Before the opening of the U.S. stock market on Friday, April 4, the U.S. Department of Labor Statistics released the non-farm employment report. The increase in non-farm employment in March was better than expected, but the unemployment rate rose further to 4.2 from the previous month.

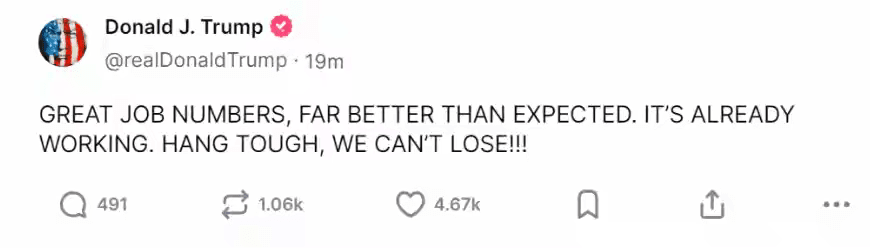

After the data was released, US President Trump said on social media that the March employment data was better than expected. He wrote that the employment data was very good, much better than expected, and it has worked. Hang in there, we won't lose.

US non-farm payrolls data was better than expected.

The non-farm payrolls report showed that the number of non-farm payrolls in the United States increased by 228,000 in March, compared with an estimated increase of 140,000. The average hourly wage in the United States rose by 0.3% month-on-month in March.

But investors should note that although the United States released a relatively strong employment report, the rising inflation risk in the United States cannot be ignored.

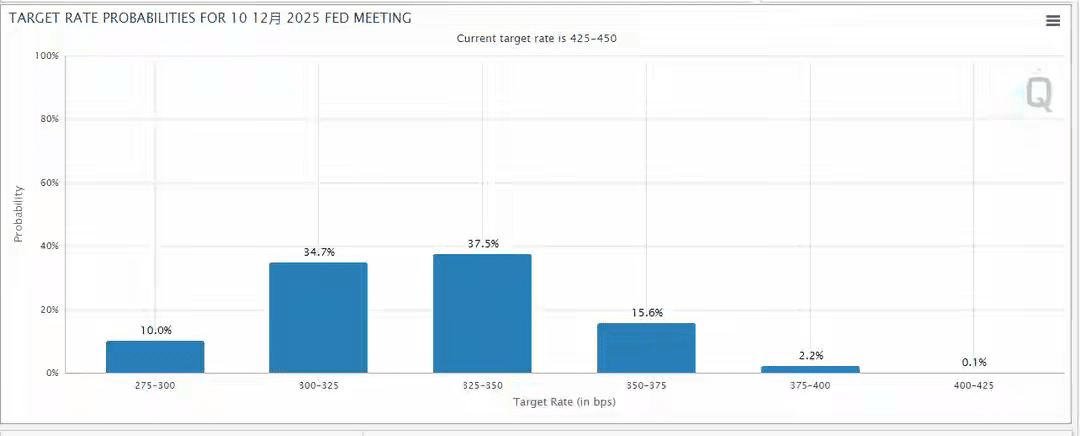

The market expects the Fed to cut interest rates 4-5 times this year. According to CME's Fed Watch tool, FEDWATCH, after the release of the non-farm report, the market expects the Fed to have a 37.5% chance of cutting interest rates four times and a 34.7% chance of cutting interest rates five times this year.

Therefore, this data is very important for the global financial market. Increasing employment and maintaining inflation are the core tasks of the Federal Reserve. In order to accomplish this task, the Federal Reserve generally uses interest rate hikes or interest rate cuts.

The non-farm payrolls data is produced by the Bureau of Labor Statistics of the U.S. Department of Labor. This data is official data and is released on the first Friday of each month, which has the greatest impact on the market.

Non-farm payrolls data is released on the first Friday of each month, at 20:30 Beijing time (April to October) and 21:30 Beijing time (November to March). Non-farm payrolls data can greatly affect the value of the dollar in the currency market.

Non-farm payrolls data is one of the important indicators reflecting the state of the U.S. labor market. It has a significant impact on financial markets and monetary policy. The increase in employment this time was higher than market expectations, and the unemployment rate rose slightly.

A vibrant employment report can drive interest rates higher, making the dollar more attractive to foreign investors. Non-farm payrolls data objectively reflects the rise and fall of the U.S. economy. In the exchange rate, the dollar is extremely sensitive to this data. Higher than expected is good for the dollar, and lower than expected is bad for the dollar.

The March non-farm payrolls data showed strong performance. After the data was released, the US dollar index rose in the short term and then continued to rise, indicating a short-term recovery in the US market's confidence in the dollar. The gold price was under obvious pressure. The current gold price once fell by $12 to $3088.13 per ounce.

Repricing of Fed rate cut expectations.

The core focus of this non-farm report is how it affects the market's judgment on the Federal Reserve's monetary policy.

At the meeting on March 19, Federal Reserve Chairman Powell said that the economy and labor market were in a stable state and there was no urgency for policy adjustments. However, the better-than-expected performance of the non-farm data in March provided new support for this position.

Employment increased by 228,000, far exceeding expectations, and the private sector contributed 209,000, showing that corporate hiring intentions remain strong. From a fundamental perspective, this report weakened the market's expectations for a rate cut in May.

Judging from the market trend, the strong performance of non-agricultural data boosted the US dollar in the short term, but failed to reverse the downward trend of the US dollar. In the long run, this data provides more room for observation for the Federal Reserve.

Powell has said that if the labor market unexpectedly weakens, policy may turn to easing. But current data shows that the labor market is still resilient, and the Fed may continue to wait and see, waiting for the actual impact of the tariff remarks to become clear.

Although the market's expectations for a rate cut in June have not been shaken, the window for a rate cut in May is closing. Overall, the market will usher in a new round of directional choices under the dual influence of data digestion and Powell's speech.