“April 2nd is going to be liberation day for America. We’ve been ripped off by every country in the world, friend and foe,” — Trump said in the Oval Office Friday.

Markets settled down over the past week as risk assets steadied after a few weeks of extreme selling pressures, and the Trump administration behaving in a relatively muted manner as of late. However, in a prepared speech from the Oval Office on Friday, Trump stated that they are preparing a “Liberation Day” tariff announcement on April 2nd (next Wed), where the US will be unveiling their reciprocal tariffs as retribution for the trade actions taken by other countries & allies.

Expectations are for tariff announcements to be more focused and immediate in nature, and only countries where the US runs a trade surplus with and have no imposed tariffs on the US will be spared, according to a WH official. Furthermore, Trump officials appeared to have softened some of their narrative recently as they acknowledged that the list of target countries may not be universal, and that certain existing tariffs (eg. Steel) might not be cumulative. Naturally, the political focus this week will be on preliminary details on the ‘America First’ review ahead of the April release, along with US/Russia talk on Mondays and ongoing Turkey/Isareal developments.

“It’s 15% of the countries, but it’s a huge amount of our trading volume,” referring to it as the “dirty 15” and signaling they are the target. — Treasury Secretary Bessent via Bloomberg

Regardless of how trade negotiations turn out, the damage to market sentiment has been done as tariff mentions have dominated corporate earnings calls YTD. Trade sensitive sectors have fallen by ~15% since the January peaks, and long momentum factors have seen some of the sharpest unwinds in 40 years, erasing 2 years of gains in just 3 weeks.

In response, professional money managers have retreated from their US stock holdings at the fastest pace on record, with Europe, UK, and China being the main benefactors thanks to their renewed fiscal spending aspirations.

Similarly, on the positioning side, managers have crowded into ‘low vol’ positions at some of the fastest pace on record, with recent performance rising above 92% percentile range and funds have taken on max defensive positions.

One positive is that retail remains to be equity ‘hodlers’, and have in fact been adding on recent dips as call option volumes and margin account balances remain elevated. Retail accounts have done very well and often outperformed their professional peers in recent years. Will their hot streak continue?

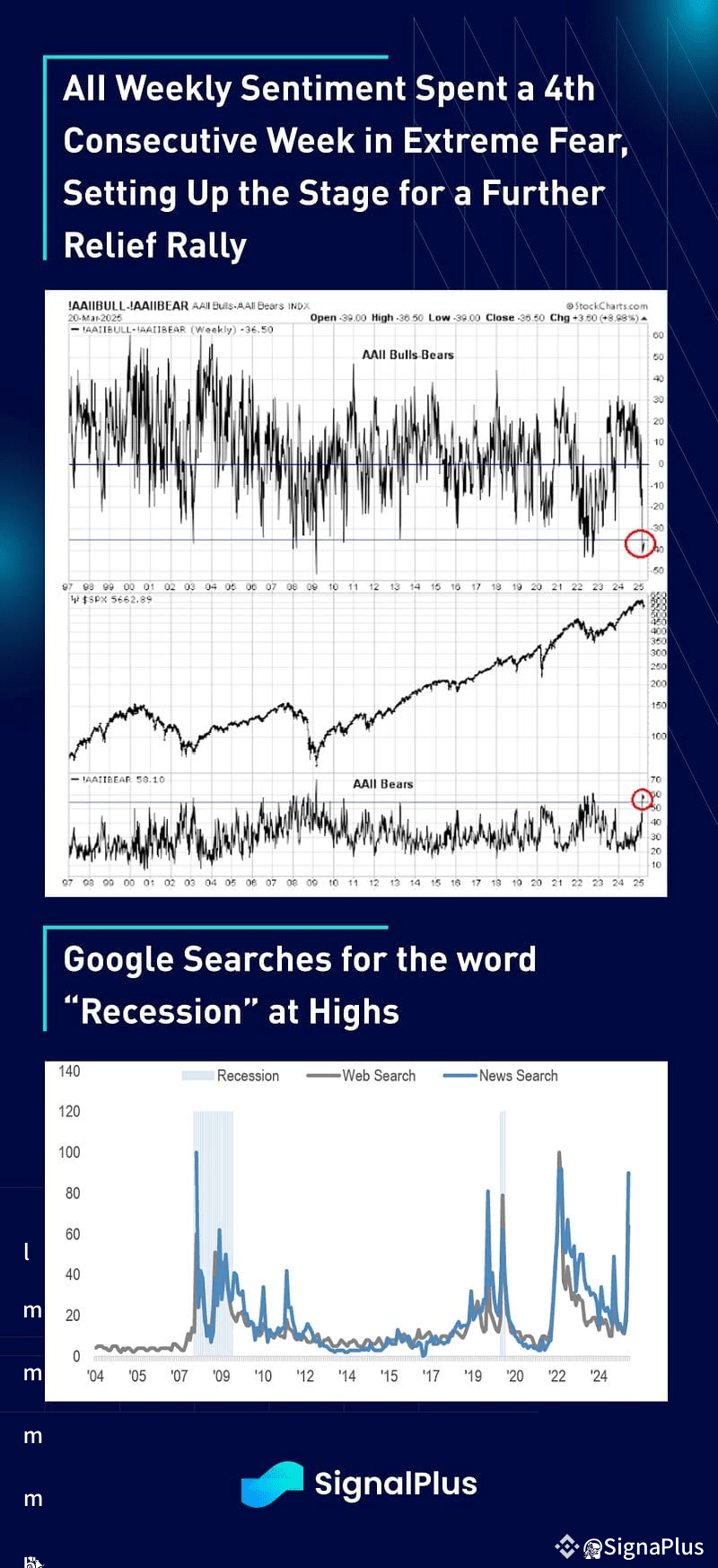

Sentiment remains oversold and at extreme levels, setting things up for a risk squeeze as a contrarian move in the interim. Google searches for the word ‘recession’ is also near multi year highs (similar to Covid / GFC), providing further support for a relief rally higher in the near-term.

