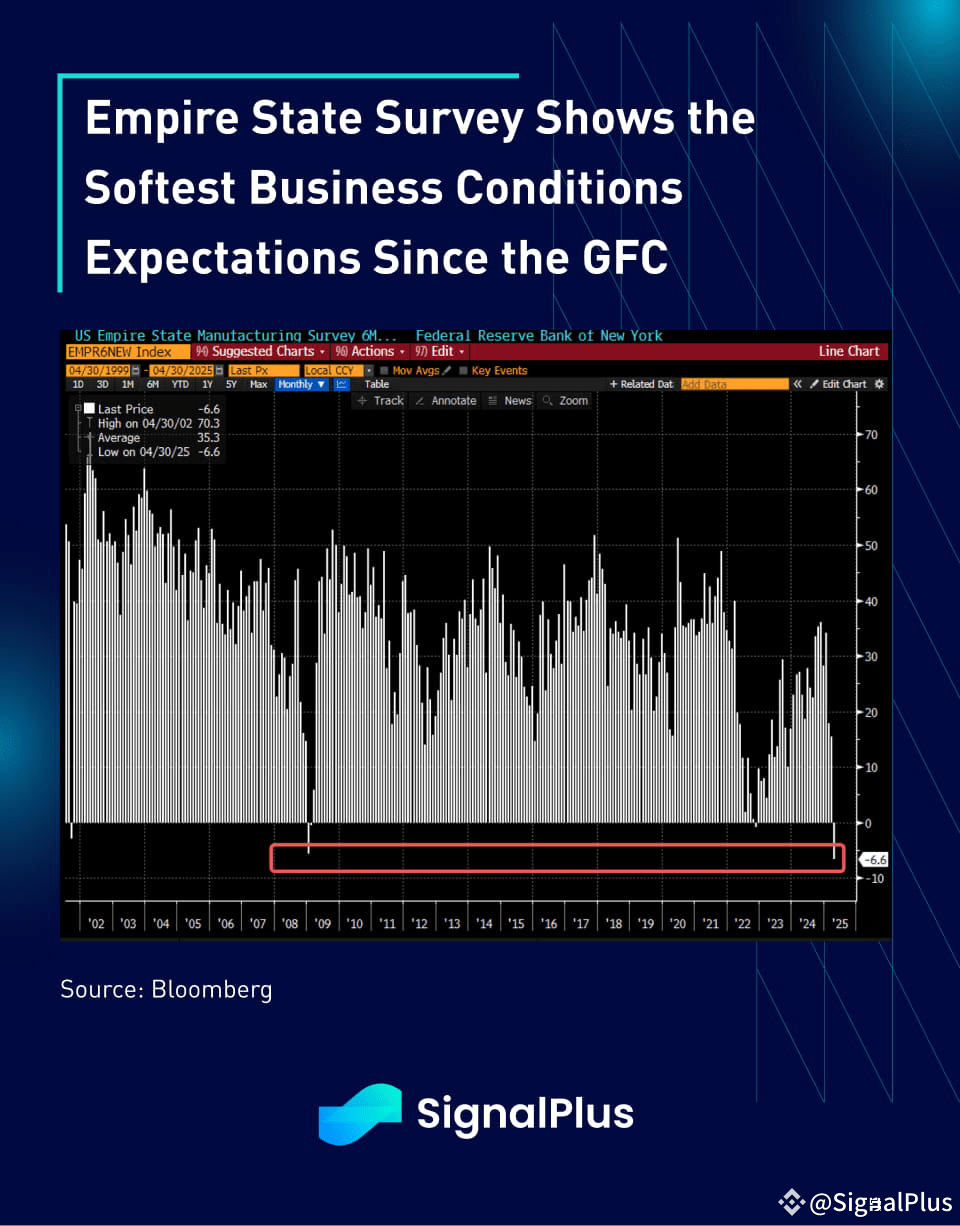

By certain measures, the current economic policy uncertainty is at the highest levels on record, surpassing even the initial covid period. This is filtering down into a substantial drop in the business outlook, flagged most recently by the Empire State Survey, which showed activity expectations falling to the lowest levels in over a decade.

The sub-indicators showed a similar picture, with forward looking shipments and capex indicators falling precipitously, while prices paid are trending noticeably higher. Similarly, corporate earnings revisions have been ratcheting down, casting a long shadow over equity markets as earnings growth compresses.

Poison Pill

Although markets have been conditioned to follow what officials say, the 'Trump 2.0 trades' have been a disaster as most of the administration's narratives have led to significant losses. A picture speaks a thousand words:

Once bitten, twice shy. It might take a bit of work for markets to take Trump's words at face value again in the near term.

Bravery or Fodder?

While hedge funds have been busy de-risking in 2025 after suffering significant losses, retail investors have been bravely bucking the trend with the levered Nasdaq ETF seeing record-breaking inflows over the past 2 weeks.

It's well documented that retail and passive money have been massively outperforming managed capital and professional fund managers over the past 5 years - will history repeat itself one more time, as doubtful as it might seem at the moment?

