The U.S. Bureau of Labor Statistics released the latest Consumer Price Index (CPI) last night (10th). The report showed that the U.S. CPI month-on-month in March unexpectedly fell by 0.1%, marking the first decline in nearly five years, lower than the market expectation of a 0.1% increase and contrasting with February's 0.2% increase.

In terms of year-on-year growth rate, the CPI eased from 2.8% in February to 2.4%, slightly below the market expectation of 2.5% to 2.6%; at the same time, the core CPI (excluding food and energy prices) rose 0.1% month-on-month, below the expected 0.3%. The year-on-year growth rate fell from 3.0% to 2.8%, also below the market expectation of 3.0%.

Latest data suggests that inflation pressure in the U.S. seems to have eased in March. However, the core CPI remains above the Fed's long-term target of 2%, indicating that inflation trends have not completely dissipated, and the potential pressure on the economy from the global trade barriers initiated by Trump still exists.

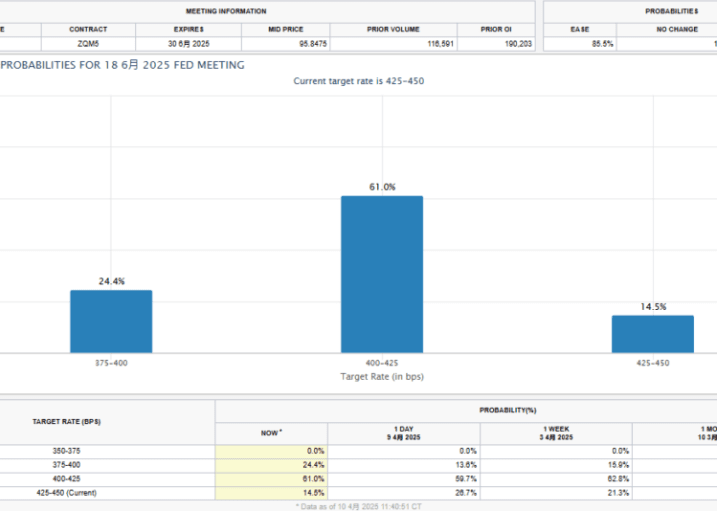

Expectations for a Fed rate cut in June have risen.

After the CPI data was released, market expectations for a Fed rate cut changed. According to the latest data from the CME Group's FedWatch tool, while the current market believes the Fed is likely to maintain the current interest rate in May (69.1%), for the June interest rate decision, the market now sees the probability of a 25 basis point cut has risen from 49.7% a month ago to 61%, while the probability of maintaining the rate in June is only 14.5%, even lower than the 24.4% probability of a 50 basis point cut in June.

However, it is still worth noting that Federal Reserve Chairman Jerome Powell emphasized in a recent speech that the Fed is "not in a hurry to adjust its policy stance" and will closely monitor the impact of external factors like tariffs on inflation. As a result, some analysts believe that the slowdown in inflation may prompt the Fed to start cutting interest rates mid-year, but the extent might only be 25 basis points rather than a more aggressive 50 basis points.

Austan Goolsbee, president of the Chicago Federal Reserve Bank, also believes that Trump's tariff policy is much larger than expected and quite unstable, suggesting that the Fed should watch and wait, aiming to find the relationship between tariffs and inflation rather than rushing to conclusions.

All four major U.S. stock indexes are in the red.

Although the CPI data unexpectedly showed a slowdown in inflation, it may be due to a memo released by the White House indicating that the tariff rate on Chinese imports has now actually reached 145%, in addition to the 125% reciprocal tariffs, which include the 20% tariff imposed by Trump earlier this year on Chinese imports due to fentanyl.

The shadow of the U.S.-China trade war continues to loom over the market, with U.S. stocks significantly retracing on the 10th:

The Dow Jones Industrial Average plummeted by 1,014.79 points, or 2.50%, closing at 39,593.66 points.

The S&P 500 index fell by 188.85 points, or 3.46%, closing at 5,268.05 points.

The Nasdaq index dropped by 737.66 points, or 4.31%, closing at 16,387.31 points.

The Philadelphia Semiconductor Index, which set a record for the largest single-day gain yesterday, also plummeted by 337.15 points, or 7.97%, closing at 3,893.30 points.

Bitcoin plummeted to $78,000.

The cryptocurrency market has also been unable to escape, with the market, which had rebounded strongly on the 9th, experiencing a drop last night alongside the decline in U.S. stocks. Bitcoin plummeted from $81,840 to a low of $78,462, nearly wiping out all gains from the previous day.

At the time of writing, it reports $79,569, down 3.67% in the last 24 hours.

Among the other top ten tokens, Ethereum is the weakest performer due to multiple factors, including several large whale sell-offs and the decoupling of sUSD. Earlier, it briefly fell below $1,500, reporting $1,525 before the deadline, down 7.04% in the last 24 hours.

Economic Outlook for the U.S. Under Tariff Impacts

Although Trump has now indicated a temporary suspension of reciprocal tariffs for 90 days for multiple countries, China and the U.S. remain at odds. Therefore, although the March CPI shows a retreat in inflation, experts still warn that the lagging effects of tariffs may push prices higher in the coming months, especially in the fields of imported consumer goods and capital goods.

Goldman Sachs analysts have predicted that if tariffs continue, the core CPI could rise to around 3% by the end of the year, putting pressure on consumer purchasing power and business costs. Additionally, the uncertainty caused by tariffs has led to a decrease in corporate investment willingness, with economic growth expected to slow from 2.8% in 2024 to 1.7%. This concern of "low growth with high inflation" may plunge the U.S. economy into a stagflation predicament. In response, Fitch's chief economist Brian Coulton also stated:

The decline in core inflation in March will surely be welcomed by the Fed, but we know that before the tariff increase, companies had already absorbed a large amount of imports in January and February, so the impact of the tariff increase on consumer goods prices has yet to be reflected.

Therefore, the current market decline may be due to the uncertainty brought by tariffs, affecting investors' judgments—despite the slowdown in U.S. inflation, the impact of tariffs has yet to be reflected in economic data, and the market may prefer to adopt a cautious wait-and-see approach.