Most importantly, US ‘hard’ economic data remains robust and in contrast with the soft sentiment, suggesting an over-extrapolation of the current weakness versus underlying fundamentals. In recent years, macro observers have generally been more precarious in their assessments than the actual reality, and we are of the view that the underlying economy remains stronger than feared as well.

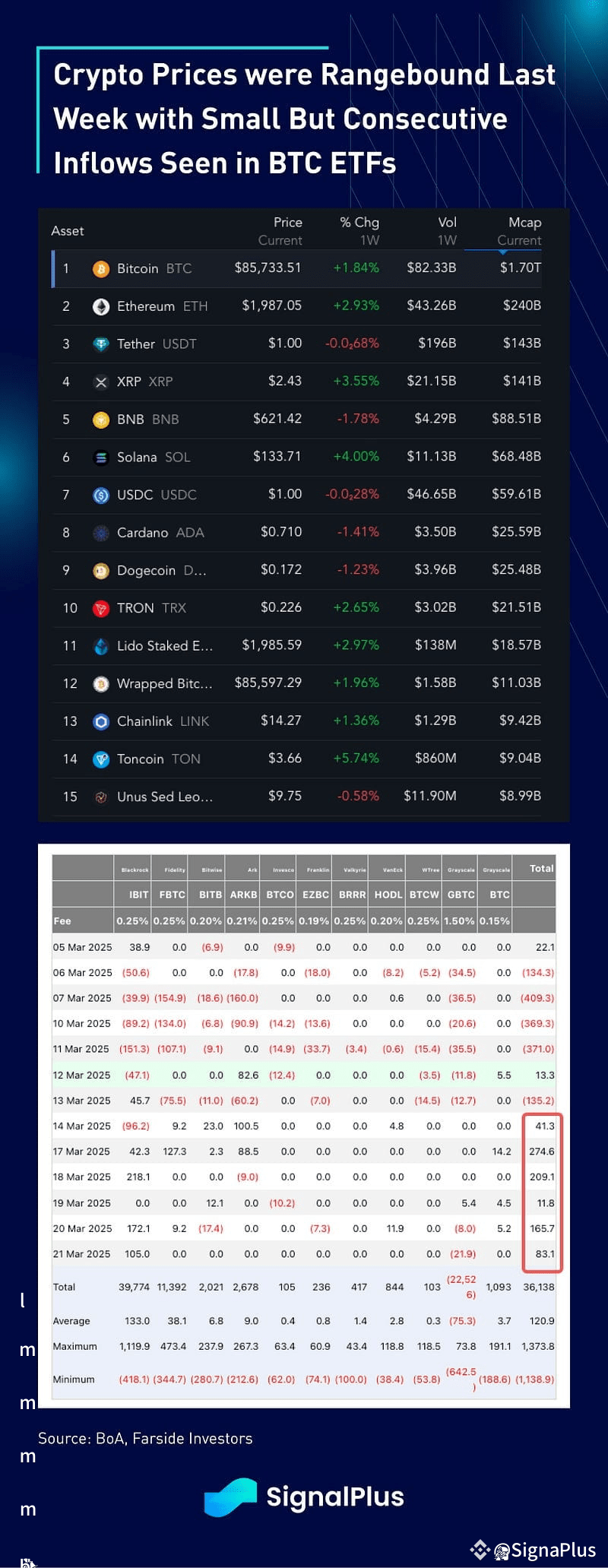

Crypto markets had a similar quiet week, with prices largely rangebound and rebounding off recent lows as a mirror move of the equity action. A recent BoA survey on the most crowded trades saw a similar dip in crypto longs, following the recent capital exodus out of US equities. ETF inflows have been positive over the past 6 consecutive sessions, albeit in very muted volumes.

Technically speaking, prices remain on a negative downward trend but are stabilizing around key support levels, with ETH settling at the highs of the 2022 range, and the next big support level at around the 1500 area.

As a side observation from an otherwise slow week, Bloomberg data-mined an interesting pattern between DOGE and the BTC/Gold ratio, drawing an uncanny similarity over the past 2 years. While, we are not attributing any trading significance or intellectual explanations, we’ll leave it to our readers to draw any interesting inclusion, if any, from the industry’s most famous memecoin.

Finally, despite the recent pullback, we still see the year as a breakout year for the digital assets industry overall, with easy regulatory scrutiny, legislative optimism, and continued mainstream adoption. None of this is more prevalent with the recently announced M&A deals from a couple of US crypto giants, namely with Kraken acquiring NinjaTrader for $1.5bln to break into the TradFi futures space, and Coinbase being in acquisition talks with Deribit, crypto’s dominant option exchange.

We are confident that we are arriving at the inflection point of this growth journey, with crypto becoming a major asset class for mainstream investors. The development of crypto options trading, industry clearing, new stablecoin rails, and interest rate curves should proliferate in the foreseeable future, backed by a new wave of institutional players and expertise that should elevate the industry to new heights. LFG!