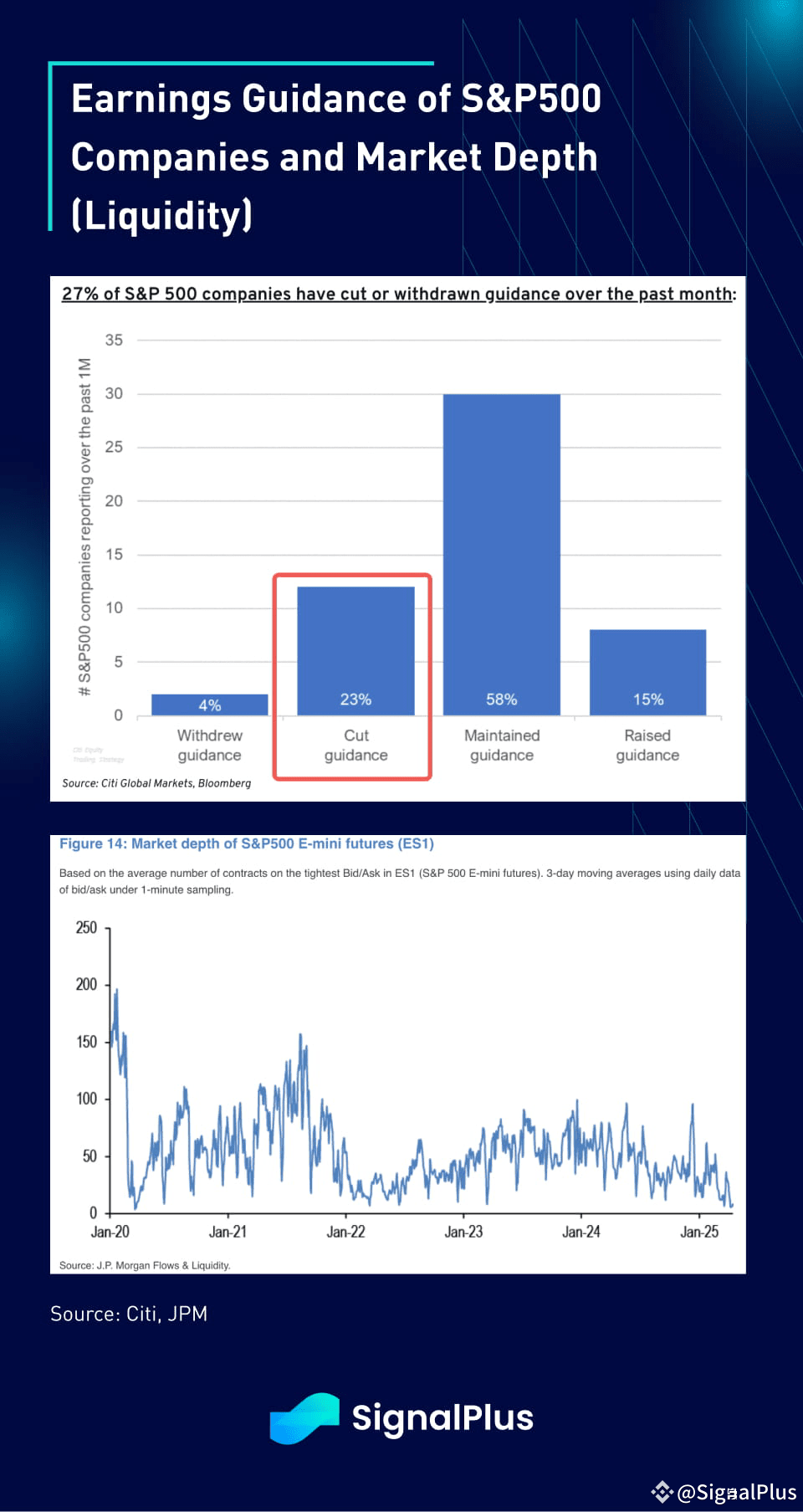

The Retail Buying is Happening at a Time When a Considerable % of Companies have Cut Earnings Guidance with SPX Market Depth (Liquidity) Near All Time Lows

All That's Glitter IS Gold

The yellow metal is making up a decade of underperformance in a hurry, with spot prices rallying by 150% since the start of 2024, and the recent momentum going vertical as investors scramble for capital safety in this upside-down world.

Ironically enough, President Trump tweeted an auspicious comment on "he who has the gold makes the rules", likely referring to his negotiation tactics, which further spiked spot prices to a new record high at above 3,400.

Furthermore, data shows that gold has been deriving most of its rally during the Asian hours, suggesting possible central bank and official flows getting out of USD into alternative safe havens. The USD decoupling does seem to be more pronounced than previous episodes...

BTC Narrative, Revisited. No Longer Just Nasdaq, but Not Quite Gold (Yet).

One of the possible ramifications of the US decoupling is a revisit to the long-term BTC bull case as a store of value. While we have also been critquing BTC as a levered Nasdaq proxy over the past year, it has finally started to show some signs of its own decoupling away from equity markets. Bitcoin is close to regaining the $90k area despite a poor week for US equities across the board.

Before we get too excited, BTC is still lagging spot gold quite substantially YTD, so the best we can say is it's turning into some hybrid of gold + levered Nasdaq at the moment, which is a substantial upgrade than being just a glorified TQQQ proxy.

JPM data shows a spike in gold futures positioning while BTC inflows have flatlined. Keep an eye out for any rebound to finally justify BTC's promise as a hedging alternative.

US Endowments Mini-Shock

Finally, outside of his international saber-rattling, the Trump administration has been wagering a domestic fight with its own US endowments, most notably with Harvard, which is having potentially negative spillovers into market liquidity.

Reports suggest that the Yale endowment will be selling ~US$6bln of its private equity portfolio into an extremely weak private market that is struggling with record low liquidity exits and poor returns.

Non-domestic observers might not be aware of the size and importance of the US endowment system, but they are collectively one of the most critical investors and 'permanent' holders across capital markets. Will a continued politicized battle lead to a slowdown in their reinvestments, or a change in capital mix?

Never a dull moment with this administration. The times they are a-changin' indeed...

Good luck and good trading this week friends!